I got a question recently from a reader about my net worth tracking…

“I was curious why you’re not including your primary residence in your net worth equation? I know many people say it’s not an asset. It’s your home, you have to have a roof over your head, etc.

Just wondered the reason. I include ours in the equation but didn’t know if that’s the typical way. :)”

This question pops up a lot, and it sparks a pretty interesting debate. So I thought I’d share my reply and thoughts with y’all. I’ll also talk about why including your home equity in your net worth calculation could either help or harm your retirement expectations, along with some hypothetical examples!

Oh, and to answer that first question about my personal situation… The reason that I don’t include my residence is because my wife and I don’t own the house we live in. We are renters… and happy ones at the moment!

Is Your Primary Residence an “Asset”?

In general, yes. When you’re taking a snapshot of your net worth, your house can be included in the asset column (and corresponding mortgage in the liability column).

So why do so many people leave their residence out of their net worth calculation? All assets should be included, right?

Well, that’s where we reach a fun grey area…

Remember, Income Production Is a Big Part of Net Worth

A net worth report is just a wealth snapshot from a single point in time. It doesn’t actually explain someone’s true financial trajectory or readiness for financial independence.

Specifically for retirement planning, we need to try and look past an individual net worth snapshot, and try to envision a long-term stream of income. After all, that’s what we’re really saving up for … recurring cash flow we can live off of, not just a big pile of “assets.”

Most primary residences don’t provide income (unless they are sold, refinanced, or rented out). So this is why some people leave out home equity in their net worth reports, because they are more concerned with tracking and growing income-producing assets only.

Here are some examples to illustrate the impact of including (or not including) home equity as a part of your net worth calculation…

Net Worth Examples: *Including* Home Equity

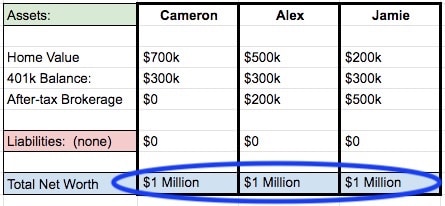

Cameron, Alex, and Jamie all have a personal net worth of $1 million dollars. They have been diligently saving, paying down debt, and investing for the past few decades.

They are all in their late 40’s, have paid off their mortgages, and own their primary residences free and clear. They have zero credit card debt. Woohoo!

Here are their current net worth reports side by side:

On the surface, it would appear that all three of these people are just as wealthy as one another, because their total assets and overall net worth values are all equal. All $1 million.

But, if we drill down into what type of assets they each own and start retirement planning, we uncover a totally different story. Each asset serves a different purpose, which affects how these people meet their financial goals.

Let’s drill down into each individual situation and discuss retirement savings…

Cameron Wants to Retire Early

Cameron’s FIRE buddy recently said, “With a $1M net worth, you can withdraw $40,000 each year (based on the 4% rule), and never run out of money again!”

Cameron loves this idea, because their expenses are about $40k per year. Retiring early would be awesome!

But, Cameron quickly finds 2 problems with their net worth…

- They can’t withdraw any money out of the primary residence. Even if they did a refinance or got a home equity loan, they couldn’t withdraw enough money to provide $40k consistently year over year. Cameron doesn’t want to sell the house or move out, so this $700k “asset” isn’t really useful for retirement.

- Cameron can’t pull any money out of their 401(k) retirement account either – until age 55. (Technically it’s possible to withdraw funds early and pay penalty fees/taxes). So this $300k “asset” isn’t very useful right now either, and wouldn’t last very long if they started withdrawing money from it anyway.

So, even though Cameron has a net worth of $1M, those underlying assets can’t help them retire.

Cameron needs more income-producing assets to make up their retirement savings.

BTW – this is why people sometimes call their primary residence a ‘liability’ instead of an ‘asset’. Cameron’s $700k in equity seems more like a burden than a help at this stage (based on the goal of retiring early). Cameron has a lot more saving/investing to do before they can use the 4% rule to retire.

