We sold another rental property! Woohoo!! 🥳🎉🍻🙌

That’s 2 down, 2 to go. This is part of my long-term mission to reduce physical assets, lessen management duties, and move everything to more passive income streams. (Here are more details on why we’re selling a few rentals if you’re interested.)

The proceeds from this sale were about $50k. And while I won’t go into the exact breakdown of profits I made from this private partnership, I’ll just say that the killer return we made on this deal almost made up for the killer losses we sustained on the prior one. :)

Once the sale closed, I dumped the $50k cash straight into Vanguard Total Stock Market Index Fund (VTI) in our taxable brokerage account. This is its new forever home! So that’s the reason for the big bump this month.

Here are the other net worth updates and June happenings …

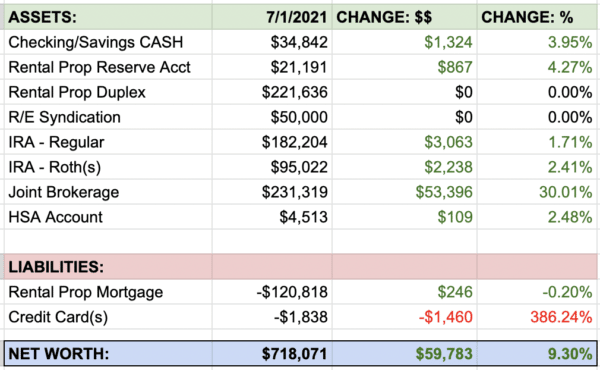

Net Worth as of July 1, 2021: $718,071 (+$59,783)

Account summary with percentage increases/decreases:

Sweet! Apart from the $50k we brought in from our real estate partnership, our existing stuff grew an additional ~$9k this month. Here are the full breakdowns and deets.

Weddings, gifts, travel, and a class action WIN!

June was a fun month, both in spending and in earnings.

- Wedding costs ($670): One of my good friends got married! Since I was part of the wedding, I had to rent a suit ($270) and my wife and I also gave them $400 cash as a gift.

Pic of me and the happy couple :) Here’s a script of my officiant speech if you’re interested. Nobody noticed me crying during the ceremony … because the groom was blubbering like a baby and all eyes were on him!

- Birthdays, Fathers Day, etc (~$300): My wise Dad turned 60 this past month! And since he’ll be running a marathon later this year, we sprung for a new pair of Asics Kayanos as a birthday gift! Other gift spending this month was for Fathers Day and kids bday parties :)

- FinCon Tickets/Accom (~$650): It’s official, I’m headed to FinCon in Austin in September. Flights were free (still got a ton of SW points to spare) so this $650 was for the conference ticket and my portion of the AirBnB rental!

- Class Action Lawsuit WIN (+$575): My wife participated in a 10-year-long class action lawsuit against Carribean Cruise Lines and the case has finally settled. We received a massive unexpected check in the mail this month. Woohoo!

- More “afterhours” work (+$800): My employer continues to offer me sporadic editing/creative work on some other websites they own. I find it fun (and lucrative!) so I’ve been doing this in some spare hours.

Detailed Account Breakdown

Cash Accounts: $34,842 (+$1,324): My wife is officially on school holidays, so no paychecks from school for July and half of August. My income can cover some of our monthly expenses through the summer, with any shortfall coming out of our cash bucket.

(BTW, does anyone follow Early Retirement Now’s posts on how emergency funds are useless? Since reading his last post I’m starting to think much differently about our cash position and questioning why we have so much cash sitting around. More to come on this.)

Rental Property + Reserve Account: $242,827 (+$867): Here is how the property made us money last month:

$1,975 — Incoming rent

(-$140) — Property mgmt fees

(-$305) — Maintenance, repairs, lawn care

(-$663) — Mortgage principal+interest

$867 — Total account gain this month

Another cool thing about this rental is that it cost me ZERO man hours to manage this month. I still have a pending roof replacement, but we’re holding off on that for a bit until the roofing companies are less busy.

Real Estate Syndication: $50,000: We got an awesome update this past month… This property is effectively 100% occupied and collecting rents well above initial projections. The partnership will be paying all investors a 7% annualized return for the first quarter of ownership (paid at some point in July) which means $875 for my cut. ($50,000 x 7% / 4 quarters = $875)

IRA – Rollover: $182,204 (+$3,063): Nothing new added here. This $3k of gains is all due to market growth. This IRA is invested 100% in a total stock market index fund.

IRA – Roths: $95,022 (+$2,238): Same with these Roth accounts. Nothing new was added and growth was due solely to the market. I’d love to figure out a way to contribute more to these Roths throughout the year (in addition to the $6k regular contribution). I’ve been reading about Solo *Roth* 401k’s and this may be an option to eventually moving more money here.

Joint Brokerage Account: $231,319 (+$53,396): I think we’ll top our goal of reaching $250k in this account by the end of 2021 (assuming the market doesn’t shit the bed). We’ll keep adding to this account as we sell the remaining rentals and will push spare cash here too if we can!

