That time again to grab those spreadsheets and bank accounts and start calculating!! Gotta know where you been to know where you’re going!

And you don’t have to be any Warren Buffett to still live a good life ;)

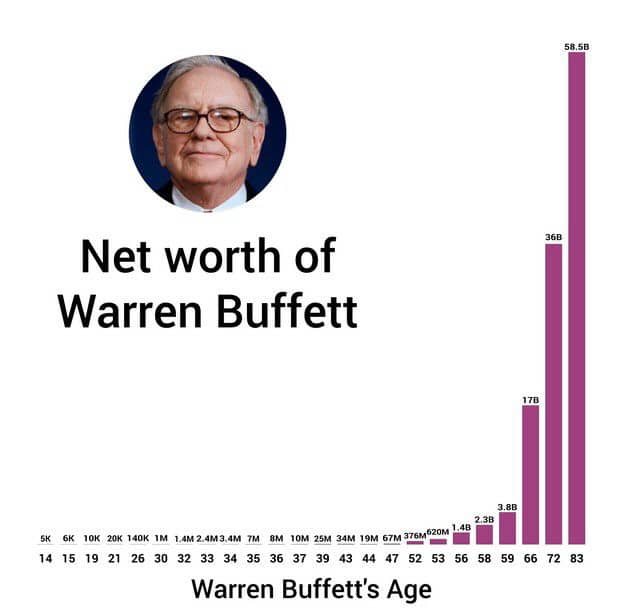

Although I get blown away every damn time I come across this chart – jeez!!

That’s some compounding!!! But look how long it took to REALLY get going there – a solid 40 years or so… So def. don’t get too hard on yourself if you’re just starting out with this stuff – it takes time! And fortunately none of us needs $58.5 billion to feel like we’ve “made it” :)

In fact, for me right now that number is only $1,659.4 – the amount it took for us to hit a new Net Worth high this month – woo! The market was making it hard for everyone the past few months, but as of May we got back to our January numbers plus a little extra on top giving us a new milestone… (Though we *did* throw in an extra $20,000 or so within that time frame as well – d’oh):

- Apr: $818,204.91 (+$16,000 – Tax refund)

- Mar: $801,707.30 (-$10,000)

- Feb: $811,570.54 (-$29,000 – Markets crash)

- Jan: $840,243.99 (+$37,000 – Markets up)

Just more proof to keep sticking with it though! Some months are up, and some are down, but ultimately everything trends upwards the more you continue to save and pay attention to things. And really it all starts with *tracking* your finances so you can see these advancements.

Some might even say it’s just as important as budgeting?! ;)

Here’s how our money broke down this month:

[These reports are shared every month to keep things transparent and start great conversations around money in our lives… Something we’re not so great at in the *real world*. By putting this stuff out in the open my hope is that we can all learn and grow from it, but more importantly that it helps MOTIVATE everyone to keep going and know that it doesn’t take much to get the seed planted! Just a little time, patience, and some good ol’ fashion hustle :) So without further adieu, here’s Net Worth Report #125…]

CASH SAVINGS (+$2,826.39): Always a good month when you bring in more than you spend! But I’ll save the celebrating until we weather through the current Baby Storm as it sure doesn’t ADD any money to your lives, haha… Unless places start accepting cuteness in lieu of cash?

SPAVINGS FUND! (+$103.19): Another nice bump here, courtesy of not going out and shopping much with said baby, as well as continued savings from nixing HBO and cheaper internet options from our move the other month… I also worked hard picking up pennies off the street, some more so than others!

(Yup, that’s asphalt… #NoPennyLeftBehind)

THRIFT SAVINGS PLAN (TSP) (+$646.23): My wife’s retirement account continues to go up with each paycheck! Another great example of compound savings over time – and in this case only around two years since she started working again… We have her invested 100% in the “L 2040” Lifecycle Fund, for those familiar with these gov’t plans… (she’s a bit more conservative than I and likes to be diversified more)

BROKERAGE (+$1,768.43): Only two months in and our $50k deposit continues to make dividends! Quite literally! You can read more about this new account of ours in last month’s report, but basically I wanted to finally diversify our *types* of accounts more and was ready to move a lot of our cash savings out so it can be more productive. And since we had yet to have a normal *taxable* brokerage account in the mix vs retirement accounts, we decided it made the most sense. All invested in VTSAX, of course ;)

ROTH IRAs (+$3,701.35): A nice little uptick here as well, courtesy of the markets just doing their thing as we haven’t been able to add extra in here for quite some time… (made too much last year to contribute which you can’t complain about!)