Alex and Jamie are in a slightly different financial situation, which we’ll get into in a sec…

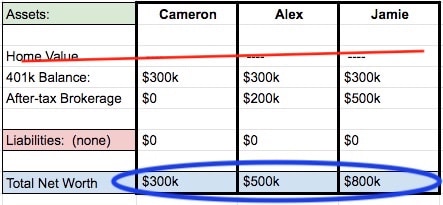

Net Worth Examples: *NOT Including* Home Equity

Now let’s look what happens if all three of these hypothetical people *didn’t* include their primary home in their net worth statement. It paints a different picture…

By removing the primary home equity, we now see a pretty huge difference in personal net worth. This gives us a bit of a better view into each of their individual paths to financial independence.

Let’s talk about Alex’s and Jamie’s financial goals…

Alex and Jamie Want to Retire Early, Too

Alex and Jamie also learn about the 4% rule, and both anticipate needing $40k per year in income for retirement.

They each take different routes to reach FI…

Alex realizes they have a $500k net worth and are exactly halfway to their FI number of $1M. Alex plans to knuckle down for another 5 years, putting all excess savings into their after-tax brokerage account. With compound interest on their existing retirement savings, it’s a quick journey to the $1M. Yeehaw!

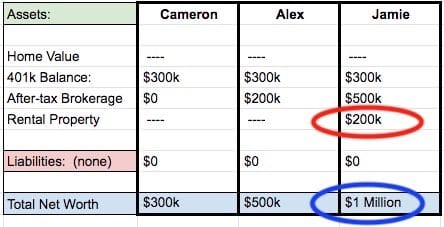

Jamie has the highest net worth out of them all, at $800k (excluding primary residence). Being fairly close to achieving true financial independence, and still relatively young, Jamie decides to do something a little unconventional…

Jamie decides to rent out their primary residence, and travel abroad for 4-5 years. Jamie has always wanted to live in South America, volunteer, and already researched 5-6 cities there that offer a comfortable lifestyle for around $35,000 per year.

Jamie quits their 9-5 day job and buys a 1-way ticket to Panama.

Now that Jamie’s home is no longer a primary residence (it generates rental income and monthly cash flow), the house can be added back to their net worth statement as a “rental property” asset…

Since Jamie now has $1M in net worth made up of income-producing assets, and only needs ~$35k in retirement income the next 4-5 years, they have achieved temporary financial independence living within the 4% rule.

Sometimes Including Home Equity in Net Worth Is a Good Thing

From the scenarios above you might be thinking that adding your primary residence as an asset in your net worth is a bad thing. But, there are definitely benefits to tracking your home equity:

First, it helps track your mortgage paydown and progress, and overall debt to equity ratio. Over time, your house increases in value, and the mortgage slowly decreases in value. It’s fun to watch your equity grow organically, and it’s motivating to track constant progress!

Banks, lenders, and potential business partners like to see ALL your assets included in your financial statement. The more assets you include, the better financial health you appear to be in, and the more favorable you look to do business with. Tracking everything is a good thing in the banking world.

Lastly, even though your primary residence might not be income-producing right now, it might become part of your investable net worth later. Recall Jamie’s scenario above… assets can change in purpose over time, so it’s good to track everything and always consider your options.

Should You Include Your Primary Home in Your Net Worth?

All in all, this is something everyone can really decide for themselves. I think the answer strongly hinges on what you are using your net worth report for.

If you’re tracking your progress to financial independence, and retirement is your sole goal, be careful about including assets that you can’t rely on for retirement income. If you include too much dead equity, you could be artificially inflating your progress to FIRE.

I’m curious to hear what you readers do. Or maybe you keep multiple net worth tracking sheets? It really only takes a few minutes to update – why not do both!?

Get blog posts automatically emailed to you!

Joel,

Thanks for sharing this analysis!

I see how not adding your home can help you be more accurate in terms of tracking your overall net worth number when it comes to the FIRE movement. To date, I’ve always included my home (asset and liability numbers) to give me a better overview. However, it’s always a good reminder to only look at the assets that can bring you a consistent income stream versus a home, which likely will not.

Thanks for this information!

