(Big ups to A. Money for the throwback OPP’esque reference ;))

Welcome to Round II of Other People’s Money!

Where we blast out juicy numbers for everyone to see, and then include a snapshot on their background for even further ogling perspective ;)

Up this time around: a millionaire who doesn’t feel like a millionaire, a traveling Cardiac ICU Registered Nurse, a Hebrew software engineer, and a 64 year old real estate millionaire who used to be homeless (and penniless) just 18 years ago…

Jump into the different lifestyles here and see if you can find some good motivation!

Snapshot #1: The Millionaire “Imposter”

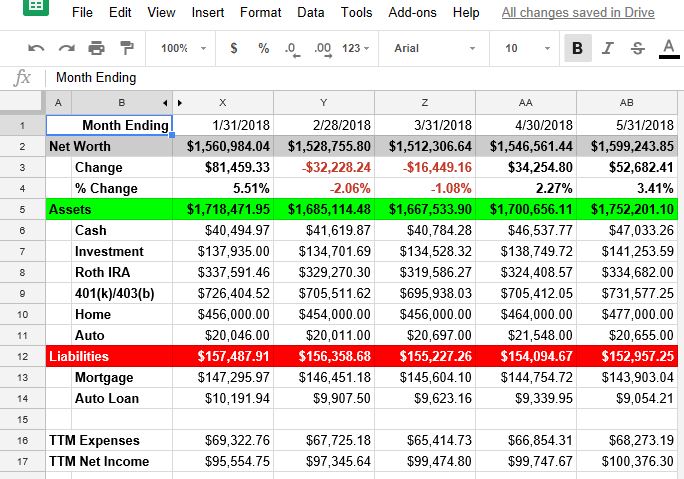

This one comes from A. Money (the same A. Money that gave this series a new name), and you can see just how much they’re hustling over there. Their retirement accounts are on fire, got loads of cash handy if needed, and their mortgage to home value ratio is looking mighty fine as well. Awesome to be able to compare so easily to previous months too!

Here’s more on his background for further perusing:

Hey J. Money,

It’s A. Money, your brother from another mother. I saw your post looking at other people’s money, and it inspired me to share our net worth with you and your readers.

My wife and I share monetary habits and have similar interests, which has made managing household finances a relative snap. We’re both savers, and we’re pretty much in sync when it comes to spending.

One thing we’ve never been able to do, however, is develop a budget. Budgets may be sexy, but spreadsheets are absolutely alluring. Rather than budgeting, we’ve been tracking income and expenses for years, initially in a shared notebook before switching to a spreadsheet starting in 2016. A few months later, we began tracking our net worth on a monthly basis. See the attached pic.

- “Cash” includes assets in a variety of bank checking and savings accounts

- “Investment” includes assets at Franklin Templeton, Fidelity, and Vanguard and our family HSA at HSA Bank and TD Ameritrade

- “Roth IRA” includes my Roth IRAs at Franklin Templeton, Fidelity, and Vanguard and my wife’s Roth IRA at Fidelity

- “401(k)/403(b)” includes my traditional and Roth TSP through the federal government and my wife’s 403(b) and a rollover IRA at Fidelity

- “Home” is our house value according to Zillow

- “Auto” is the combined value of our two cars according to KBB

- “Mortgage” is our mortgage balance

- “Auto Loan” is the balance of our one auto loan

- “TTM Expenses” is the sum of our expenses for the Trailing Twelve Months

- “TTM Net Income” is the sum of our net income for the Trailing Twelve Months

We both max out our Roth IRAs, TSP/403(b), and HSA. We also contribute $200/week to our Vanguard brokerage account.

An interested reader,

Aaron

After congratulating him on being a millionaire, he responded with the following:

I wrestle with the “millionaire” label. It feels great to see those seven figures as they creep up over time, but part of me feels like my wife and I need our investable assets (I’d include our home value here, but not our auto values) to exceed $2M to reach that status. #imposter #notworthy

Seems like no one’s immune to the ol’ Imposter Syndrome ;) Hopefully they realize just how well they’re doing though! “Wealthy” or not, they’re absolutely killing it.

