What up, what up! Another month, another net worth update! You tracking it diligently yourself over there? Even if you’re keeping it to yourself like a normal person?

I hope so.

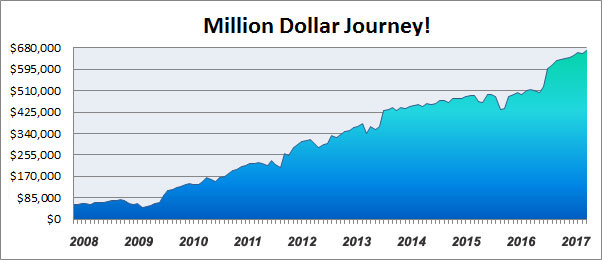

I honestly can’t even put into words how impactful it’s been in my own journey over here, so I won’t… Instead, I’ll show you a picture :)

Of course, tracking itself doesn’t grow your money, but what it DOES do is get you thinking and paying attention to it more which is the key to everything.

You have to have your mind right first before you can start taking action! Then once your dreams and values and overall “why” is locked in, you can hit turbocharge on the game plan and ride high on all that motivation…

I thank my lucky stars every day I started paying attention to this stuff over 10 years ago… Which I owe completely to this same financial blogging community here from people sharing their net worth reports too! It all just clicked, and the second I decided to start my own blog I knew that the one thing I’d make sure to do is share my numbers as well no matter how ugly or awesome they were.

And now, 100+ months and net worth reports later, here we are :) So hopefully it sparks something in at least one of you guys as well!

If you ever start doubting, just remember this:

Haha… It’s not always easy or fun – as you can see in my own dips up there, as well as the red marks in today’s update – but so long as you can look at your #’s and see them trending upwards over time you know you’re at least on the right path :)

And then we get to go back to what we truly care about in our worlds – our lives! Money is only a tool, never forget! The real goal here is to not have to think about it one day!

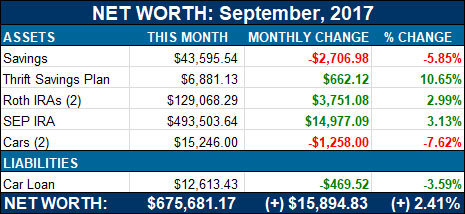

Here’s How September Broke Down…

These updates would probably be pretty boring if I didn’t mess up from time to time, eh? ;)

CASH SAVINGS (-$2,706.98): I made a big goof this month – I forgot about quarterly tax payments! I’ve been so loosey goosey with my cash flow ever since watching my kids part-time that I completely forgot about that whole “tax thing” (as well as other errands that’ve been building up – yikes). I don’t know if you’re allowed to blame your kids for your own stuff, but I’m going to do it anyways since they’re not old enough to call me out on it yet ;) Still, time to get my ass in gear!

THRIFT SAVINGS PLAN (TSP) (+$662.12): Another hefty increase here courtesy of Mrs. BudgetsAreSexy who continues to diligently (and automatically) contribute to her retirement account since taking her gov’t job last year. It’s the best when you do it from Day 1 so you don’t even feel the difference in your pay check each time! Highly recommend!

ROTH IRAs (+$3,751.08): Another plump increase here as well, courtesy of the market… We’ve been hinting for months that it’s all going to come crashing down at some point, but somehow it still has room to grow it looks like… But don’t be fooled, it will happen! So get those game plans and emotions in check! The doomsayers will be flooding the streets!

