What up money moguls!

Got a new company to share with y’all today, and it’s giving my Digit a run for its money ;) It’s called Acorns, and it’s an app that rounds up your transactions to the nearest $1.00 and drops your spare change into investments. It’s all automatic, and it’s all awesome!

(And yes, if this sounds familiar it’s quite similar to Bank of Horrible America’s Keep The Change program. Only, it *invests* your money instead of saving it, and you don’t have to be connected with B of A (whew). They also help you choose the right portfolio to dump the $$ into which is cool.)

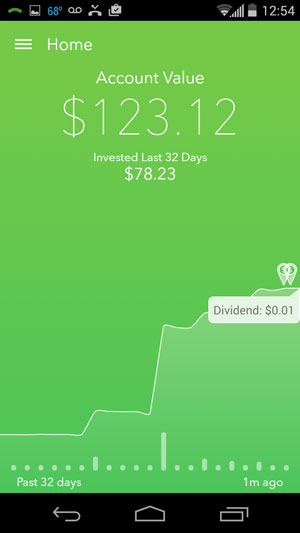

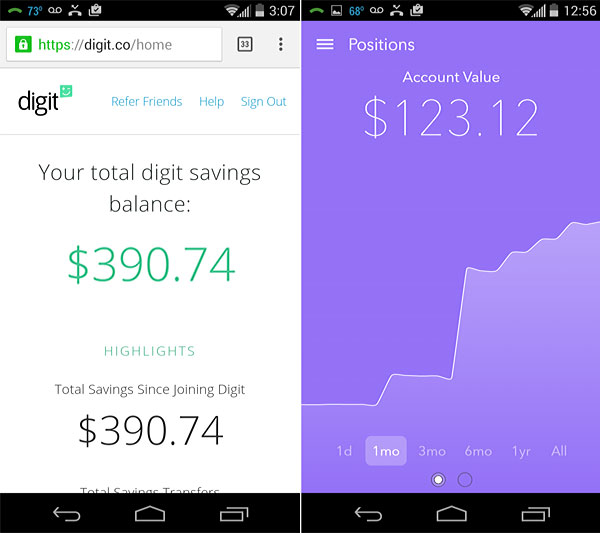

I’ve been secretly using Acorns for a little over a month and a half now (I’m cheating on Digit, shh!), and so far I’ve banked $123.12 of investments:

[Update 1/24/17: Now up to $600.22!!]

Not an amazing amount of money, but hell – it’s mostly from spare change! (Technically only $80’ish is from spare change as I was playing around with their “invest more” feature and dropped in $40 to test things out… And the market then changes things for the better or worse too ;))

I tend to get long winded when I’m super excited about something new – especially money products! – so let me try and hit you with the TL;DR version of why I’m crushing on these guys right now:

- It’s all automatic!

- I barely notice the money being pulled out

- It’s a fun *extra* way to invest on top of the other avenues I’m already doing

- There’s no transaction fees! (Although there is a small monthly fee – see below in “cons”)

- I love checking my account every week to see how high it went

- Most of their portfolios are Vanguard index-based!!

It’s also the very first app to let you create an investment account straight off your phone too. Not that we’re *that* lazy that it’s necessary, haha, but still. Shows you how future-thinking they are at least :)

Here’s how Acorns works in a nut shell (no pun intended):

- You download the app (Update: You can now sign up through their site directly as well)

- You create an account

- You link up a funding account (like your checking)

- You answer some questions about yourself (which helps them recommend a pre-made portfolio)

- You sit back and do nothing :)

So, pretty similar to my beloved Digit, only it *invests* your money instead of *saving* it. Which of course has pros and cons on either side (it has a chance to grow which history shows it will, but you can’t easily just “take it out” like with savings as it’ll trigger tax stuff and what not).

I gotta tell you though, it’s quite awesome to watch my Digit savings go out and then have Acorns investing come in and round up the difference to invest! Haha… A match made in nerd heaven.

You can also tweak the settings to round up to other numbers as well and not just a dollar. And if you’re feeling aggressive, you can always dump in more money in one-time chunks or just attach more financial accounts to your Acorns one too. I have both our “house” checking and our “house” credit card attached so it’ll round up from two areas and not just one like with checking only.

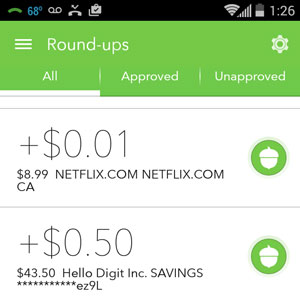

Oh, and in case you’re wondering, they don’t actually invest $0.38 here and $0.05 there – what they do is wait until you’ve hit $5.00 in rounded up amounts and THEN they invest your money. Which makes sense – this cuts down the amount of transactions being sent all over the place! And all this money comes directly out of your main “funding” account you’ve attached to your account (for me, it’s our “house” checking), and not the others if you’ve attached a handful of them – if that makes sense?