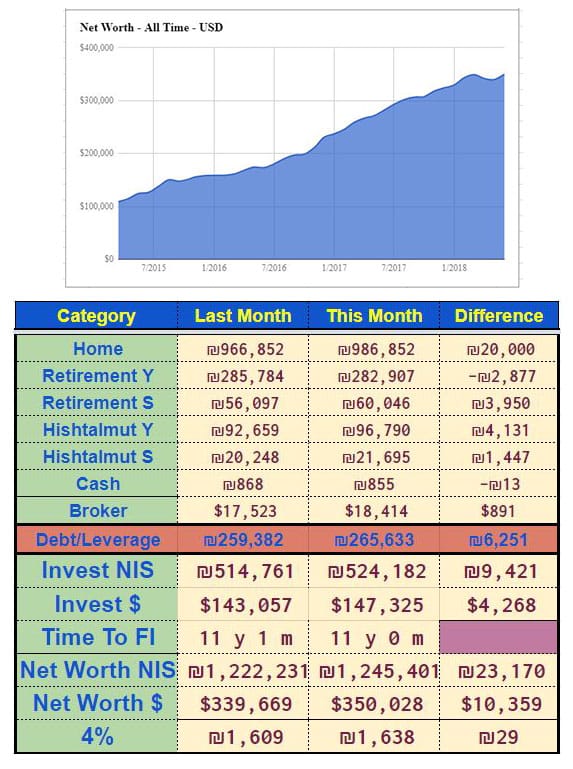

Snapshot #2: The Hebrew Software Engineer

This snapshot comes from The Financial Translator, and you’ll see the top portion there in US dollars after he graciously converted it for us (he lives in Israel), and then the bottom section in both dollars and shekels for some nice mashing up, haha… Check out that “Time to FI” row though towards the bottom – excellent idea!

Here’s more on his background:

I am a software engineer my wife is an archaeological concervator. We make over the average salary for a household. 2 little boys ages 3 and 1. Both of us have masters in our respective fields (school here is dirt cheap – a.k.a subsidized by the taxpayers).

I started tracking in Jan. 2015, we had a NW of $108,671 back then. Now its $350,028. Every child slowed us down a bit, but that’s ok, it’s for them and we keep hustling.

Our plan is to retire early in 9-11 years or semi-retire even earlier. We also bought an option on an apartment in Dec. 2014, they started building in April 2016, and we are finally moving in this summer if all goes well with the final inspections. Essentially we saved money on the deal because we (all the 80 apartment buyers) basically cut out the middle man and his profit. But it was nerve wracking and time consuming, and the building is in deficit so we need to come up with an extra $15,000 (per apartment) over the initial price estimate. We will never do it again. Either rent or buy off the market next time. But we learned a lot in the process, like we would rather pay more next time than go through that type of pressure.

This year was a perfect storm for us as we had two kids in private daycare (public daycare doesn’t start here until age 3), and we payed rent and a mortgage. Tough, but we pulled through. Private daycare costs us $1,247 per month for 2 kids (we get 10% off for sending them to the same one), rent was $1,090 if you factor in utilities, and our mortgage payment is $1,020 per month. Income is $6,763/mo net after taxes and retirement deductions, so we had some wiggle room.

– The Financial Translator

(Your biggest fan from Israel)

Love how connected the internet makes us :)