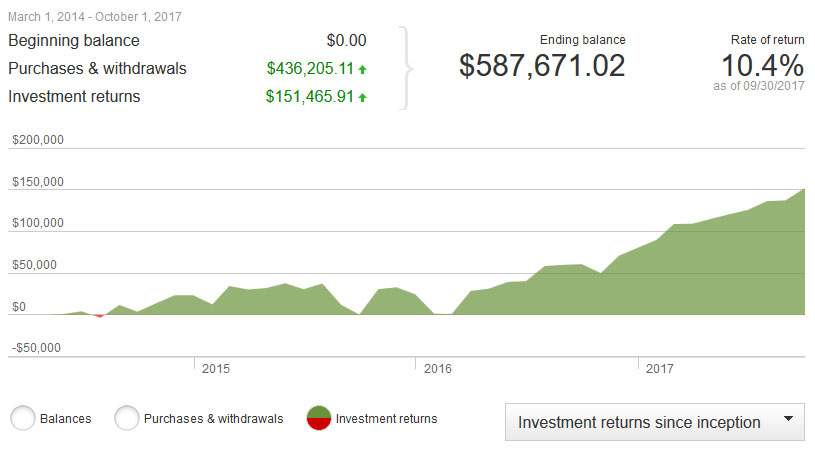

SEP IRA (+$14,977.09): Same with this area too – nothing new added, just the markets doing their thing. We still have most of our money in Vanguard’s VTSAX fund and plan to for years and years to come. Here’s what that performance has looked like since we moved our money over a few years back:

CAR VALUES (-$1,258.00): A bigger hit than normal because I dropped my car’s “condition” down a notch due to that fire hydrant fight it just had to get into ;) We’ll bump it up again later if we end up getting it fixed and looking shiny again, but for now it is what it is and we keep on moving forward…

Here are the values of both our rides per Kelly Blue Book:

- Lexus RX350: $11,539.00

- Toyota Corolla: $3,707.00

CAR LOAN: (-$469.52): Slowly going down each month! And a big change from last year’s $19,000 or so it was at when we first picked up the car (Lexus). The goal is to have it paid off within the next year, if not sooner if we come across a nice chunk of change… We just love having the cash padding since most of our income is still tied to my fluctuating blog income here.

And that’s September!

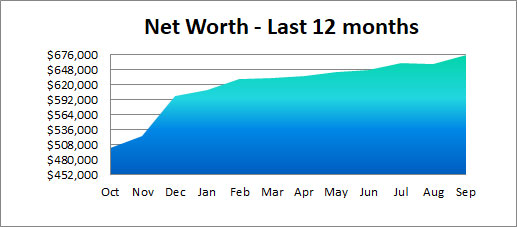

Here’s a zoomed out snapshot of how the past 12 months have gone in our household:

And then, as always, the kids’ net worths… because that’s fun to track too :)

Hope your journey is going well also! And you’re doing a much better job than I am in the cash-flow department! You can find all 100+ of our net worth reports here if you want to drill down into certain months, or click here if you want to see how other bloggers are doing in our industry.

For perspective, I rank #102 out of the 420 net worths we’re currently tracking :) Use it to connect to other bloggers around your same range!

Upward and onward,

![]()

FYI: If you’re wondering where Mr 1500’s post is today, we’re actually hitting pause on his column for a bit while he catches up with a few things and re-assesses all his hopes and dreams ;) Apparently early retirement can get even busier than having a 9-5, who knew? We love all his stuff though, so hopefully he’ll be back soon and in the meantime you can catch him over on his own blog at 1500Days.com. Go get’ em, bud!

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

I have tracked net worth every month for the past 6 or 7 years since finding your blog. I spent many hours also going back to capture historical data so I have a picture of my net worth since 2009. It is an invaluable tool to help someone like me, who needs to keep this stuff in mind, stay on track. Last month the gains were enough to buy I nice mid-tier SUV…. Don’t get me wrong, it won’t be all peaches and cream. I have been around for .COM bust, 9/11, and 2008/2009. So I EXPECT it to get hammered.

Rock on!!!

Love that you went back in time to grab some historical stuff too, haha… I did the same thing when I first started :)

So cool you’ve been reading the blog for that long!

We’ve been tracking our net worth for about 6 years now. We’re a good ways behind y’all, still early in the process. But I do love seeing the upward trajectory!! :) It’s a great reminder, in the middle of all the saving and frugality, that we are on the right track. It’s nice to know that.

PS. They’re your kids… you can totally blame things on them like that!!! :)

Awesome job and you continue to kill it. I’m sorry to see Mr. 1500 is taking a pause though. I love reading his stuff. Hopefully he starts back soon.

Agreed – he’s a terrific blogger. Was nice to have the 1-2 punch going too of someone working *towards* independence (me) and then someone who’s already *made it*. Hard to argue with someone who’s living the dream (though I certainly tried with some of his posts, haha…)

Big thanks to both of you for the kind comments. I need to get some projects out the door and then we’ll see what life feels like after that.

