Before getting to the net worth update, 2 quick things to share… The first is a comment I received last month from a reader, Max S.:

“Good Morning Joel.. I finally did my first net worth report. After all that time hearing JMoney telling us readers to track our net worth I just never got around to it. Seeing your first net worth report motivated me to do my first report. Thanks for the push.

Can you tell JMoney I finally got started tracking my net worth so he can stop all that nagging about it now. jk :)”

Although J Money may have transformed the financial lives of millions of people out there, it’s nice to know that I at least motivated 1 person he didn’t reach! Haha. Jokes aside, the reason I’m sharing Max’s note is because maybe it’ll encourage any other net worth virgins out there to track for the very first time. 🎵💃🎵. It truly only takes a few minutes to do and it’s one of the best tools along your journey to FI!

The other thing worth mentioning is getting an “accountabilibuddy.” If you are finding it hard to stay on track each month, I recommend finding a buddy or a partner you know and trust to help! You don’t have to share every specific detail, it’s more to make sure each other is doing their FIRE homework regularly!

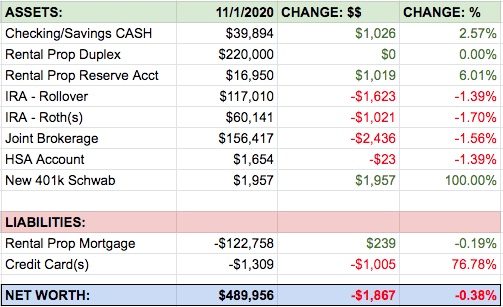

Net Worth Update November 1, 2020:

Here’s the account summary for me and my wife, as well as growth shown in dollars and percentages for each asset:

Well, shit. 😩

Our net worth went down a few grand. Not the greatest start to tracking this stuff publicly, but we have to show both the goods and the bads in the wealth building process!

Here’s What Happened in October…

First off, there was a crap ton of volatility. The stock market does weird stuff leading up to a presidential election (and will continue to do weird stuff afterwards!) – more on that below.

For the first ~23 days of October we had some pretty killer growth. In fact, all our assets listed above topped the $500k mark for a little while! Woohoo! But then, things started to tank pretty quickly. The worst day was October 28th where our beloved VTI fund dropped a full 3.31%. :(

As the saying goes, “the market giveth, and the market taketh away.”

This doesn’t bother me all too much, though. The larger an investment portfolio, the less overall control we have on performance.

Asset Growth (and Shrinkage):

Checking & Savings Accounts: $39,894 (+$1,026): A little increase here, but we have about $1k in new debt added to our credit cards that is due in November. Our goal with this cash balance is to reduce it slowly over time and siphon some pre-tax income into my new 401k plan. This balance acts as our emergency fund, and includes the random churning bank accounts we currently have open.

Rental Property, and Reserve Account: $236,950 (+$1,019): This past month we collected $1975 in total rent, and had -$956 in expenses ($294 prop mgmt & maintenance + $662 mortgage pmt). Keep in mind taxes/insurance are *not* included in my mtg payment, I pay them annually in a lump sum. So although it seems like this rental might make $1000 in cash flow each month, it takes a massive drop when my ridiculous taxes are due in January. This year the tax bill is $5,185, even after my appeal.

IRA – Rollover: $117,010 (-$1,623): Kind of sucks when things are in the red, but that’s just the way it is sometimes. Back in July I pegged this IRA against the rental property to track which one will grow at a faster rate (they were both worth $109k at the time). This account is still ahead by about $3k, but if it has another negative month like this the rental asset will catch up and be worth more! :)

IRA – Roths: $60,141 (-$1,021): Same story as above… account value dropping a bit with the overall stock market. Since these are both long term retirement accounts, I’m just trusting that over the long haul we will have more green months than red months!

Joint Brokerage Account: $156,417 (-$2,436): The reason this account is moving at a slightly different rate than the IRAs is because a) we have some bonds in here which grow at a slower but more steady rate, and also a few individual stocks. However the majority is all in broad, low cost index funds. VTI mostly!