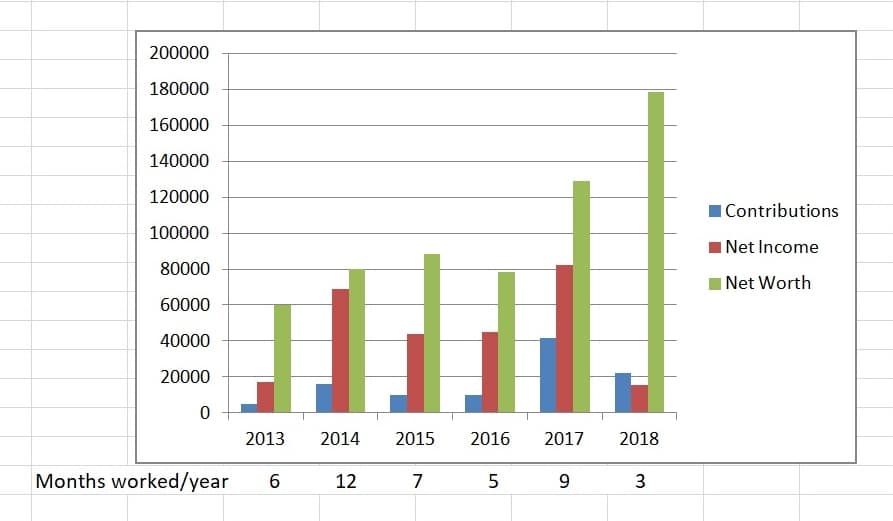

Snapshot #3: The Breadwinning Traveling Nurse

This one comes from another personal finance blogger, but whom currently prefers to remain anonymous. Notice the # of months worked there for each year though, and how the worth still continues to go up despite some years only working half the time! Where do we get that deal?? ;)

More info:

- I am an Associate’s-prepared travel Cardiac ICU Registered Nurse. My goal is to work two 13 week contracts per year. I bring home the bacon.

- My husband works for the subsidiary of a major airline as a trainer and ramp agent (the guys who load bags on the plane). He works just 20 hours a week and makes about $1 more than minimum wage, but brings home the flight benefits. We don’t have any babies.

- My husband also goes back to North Dakota every fall to help his father harvest, and I do temporary vaccination work at the local health department. I have a 401k there, and make really decent money for rural North Dakota, and he gets a cash gift from his dad for the help. The gift varies, but of course never goes above the cash gift limit. The highest we’ve ever gotten was $10k last year for six weeks of work.

- We are effectively homeless. We’ve been living out of a travel trailer the last two years but recently sold it in order to weather a Tucson summer/monsoon season, now we’re renting some dude’s pool house. My current contract is up the end of June but I’m hoping for an extension. Then we’ll be free again to move about the country.

- We typically keep about four years’ expenses in cash, but recently funded a hard money real estate loan for $35k with 4% interest for seven years. That cut our cash almost in half, but brings in $458/mo in passive income.

- After finding the FIRE community last year we really stepped our retirement game up and now I contribute 50% (company max) to my 401k and my husband contributes 40% (his company max) to his. We invest 100% in stock index funds.

- Everything leftover from our paychecks goes into a money market that we’ll use to max next year’s Trad IRAs and HSAs, and everything leftover from that will go toward next year’s expenses. Anything leftover from that goes into our taxable Vanguard index funds.

- $200k is our Coast FI number which we’ll easily hit if I get an extension or a second contract somewhere else this year. Then with farming and the health department… forget about it. We’re rich, bitch!

- My husband will be able to retire with flight benefits after the age of 52 + ten years of service so our real FI date isn’t until 2031.

- He loves his job and is happy to keep working but I desperately want to get away from bedside nursing. I want to help people die, man. You know, be an ultra-part time hospice nurse.

- I don’t include our cash, that hard money loan, or our vehicles in our net worth – our net worth is strictly our retirement and brokerage accounts.

Living in a pool house, farming, not including cash in your net worth?! Who are these people? Haha… Gotta love how drastically different our lives are :)

And as someone who has also worked in the airlines industry chiefly for the flight benefits, I can attest to it being quite a hack! They pay you like crap, but boy does it infuse some adventure in your life… I went everywhere from Cancun to L.A. to London, Puerto Rico, and even the Mall of America for a quick 1/2 day jaunt during my first few months working there… Super cheap way to travel the world if you can pull it off!

(Another great blogger who does this too is Miss Mazuma. She’s a flight attendant by day, blogger/world traveler by night and just overall FUN person :) Check her out if you haven’t before!)