SEP IRA (+$14,933.89): This account we *did* pump up two months ago, but the earnings this month are strictly from the markets doing well this round… And it really is SO CRAZY to think about as we literally didn’t move a finger at all – in fact, I didn’t even check the market *once* with all the baby hubbub, yet we still “earned” $15,000 just like that! That’s passive income at its finest, right there… And all it takes is getting that ball rolling, *and then not touching any of it!*

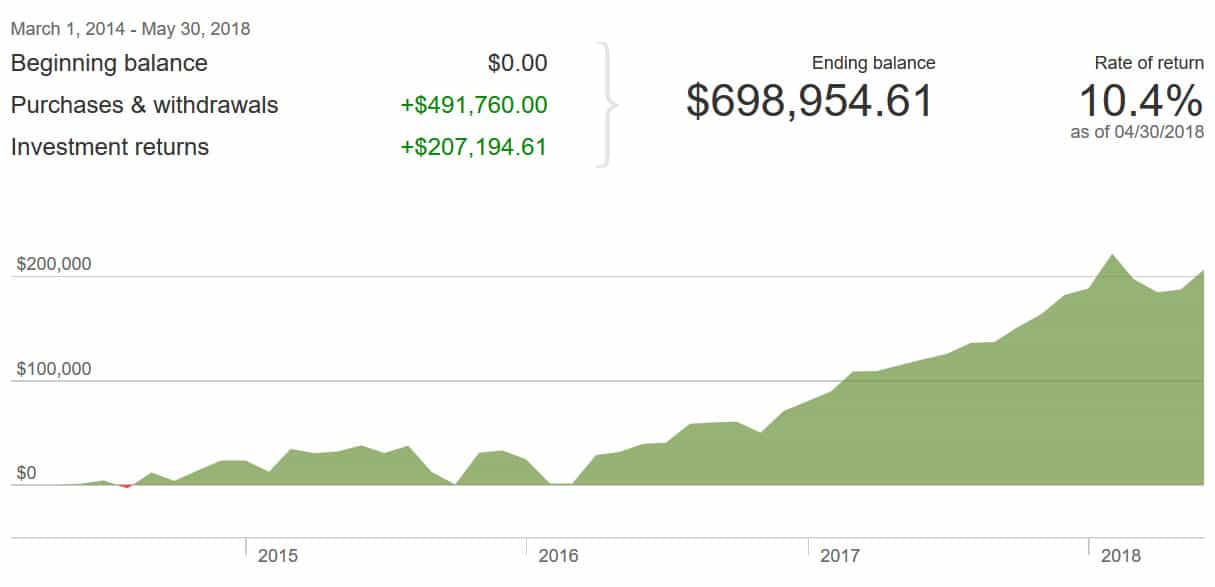

Here’s a screenshot of our investments since moving to Vanguard four years ago:

CAR VALUES (-$281.00): The only category you can’t get mad about losing, haha… It’s supposed to go down! And if you don’t have any car payments it’s even harder to be bothered by it ;)

Here are the values of our two cars presently, via Kelly Blue Book:

- Lexus RX350: $8,859.00

- Toyota Corolla: $2,789.00

Total change in net worth this month: +$23,698.48

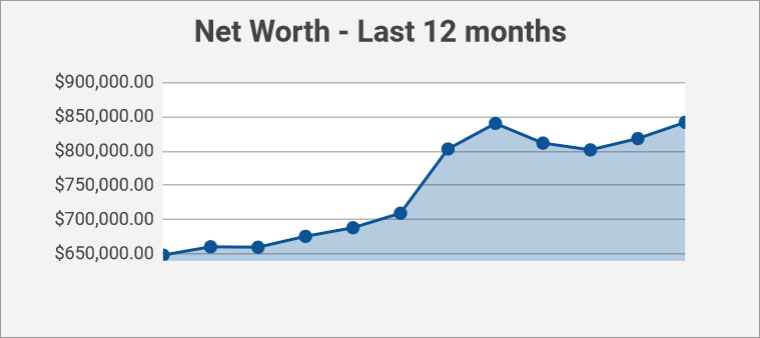

And then here’s a snapshot of just the past twelve months to give you a better overall picture. It doesn’t always go up, no matter what you do!