(For example, if they’re rounding up your credit card transactions they’re not gonna pull the $$ to invest off there – they’ll pull it from your linked checking account so you never have to worry about anything funky happening. You just have to make sure you have the $5.00 in your checking account ‘cuz unlike Digit, they won’t reimburse you if you overdraft!)

Of course, no Acorns review would be complete without covering the possible downsides of using the app.

The cons to using Acorns:

- If you don’t do a lot of transactions, or set up automatic roundups, you’re not going to invest much. That’s probably good over all (less transactions = less money going out! ;)) but in this scenario you’ll invest less too. Unless you increase the threshold or attach additional accounts to track transactions from.

- Their customer service isn’t the best. I had to tweet them to get a response faster (I lost patience after 3 days of sending them a question via email), but once we were interacting they were super fast and helpful – for what that’s worth…

- As of 5/28/22, they offer two pricing options: A “Personal” plan @ $3/mo which gives you all-in-one investment, retirement, and checking perks, plus a metal debit card, bonus investments and money advice, and then a “Family” plan @ $5/mo which gets you investment accounts for kids, plus personal investment, retirement, and checking accounts, and exclusive offers and content.

- You

needan Android or iPhone to use Acorns. (UPDATE: You can now sign up through their site directly or through their app on your smart phone) - You also need to be in the U.S. (they’re not international yet)

- And of course, you can lose your money. Your account is insured through the Securities Investor Protection Corporation (SIPC) for up to $500,000, but there’s no promise your investments will go up. However, this is with *any investing* you do, not Acorns specifically. If you don’t believe in the stock market or ETFs/indexes, then I’d advise against this.

- UPDATE: Acorns doesn’t work with *all* financial institutions, particularly the smaller ones, but most of the larger banks will connect just fine. If yours doesn’t connect with them it might be worth trying again at another point as I’m sure they continually add new banks to partner with.

Luke from ConsumerismCommentary.com also did a good review of Acorns that I liked, though his recommendation in the end was not to use them (he didn’t like the fees, though they’ve since changed). I obviously don’t agree since I’m having a blast investing through them, but it’s a good read nonetheless :)

I think the main thing to keep in mind is whether you use Acorns on the side, like I am, or if you want them to be your main source of investing – which could change things. In theory you can just invest all your money directly with Vanguard or the other funds for no monthly/yearly commission (outside of the funds themselves), but the question is – will you do it? Most people won’t… It’s the same beef people have with Digit since they don’t pay interest on the savings.

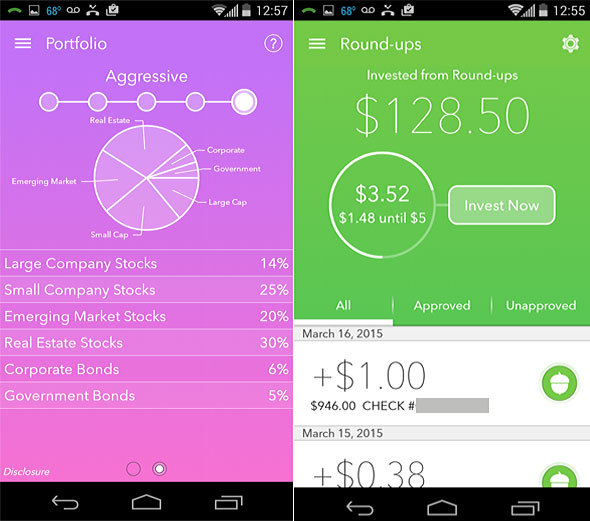

[More screenshots form my personal account… You’ll notice my portfolio is “aggressive” (they recommended one notch lower for me, but I like more risk) and that I’ve invested more than what my account is currently worth ($128.50 vs $123.12). Not ideal so far, but I’m not worried… It’s $123.12 more than I had invested before! :)]

Other FAQs through their site:

- Is there a minimum investment amount required to open an account? Nope. Your first investment will be $5.00 whenever/if ever you hit it from all the rounding up…

- Can you withdraw money anytime? Yup. But again keep in mind the tax rules/etc since these are investments and not just savings.

- Can you change your investment allocations? Yup! They offer half a dozen choices to go with… but they’re indexes and not individual stocks like Apple or GE, etc. So if you like that sorta thing Acorns won’t be for you.

- Does Acorns rebalance your portfolio for you? Yes, usually every quarter.

- Are dividends re-invested for you? Yup!

