One of the cool things about running a blog is that sometimes people send you cool stuff.

You get a bunch of crap/spam/nonsense as well, but fortunately the gems help make up for it :) (Here was the last piece of fan mail I received – “I don’t really care to read about your life for the few nuggets of financial advice you give. My time is too valuable.” Haha… Love you too!)

One such gem appeared last month when I received a “bank box” from Capital One that had some funky contraption in it called an “Echo.” I’d never heard of it before, but from the shriek my wife let out when I opened it (“OMG!! WHERE DID YOU GET THAT??”) I got excited to learn more ;)

From Amazon (Amazon makes it):

Amazon Echo is a hands-free speaker you control with your voice. Echo connects to the Alexa Voice Service to play music, provide information, news, sports scores, weather, and more—instantly. All you have to do is ask.

Why did Capital One send me it? They teamed up with Amazon so Capital One customers can get real-time access to their accounts faster, and they thought it was cool enough that I’d share.

It worked :)

I’m still unboxing all my stuff from our recent move so I haven’t tested it out yet (more on the move later – so glad it’s over with!!), but I use Capital One for my business accounts and excited to break it open and see just how lazy it ends up making me, haha… Gotta love technology!

Then last week I got another shipment, this time from the folks at Tip Yourself, who generously shot me an iPhone 6 so I can (finally!!!) test out their app. I’ve been wanting to do this for months now as they’re making it SUPER easy to save money on the fly anytime you want to tip yourself (see what they did there? ;)) but since I rock an Android these days with Republic Wireless I’ve been out of luck until they get that version out the door.

More on Tip Yourself later, but if you’re looking for a new way to save, check ’em out and see what you think. Whereas my beloved Digit automatically saves for you, Tip Yourself gives you a bit more control over it and plugs you into a community of other Tippers doing the same. Which hopefully motivates you further. I’ve been thinking of it as a way to impulse save instead of impulse buy – a much better way to reward yourself :)

[UPDATE: Tip Yourself is now defunct.. They sold it to another company who eventually closed the doors on them, womp womp…]

*******

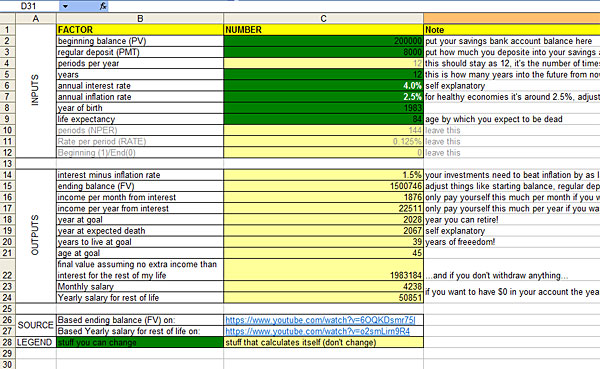

The gem I really want to get into today, though, came in the form of a simple little spreadsheet that a Wilfred Waters sent over to help you gauge when you can retire.

Now this isn’t the first time we’ve featured spreadsheets like this, as we just showcased a beast of one two weeks ago, as well as my own “early retirement” spreadsheet in recent years, but it IS the first one to ever mention “death” in the same spot. And WHY would one ever want to do such a thing??

I’ll tell you: PERSPECTIVE.

I was giving it a once over thinking it would be similar to all the others I’ve seen over the years, and then BAM! – “Years to live at goal” comes up and knocks the breath out of me. Wowwww… What a great thing to reflect on!

Here’s a snapshot so you can see what I’m talking about:

[You can download it directly here – it’s only one page]

[You can download it directly here – it’s only one page]

Scroll down to line items #18-#20 and let it soak in for a bit…

- Year at goal

- Year at expected death

- Years to live at goal

For all the time we spend tracking our pennies and peering into the future, nothing says “REMEMBER TO LIVE, DUMMY!” than a calculation like that telling us how much time we’ve got left, ack! Whether we’ll be spending it in retirement, or not!

The fact of the matter is that each of us only has a set amount of years left on this planet, and death doesn’t care whether we’ve hit our goals. Not that you should quit and get all YOLO up in here, but it’s a good reminder to appreciate our days as best we can regardless of future plans.

We’re alive for today only, so far, and adding a reminder like this straight into a spreadsheet you look at on the daily is a great way to keep it top of mind. Especially if it shows you’ve only got a handful of years left from the point you expect to hit your freedom!

I’ll be incorporating it into my own spreadsheet starting today – and thank Wilfred very much for it.

Here’s the link again to it if you want to try it out: Financial Life Plan

He calls it a financial “life” plan as you can see there, but I’m dubbing it the financial “death” plan going forward ;) Because seriously, have you ever seen such a thing??

The rest of the spreadsheet is fine too, btw – nothing too fancy or anything (enter a few numbers at the top and it’ll give you an idea of when you could expect to retire’ish), but it was that death part that really hit home with me. And you’ll probably want to swap out “savings” in the template with “investments” too as no savings these days are ever going to return anything good. Especially considering inflation, which is also accounted for here as well (though taxes are not, because “I am an expat in Kuwait” he explains. The surprises just keep on coming!)