HSA: $1,654 (-$23): My plan *was* to increase this account immediately with $3,550 (the max contribution for 2020), but, I just learned that my employer will likely be changing my benefits, again! (and not in a good way 😔 ). Since I’m only enrolled in a HDHP for 3 months this year (Oct-Dec 2020), a max contribution would require me to stay in a HDHP for the entirety of next year also. To play it safe I may just prorate my contribution for 2020, and there’s still a few months to figure this out before year end. If prorated, I think I can put in $887 safely ($3,550 / 12 x 3), right?

New 401(k) at work: $1,957 (+$1,957): Woohoo, this is the first month adding to my new 401k plan! But, there are 2 sucky things to mention: 1) My contributions to this account in October were actually $2,044, so I lost about $87 having this money invested. Not horrible though, because I saved more than that probably on income tax. And 2) I mentioned above that my company benefits will likely change, or be taken away – and this 401k plan is part of what will be killed. Oh well, anything contributed here can always be rolled over to an IRA, converted to Roth, or put into another plan down the line if one is offered to me.

Breakdown of Liabilities:

Rental Property Mortgage: -$122,758 (+$239): There’s nothing sweeter than watching tenants pay down your property loan each month. It’s a very slow process — 30 years to be exact! — but the speed doesn’t matter… Progress is progress!

Credit Card Balances: -$1,309 (-$1,005): We have all of our credit cards set to auto-pay the full balance on the due date. This means we typically have a rolling credit debt of a couple thousand dollars at any given time.

My wife and I have no other consumer debt at this time!

Other Happenings This Past Month:

My wife got a new exercise bike! She says it’s her early Christmas present, but I feel like by the time Christmas rolls around she’ll “forget” she said that and will want another present then also. (Totally fine with me, because I plan to pull the same trick!). She picked up this bad boy off Craigslist for $200 – it was only used once by someone who bought it last month and is moving to a smaller apartment.

Another money win… We switched to AT&T Fiber internet! Not only do we get 960Mbps download speed for $20 less per month than our old Spectrum service, they also gave us a $200 Visa Gift Card signup bonus for switching! That’s a $440 difference this next 12 months. Woohoo!

Another little unexpected bonus… We got a $72 check from Apple as part of a class action settlement for some power button issue on the iphone 4 about 9 years ago. Were any of you guys a part of this claim and did you get the payout check too??

Future Volatility & Unknowns

I’ve seen a bunch of news articles lately about how the stock market behaves strangely before, during, and after presidential elections. Experts have their opinions, predictions, forecasts, prophecies, prognostics, indices, and some people even use the Big Mac Index to guess future stock market growth!

Although rollercoaster markets concern me, they don’t worry me. They don’t change my overall gameplan. Emotions aside, my wife and I will keep our money invested through thick and thin.

We are in it for the long haul – and I hope you guys are too!

How were your updates the past month? Share your milestones and juicy details in the comments — which as a reminder is a judgement free zone!

Have a great weekend! (And for you hopeless romantics out there – Today is exactly 100 days until Valentine’s Day!)

– Joel

Get blog posts automatically emailed to you!

Joel,

Congrats on the net worth! Sounds like you and your wife really are working toward that long-term goal – and you’re sticking to your plan.

I hear you when you say that you’re worried about potential market volatility decreasing your overall net worth. I am too. However, it’s always good to stick to your original investment strategy and not pull out from the market.

Consistency typically wins the long-term game.

Good luck – and keep it up!

The Millennial Money Woman

Thanks dude. We’re in it for the long haul for sure. :)

That exercise bike looks pretty sweet, great find! I prefer riding outside but here in Ohio I’m not quite brave enough to ride when there is snow/slush/ice around, so end up putting the bike away for a few months. Our rec center lets us pay a month at a time without a contract so I might do that December-February. March-November I’d rather run or bike outside.

We bought a truck last month, so net worth took a hit, but my husband’s 2005 Dodge Dakota is approaching 197k miles and rather rusted. We found a 2018 Ram for a decent price with only 34k miles so we should have it another 10-15 years. We did get a loan, but the interest rate is only slightly higher than our mortgage.

I’m still driving my 2001 Honda Civic with 198k miles, hoping to get it to 250k and at that point we should have the truck close to paid off.