No matter what happens, I had a great time writing for BAS and I’m incredibly thankful for the opportunity.

Onward and upward! Just without me for a bit.

Hope to see you back soon! Definitely subscribing to your site as well. As J mentioned, you do pair nicely as one of you has hit your early retirement goal and the other is on the way.

Congrats on the net worth increase. That chart over the last year is really impressive! I watch our net worth like a hawk but my husband is more creative and less spreadsheet, so we have a net worth update together at the end of each year. That’s when I get to fill him in on our increases. I really look forward to sharing our awesomeness with him.

Keep up the great work and thanks for being a financial inspiration!

Mrs. Mad Money Monster

Congratulations on your NW increase, I love the onwards and upwards chart! I’ve also been tracking it for over 10 years and ghetto style in a small notebook (and also on the blog). Yes, and some of us older millennials remember the crash. I didn’t know what I was doing at the time and sold things off alongside everyone else. Ready to hunker down and click buy instead of sell when it comes!

Notebook net worth – love it! Whatever does the trick!

Congrats on a nice jump in your net worth! I’m so sorry to hear about the fire hydrant. We got a few dents in our new Toyota Corolla too, but they weren’t major. And we didn’t want to spend money fixing those dents, so our car is not at its best @_@

Hey thanks for sharing your update and congrats on another good month! Quick question: Why do y’all carry the car loans when you have money in savings to pay them off. Tell me to mind my own business if that is too personal of a question. Thanks!

No worries at all, my man – total open book here :)

We keep the car loan because we like the feeling of having a nice padding of cash saved up, especially as my income always fluctuates. It also feels good knowing that we *can* pay it off at any time as well, making the debt sting less :)

I agree that when it comes to your net worth, from month to month, it may not be up every period. However, if the general trend is up, then you have nothing to worry about.

I got to admit that I have been tracking my net worth religiously too for the last ten years. It’s wasn’t so much fun at first, but for the last couple of years, it’s definitely fun.

Even though nothing has changed in my life after I hit the $1M net worth, but my mental state had changed quite a bit. It gave me more motivation to hit the second million.

It took me ten years to hit the $1M net worth mark. However, it took me about one year to hit the next $0.25M after I hit my first $1M.

I would recommend everyone to start managing their money if they haven’t started their journey.

Wow man – you’re doing a helluva great job over there. Super impressive!

Well, September was a big bump up for me. It had a third paycheck (5 Fridays in September, and getting paid every two weeks). And while I hate working storm duty, I had plenty of overtime from Hurricane Irma. As a salaried employee, we don’t get paid overtime except during a named storm. So, those 19 hour days add up.

And the stock market was running well.

All in, an addition bump of $12,000. I thought I might hit $360,000 (nice round number), but ended up at $359,000.

I don’t know what you do for a living, but thank you for doing it! Sounds like you come in handy during these nasty storms!

Looking good! The only thing your family could do better is to increase the TSP contribution. Any plan on that one? Great job overall.

Not while our cash flow is a mess :)

The markets are being quite kind right now ;) We saw a healthy boost in our NW this month, but much of that is due to a strong bull still charging along!

Nice net worth increase J$! Solid progress.

Of course the market won’t behave like this all the time, but never the less — good progress saving!

I’d like to hear more about how you decide how much to put into the 529 plans. We have a 5 and 3 year old and recently starting stepping up the 529 contributions based on several online calculator projections.

I just put in as much as I’m able to, really :) When things are good we throw in some nice chunks, and when things are not we stop. Currently we’re doing $50/mo automatically into each of their accounts just to make sure we’re doing *something* vs nothing, so I’d def. recommend at least doing that if you can. But really, I don’t have any master game plan going at the moment… My babies are never leaving me anyways!!! :)

Great job! Because of you, we have been tracking our net worth and guess what? We hit $1 million in September! This is the only place I am allowed to talk about it though since we have “stealth wealth”. No one knows that we have some cash! haha. I will be 39 this month and our goal, or at least mine was to it $1 million before 40! Yay!

Now I need a new goal?? Any ideas?

SWEET!!

Yes – now go start a blog to share all your tips and tricks with the world :)

I need you staying busy while I try catching up to you! Haha…

lol! I don’t know if I’m up to the blogging task! Maybe if my husband will help me with it, it could be done!

