Before we get to the net worth update… I came across this funny old post from a couple years back called “Money Trails”…

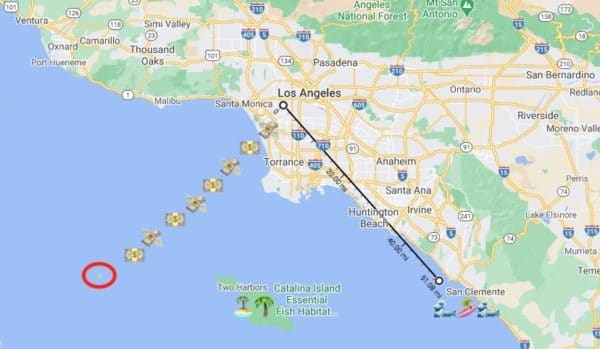

Basically, it tells you how far your money will let you travel if you line up all your dollar bills, lengthwise, in a single long straight line…

Here’s how it works:

- Convert the length of your dollars (6 inches per $1 bill) to feet… $542,510 = 271,255 ft.

- Convert feet to miles… 271,255 ft = 51 miles

- Google map a radius of 51 miles from your home and pick a location

- Imagine laying all those dollars end to end to that location

From my home in Los Angeles, it looks like my money will take me down to my fav surf spot in San Clemente! Or, if my dollar bills could float (and I could walk on water), I could visit Catalina Island or that other tiny little remote island in the middle of nowhere on the left…

Unfortunately, I’d need a net worth of $26,252,150 to make it all the way to Hawaii. Or more than $35 million to visit my brother on the East Coast!

What a fun (and utterly useless) perspective on measuring your net worth! I’m curious… How far can YOU get with your current dollars? Here’s the original post if you want to check out instructions.

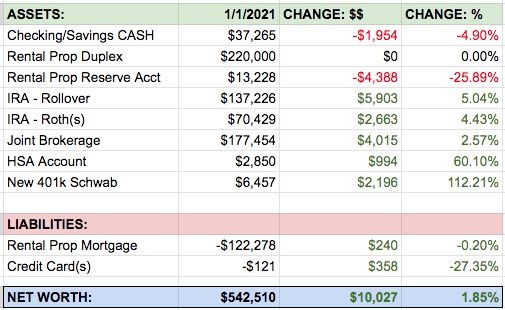

Jan 1 2021 Net Worth Update: $542,510 (+$10,027)

Sweet! Another $10k bump since last month’s report!

Here’s the account summary, as well as growth shown in dollars and percentages for each asset we’re tracking:

December Abnormal Expenses…

We stayed in Los Angeles for Christmas this year to comply with our lockdown orders. Although not traveling saved us a few bucks, we still had some hefty December spending — and a negative savings rate. 🙁 Here are the major things that hurt our wallet:

Tax bill paid for rental property: Technically this $5k bill wasn’t “due” until the end of January, but I hate having outstanding bills just sitting around so we paid it early. This was paid with our property reserve account, and tax isn’t due again until next January.

Christmas presents, a tree, food, and booze: We dropped another $600 or so this past month on presents (+ a tree!), in addition to our November gift spending. Our grocery bill was pretty killer this month ($627) which is quite high for a family of 2. But, some of these were fancy meats and stuff we don’t typically buy, plus contributing to family meals for Christmas. My birthday was on Dec 30th and my wife made a special beef wellington with expensive filet mignon – delicious and worth every dollar!

Lower income for school holidays: My wife isn’t paid as a salaried employee, so we miss paychecks over school holidays. Thanksgiving and Christmas breaks total over 3 weeks of missing pay! This is one of the reasons we sit on a large emergency cash fund, to see us through dips in income like this. Summer break hurts the most, which we’ll tackle somehow in a few months when the semester is coming to an end.

December good stuff and wins!

Stimulus payments, $1200: We got our stimulus payments on Dec 31st – a nice little way to end 2020. We qualify for these checks because we have less than $150k in combined income.