- Do you have to pay taxes on the money you make? 100% yup :)

One-on-One with Jeff Cruttenden, co-founder of Acorns:

A lot of people found the interview I did with Digit’s co-founder helpful when writing up that review, so I thought I’d do the same here with Acorns founder, Jeff Cruttenden for my Acorns app review. It’s always more interesting hearing from a *person* on the background of their companies than it is reading off their site :) So hopefully you enjoy this one too!

First off, thanks for making Acorns! I’m all about new ways to be rewarded for being lazy, and even more so when we’re talking about money. How’d you come up with such a bad ass idea?

While I was in college, I was surprised at how many of my peers had an interest in investing but couldn’t overcome the barriers in their way like high minimum balance requirements and fees. From that point on, my father and I sought to simplify investing and create a more realistic approach for young people to get started.

As a recent Boglehead convert, I was THRILLED that 4 out of your 6 investment options are with Vanguard indexes. What made you guys go that route?

The portfolios were developed with guidance from Dr. Harry Markowitz – the Nobel Laureate commonly referred to as the “Father of Modern Portfolio Theory” and a team of economists, mathematicians, and engineers. Each of the six indexes was chosen to optimize the diversification of our portfolios across asset classes for where they fall along the efficient frontier where returns are optimized for a given level of risk. Four of the six are Vanguard indexes as they best represent the asset classes to accomplish optimal allocation.

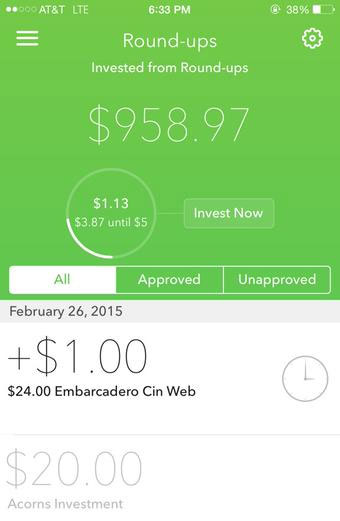

In about a month and a half I’ve banked $123.12 in automatic investments because of y’all. It’s not a ton, but it’s a lot more than $0.00. How much have YOU been able to invest using your own app so far?

$958.97

I have a dumb tax question – at the end of the year, how will all these purchases look in terms of transactions? Will I have to report/document 1,000+ purchase dates and ticket amounts for all these micro-investments going on? Or will it all be nice and simple somehow just like everything else with Acorns?

I have a dumb tax question – at the end of the year, how will all these purchases look in terms of transactions? Will I have to report/document 1,000+ purchase dates and ticket amounts for all these micro-investments going on? Or will it all be nice and simple somehow just like everything else with Acorns?

Acorns provides each investor a Form-1099 at the beginning of each new year for the past year of investing with Acorns. This can be found at statements.acorns.com. While you need to pay taxes on all realized capital gains, you can also deduct any realized capital losses. Acorns does not provide tax advice but recommend consulting with a tax preparer or CPA.

I’ve been obsessed with another product that recently hit the streets as well – Digit. And every time I mention them to other finance lovers I often get back, “kinda like Acorns?” Would you say they’re your closest competition? What do you all do, in your opinion, that’s so much better than them? (In full disclosure, I’m an adviser to Digit. But don’t worry, I won’t hold it against you ;))

Acorns is the first true micro investing company, allowing people to round up purchases and automatically invest the change. The Acorns app and financial engine were built to help people micro invest commission-free into a diversified portfolio of index funds. Thus, the main difference between Acorns and Digit is that Acorns invests the money you add into your account whether it be from your spare change, recurring investment, or lump sum. Digit is a great way to help you put away money into savings.

Any cool features coming down the pipeline?

We will be launching our web app in the next few weeks. We just started our beta and are looking forward to adding this to our current and potential customers as a way to invest with Acorns.

Lastly, if you could grab a beer with anyone in the world – dead or alive – who would you choose?

My dad.

So to recap this Acorns review:

- Acorns is a good way to invest if you’re having trouble doing so

- You just download the app and link up your account

- Let them advise a portfolio for you to invest in (or just pick it yourself – like I did)

- Then watch the account grow over time with micro-investments!

And there you have it :) Another rundown of another company I’m now obsessed with again… Between using Digit and now Acorns, I’ve put away over $500 this year without lifting a finger: $390.74 from Digit and $123.12 from Acorns. That’s pretty cool!

And if it seems like I’m an easy “win,” I assure you it’s not the case. I’ve poked around over 50+ financial companies over the past few months (we get pitched like crazy as bloggers!) and these are literally the only two I’ve started using myself. That’s a small %, and especially so considering it takes me a LOT to be convinced to un-simplify my finances.

