Last year I began sharing my net worth reports. And today marks the 12th consecutive month of tracking. Woohoo! Happy…. “net-worth-iversary”?

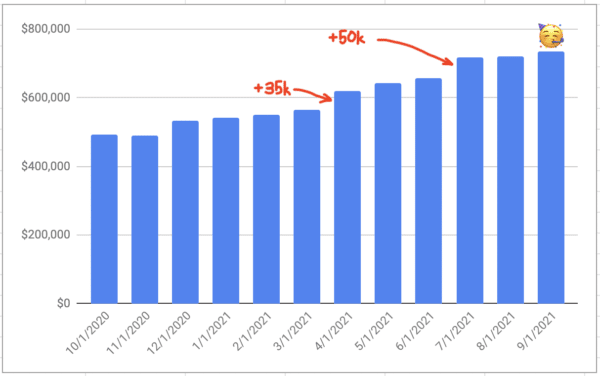

It’s been a wild year. Here’s a chart of the 12 monthly report totals…

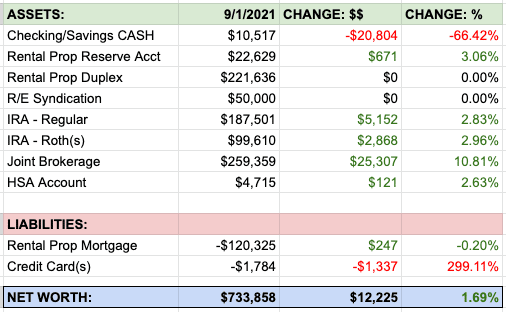

Assets as of 9/1/2021: $733,858

A few interesting notes and realizations when I look at this chart…

- Total growth since Oct 2020 was +$245k.

- But, if we remove the ~$85K of outside contributions from stuff we weren’t originally tracking, the total organic market growth was about $160k. (Rough numbers, I’m too lazy to work out the exact math.)

- This is pretty nuts — 32% growth in 12 months! But, even if we had just average market returns (say, 10%) for the original assets, we’d still have seen a ~$50k increase over the year.

- This reinforces the point that investments have the power to work faster and harder for you than YOU can work for you. As net worth grows higher and higher, personal contributions have less and less of an impact on overall growth.

Investing at all-time highs

Three times during the past year, I dumped large sums of cash into the stock market. Each one of these was at an “all-time market high.”

- $35k into VTI in March

- $50k into VTI in June

- $20k into VTI just last month! (investing our emergency fund)

Not gonna lie… I was kind of shitting my pants during these moments. It’s really hard to buy stock when it’s the highest it’s ever been. But looking back, I’m so glad I went through with it and trusted the research vs. waiting for a dip to invest.

I’m not saying this to prove that “I was right” — the market could have just as easily gone the opposite way… But for anyone out there who’s sitting on a large pile of cash that they know should be invested but are feeling scared… You are not alone. It’s scary! But try and remember that history shows investing at all time highs is still a smart thing to do. So, do it!

Big Spending in August

We had another mammoth spending month with all types of big bills…

- Poor Cooper was back at the vet last month and racked up a $437 bill 🐾

- I finally visited the dentist after 4 years and paid $245. Sadly I’ll be back there this coming month for a filling replacement. 🦷

- Wife and I bought tickets to Boston for Christmas to visit family! ~$400 🎄

- Car insurance ($280), renters insurance ($120) and liability insurance bills ($347) 💵

- Wife and I got a new (used) couch! $300 + $150 moving costs 🛋

- Sadly, my old surfboard had to get repaired after a surf accident a few weeks ago. I paid my little brother $150 to take on the repair job. Old board:

- Check out this new surfboard though… I picked it up for a bargain $75! Not sure if I want to keep it yet or flip it online. 🙃

Good Savings and Extra $$ in August

Not as many money wins as there were expenses last month. But any extra money is good extra money!

- Last month we spent $0 in gas! Quite a difference from the $500+ we blew in July for our road trips.