Teacher appreciation funds: Because my wife is such a kickass teacher, the families and students gifted her a total of $365 in vouchers and cash this Christmas! Thank you to all you parents out there who gift money to schools and teachers. I can’t tell you how well this is received by teachers and how much it makes them feel appreciated. THANK YOU.

Trash turned to treasure: Out on a morning run, I came across a compost tumbler that someone was throwing away. I snapped a pic, created a free ad on an app called OfferUp, and someone picked it up a few hours later for $40!

My conscience got the best of me the very next day… I noticed more free items and furniture out front of that same house and learned the people there were moving houses. I can’t imagine how much it sucks moving homes during a pandemic, so I ended up giving the $40 to the family as a moving present.

This is why I’d be a horrible business owner – I have a problem giving my profits away. At least I have a fun story to tell, and maybe some good karma down the road somewhere. 😉

Detailed Asset Breakdown:

CASH Accounts: $37,265 (-$1,954): We skipped a paycheck from my wife’s job this month, and also transferred some cash into our HSA account. This cash balance is trending downward, which is OK as it’s still higher than what we really need for our emergency fund.

Rental Property and Reserve Account: $233,228 (-$4388): We paid our property tax bill which accounts for $5,185 of this expense. Our positive cashflow was $797, which is the difference between $1,975 in rental income minus $1178 in total expenses. :)

IRA – Rollover: $137,226 (+$5,903): The increase in this account was solely from market growth and reinvested dividends. Someone asked me about why I don’t do a backdoor conversion of this account over to our ROTH… and the answer is that we plan to in future years. More to come on this topic!

IRA – Roths: $70,429 (+2,663): I’m excited to contribute to these Roths again in January for 2021. The plan is to transfer funds from our joint brokerage over these accounts to begin tax-free growth as early as possible within the year.

Joint Brokerage Account: $177,454 (+$4,015): I made some large buy/sell trades within this account in late December. Due to our low income in 2020, we were in a good situation to do large capital gains harvesting. Although we’ll pay a small amount of state income tax, we’ll pay 0% in capital gains tax and reset our cost basis for a bunch of stocks. At some point I’ll do a deeper dive into this account and explain what all that crap I just wrote actually means.

HSA: $2,850 (+$994): The increase here came from an after-tax contribution of $887.50 (prorated contribution for 2020) and the rest was market growth.

New 401(k) at work: $6,457 (+$2,196): This 401k has been only open for 3 months, so I’m proud that there’s already $6k in there. I get zero company matches, so this is mostly personal savings and a tiny bit of market growth.

Breakdown of Liabilities

Rental Property Mortgage: -$122,278 (+$240): If my calculations are correct, this mortgage balance will be less than $120k at the end of 2021 if I just leave everything alone. I could speed things up by making extra payments myself… but why do this when the tenants are paying it down naturally each month?

Credit Card Balances: -$121 (+$358): Other than this small credit card balance, my wife and I have no other consumer debt. :)

Overall, 2020 was a very good *financial* year for my wife and I. Since we only started sharing these monthly net worth reports in October last year, I can’t really give a complete and full 12-month comparison and overview. Something I promise I’ll do when I’ve got enough data!

How were your updates the past month? Share your milestones and juicy details in the blog comments — boasting is heavily encouraged! 🏆🏆🏆

Have a great weekend, peeps!

– Joel

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Happy belated birthday Joel!

That beef wellington with filet mignon sounds amazing and I can certainly believe that it is worth every penny.

Congrats on the 10k bump in your net worth. I’ve seen my net worth grow a bit as well, especially with the recent market performance.

Keep up the incredible work.

Fiona

Thanks Fiona. Congrats to you too! :)

end to end, huh?

It looks like I could go almost exactly 70 miles to a town called Lockhart. :)

Cool! Just looked it up, looks like a cute little town! :)

2 questions:

1. are you not including your primary residence in your net worth?