Anyways, thought you guys would love to hear about this one so hopefully it helps :)

Will Acorns be for everyone? Of course not. But if you’re having trouble setting aside money to invest, they’re a great app to consider. As always, please do your own due diligence before ever signing up to these things. What works for me might not always work for you!

![]()

————–

PS: I’m not getting compensated whatsoever for this review, which proves even more how much I’m a fan! Not that I would turn down any, haha… I gots no problem pimping out companies I use myself. (UPDATE: I now get compensated for signups :))

Other “Automatic” Reviews:

- Automatically save more money: Digit Review

- Automatically pay off your debt: Qoins Review

- Automatically track your money, investments and net worth: Personal Capital review

Get blog posts automatically emailed to you!

Such a great review J! And this Acorns app is really helpful, I’m just wondering if it’s available worldwide?

For now it is only available in the US

Poor investing by Acorn and too many fees. You will lose your pocket change. I used this app for 6 months and lost money along with the fees charged. I do not recommend this app. Keep your pocket change and spend it. Just a heads up!

I would say if you don’t like Acorns you should still *invest it somewhere* vs spending it all. Even with “poor performance” and fees you’d be left with a chunk of $$$ vs $0.00! And plus these past two months have been horrible w/ the market anyways – so no matter where you were investing through you would have lost money. It’s a LONG term play.

I have been using the Acorns app for a few weeks. So far, I can say that it really helps me use money productively. I am so excited what results this app is gonna give after 1-month use.

Aha! Finally…your review on Acorns.

I would definitely, without a shadow of a doubt, use this if it was available internationally!

*Hope you’re hearing this Jeff*

Me too…I live overseas but do my banking in America…I wonder what the issue is…

I’ve been using Digit and Acorns for the last couple of months and love it. Fun ways to save and invest.

Did you ever take a look at Betterment which is another investing app? I looked at Betterment and Acorns and went with Acorns over the other but I was curious as to what you thought of Betterment, if you looked at it?

Nah, never really poked around Betterment but a lot of finance bloggers rave about them. Same with Wealthfront or whatever it’s called…

I find I’m much more drawn to the places where I can take one glance at and “get it” – if that makes sense? And that’s warm and young/hip looking too. Digit and Acorns both clicked with me within seconds, and when I just clicked over to Betterment right now for example, I see a lot of stuff and don’t know what I’m supposed to do or what exactly THEY do for that matter. They also look very corporate, so I start tuning out within seconds ;)

That might be unfair and not giving them a shot, but it is what it is unfort… Perhaps one of these days I’ll spend more time and then do a review. But only if I like it :) (I hate reviewing companies I hate, unless they really piss me off and I want everyone to be aware – hah!)

Very interesting! I can’t believe you’re cheating on Digit though ;). I’m not a huge fan of the fee associated with Acorns, but I suppose $1/month is a pretty small price to pay.

I’m pretty good about setting aside money on my own, so I don’t know that I need to pay someone any more to do it for me- but I love the idea for getting those who struggle with savings/investing “in the game”.

These apps are definitely useful for those not disciplined to save on their own. The set it and forget it type stuff is better than not saving or investing at all.

It’s killing me that you missed a phone call and have a voicemail. Why is that what I notice? Love all of these apps that are helping people save. I like to think that it’s putting us on the same footing as the big companies who make stock purchases based on microseconds. Stick it to the man!

haha… and it was a coin collector friend of mine! the humanity!!

I read about this app and was intrigued. But then I was turned off by the fee and the taxes. The fee – only $1/mo on balances less than $5K doesn’t sound bad, but if you have $100 invested, that $1 fee is 1% per month. With a financial advisor you are paying that 1$ annually, not monthly.

Second is the taxes. It was “glossed” over in the Q &A section. If you have capital gains, you will have a taxable event. Same goes when/if you sell anything. So if you have a bunch of dividends and/or sells, you are going to have a ton of transactions for a few cents come tax time. Not a big deal if you outsource it to a CPA, but they aren’t going to be too happy about it!

Are these deal breakers? Not for everyone. I’m all for getting people to invest and if this helps those who otherwise wouldn’t invest to invest, then that is great. You just have to realize you are paying a high fee (even though it seems small) until you get a decent amount in your account and you will have fun come tax time.

True true, all good things to think about for sure.

With the capital gains though, don’t you just pay that when you *sell*? If you’re fortunate enough to have grown it over time? I feel like I’ll just sit on it for years and years or something and then either xfer over to a new account or just sell at that point. Which will then trigger. So in that case it’s only a 1-time annoyance? It would be INSANE for a day trader though, haha… not that they’d like this anyways – who day trades index funds??