Snapshot #4: The 64 y/o Millionaire

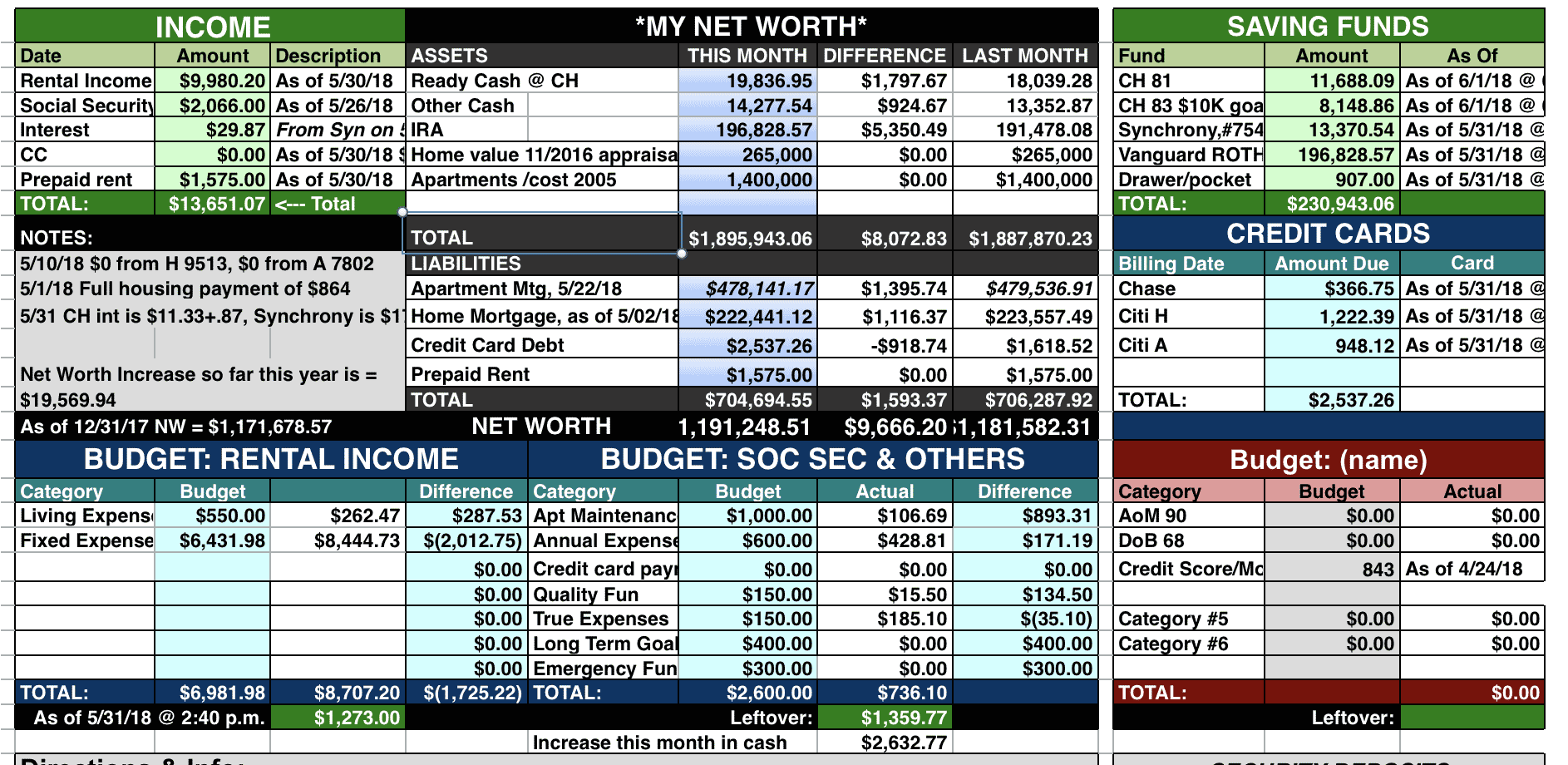

[Click to enlarge… if this spreadsheet looks familiar, it’s because it’s the one I designed!!

Which you can download and use here :) ]

And last but not least, the snapshot of “Barb” who has gone through quite a bit over the years… She was a bit hesitant to share her story as it included receiving an inheritance (and we all know what comes with that when you tell people!), but I told her it’s a safe zone here so hopefully y’all are good to her ;) The last sentence of her note says it all.

Barb’s story over the past 18 years:

2000 — Was homeless and penniless, on relief and renting a room in a bad home.