Lastly, baby net worths…. Although now I need to add in a new one!

(For those interested, the 529s are from the state of Virginia and are invested in their “Aggressive Growth” portfolio option. Which “maintains a target asset allocation of 80% equity, 20% fixed income. This target asset allocation is comprised of the following Asset Classes and Funds: 48% domestic equity, managed by The Vanguard Group, Inc.; 32% international equity, managed by The Vanguard Group, Inc.; 14% market fixed income, managed by The Vanguard Group, Inc.; and 6% international fixed income, managed by The Vanguard Group, Inc.” Yeah Vanguard!!)

And that’s May! Anyone else reach a personal high? Anyone hit early retirement? :)

Our 401k Millionaire friend Fritz from The Retirement Manifesto just did, and is probably sitting in a jacuzzi somewhere right now pouring champagne all over his face! And really, isn’t that what it’s all about??? ;)

Make sure to pop over and give him a hearty congrats… You’ll also love his announcement and parting thoughts: 6 Lessons Learned During 33 Years In Corporate America

‘Til next time, friends! Keep those guards up and wallets down!

It’ll all be reflected in next month’s net worth report ;)

![]()

(I’m skipping the “life” update here as you already know what’s going on in our world… BABY EXPLOSION!!!)

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Very cool, sounds like a good month! We just hit a high net worth amount this month as well, however that is largely due to me finally doing some actual research to see what our current home values are and make adjustments to those values. Coming up on hitting 1/3 of a million in quarter 3. That Warren Buffet chart is amazing, is it inflation adjusted? either way it certainly shows the magic of compounding and the value of starting early.

I’m not sure if it’s adjusted for inflation, but I hope so or else I’m really never catching up to him ;)

Do you know that Simpson scene where Homer is in the hospital playing with the bed dial and going “bed goes up, bed goes down, bed goes up, bed goes down” – that’s basically the master background voiceover reading posts like these.

https://www.youtube.com/watch?v=0TboDmLD0ZU

Yes! This is a perfect match!

haha… good job, guys.

Yours has always been the most comprehensive net worth report that I’ve ever read. Not to mention most frequent. I feel guilty sharing mine only once a year :)

You can email it over to me every month if you’d like :) I love seeing people’s money!

Another good month – that SEP IRA continues to rock it…snowballing at its finest. And the account / allocation is simple but extremely effective – good stuff. – Mike

We technically have hit a record high every quarter since I started tracking a few years ago. That streak will be broken once our contributions make up a smaller percentage and the market takes full control

Great month, have fun setting up another 529!

Oh yeah, I remember contributing a lot every month and not seeing any effect during the market/housing crisis of 07/08 haha… Then fortunately it had a helluva comeback and went in the other direction :)

Congrats on the great net worth increase! I’m so excited to see your net worth reaching closer to $1M. Definitely inspirational for a lot of people, including me.

Having a baby makes your life more hectic for sure. It’s not to mention other kids we might have. Hubby and I will be in the same boat on three months.

I want pictures, please!!

Yes, May is a great month indeed. Last quarter, my net worth took it on the chin and it was down about $35K. The market decided to pull me back up and dust off the losses and I am back on track again and reach a new milestone. Passive income rules.

Looks like a great month! Looks like our May’s net worth will be an all-time high for us. Looking forward to Baby Dime’s debut on the net worth updates next month. His he buying stock his socks?

Haha… he should, he goes through a lot of them :)

We hit a high- 1.18 million. And to think I had a negative net worth only 3-4 years ago. Reading lots of personal finance sites, setting things in motion, having a high paying job, and then a good insurance payout (hello Tubbs Wild Fire) all led to this dramatic bump in net worth.

Much like you, we are currently renting which helps with having money in the bank (or VTSAX). I dropped a bunch of money into the market in January but was happy to see we were back to even this month.

As for the future, I hope to see another $300-500 K bump by next April if all goes according to plan with building and selling my burned down home. We will see what happens!

WOWWWWW!! That’s all kinds of incredible!