Fiona

I think that’s why it’s maybe a good idea to remind yourself *why* you’re tracking your NW. If it’s to track assets and growth over time that’s one thing. But it’s not a complete future expected income report.

Happy Holidays Fiona! Have a great week buddy!

Very impressive that Cameron paid off his $700k home :)

We don’t include our home value in our net worth calculation. As you said, we can’t use it to pay for any of our annual expenses. But also, I think the value of the home (based on websites) is subjective and can easily change. Plus, if I actually sold my house, I would probably pay additional fees to the realtor, etc., reducing the asset value even more.

I hear ya! It’s good to know your expenses are lower because of owning the home. And not tracking it cancels out the added expense if you didn’t own.

It’s funny about realtor commissions and taxes, etc… Because I track the current assessed value of my rental property. But in reality, if I sold them, the cash valaue would be a lot lower because of these fees. Should I be adjusting for that in my NW report? Something I’ve been thinking about recently.

Great article! I like the graphics and examples.

I offer everyone another perspective. that is in the line of “Millionaire Next Door” book by Thomas Stanley.

What if you buy a modest home ($ 300,000) and pay it off by the time you reach 40. At the same time you max out your retirement accounts so that you have $ 1,000,000 saved.

Now it is time to retire. The advantage of the homeowner over the “renter” is your cost of housing is ZERO.

What are the 3 main basic things any retiree needs – 1.) Shelter/Housing, 2.) Food and 3.) Medical. If you can eliminate 1.) then all you have to do is worry about 2. and 3.

Meanwhile, the average rent across the County is $ 1,200 a month and rising. What happens when you are 10 years into retirement and your rent is now $ 1,700 per month? With a paid off house you can control future “housing costs”.

Also, what about reverse mortgages? You can retire and tap into the equity in your home if you need too. So, I think your primary residence is an “asset” for sure, and a powerful one at that to control future costs and tap into via a reverse mortgage if need be.

Merry Christmas and Happy Holidays everyone!

Yes the reverse mortgage is absolutely a tool people can use later in life! Thanks for bringing that up.

The thing that you mention about rent… This is one of the reasons why a) I am not sure what my actual FI number is (because I don’t know what future rent is) and b) why even if I hit my FI number I’d be a little scared of retiring without owning my home. The good news is I have years to figure out this problem, and I don’t want to make home purchases in Los Angeles when I don’t know if I’ll be here long term.

I love how you said “eliminate #1.” That’s a great goal, and love everything in the Milli Next Door book too! :)

Happy Holidays and Merry Christmas to you too!

I absolutely include our house value in net worth but only because I have other subtotals to account for compounding assets. Here are those figures from Saturday morning, for instance:

In the market: $576,590.60

Retirement total: $531,968.28

Net Worth: $897,836.42

…this neatly breaks out what’s invested and earning returns, what we can’t touch for another nineteen years without IRS shenanigans, and what we’ve accumulated in the course of our lives. Net worth doesn’t impact planning — it just provides a sense of accomplishment.

(I suppose it’s time to talk with my wife about throttling back 401(k) contributions in favor of after-tax investing, if we’re going to FIRE without morbidly relying on inheritance.)

I’ve heard rumblings that the 401k scheme may be changing. Don’t want to change topics but but depending on your income level it might be good to switch to doing more after tax investments anyway.

As for Net Worth – CONGRATS on nearly topping the $900k mark. I love how your track 3 totals so that you’re not over/under inflating your numbers. Great work!!

When you’re older, you have to plan for being unable to live independently. If I have $2 million in investments ($80k a year using the 4% rule) while I live in my own house. If I could get $500k out of my house, that means I could have $100k a year for my years in an assisted living situation.

That’s a GREAT way of looking at it. Your home is absolutely an asset which can be converted to income upon moveout. Brilliant example – and one that I’ll hopefully live old enough to use one day!

This was super helpful, thanks!

You’re welcome Amelia! I think there’s a bunch of ways to look at it, but ultimately everyone gets to do it however it makes sense to them and their situation. Have a great week and happy holidays!!

VERY interesting read.