So yeah. Death and finances – good times!

——-

PS: I’ve mentioned this before when I was going through my death period last year, but I still can’t get over how crazy this is… In 100 years from now, EVERYONE we know and love and follow and even despise will all be dead. All friends, family, celebrities, presidents, even most of the babies being born right this very second. In 100 years the Earth will be inhabited by a completely new set of humans and there’s nothing anyone can do about it! SURREAL!

PPS: Here’s a list of other Early Retirement spreadsheets collected over time too – more info can be found at the bottom of this page here:

- J’s “early retirement” spreadsheet v1 (v2)

- Robert’s “monster retirement budget” spreadsheet

- Hannah’s “early retirement + real estate + pension” spreadsheet

- Tawcan’s “early retirement + dividend investing + passive income” spreadsheet

- Kate’s “early retirement + taxes/distribution simulations + roth ladder” spreadsheet

Get blog posts automatically emailed to you!

Sobering. Yet another reason why I have a dislike for Excel. ;-)

This post really put the nail in the coffin……

Zing!

Interesting approach, and something I might copy. It is a bit morbid, but like you said, a great way to remind ourselves to appreciate the moments we have.

Pursuing financial freedom can be a consuming goal at times, and I’ve struggled with keeping things in perspective. I’m glad this reader had the emotional intelligence to put this into his calculations.

Hah – yeah! Anything to break us from our obsession is great – I think many of us struggle with that here.

Yep. It’s depressing but something you want to think about once in a while. It’s tough seeing parents age. Seeing my children get older is awesome. Parents (or myself) getting older? Not so much…

An echo and iPhone 6! Nice.

I’d love a (free) echo but not sure I’m ready to pay for one yet. I’m not convinced the convenience is worth it but hopefully as the technology continues to improve I’ll get one. I’ve never been an early adopter when it comes to technology. I look forward to a review by you though!

Me neither… Hell, I didn’t even see the purpose of the internet for the first half a decade it came out! Haha…

How fun to get free stuff! Neil has been working on a “when you can retire spreadsheet” including a calculation about what amount of spending equals an additional day of work before retiring. I’ll send this new resource his way!

That’s a good idea! Though maybe he should change it to “an extra day of life?” ;)

Kalie,

Please send this to me (wilfred.waters@gmail.com) as this is exactly how I think about big purchases. For example, if I buy a crappy car then that will delay my date of retirement by 1 month etc. In my opinion, time is a much better way to think about retirement saving than money itself. Suddenly it becomes meaningful. You can literally feel it.

Wil

We’ll send it to you when it’s ready, Wil!

Looks like a fun one to try out. I took the J. $’s early retirement spreadsheet and revamped it a bit to show me that I’m approximately 10.5% complete with our retirement needs and at this rate our anticipated retirement date is November 3rd 2033 putting me just over 46 years old (note this is a maximum calculation given nothing improves and calculated using what I see as very conservative numbers). And since I plan to live to at least 120 given the awesome medical advancements that will be around by then this would give me a good 74 years in retirement! – building me a sweet cabin in the woods and huntin’ my own bear meat.

I’ll probably only live until 110, so I want first dibs on attending the house-warming party!

Sounds a bit morbid – but boy do you get a reality check when you hit your 40’s and 50’s and start attending more funerals than weddings…. Gotta find a balance folks – FI is great but smell the roses along the way.

That is freaky :(

Amen….In the blink of an eye have had “Dear Friends” pass…Makes one seek out what is important….

Remember to live, dummy!! You’re so right about perspective. We tend to look so far into the future we either don’t enjoy the present or are too busy looking past it to find enjoyment in the future. But the future is not guaranteed! :)

I’ll be looking into this more. Great post!

Glad you liked MM :)

Nice! I love having a new spreadsheet to nerd out about and get distracted by ;) You’re so right with that perspective. I’m only in my 30s, but I’m constantly trying to remind myself to get out from behind the computer more often. There’s so much cool stuff out there to see and do!

Not sure I would want to stare down that figure every time I cracked open the spreadsheet, the occasional reminder is good enough for me

Pretty sweet gifts – I am intrigued by the Echo but am a late adapter to most technological advancements like this (I pushed off having a smart phone for years)

We always think about our early retirement number that we often forget life is happening right now. Would you ever consider maybe reducing your savings rate by a small portion and pushing out your retirement date to allow you to do slightly more now?

I believe living life at all stages is important as you never know when it may end and your money will not be coming with you!

I would, yeah!

I’m trying my best to do stuff that *excites me* whether that means saving or blogging or going for walks or even buying Lexuses ;) I’m always considering the costs in the back ground, but it’s more about trying to be “retired” every day than it is to stockpile as much cash as possible. Then again, easier to do that when you work for yourself at home, but yeah – good to try and find happiness each day if you can!