Nice job last month! The market didn’t move that much so it’s nice that you had some gains. We’re pretty much flat. We replaced our HVAC and that set us back a bit. Our net worth still increased so it’s all good for now.

I guess this makes me 34 years old on the “Buffet Net Worth Scale”. If I can match his compounding, I’ll be billionaire in 10 years, and match his current net worth when I’m 109! Something to look forward to! I need to start taking more vitamins.

Yeah you do! Haha…

This makes me wish my readers wanted me to share our actual numbers and not just a monthly report on our doings!

We did hit a new high this month but I’m not reading anything into it because I am thinking ahead long term to a year, five years and ten years down the road and where we want to be with our total assets (how much for retirement again??) and debts (begone!). These monthly reports are great for keeping my mentality on the right track but I don’t worry overmuch whether it’s up or down a bit this month, as long as the year to year trends are generally going up :)

That’s interesting your audience doesn’t want real #’s – I’d think that puts things in better perspective? Although I’ll admit it is getting tougher for me to keep doing it the higher it gets… Not that I mind sharing, but just always hate the thought of it possibly coming across as “boasting” vs “disclosing” :( My wife says no more when we cross $1,000,000, but we’ll see :) First we gotta cross it! Haha…

Nice on the record high again after a few months of market craziness! Also hit a record high myself but just missed crossing six figures! Oh well, as long as the markets don’t go way down I should be hitting it next month :)

Love seeing you inching closer to the million!

That first $100,000 is the hardest ;)

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

I love that picture of Warren Buffett’s amazing compounding too! It is INCREDIBLE. I want to make it my Whatsapp picture haha.

Congrats on the positive increase (and a big one too!). I had a dip in February and March too (for the first time in 6 months) and am happy that the past two months have been in the positive territory.

Great month, even with a new baby. I agree that they certainly don’t add any money, and it seems to only get more expensive the older they get. Who keeps saying babies are super expensive when teens are eating us out of house and home?

J –

NICE! I am getting closer and closer to the $500K mark, I can taste it. Looking forward to this big month of dividends for me, which will continue to fuel my investment accounts. LETS GO!!!!!!

-Lanny

I want an email as soon as you cross it, sir!

Thanks for sharing J.

Mine is nowhere near yours but I’m actually pumped to see that hitting a million is possible. I have about 18k saved for retirement, but I’m not bummed at all.

We will definitely pop champaign once you hit millionaire status.

Hey – gotta cross $18,000 before $1,000,000 :) We were all there once!

So you have a ton of boys and I have a ton of girls, the world is balanced my friend. Good job on the net worth increase. I think i hit a milestone every month, bu then reality sits in that im not buffett. So with every kid the cent amount goes up, cant wait to meet baby Quarter and baby silver dollar? Haha.

My wife says “NO” :)

first time poster! here’s some sharing from me, and also seeking input.

net worth -161,016 (yes, that’s negative, doesn’t include the home i currently own or my car, etc)

checking 11,999

401k 13,001

Roth 12,016 (invested in vtsax)

credit card 1,786 (pay full statement amount every month, never pay fees. double cash back card from citi)

car loan 11,910 (2.84% interest)

student loan 9,170 (3% interest)

65k/year salary

the real issue for me here is-i’m selling my house and closing is at the end of this month. I’m estimated to pocket a little over 80k after the sale. i’m moving in with the girlfriend and will be paying rent (if you want to call it that), so my monthly expenses will drop from about 2800 per month to about 2300 per month.

my plans are to immediately contribute 5500 to 2018 roth (maxed 2017 with my tax refund)

figure the exact percentage i need to max my 401k on my last pay period of the year (currently contributing 10%, so this will probably mean contributing 50% which means setting aside about 15k for those purposes)

possibly holding back 5500 for 2019 roth on january 1, 2019

i like to keep 10k in my checking as emergency fund

i do not intend on paying my debts off early, with those interest rates i’d end up “saving” about 3 grand over the next 7ish years…who cares?