For my Net Worth, I DO include my primary residence.

I do so in order to track my true Net Worth. Living in NY, my area causes my house’s value to fluctuate (mostly up). I also have some business ventures and investments that require your net worth to be ABOVE $1Million. In those cases, they DO account for your home.

I wanted to point out a few items to consider:

– Once your home is free and clear… you are NOT really free and clear of expenses. A primary cost is Real Estate Tax. In my case, that alone is about $1,000/mo. Insurance, repairs, utilities are another concern.

– In your example, IF Cameron, Alex, and Jamie all have the SAME house (cost-wise), then it would also stand to reason that Cameron would have the smallest remaining mortgage, Alex, the 2nd least, and Jamie the largest. The point here is that these remaining balances would result in remaining monthly mortgage payments. On the other hand, IF they did NOT have the same COST for their houses, then Cameron would also likely have had the “nicest” house, Alex the 2nd nicest, and Jamie the most modest.

– At retirement, each of these fellas COULD sell their respective house and convert that capital into an income-producing asset(s). This could play into the financial picture in different ways.

I think what should be used TOGETHER with the NET WORTH report is a PROJECTED INCOME report. This report would fill in the blanks where the Net Worth falls short.

In summary, the Projected Income report lists all your remaining years on this planet on one axis. EACH income source on the other axis. Note that income likely will change year to year. Examples:

– Social Security WILL kick in at some point… put that in.

– At retirement, one might decide to SELL their house and convert to a Dividend Producing Portfolio with an estimated return of 5% (not to mention any growth of the underlying stocks). Put that in.

– You may be beneficiary of inheritances…put that in.

– You may own a business that you intend to sell. Put that in.

– If you worked at a company, union, or agency that ALSO gives a pension… put that in.

– Also put in any reduction in salary (perhaps a recession hits?, you take a chunk of money out of an income-producing asset to buy a boat, etc.)

– If you are still working, account for raises / promotions. (As well as scaling hours back to prepare for retirement

– I am sure I missed other sources…

In summary, I include my house as an asset.

Quick shout out: I really enjoy the Budgets are Sexy posts and website. Thanks for taking the time to keep this going.

I surely could have written this better, so pardon any misses in thought or grammar.

MERRY CHRISTMAS and HAPPY NEW YEAR to all!

Hey Ugo! I love a long and detailed reply. :) This is where all the juicy details come out! My scenarios definitely glossed over each of the annual expense breakdowns (on purpose). There’s a ton more that could be added to the story.

I like this Projected Income Report you speak of. And how the NW report ties directly to that. I’ve used some softwares in the past, OnTrajectory is one i liked, which allow you to add income in future years with new sources (like Social Security, etc). They also let you add larger expenses for future years (like lump sum tuitions of giving money). All in all, proper retirement planning must be done before someone just hits a specific number on their NW report and calls it a day. :)

Cheers for the shout out. Happy Holidays!

I get NOT wanting to include it, but at the end of the day it’s an asset that you own (or owe). I include my vehicle as well which I know is sometimes frowned upon. Am I going to sell the car (or home if I didn’t rent)? Not likely. But I could! I actually signed up for Personal Capital a while ago and, since I already track my net worth via Mint and in a separate spreadsheet (a little overboard, I know), I only have my investments/cash on there.

I include my car – but it’s probably only worth like $7k and compared to my overall portfolio it doesn’t make a huge difference. I agree – the home is an asset and should be tracked as one as it “could” be traded for cash value. :) Cheers IF – you’re not overboard, 3 different tracking methods is standard in our crowd ;)

I also include my vehicles in my net worth. Then every month I depreciate their values by $100 until they fully depreciate. That way when I buy a my next vehicle it creates a smooth transition.

That’s actually a great idea. It’s not like a liability (because it’s worth something irl) but it does slowly take money out of your life each month. Kind of like buying a declining stock. Thanks for sharing Al, I like this idea!

I like to include all of my assets and liabilities in my net worth. However, we have a bigger savings account that we are using to save up for some remodeling projects, vacations, and to pay for our next car in cash. So I then include a separate line at the bottom that just sums up my retirement investments. This way I can see our whole picture but then also see how much we have set for retirement.