2002-2003 — Both parents passed leaving me around $500K, mostly in real estate.

2004 — Turned 50.

2005 — Sold remote, inherited, apartment building and purchased over priced, larger one in my area.

2008 — Stocks and real estate market both crashed. Home was worth about half what I owed and had to reduce rents. Today, in 2018, it’s worth about what I originally paid for it.

2014 — Turned 60,

- Found YNAB and started budgeting,

- Discovered FIRE community and found places I could learn from. Dove in head first and haven’t come out yet.

- Moved my traditional IRA to Vanguard, converted to ROTH ($129K) and invested everything into VTSAX, thank you jlcollinsnh. $0 taxable income and many accumulated tax credits were used to pay the taxes when I converted from traditional to a ROTH IRA.

2016 — Refinanced home from 6%/30 yr interest only mortgage to 2.75%/15 yr mortgage. By the end of the year realized I’m a millionaire, but still struggling.

2017 — Major repairs at apartments to the tune of over $50K.

2018 – Today, have started pulling returns from VTSAX and use that to purchase VTIAX, a little to VBTLX and even less to BNDX in my ROTH. Also started investing a little in a couple of taxable brokerage accounts. Mostly in VXUS with a little to VTI.

******

Ever since I purchased the apartments I have been accumulating tax losses at a rate of approximately $25K per year, (have been spending more than I could afford) on upgrading/repairing them, and the tax code has been very good to me. Today, the taxable income on my taxes is below minus $100K. Want to stop increasing this number and instead have the money available in my accounts. Tax credits are great but don’t help with today’s expenses, or investing and the returns are awful.

Today when I fill out my monthly budget, I start with my living expenses of $550. Then pull some off budget, and some even off net worth report.

- Prepay apartment mortgage – $200

- Emergency backup – $200

- Emergency funds – $300

- 30 year bond purchase – $200

Then fill out remainder of my budget, starting with “future spending” goals and lastly fund monthly fixed expenses. Today’s budget looks like the attached image.

I know the bond purchase is not a great move financially today as rates are so low. I look at this as building up my floor, guaranteed, basic, no matter what, income. It isn’t much today and will increase with time. My hope is that no matter what, US will continue to pay it’s debts.

I am prepaying the apartment mortgage, a little, with sights on being debt free before my 80th birthday. The $200 prepayments will cut 2 years off how long I need to make these payments. The additional $200 is there as a back up to my emergency fund and if things work out, I will consider moving it to my mortgage to pay it off even earlier. Today I want to keep it liquid, in case I need it in the future.

My plan for my ROTH account is to let it simmer, hopefully for the remainder of my life.

Generally, I hesitate to share my story since my net worth is completely built on inheritance. Never appreciated what it takes to hold onto any windfall, be it inheritance, lottery or jackpot winnings. Today I do.

And that last part is what it’s all about, right?? Growing over the years and learning to appreciate everything we’ve got? We’re all in different stages with this stuff, but so long as we’re paying attention NOW and doing our best, the future looks bright!

Hope you guys got something out of these today, and we’ll continue the series again in a bit :)

To see the first post we did in this series, click here: A Look at Other People’s Money

******

Huge thanks to everyone who opened up and let us into their lives today! If you’d like to share your story and screenshots with us, pass me a note and we’ll make you famous in a future installment.

Get blog posts automatically emailed to you!

This was a fun read. Seeing the inner workings of strangers’ net worth. Isn’t that why they put National Enquirers and US Weekly at the checkout line…to suck you in with the gossip.

I agree though J Money, it is fun to see how vastly different people are living on this earth. Pool house! Part-time nursing! They all sound awesome. Keep up the good work out there everyone and keep seeing that monthly change be positive.

You know, that wouldn’t be such a bad idea for a magazine – National Enquirer for Money!! Where all you do is read about your favorite celebrities’ net worths as well as other peoples’ right off the streets, haha… It would probably get more people interested in this stuff! And then you sneak in the personal finance tips once they’re hooked ;)

I LOVE that idea! Money Magazine used to have those. I promptly canceled my subscription when they stopped including those and upped their ads. And, I do like the idea of celebrities’ mixed in with regular people. You’re on to something there!