so this leaves me with 54k to play with…i have no kids, don’t plan on it (i the youngest child, i have 4 nieces and a nephew who i love, but i’m too selfish for kids), i’m 37, i hope the Caps win tonight, i plan on buying a new phone (1k) and new grill (500?) as my only rewards to myself for being a good human…

i’ve read all about dollar cost averaging vs investing in a lump sum and how dollar cost averaging loses almost every time…if i were to DCA (into vtsax, of course, i know where i am right now), i’d likely do so where i’d invest something like 9k every month, or 4500 every two weeks until the end of the year until my checking bottoms at 10k, then once per month in perpetuity i’d throw more into the brokerage account to end up at 10k again

please tell me how i’m right (our president is insane and could start a war anytime), or how i’m wrong (the markets are doing so well, hop in), what i really should be doing, how excited you are about the Caps tonight, and please don’t be shy with insults, i used to work in TV, i’m used to getting yelled at

Haha… all I know is that I very much enjoyed reading this (AND GO CAPS!!!)

I’d make sure you don’t owe any taxes on that $80 grand you’re about to profit from, but outside of that i think it’s great you’re pre-planning everything and trying to optimize the results. I’d personally just invest all the extra money in one lump sum vs dollar cost averaging, but maybe DCA’ing is more exciting to you or extends the good feelings?, in which case i say run with it. You can always decide to dump the rest in any day if you don’t want to wait anymore. I also agree on splurging a little because if you can’t with a windfall like that, when can you?? It’s no fun just saving and investing your whole life…

so yeah man, i hope the sale all goes smoothly and be sure to come back here and update us over time… sounds like fun times ahead!

I just recently started listening to all these podcasts on FI and came across your interview with Mad Fientist. Great interview by the way! You are hilarious! =)

Quick question on these net worth numbers. Are these post tax or pre tax numbers? What I mean by that is, do you remove the effect of federal/state income tax assuming that the gov’t will be taking some portion of any capital gains? For example, let’s assume I have a stock portfolio that is $100K but the cost basis is only $10K (obviously a very hypothetical scenario). On the $90K, the gov’t is going to take their share of the pie (assume combined fed/state income tax rate of 20%, so $18K). When I think about my net worth, should I think of my net worth as $82K? Which would then be the number that I use to base the SWR on?

Your thoughts on this would be greatly appreciated!

Thanks!

These updates don’t factor in tax stuff at all – I mainly use it as an overall “snapshot” of my money to keep myself motivated :) I know people who do include it in their net worths though, although usually I see it in “retirement” or “cash flow” spreadsheets/calculations instead. Just depends on what you’re going for :) (And even better if you DO keep multiple spreadsheets for each area you’re tracking! The more angles you look at this stuff the better!)

We also hit an all-time high this month, which is always super exciting :) I also have suped up our spreadsheet a bit to add a couple of things I’ve been wondering about: years of retirement funded (investments/retirement budget estimate) and a straight line projection of my partner’s retirement date based on our actual rate of change in investments over the time I’ve been tracking them (~ 2.5 years).

I’ve also been gradually rebalancing, and today pulled the trigger on another change in one of my retirement accounts. Gulp – that always makes me so nervous!

That is a seriously adorable baby you and your wife have made. I hope he is and continues to be “Basic Baby” (healthy, happy, with typical needs and development).

Thanks Rae :)

And congrats on your guys’ new highs as well! Love that you’re calculating it from all different angles!

I’ve been looking at FI stuff for about 3 quarters now, and budgets are sexy has popped up in a lot of places. I assumed you were one of those bloggers that was already worth multiple millions.

That being said what really made me comment was that your wife is federal employee which I noticed when I saw TSP section of your table. You mentioned she is in the L2040 fund, because she is more conservative and wants to be diversified more.

I was in the L2040 for several year (up until like October 2017). Then I realized I was missing out on a lot of potential. The L2040 is currently 28% Bonds/Government Securities so wouldn’t this be less diversified than having more of that money spread out through hundreds and thousands of different companies (i.e. the “C Fund” and “S fund”). I’m currently gambling it up using a seasonal strategy, but I will probably fall back to 80% “C” and 20% “S” within the next year. If your wife wants to have some assets not in equities I’d push for putting that amount strictly in the “G Fund” and skipping the “F Fund” altogether. I also skip the “I Fund” for the same reason a lot of people just do a US total stock market index (a lot of big US companies do business overseas resulting in international exposure) especially since the “I Fund” is only developed market.

Hey, thanks Kit! Very nice to e-meet you! Def. not worth millions over here, but one day?! :) Going over to check out your blog now – love reading new ones!