About the taxes – what you said is false. The only time when you have to pay taxes on stock investments is when they are “realized” gains not “unrealized”. Realized gains means it is either a gain or loss when YOU SELL. Unrealized gain or loss is when the position is still OPEN – and it is a paper gain or loss. So if you do NOT sell your stock/bond investments (cash out) then you do NOT have to worry about paying taxes on your ACORNS investments annually…only when you actually SELL or have REALIZED Gains.

You Southerners get all the good apps… Wish we had something like that up in Canada. You were actually able to get the founder in a interview! Bugetsaresexy = BigTime!

Nice review

I owe it all to Twitter :) Sometimes the only way to reach someone “high up” is on there as they get inundated with emails and other types of messages flying all over the place. I had reached out to a handful of Acorns people previously to no avail.

I’ve read a little bit about Acorns recently and someone just sent me an invite so…awesome to read your review J$! I love that they automate it and make it simple, especially with the exposure to the Vanguard funds – that’s huge for someone new to investing or little to start out with.

As others have said though, the fee is a bit concerning. At first glance, $1/per month under $5,000 doesn’t seem bad, it’s pretty good really, but if you’re starting with $100, $200 or even less then it’s a pretty high percentage. But, if someone is doing absolutely nothing then it’s better than nothing. :)

I think these apps are great for people who struggle to save money and invest. But for me, it is a weekly or bimonthly activity to take what is left over after bills are paid and funnel it into my Roth IRA, student loan principal, or after-tax brokerage account. But for people who aren’t as savvy with their personal finances, these seem like easy “cheats” to getting ahead and beginning the saving train.

If you don’t mind, please update this post after seeing your tax forms for next year. While they provide you the Form-1099 (as legally required) I’m still curious to learn how complex it is going to look, especially with regards to tracking the basis.

Good point David. Although unless he sells any of the investments this year nothing will be reported as far as gains/losses except for any dividends/interest earned. I imagine if you used Acorns for a while and decided to cash out your savings (sell you mutual fund holdings) that you’d have a pretty hefty 1099 reporting all of the individual lots. In that case it may be easier to attach your 1099-B and summarize the information on your 8949 and Schedule D.

I’m going to go with Wiggles answer here – I’m not as smart to know about all that! ;)

I will say that I don’t plan on cashing out anytime soon though and partially just to not have to deal w/ all the tax stuff. It’s the reason why I love retirement accounts so much – you just keep pouring in the $$$ and letting it grow w/out any hassle! And maybe the tax stuff will force people/me to hold tight w/ the brokerage acct $$ even more cuz of it all? That wouldn’t be the worst problem in the world :)

Now Acorns is something I love and I can get behind!! I actually heard about them from the Stacking Benjamins podcast and recommend it to clients over Digit. :-)

Hahaha….

I was gonna say – if you don’t like this one then it’s a lost cause! ;)

I like apps like these… Sure I save my money on my own but any extra that can be saved without me really noticing.. Even Better. Going to give it a try

Let me know how it goes!

This is funny timing, I just stumbled across another finance blog yesterday and her post was about Acorns. Maybe I should check it out. I’m kind of obsessed with Digit right now, but who can really pass up more ways to trick yourself to save more money? Thanks for the review, as always it was great!

Gotta fire away at all angles, friend!

Tried Acorns for about 5 months, got up to a balance in the $50 range, made roughly -$0.82 off my investing, and yet paid $5 in commissions to them. Although I like the concept, I don’t like the fees. And since I am good about investing my money (almost to the point of being bad, because I invest almost all my spare cash), I don’t need to find new ways to invest. I can see the benefit for some, just not an app for me.

Thanks for sharing your experience! Exactly what we need to see to hep make better decisions with this stuff… you gave it a shot :)

Thanks for the review, very interesting. Do you know if Acorns “links” with websites like Mint.com or Personal Capital? Would be curious if they do. If they don’t then it’s a turn off for me, as I wouldn’t want all those untracked debits from my account when I view it in Mint.com. Also, I would want to link/display my acorns investment on mint or personal capital.

I don’t know if they “link” exactly, as I don’t personally use Mint, but I do know that all the transactions would show up in Mint since you have your banking with them, ya know? And then all you’d have to do is categorize them as “acorns investing” or “digit savings” or something like that?

I guess in terms of net worth tracking and what not though, if they don’t link up you wouldn’t be able to see that… So, I guess my answer isn’t that helpful, haha… I’ll see if I can get anyone to answer it for you if you haven’t Googled and gotten it by now :)

They’ve said in a few places that the linking will work when they release the web app in the next few weeks/months.

Great review J. Money! Seems that there are more and more of these apps available to the public to help with saving/investing. That’s great to see.