Congrats on the truck! And happy 200k birthday to the Civic soon! My wife used to ride every day to work, but since working from home she’s missing the commute. Spin classes are a bit more fun for her. She hooks up her phone to a loud speaker and blasts the music so loud people can hear it a few blocks away probably :)

Thanks! I almost feel like I should do something special for Ciera (the Civic) when she gets to 200k but then I remember that cars don’t have feelings. Haha. She is due for an oil change though. I bought this car with cash in 2017 for $1800 with 138k miles. I did need to replace the transmission with a salvage yard transmission in 2018 when my transmission pump went, but I’ve definitely gotten my money’s worth!

I loved biking to work when I lived closer, now that I’m further away it’s not really a feasible option, unfortunately. I’ve never tried spin classes but I’ve heard good things! Sounds like fun!

Maybe a tiny air freshener or something would be a good gift :)

Love the breakdown, and the bike! For 1/10th of the price of a Peleton… I echo Max’s sentiment, seeing a new net worth report on Budgets Are Sexy was the push I needed to publish mine. Keep up the great work–even when the numbers go the wrong way!

I just love the transparency! Thank you for these posts they are motivating for sure. I’m sure you’ll make up the loss next month. I laughed out loud at you wife’s early Christmas present and probable forgetting by the time Christmas comes. LOL. Just start planning, Joel.

Maybe when Christmas rolls around I’ll go out to the garage and wrap up the bike in wrapping paper. That’ll jog her memory. :)

Actually, in all seriousness, my wife can have whatever she wants (because she usually wants nothing!). I was glad to hear she wanted to spend money on herself for a bike – this is a rare request!

Cheers IF! I just checked your post out – congrats!

My wife got a trainer years ago for her bike and rides that thing incessantly in the winter — she’ll put on an episode of Brooklyn 99 and just hammer. Now that I run regularly, I’m getting worried about what I’ll do when it’s icy out; we don’t have room for a dreadmill. Maybe I’ll just let myself sleep in as needed instead. :D

J$ got me on that net worth train around 2016 and I still use a heavily-modified version of his snapshot spreadsheet. We only keep historical records as of the first of each year, rather than monthly, but we’re up more than $125k since January 1. Hell, it’s up $8k OVERNIGHT from just yesterday. Stock market’s a weird thing.

That’s awesome Adam! 125k gain aint no joke. I keep historical records but in a slim format on a separate spreadsheet tab. It’s fun to go back every now and then to look how far we’ve come :)

Way to get that person to finally TAKE ACTION!!!

Perhaps you need to start a Net Worth Tracker for the site too now since you’re starting to do them :) Mine is old news!

I better get a few under my belt first! Yours is still a wicked source of motivation for everyone!

Hm, one thing that I don’t really get. Why so often I see FI related with strict frugality…. Since my early 20s, I had one principle – always try to earn more money, and the increase in your earnings to be higher than the increase of your spending. Period. That leads to a) you enjoy spending without any guilt and b) despite the increased spending you save and invest in passive income even more.

Ever increasing spending is OK, as soon as your earnings increase not only match the spending increase, but also beats it.

I know some people will say that money doesn’t buy happiness. I agree that money ALONE can’t buy happiness, but they can contribute a lot!

Hey Peter! I hear ya… There are some extremists within the FI crowd that take frugality to levels that seem really uncomfortable. It confuses me too.

But for the most part, I think it’s more about sensible and economical spending. Spending less on things that don’t provide value, in order to buy more of the things that do provide value.

Personally, I’d be happy to increase my spending in every area of my budget… So long as I get proportionate increased value or happiness for the additional dollars. If there is no added value, or diminishing returns, I don’t wanna more than I need to, regardless of my income or net worth.

Also – another quick note. Some of my friends have embraced extreme frugality recently. But they are either in heavy debt or need to make radical changes to their lifestyle. Everyone’s situation is different – so sometimes I encourage stricter frugality and other times I don’t understand why.

Wow, very brave of you to post your balance sheet for all the world to see. Keep up the good work!

Yep – just tryna put my money where my mouth is! If I succeed, people will learn from it. If I fail, people will learn from it. Either way, it’s helps others!

Ah, I see you already thought through the one year testing period : )

Nice work, are they really taking HDHP/HSA away altogether as an option? That’s a huge bummer!

Max

I think they are taking away ALL benefits. Moving me completely back to a contractor position. The change happens March 31 apparently. I’ll know more soon.

I could go out and get my own HDHP. But they’re still very expensive!