2. why would you leave Australia, isn’t that just CA stretched out?

1. We are renters where we live.

2. I fell in love with an American girl. So, i’m kinda stuck here now. :)

I haven’t really tracked net worth in the past but got curious this morning how “2020” went for us financially.

The snapshot for a family of 5 (age 38) with gross income of about $150k.

Our net worth increased 24% from $460,000 to $570,000.

Cash holdings are about the same so it’s mostly due to contributions and growth in our retirement and college savings accounts–all systematic monthly contributions for dollar cost averaging, so none of this is from crazy buying during the March or anything.

We had extra income this year from the 1st stimulus ($3900) and a 1-time inheritance of $8k but also had a few major cash outlays: $10k new roof, $5k other home improvements, and paid $1200 to refinance mortgage in March, $1500 vehicle repairs. Maxed HSA contributions for the first time ever with a v. low-cost medical year.

Net worth includes our only liability of a $161k mortgage that will be paid off in 12 years. Home worth $275k and didn’t factor in any change in value. No loans on vehicles and not included in assets.

Both kept our jobs, lost a few fringe benefits and won’t get a pay increase this year, but thankful our monthly income remained steady. We are steady-savers, nothing too extreme. Kids are in lots of activities and we don’t plan to retire until 55/60, so we are not the lowest spenders. Enjoying life while saving for the future.

It was a good practice to track this – thanks for the motivation!

This is so cool to hear. Slow and steady wins the race. Extreme lifestyles (frugality or spending) aren’t sustainable in the long run in my opinion. So it’s awesome that you’ve found a balance that is both saving for a solid future, as well as enjoying family life as much as possible along the way.

I like that you started tracking and paying attention to net worth numbers. Congrats on passing half a millie! Things get very fun and interesting from here! :)

I love the distance math. When I saw your map and the line drawn out in the ocean, I asked myself “I wonder how much is needed to get to Hawaii?” I had a good chuckle when I did the calculation on my own and then saw that right below the map you did it yourself! Great minds think alike!

Haha love it. Probably will never make it to Hawaii, but I’ll probably get to Mexico in a few years :)

Congrats on a very good financial year and thanks for sharing these deets with us. I’m so excited that for the first time since we started tracking it, which would be back in Jan 2019 when I first found FIRE we have a positive net worth!! It’s not big, only about $6,000 but that is HUGE for us. Have slowly been paying off debt and the thing that finally put us over the hump this year was selling our camper trailer in December. We owed $16,000 on it but no more! Yay positive net worth! It’s a great way to start out the year for us.

YAAS!!!! Proud of you – that’s such great news. Congrats! What a great way to start the new year!

Our checking and savings increased just over $1,000 despite the same big spending. Having three extra 20-something humans for two weeks put a dent in normal savings. Most of that is for my Tesla fund!

Our Roth and IRA was up $17,700. About 2.4%, not bad.

Our mortgage principal went down about $800 from the regular monthly payment.

Thanks for asking. I looked at net worth increase for 2020 but didn’t really look at just December. A good month and year overall.

Great to hear, Stef! Funny you mentioned the extra humans. Whenever I visit my parents I somehow turn into an eating machine like I was back in high school. :) Other people’s fridges have way more interesting things in them!

Congrats on the good December and good year. Have a great weekend!

NW increased by 0.8% for December, up 9.5K.

It was a good year. NW rose $139K to 1.14M.

The increase puts me at a 14% increase for the year.

Not bad for being largely out of equities for the whole year.

Wow Gene, that’s awesome and surprising you were out of mostly not in equities. Curious if you’re keeping this position carrying though 2021?

I’m roughly 5 years away from retirement. The current valuations are lofty enough that it makes me too nervous to stay in the market and risk a significant drop which would require me to delay my retirement until the market had largely recovered.

I can miss out on some additional growth and still retire on schedule. But if the market were to crater me, I would have to wait it out.