HSA: $4,513 (+$109): Small growth here, but tax-efficient nonetheless! I wish there were backdoor ways to get more money into HSA accounts! Anybody know any sneaky methods?

Breakdown of Liabilities

Rental Property Mortgage: -$120,818 (+$246): Last month, my wife and I passed 6 years of ownership on this rental property. Our beginning mortgage balance was $136,500… and by the end of this year we’ll be under $120k. Sweet! Slow and steady paydown wins the race.

Credit Card Balances: -$1,838 (-$1,460): Went a little crazy this month on the credit cards with gifts and expenses, etc. This will be paid off in full shortly, as we do every month.

We have no other consumer debt at this time. 😎

What did you guys get up to last month? Cheers to a great month ahead!

Happy Friday!

– Joel

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Congratulations on selling the rental property! Man, I bet that’s a weight off your mind. You certainly picked a fantastic time to turn real estate into dollars; that brokerage figure looks real good!

I appreciate the link to the uselessness of emergency funds. Ours exists solely for the peace of mind it provides to my wife, in an account she alone maintains. To be fair we’re in the middle of blowing $40k on a roof, exterior painting, and most of a new car — none of which was expected a few months ago — so it’s come in pretty handy; I think we can replenish that inside of a year if we buckle down a bit.

Regarding your HSA. are you and your wife on the same plan? That’d then be a $7200 max contribution for 2021 rather than $3600, yeah? And you probably know but for anyone who doesn’t, don’t forget it’s often worth paying for covered medical stuff out of normal taxed dollars and saving receipts so you can later pull those dollars penalty-free from the HSA after they’ve been invested for a while! Our invested HSA funds total $52k on $32k of contributions and I’m absolutely paying for the small stuff out of pocket to let the market push it higher.

Wicked tip on the HSA – thanks Adam! Yes I’ve heard growing that account as much as possible and hanging onto the receipts is the way to go! We got a really late start with HSA’s, and right now neither my wife or I have a HDHP so we’re not eligable. :(

Congrats on selling the rental property! Love that you are going simple and as passive as possible. This is where I have landed as well on real estate. For me it’s primary residence and REIT ETFs going forward!

Syndications are really cool too! I don’t have any REIT ETFs but love how diversified they are.

Any time you can plunk $50k into VTI I would say that qualifies as a good month! LOVE to keep reading somebody else’s net worth, just not my own haha

Glad you like these :). Hope you had a good month too!

I figured out a small hack for being able to increase your ROTH IRA contribution limit above $6,000 with Schwab.

If you have a ROTH IRA with Schwab and you apply for the investor credit card through AMEX, they will deposit 1.5% cash back directly into your ROTH monthly. This is considered a bank bonus and does not count towards your contribution limits. I reached out to Schwab to verify this.

So the more you spend, the more they will contribute. 1.5% doesn’t equate to a lot of money, but it’s something. Cheers!

WHAT!!?? Are you kidding? I’ve never heard of that hack before!… Have you actually done this? I see Fidelity offer a similar deal with 2% cash back that can be put into your Roth. Are you 100% sure you won’t get screwed at tax time as a “contribution”? This would be amazing if it worked.

Here’s the response from Schwab:

“Thank you for reaching out to Charles Schwab. I’d be happy to assist you with your contribution inquiry!

Per the Retirement team, cash back is consider an award; therefore not viewed as contribution. If you have any questions about the cash back award and how it will affect your taxes, you will need to reach out to your tax advisor..”

I only just recently started after learning about this, but I do trust Schwab fully.

A friend of mine has the Fidelity card, but he says Fidelity counts the 2% as a contribution. Not sure why the 2 brokerages have different rules on this.

Drew

Really interested in how this all works out!

I’ve followed ERN’s emergency fund posts and agree with him. Having money sitting in cash is a waste. Mine is invested in index funds and a few stocks and has been for a couple years. The big test was this pandemic.. At the beginning , when the stock market tanked and I was worried about possibly being laid off, I was thinking I was a fool. But, it turns out, it was a smart move. Even with the huge market drop, the value never dropped below my cost basis – meaning I was always ahead. I wrote about it here: https://roadtoatesla.blogspot.com/2020/05/1-year-post-finale-follow-up.html

Hey Shaun, this is awesome, thanks for sharing. I read your posts and will continue down the rabbit hole with ERN. (Even though my mind is already made up – I think I’m gonna dump $20k from our emergency fund into stocks, keeping 10k in cash.) Cheers for reading and the encouragement.

You’re going to be in Fincon this year?! I hope to meet you in person!!

Congratulations. I can’t imagine what a $50k+ increase in net worth feels like in just a single month.. I hope to do that over months of hard work, let alone a singular month.

Maybe next month, we’ll see a $100k increase? ;)

Yep, I’m FinCon bound, and trying to convince my wifey to join too! Look forward to meeting you, and everyone.

To be fair, the $50k increase came from assets that we already own outside of this personal NW report. Regardless, months (and years) of hard work and saving still needs to happen in order for us to FIRE :). It’s a long journey!