Funny timing! I just started using Acorns last week and I’m already obsessed. I kept putting off opening and ETF because of the trouble of coughing up $1,500 – $3,000 in one go. This made it so easy to get started!

BAM!

Sorry to be a curmudgeon, but this literally feels like “tripping over dollars to pick up dimes”. Love that saying…anyway, you already have a Vanguard account so why not just have Vanguard automatically take a certain amount of money out of your checking or savings account each month. Don’t let friends pay unnecessary fees or something like that.

Yes, an even better option – provided you actually *do it* :)

I think for me, personally, I like having these little fun things on the side doing it’s biz and just adding to the main pile over time. I’m already maxing out my SEP and usually ROTH every year anyways, so this is like a fun “extra” treat. Automatic transfers doesn’t do it for me where as this is like a game to see how hi it can go. As lame as that answer may be.

(Keep in mind I manage my money very emotionally too – which is the only way I ever reach my goals ;) https://budgetsaresexy.com/2015/03/answer-financial-debates/)

so it really is all just *extra”

If I am correct if you are already maxing your IRA/ROTH this does no good, correct?

Sure it does – you can never invest too much money :)

Keep in mind Acorns creates a brokerage account for you which is *taxable* vs an IRA or ROTH which is a *retirement* account. With those you’ll still pay taxes at some point of course, but there are limits to how much you can invest and max out every year. With brokerage accounts there are no limits – you can invest $100 or you can invest $100 Million!

Now if you’re asking if it’s no good to invest more money “on TOP” of your retirement accounts, as if you should be enjoying more of your life and spending it vs saving, then that’s a different story. And one only you can answer :)

This seems really cool! I just heard of this via one of our advisors the other day, and it’s definitely something I want to check out since I really don’t use cash (I’m wired backward; I tend to spend MORE somehow when I’ve got actually cash on hand). I’m happy racking up the points via my credit cards, but I do miss having piggy banks full of change you could periodically count out and be amazed at how much your handfuls of coins added up to :) This seems like a perfect solution!

Try it out Kali and let me know what you think! :)

Do you know how they pass through ETF fees from Vanguard when they buy/sell?

I do not, sorry :( I usually pass over all the details like that – for the good or the bad, hah.

Maybe it’s in their FAQs?

https://acorns.com/support/

My bank does this for me. When you have a checking account there you must also sign up for a savings account too. Then every time you use your debit card, the amount between your purchase and the next dollar goes straight into your savings account. Sometimes it annoys me because my list of transactions is twice as long now since every time I use my debit card 2 transactions come out of my account, but it does also help me with saving so that’s a plus.

Haha yeah – it def. hurts the minimalism side of things for sure, but I’m hoping the sexy results more than make up for it :)

Pure genius! love it!

Let me know if you end up giving them a try!

Very cool idea – my guess is that it will be either be swallowed up or shut down in 18 months. Unlike the savings app – taking other people’s money to invest is going to blow up their overhead. Vanguard or Fidelity would be smart to buy (or copy) them quickly.

As long as it still exists *somewhere* for me to use, I’ll be a happy man :) And yes, even happier if Vanguard gobbled it and used for its members!

Hey J-Money!

I have been following your blog the past couple of months and decided that, in addition to my regular saving (I have the money automatically deducted every two weeks from my checking account on pay day) I’d go ahead and try out Digit and Acorns. I also decided to go ahead and try out Personal Capital as well, since I presently don’t track all my myriad of bills and such in one location. Long and short, I LOVE PC, but can’t figure out how to add Digit and Acorns to it for more accurate tracking. Any ideas/suggestions?

Thanks!

Awesome man – let me know how you find the two (acorns & digit) after a while. I use them both as “extras” too and it’s been a fun ride so far :)

As for tracking through Personal Capital, I actually haven’t tried as I don’t use PC as much as I should (I prefer old school spreadsheets), but if you’re having a hard time connecting to them, I wonder if you can label the transactions as “savings” or “digit” as well as “investments” or just “Acorns?” So when it spits out your spending and budget/etc, all those withdrawals will be labeled accordingly so you can track easier? It’s not as sexy as just pulling in the info directly from Digit/Acorns (it might not be possible yet), but at least you’d be able to account for them in your records…

Or maybe just manually add in the current balance once a month so it reflects in your Net Worth properly? Kinda annoying but would solve the trick if you don’t mind it not being in real-time every time you log in :)

I LOVE the round up idea and have been searching for as long as I can remember for one that was not associated with a random bank Ive never heard of (And also not BOA). This is PERFECT…except for the investing part. I’d rather just save. Have you ever come across a platform like this (mobile round up) that was just for saving and not investing? Id love to use my Digit account (that I am obsessed with) with another round up program but am not comfortable investing quite yet. Hoping you have come across one in your endeavors, and hoping you can point me in the right direction.

good idea for sure :) I haven’t heard of any other solid players out there doing the round-up savings thing yet, but will shout if I do. I’m glad you’re enjoying Digit so far! I just crossed $900 in savings and waiting to hit that first G – woo!