- We made $300 in cash back credit card rewards! $200 from a new Cap One Quicksilver card and $100 from an existing BOA Visa.

- I picked up some after-hours work at my employer for an extra $600!!

- Lastly, I participated in a Tech Studies User Product testing workgroup and got paid $150 for 1 hour of participation. Quite fun actually… I just played around with a cell phone app for an hour and gave some feedback. After, they gave me a $150 visa card. (I believe this group is still looking for participants in Los Angeles, Las Vegas, Dallas and Phoenix. If you are interested and live in these cities, click the link and fill in the forms, they will call you to schedule.

Asset Breakdown: $733,858 (+$12,225)

All in all our net worth grew by ~12k. Here are the account changes…

Cash Accounts: $10,517 (-$20,804): We dumped $20k from our savings into the stock market in an effort to lower our emergency fund. Kind of scary, but it’s already paying off a little bit. I haven’t had this little cash in my account since I left Australia 14 years ago. Feels weird!

Rental Property + Reserve Account: $244,265 (+$671): Here is how the property made us money last month:

$1,975 — Incoming rent

(-$140) — Property mgmt fees

(-$387) — Maintenance (kitchen sink/faucet issues and dryer repair)

(-$114) — Lawn care

(-$663) — Mortgage principal + interest

$671 — Total account gain this month

As far as management time, I put in only ~10 mins this month for a call to my property manager. She handled everything else. One of the reasons we love this duplex and plan to keep it long-term is the low time overhead for us.

Real Estate Syndication: $50,000: The multifamily real estate market in the U.S continues to kick ass. Rents are still rising, demand is still strong, and I’m seeing much more deal flow for new syndication opportunities. Kind of tempting to invest in a new deal. ;)

IRA – Rollover: $187,501 (+$5,152): Booyah! The market continues to provide. If I leave this account alone and untouched, it will grow to over $1 million by the time I turn 60. Crazy.

IRA – Roths: $99,610 (+$2,868): We’re in spitting distance of crossing the $100k mark!

Joint Brokerage Account: $259,359 (+$25,307): Massive change here is due to the new cash we transferred from our checking accounts.

HSA: $4,715 (+$121): An interesting note here…. HSA accounts are supposed to be used for medical expenses… And this past month, I had a $245 dentist bill. But, I chose to pay cash instead of using this HSA account to cover my medical bill. HSA accounts grow tax-free —> So it’s in my best interest to pay cash for medical expenses early in life, and let this account grow/compound as much as possible over time. Many people don’t think of their HSA as a “retirement” account. But if you play the game correctly, it can be quite a nice little tax shelter. More about that here if you’re interested!

Breakdown of Liabilities

Rental Property Mortgage: -$120,325 (+$247): Just for giggles, I did another refinance exercise with Chase bank to see the new rates they were offering. With rates in the high 3%’s for an out-of-state investment property, the numbers didn’t make a whole lot of sense. Our mortgage right now is at 4.25% and has ~24 years left.

Credit Card Balances: -$1,784 (-$1,337): Anything we buy via credit card gets paid off every month before interest kicks in.

My wife and I have no other consumer debt at this time. 😎

How did you all do this past month? Any big wins or changes to share?

Happy Friday!

– Joel

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Great stuff! It definitely takes some getting used to having a small amount of cash on hand. I consider my investments pretty much off limits, but in a pinch I can always sell some of my more speculative individual stocks in my after tax account without touching my “real” retirement allotment. So I don’t have the cash per se, but it’s floating around somewhere.

I have a few bonds that I can sell. Hopefully if I have to pull money at a strange market time I have the options to sell stocks or bonds. :)

Great gains. I always see people saying they don’t want to invest at market highs. To me it’s a no brainer invest and today’s highs are tomorrow’s lows. That is a nice net worth. I’m marching toward $600,000. Can’t wait to read your future updates

Nice work Doug! I see you’re tracking dividends on your blog. Good stuff!