Okay, you start building it and I’ll get the people to feature :)

I find other peoples financials fascinating. Thanks for compiling these stories.

Traveling nursing seems like the ultimate employment hack. My brother is one. The pay/housing allowance combined with the flexibility to take off long long stretches of time between a gig is brilliant.

Glad you liked this, man! We’ll keep doing them if people continue to enjoy :)

Maybe it’s just a matter of changing our mindset. I definitely don’t feel like I am financially independent or well off if I still owe other people money. I’m still a slave to the creditor.

I know it’s a controversial topic in the PF community. Don’t mean to offend anyone. That’d just how I feel about money, wealth and debt.

What if its your choice to have debt though? Like part of your overall plan/strategy? I didn’t feel like a slave when I owed $20k on our car even though I had the money in the bank to pay off at any time. But back in the day when I had c/c debt and not the money to pay it off I def. felt bad, haha… I know a lot of people who have debt on purpose while growing their real estate empire as well. Not saying it’s necessarily good or bad, but does that line of thought change anything for you, or does all debt make you feel queazy no matter the circumstances?

These are great stories and it shows that it’s never too late or too difficult to try and get your finances right. All of us need a little break here and there. I am glad that some of us take those opportunities by the horn and did something with it and the results were astounding.

Everybody has totally different lives! The nurse is the one that I’m most interested in reading about. How does that amount of traveling and time apart change the dynamic of being together and married? Oh and I relate to A. Money big time. I would celebrate the first million a lot harder if I believed we deserved it…(not saying A Money doesn’t!!! It’s just me!)

Why is Other People’s Money “OPP” and not “OPM?” Did I miss something?

I do like this financial voyeurism which is one of the reasons I enjoy Budgets Are Sexy. I’ve been using a budget for over 30 years and started with a 13 column ledger (wish I would have kept it) and a pencil with a big eraser. I especially enjoy seeing the Net Worth / Income over time. I think if more people realized that the first 10 to 20 years is a slow grow (really depends on savings rate and what you do with financial windfalls) they would not be as discouraged with their own progress. How many times have we said I’m not getting anywhere fast so why not pull some from savings for the boat, trailer, vacation, second house, etc.

We should all just keep up the good work. We did deserve that first million but more importantly that first thousand. Celebrate all of those successes and help others get there too when you can.

It’s not OPM because Jay’s wife now works for the feds and OPM is the Office of Personnel Management.

That’s probably not the actual reason, but it’s a reason :).

Ughhh I totally messed that one up! Should be “OPM” yes – not OPP haha… Got too excited about the song reference but just went back and edited it. Thank you :) And I’m glad you’re enjoying these, Bert! (Very funny, Kit ;))

I agree with Ms. FAF that it’s about each individual’s mindset. I also wouldn’t feel free if I still had debt. If I were in your shoes, J, I probably would have paid cash for the car to begin with.

Great series! It’s so interesting to see how others handle their money.

To the young woman who inherited her cash, just remember it’s not how you got it, it’s what you do with it. There are plenty of people who squander away all their money, whether earned, inherited, or won. You’re doing a great job.

Jay, how do I get you show everyone my money? I’d love to show how we went from a single income putting my wife through private vet school to now where she makes 3 times what I do. She is an amazing woman, her only flaw is she won’t let me stop working yet.

Nice!!! Pass me a screenshot of your net worth or spreadsheet or whatever you have, and then some bullet points on the background and we’d be happy to feature it :) Email: j @ budgetsaresexy (dot) com

So interesting to get a glimpse into these different lives! I was struck by something in each one, but particularly by this: “She was a bit hesitant to share her story as it included receiving an inheritance (and we all know what comes with that when you tell people!)” Our debt-freedom is going to come 8 months early (in Sept. of ’18 instead of June ’19) because of an inheritance. It was something that I found difficult to write about. It’s a weird combination of emotional grief and financial windfall – and a deep desire to be wise with it to honour the giver. When you say, “we all know what comes with that when you tell people!” I wonder what you are referring to. I anticipated some resentment, but I didn’t receive any. Was resentment what you meant?