That’s a nice simple spreadsheet to incorporate into your personal spreadsheet. I like more complicated calculators, though. Firecalc is one of my favorites.

Yeah, the death thing is depressing especially now that we are over 40. Feels like life is half over already…

Adding the element of death makes it REAL.

In my retirement spreadsheets, I plan on living to 100. It probably won’t happen, but I want to plan for the worst case (best case, really) scenario.

You can check out my spreadsheets here: http://www.fiscallyfree.com/2016/05/retirement-planning-step-4-recalculate.html

Nice! Will check it out!

Just gave the spreadsheet a quick go and is simple…

I have no idea how long I will live but assume mid 80s just for the hell of it, puts me at roughly mid point on the spectrum, buttttttt we all know those are full potential years. So get cracking, get saving or bloody hell get living! With 600K saving I bumped interest rate up to 6% and looks like I get to withdraw $1900/month. That covers my living expenses so now to find a side hustle for the extra $1000 (insert make money from freelance and photography and outdoor related stuff)

“So get cracking, get saving or bloody hell get living!” – good bumper sticker right there :)

Gotta love that Echo, are you liking it so far? Free stuff is always great! Very depressing to think about death though but that’s life and we all have to face it. The key is enjoying it while it last

Haven’t taken it out of the box yet! Will be soon though as we’re just getting nice and settled in here at our new place.

The echo and iphone gifts are pretty sweet! Looking forward to hearing more about tip yourself. And possibly the echo?

I can definitely say the mention of death in a retirement spreadsheet is a first. Some serious perspective!

I know that YOLO gets a lot of flak but the more I think about the concept, the more I wonder whether these kids have it right. At least within our weird little circle of personal finance nerds, we’d probably benefit more from that “life life now” approach than we’d care to admit.

You’re probably right on that ;)

whateves man – A.I. is going to make it possible for me to live forever! So I’ll still be here in 100 years!

I think I’m in a bit of a “death phase” right now and it’s really jacking up my perspective on everything. Mostly for the better I think; either way I’m going to incorporate this into my own spreadsheets

Side note: Wait But Why has a couple of a thought provoking posts on how precious time really is (careful though, this site is a huge rabbit hole; it’s easy to get sucked in!). This post is a good summary that breaks your life down into how many milestones you’ve got left (e.g. I’ve probably got about 30 Christmas mornings left): http://waitbutwhy.com/2015/12/the-tail-end.html

I KNOW!!! I devoured that when it came out – such a wild way to think about things!!! But so true!!! :(

Thanks for sharing my file in the PPS. I love seeing what other people come up with — keep them coming!

Thx for passing it over the other year! :)

I was $40K in debt in my 30s and it took a long time to pay off and be debt free (which I did by budgeting and getting rid of my car). I did pretty well maintaining that but then was diagnosed with ovarian cancer in 2013 at the age of 45, (thankfully surgery and 6 rounds of chemo took care of the cancer) and fell back to some old habits.

After I recovered, I went through a stretch where I thought “why bother saving?”. Why not have fun now when I’m not sure if I will be here in 10 or 20 years? So I built up a little debt again ($3K). Thankfully, I got wise… or maybe more hopeful? Anyway, I am debt free again this month and am starting to save for retirement again but cancer did clarify what was important to me. When I wasn’t sure what the outcome was going to be after my diagnosis, the one regret I had was that I hadn’t traveled more so now that is a big part of my budget. I think I have finally found a balance between retirement savings and living now that works for me. I hope.

Damn, talk about putting things into perspective. Good for you for prioritizing the important stuff like that!

I remember running an article years ago here on someone running up *hundreds* of thousands of dollars when he found out he had some kind of terminal disease. He took out tons of credit cards and loans and just went all out, only to find out that he in fact wasn’t going to die. Which of course was great!, but then he now had to deal with the financial mess he put himself in :( I wish I could find it cuz it was pretty wild to read, but it always got me wondering how I’d react in a similar situation. I’d like to think I’d be composed, but who knows!

Anyways, glad you’re on the mend now and finding that right balance :)

I love this! You need to plan for life and if you knew when you were going to run out of it, you would plan differently. This is perfection.

How long will we live? According to new research…more than half of millennials will live past 100. It is expected that 50% of the babies born (in the US) in 2007 will live to be 104. I have not read the book talked about in the below blog post, but it is now on my TBR list. Sobering stuff as we think about how long our money needs to last.

http://www.skipprichard.com/you-may-live-past-100-living-in-the-age-of-longevity/

Oh wow…. Good “problem” to have though! :)

I’ve never heard of tip yourself. Planning on checking it out. Thank you!

They’re pretty new :) Let me know what you think!

Hi

Is there a spreadsheet that allows for declining expenditure throughout retirement?

My thought is that expenses are high at the beginning, decline in the middle and then will either increase or taper off, depending on health in years 80+.

I can’t recall one at the moment, but I’m sure there are some out there :) Gotta keep exploring!