Love it! Seems like a great way to go and the best of both worlds. I like that you’re siphoning off money for repairs and remodels. That’s a huge part of home ownership that many people forget :)

Great article, and is something I have thought about in the past. I actually find myself separating my Financial Independence(FI)/Retirement number, from my Net Worth number, although the former is definitely part of latter. My primary concern is retirement and financial independence, so I specifically track those assets which contribute to that goal, the positives, retirement accounts and brokerage accounts, and the negatives, credit card and auto loan debts, a quick note, my house is paid off, so in my mind is neither a positive or a negative, but not having a house payment is nice. I think we get too caught up in the whole Net Worth number instead of looking at the FI number, although saying you’re worth a million dollars is quite an achievement, and make for interesting party conversation among like minded folks. Just my two cents about looking at things a little differently

Great way to look at it Bob. Things that add, and things that take away. It’s important to track both. In fact, that’s also why a lot of people include their cars in net worth tracking – it’s an eye opener looking at a depreciating asset over time working against your wealth building.

Congrats on your house paid off! And I agree that $1M net worth should be celebrated no matter what assets are underneath the covers :)

We rent out a floor of our primary house as an airbnb, so its definately an asset.

But it doesnt really matter after all, if you look at our numbers:

Assets: 1 400 000€ (Primary house 500 000€)

Liabilities: 160 000€

Cash: 25 000€

Retirement fund: 25 000€

Furniture, car etc: 20 000€

We live in Europe so other laws and advantes. We kept everything stupid because we just want to invest in things we know/ understand.

We are totally FI and have been so for the past 6 years, and still our neth worth has only gone up, so Im happy with everything :-)

Congrats on FI and having a great start with increasing NW! Love that you are able to Air BnB a room – it’s the best of both worlds. Post-FI House Hack! :) Merry Christmas and thanks for sharing! Stay safe over there! Joel

We weren’t including ours either, but it just feels a lot nicer when it is. Sort of gives a high – so we turn it on and off on personal capital as and when we need a mood booster. But we do realize it does not generate any income, and so can’t be used post FI.

For that matter, you couldn’t even use your 401K (w/o penalty) if you’re retiring early. So I guess how you calculate your net worth is upto you. May be someone should come up with a term to indicate just that.

How about IGNW (Income Generating Net Worth)? Or Gofi’s IGNW in my honor, if you would please, I wouldn’t mind at all.

Haha! Another acronym to remember :) I do think if someone is truly planning to retire before traditional age, they should probably thinking ahead and figure out where withdrawals will come from. The earlier you start thinking this way, the less surprises will come later. Merry Christmas Gofi!

Here’s my usual answer to proteges:

*sigh* By definition, yes, the primary home you own is included in your net-worth. Now let’s work out what questions you should have been asking instead ….

That’s a great answer – because it opens to a better discussion about *why*. Cheers Joseph – Merry Christmas!

I included our primary residence (which we sold in nov) in our net worth. For the estimated worth of the house I was very conservative ($275,000) and I used that number because we had that much money into the house ($100,000 between reno and 20% down payment and $175k financed). We sold the house for $375,000 and ended up netting over $110,000 profit. Our investment panned out. We are now renting until we get orders for our move this August (husband is military). My website has a breakdown of our monthly net worth. It has been very helpful keeping track of it.

That’s awesome, Liz. I think underestimating home value is a great idea in general. If it’s sold and converted to a cash asset, there’s fees and cap gains that are accounted for. Just checked out your blog and DANG!! Congrats on the 50% net worth increase over the last year!!!

Thank you! My husband’s enlisted in the military and I’ve been a stay at home mom for 6 years. I now have a job on Saturdays were I bring in $300 a month. We have just saved away and got lucky with our house flip as well

Really interesting to see primary residence used both ways, hadn’t really thought about the downsides of including it!

I guess the impact is much worse if your home is the majority of your NW. If it’s only a small part and you have a bunch of other assets, it’s not that much of a difference. :)