Yup! Mainly from other people, and especially online in forums :) You could be hustling up a storm and doing great with your money, but the second you mention receiving an inheritance it’s as if it nixes all your work completely and now you “cheated.” Financial Samurai actually had a great post about inheritance stuff which I’ve never forgotten: https://www.financialsamurai.com/why-are-people-so-ashamed-about-inheriting-money/

Might be worth a read if you haven’t already :)

I think that resentment for so-called “cheating” comes from the “self-made-man” ethos. We did pay off 80% of our debt before the inheritance sped up the last 20%, and I felt what Financial Samurai said in his article (which I hadn’t read – thanks) was true: “The only reason why you’d be ashamed of inheriting your parent’s or grandparent’s money is if you DISHONOR their money by spending it frivolously on stupid things.” There is a gratitude and peace in knowing we have honoured the givers of this gift. On a separate note, shouldn’t the online pf community discuss inheritances simply for the sake of being prepared to use them wisely and to be prepared for the potential pitfalls of estates, etc.?

YUP! 100% agree on all accounts! I don’t know why it’s such a sticky point online, but it is… At least in the forums and comment sections of bigger media sites. You’ll def find more logic/civil discussions in the blogging community which is at least good :)

I called it “Ramen Resentment.” People feel like you just didn’t eat enough Ramen to deserve where you are.

However, kudos from going to nothing to hanging on to something and admitting mistakes you made along the way. 2 years ago, I inherited the same amount from my father as did my four siblings. I was so torn about how to honor him and just not wanting to spend it (it meant accepting the loss) that I finally bought a condo that I rent out. To me, my dad wanted me to have safety with that money, and I know that to him, knowing I had a paid off place to live would be the safest. I don’t live in it because I couldn’t afford the area I want to live in, so I rent a much less nice apartment in a better area:-)

I think my siblings bought fancy cars:-) Oh well.

Anyway, lots of people blow inheritances, especially after being poor for a long time. I was reading the blog of the guy (can’t remember the name) who retired at 33. His first money lesson was a blown inheritance before he got his financial life together.

Ramen Resentment – love it!!

Almost as much as your website name… Which of course I now have to go check out :)

It is so fun “snooping” into other people’s lives and finances. Thanks for sharing (to you and the folks mentioned).

I’m not a millionaire but already know I will feel like an impostor. By the time I hit $1M in my retirement accounts, inflation will not make it mean as much then as having $1M now… I’ll probably need about $1.3M before I actually call myself a “Millionaire”.

It’s all a worthy goal no matter how it makes you feel! I want an email the second you cross it, please :)

Thanks for the naming credit. Appropriate that this should post this week, as I’m up in Bar Harbor rubbing elbows with the truly rich and fabulous. A nice thing about taking family vacations is that I cease tracking everything and anything financial.

Nice!! Love that you’re still on $$$ blogs during vacay too – only the best for you! :)

I love Bar Harbor!! It’d be nice to be up there right now.

Bar Harbor was fantastic. I hope it’s not another 14 years before we get back there. There was plenty of hiking and plenty of lobster sprinkled with the occasional reading of “$$$ blogs”. Now it’s back to the real world.

Thanks J and all contributors on this post for being open and sharing your various situations. It’s great to see the various paths that people have taken to get to where they are today. I share the same feeling as some others – that $1 million won’t be worth as much when I hit that mark so have a larger number in mind to feel FI. I also like seeing the various ways folks are tracking their money…now off to fancy up my tracking spreadsheet!

Haha awesome… always fun adding in new things to track in them :)

All of them are great stories and shows that we come from different backgrounds and find various ways to build your net worth. Really like the couple who was living in a trailer then sold it and ended living at someone’s poolhouse. Talk about various ways to live, that is pretty unique right there. Like it!

Not only do I love reading other people’s stories and seeing where they’re at in comparison to the rest of us normal people, but I love seeing the different spreadsheets being used to give me ideas on my own. I look forward to the next iteration!

Yes – the spreadsheets make it a good 10x better :)

These articles are great. Always interesting to see where different people are financially to compare myself against. Keep them coming!