Hi!!! I’m very interested in ACORN but what i’ve read so far is that there is fee? is there other way not being charge or anything please,,i would love to invest for my kids especially im a stay home mom and work only weekends.Thank you!!1

yeah, they charge you $1.00/mo for using their service. no way around that I don’t believe, sorry :( You can always just invest money for your kids through other places though, like Vanguard? There might be certain minimums to invest but a lot of funds don’t cost $$ to pick up.

Can’t get behind this given the high fees. Any referral income from this reccomendation?

Not at first, no. I blogged about it because I love and use them myself (and still do). Then a few months later I had the chance to become an affiliate for them. They’re def. not for everyone, but if you suck at investing and not doing it, then I personally believe it’s a great way to get started. Fees on any money saved vs $0 saved is still damn good ;) And a dollar/mo isn’t the worst (I’ll agree it’s good to look around once you hit the $5k mark though – at least if you’re comfortable pushing on without them and will continue investing)

Hi J. Money,

I put an initial $5 into Acorns back in Dec 2014 and every once in a while check it on my phone. I havent been rounding up and I havent put any additional moneys into it. Its been fluctuating between $4.53 and $4.98.

I was just going to ‘set it at $5 and forget it’, hoping it would turn into $10.

After reading your review I realize I definitely need to be above $5 for anything to actually happen.

My question for you is:

You say you have ‘invested’ ~$123 from roundups but how much has it grown? I know its silly to ask because its all about the long term but are you actually seeing it ‘grow’ and/or ‘shrink’. I just wonder if a dollar is a dollar, minus fees when it comes to Acorn.

Thanks for taking my comments and question!

Great question indeed :)

I never invest for the short term, so any $$ I put in will stay there for 20,30, 40+ years until I need it (unless I retire super early, but that’s a whole other story), so I don’t even worry if that part of the game fluctuates cuz I know in the end it will be a TON larger.

To answer your question though, my account balance right now is $213.29 and has a total loss of $5.54 or 2.69%. So I’m down $5 but up $213 that probably would have been spent at some point – at least that’s the way I look at it :)

Hope this helps

ive been it for 6 months and have invested 640 dollars of my own money, but I’m down 27 dollars. So far for me it’s losing me money. I love it but it’s not working

Sorry to hear man. If it makes you feel better, all of my investments *everywhere* are down recently too due to the craziness in the marketplace (and same with most everyone else right now ;)). Hard to gauge long term success off only 6 months – it’s much more of a longer play than that. But of course def. dip out if you don’t think Acorns is the best place for you…

A better comparison would be how $640 of your money invested elsewhere in this same time period fared? And if you would have set aside that $640 to begin with if you weren’t signed up to Acorns? If you would have ended up spending it, you’re actually up $613 :)

I’ll get right to the point. I get an email today saying acorns.com has pulled $50 from a ING account I own. I am like acorn.com?? What is that?? I google it and call them. “This happens sometimes” they tell me “when a customer TYPES IN THE WRONG ACCOUNT NUMBER.” Are you kidding me?? You don’t verify that the person is the legal owner of the account?? “Yes we do, we send two small deposits and the customer verifies the amounts we sent.” Ok, then how did your company pull $50 from my account because I never verified anything. “Well, they actually can withdraw up to $1000 before they’re required to provide verification. I don’t actually agree with this practice but our developers…” Well, have a nice time getting sued acorns.com. You are going to get your butt handed to you. “We can definitely get your money returned” she says “but, unfortunately, it will take 7-10 business days.” Yes, for real, people. Pulled money from my account with no authorization whatsoever and no attempt to verify that their customer was the legal owner.

PREPARE TO BE SUED. Class action anyone?

Oh wow, that’s pretty crazy I agree… I had to verify like 10 billion things to attach my USAA account to them, but not sure how it works w/ other institutions.

I’ll pass this over to my contacts over there and see what the deal is.

I tried to withdraw my money and have gotten nothing but excuses and runaround from their ” support” latest update was 6 weeks for a check. I requested the withdrawal and my stocks were sold in the end of October. So they are essentially hanging on to my money for 5 weeks longer than it should take assuming I see a dime. The ach transfer failed from their end although they insisted it was my bank ( my bank said it was their error and I trust my bank more!) do not recommend them at all.