I’ve considered the possibility that the recovering economy may bring GDP up and therefore make the market valuations more attractive to me without a “crash”. And if GDP recovers while equities remain steady, at some point I’ll start getting back in. Maybe when the Buffet Indicator drops back down to about 120%.

It may be splitting hairs, but I’m trying to value the market vs “time” it. I took the last installment out of the market when the Buffet Indicator pushed past 150%. I didn’t start reducing my positions until it had gone over 130%. The only time it was over 130% prior to that in my lifetime was just before the 2000 crash. Currently it is over 190% Yikes!

If I miss out on some growth, so be it. And I’m even ok with that. I consider that “loss” the same as paying insurance that ensures I won’t have to delay my retirement plans past my “sell by” date.

Interesting! I’ll be honest – I had to google what the Buffet Indicator was! :) Can’t blame you for trying to preserve capital, it’s more and more important as you come closer to your retirement date. Most people find it hard to give up good returns for less risk, so I’m glad you’re doing what’s right for your personal situation!

I wasnt impressed with my distance! It was hundreds of miles but that isn’t far for a distance runner. When I add up all the actual miles I’ve run its right at 23,000 miles. It’s going to take a long time to save up that much distance.

Try this Steve… Break your wealth down into pennies… 100 x pennies is longer than 1 dollar bill, but the same value. Each penny is .75 inches, so 1 dollar is 75 inches. I’m too tired right now to compute into feet and miles, but you’ll find you’ll go probably 10x the distance your bills will take you? :)

PS. holy moly 23,000 miles!!!? You’ve nearly circled planet earth?

My net worth is mostly Bitcoin, so I’m up about 100% in December and about 400% in the past year. After the Christmas lambo, I’m still up a few hundy. Might diversify into blockchain crypto, but I’d love to hear your thoughts. Thanks Joel for all you do!

Congrats Ben! You are a smart investor. I do know of a secret crypto fund that I just heard about… Super small right now, but it’s gonna blow up massively this coming year. It’s called Joelcoin – let me know if you want to invest and I’ll give you the account number to transfer all your money to. :)

Happy New Year, Joel!

2020 was a good year for net worth. We ended up ~13% year over year in December.

We did, however, decide to give away a chunk of the gains by funding our first donor-advised fund. This allowed us to donate appreciated equities and also realize a nice tax deduction for the year (which is welcomed since we also sold off an appreciated rental property too).

Wishing you a healthy and prosperous year ahead. :)

Awesome, Michael! That’s one of my goals this year – to set up a donor advised fund. I’ll have to hit you up and pick your brain about the process. I was just gonna transfer cash, then invest it. But now that I think about it, appreciated lots of stock is a way better move. I’m still scratching the surface of researching this stuff!

Congrats on the Net Worth gain my friend! And exiting the rental in a hot market!! :)

Congratulations on the NW increase! And a great way to end 2020 indeed with stimulus checks. It’s like Christmas 2021 came 51 weeks earlier than normal.

My 2020 was OK.. when I started the year I was on track to increase my NW by 100 – 200% but then the pandemic ended and I only increased my NW by 50%. Smaller numbers such as my NW have an easier time climbing up than higher numbers like yours, ha.

I am hoping 2021 will be the year everyone can safely socialize and actually do stuff. But then a new strand of COVID could happen so who knows.. We shall see!

Good work David! 50% is awesome, congrats! I too am looking forward to this covid stuff being more under control so we can get out and start being comfortable around stranger again :) We’ve got it pretty bad here in LA right now, apparently 1 in 5 testing pos. :(

But you could have had another $40 on that net worth! Haha love that story, hopefully some good karma coming your way. Cheers to a fruitful 2021!

I’m actually quite proud of myself… The old Joel 10 years ago would have given them $100 as a moving present, instead of just $40. So breaking even is actually something to celebrate :) Cheers to a good year IF!!