Sorry to hear :( Will pass your note over to them and see if that helps any…

Hi Steph,

Jordan has reached out to you in order to help resolve this matter. If you have any questions please feel free to contact him. You can also reach our Support Team at (855) 739-2859.

The blog was extremely detailed and very helpful. I’m still not sure about having acorns pull my $5.00 out of my account, but I may try it with a few lump sums, if I make some money then ill try it the change way.

Thank you for the excellent review

No problem :) Let me know what you think if you end up giving it a shot later. What’s mostly important here is that you’re just investing *somewhere*. So if not w/ Acorns, do be sure you’re putting your $$ somewhere!

Started Digit about a month ago. One thing I learned there is you can set a bank balance where if it at that minimum digit won’t take any. That was good to know. They will be any bank fees if they put you in a negative balance.

With acorns, I love this as I need to save outside of my 401K. I have a lot of transactions right now. As that tapers off, I can put in a small automated amount. This is like the share drips , except you have to put money there. I love this round up feature.

Once this builds up to a sizeable amount then I can shop around to a different account if I feel the fees are too high. It will take a while of rounding up to get to $5000.

I did do it all by the computer, so you don’t really have to have the app as you stated. Very simple sign up.

Thanks for these reviews. Digit is my favorite! I live the texts every day and I always text back “why” even if I know, just to see in text.

haha yup! their SMOOTH as hell with the texting – I’m going to let them know you’re digging it :)

Thx for the heads up about signing up through the web too – forgot to update this review when they launched their upgraded website.

Curious about the tax return impact from their rebalancing. Is there a ton to report for tax purposes-especially if we do our own taxes? ;)

Great question indeed! And one which I’ll find out about here shortly as soon as I get our #’s squared away for the year… Or rather, when my *accountant* gets them squared away, haha…

Just started using this app and I setup a recurring deposit of $20. I like the round-up feature too. It’s a bit like Save the Change from BofA, but you’re investing it.

Good call on the recurring deposits. Grows a lot bigger that way :)

I found the app very easy to use and since I am a college student, I dont pay monthly fees. I like the interface and do wish that I had some more options with how to exactly invest my money like diversifying it in specific ways but overall it is great for getting into investing.

Hoping this comes to the UK soon!

Quick Question – what’s so bad about BoA ?

Awesome blog! Wish I found it sooner

Glad you’re liking it :)

I personally hate BofA just because they treated me horribly when I used to have an account with them, and their customer service was pretty lacking. I think with all the new technology and online banking now you can find so many better banks out there that won’t try and charge you for breathing.

Great post, thank you! Love your blog. I’ve been considering Acorns for quite some time since pretty much all of my spending is done (responsibly :)) with credit cards so that I may easily track my spending, categorize costs etc. It would just make sense to invest all of that change! My concern though is I already have investment accounts open with Betterment. Would it make sense to employ both? What’s your take?

A million thanks again!

I think it’s never bad investing *more*, whichever account the money goes, but it might get annoying having a bunch of accounts open though. You can always try it for 6 months or a year and then stop if you don’t find helpful? Or roundup the amounts yourself for a month and then xfer $$ over to Betterment in one chunk at the end of the month and see how it feels? And increase it going forward too? It would take some calculating in the beginning, but would give you a sense of how it would look in the end :) Just some ideas anyways…

Loved the review, thanks for sharing.

i see i can do this from my laptop do you still get the refer bonuses and the $1000 at the end of january for 10 referrals if its done fro a laptop i have y refer link and everything

hey – very sweet of you to ask! go ahead and sign up however is most easiest for you :) it’s all good whether I get the referral or not, but I think so long as you click the link here on your computer and then sign up from there it should work?

I was very excited for Acorns, and I tried Acorns for 2 months, and finally gave it up. Two things you did not discuss in your review:

1. Acorns will not connect with smaller credit unions. So in terms of the rounding up feature, it wasn’t happening for us.

2. Acorns will also not connect to financial institutions where you have second-stage authentication turned on for your log in. So, we couldn’t connect our Wells Fargo debit card of chequing account.

Without the rounding up feature connected to our chequing accounts, Acorns just didn’t do it for us. There’s no way I would turn on rounding up on our credit cards!!

Oh, totally – if you can’t do the roundups def. not worth it! I’m sorry they didn’t connect with your banks :( I thought I had noted that they don’t work with *all* banks, but I must have missed it… Going now to update – thx! (And weird about double authentication? My USAA account worked fine with max security on, but it probably depends on the institution and how it connects up with Acorns… I do remember having to try it a couple times before it fully connected with USAA due to all the security though)

I highly recommend to waive the fee for seniors.

AARP recommended it and it would help a lot of elderly people with their SS check, limit income.