You will catch up, no doubt!

It is amazing how success compounds (at least in a rising market). We hit 1 million in March and are on track to hit 1.25M by the end of the year (maybe even at the end of this month)! The first million took us a little over six years — I know because my daughter was born the month our net worth first turned positive (we had a lot of student loans). The next million shouldn’t take us much more than four, unless the market tanks, which it very well might.

Oh yeah – I like to say the first $100,000 is the hardest and then it’s all just watching it compound from there :)

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

Nice update!

So when do you think will the market “correct”? Will it correct at all, or do you think we will go into a sideways market for a long time?

I am from Europe and I have the feeling that lots of people are just eagerly waiting for the big collapse/downturn.

If a downturn happen, what do you think will trigger it?

Kind regards

Harald

I have noooooooooooooooo idea on the hows or whens or whys – nor am I smart enough to guess! – but all I do know is that it WILL crash at some point and I pray we all are ready to embrace it without freaking out :)

Good job on the Net worth, it is eating over there at Vanguard. 100K plus in returns is insane. Iv been with vanguard for over 10 years now. 700 k is only a hop skip and a jump away. Peace Brother.

J. –

Getting plans ready for the up or down swing in the market is key, as you said it. I wouldn’t mind dollar cost averaging down or picking up higher yield in the down market. Not paying attention to the market values is the tough part for all. Time is taking care of quite a bit for you and sometimes & sticking to your plan, that’s all that’s needed! Nice job J, talk soon.

-Lanny

I think it would be interesting to see a zoomed out shot of your graph (though the zoomed in shot is very interesting too:) because it would emphasize those dips you refer to. “What must he have been feeling in 2009?” Looking at it today, 2009 is nothing more than a blip (because that’s what it was), but at the time, you must have been wondering in what direction things were headed. Your graph illustrates what I’ve heard: The first $100 K is slow in coming, but things speed up after that. A nice little $14,000 jump in your investment portfolio? I can see why things speed up! Here’s to more of the same, and a strong navigation of the next recession, whenever it hits.

That made no sense. Sorry! What I meant was that it would be interesting to take a slice of your graph – say, from 2009 – to show that one period of time – even a whole year – does not tell the whole story. Too many of us have a history of being discouraged by what seems long but really is the short term.

Yup! Totally get that… If I were tracking investments only or was with Vanguard for the entire time I would totally go take a screenshot and hit you back :) Unfortunately i only moved to Vanguard 3 years ago so all we have to look at is Net Worth in general which includes everything, but as you can see from the bigger chart way up top – the dips are def. there and indeed blips :) Every now and then i’ll read a report of mine from 2008 or 2009 though and get sucked right into it again – pretty wild!

Hah I’m glad you didn’t break open the hydrant, that one would have been hard to sneak away from with your dignity intact.

Your net worth reports always make me wish the conclusion on my blog was to share the full net worth story in its gore and glory. Would you believe that most, if not all, my readers don’t want to know our real numbers? I asked the people and the resounding answer was “keep it to yourself”! Humph. So much for being all open about money.

I guess it saves them the mini heart attack when they don’t have to see how much we spent this year but it’s hard to celebrate vague milestones.

HAH! That’s exactly why I never poll anyone with what they want or don’t want to see here – I’d have stopped blogging years ago if I couldn’t just do whatever I wanted to do :) Though certainly I probably lose a ton of readers as well going this route…

Ahh the baby penny + baby nickel chart idea is adorable! Congratuations, these kiddos are financially better off than than 50% of all Americans! (Um… sorry came out a little sad…)

Hey, J. Dog!

Great news you shared up there at the top of the page. Glad to see things are growing for you.

I haven’t done a formal review of our NW lately, but I kind of keep a mental mind about it.

Our biggest change in NW come’s from the Market, and it’s been growing pretty well, as of late.

Hope it keeps doing so.

Now that we’re in the 4th quarter of the year, I need to dust off the old Spread Sheet and run the number again.

Unfortunately, our NW is going to take a good sized jump in the next few weeks.

I say unfortunately, as my Wife’s Mom passes and my Wife and her sister will be inheriting there Mom’s estate, which is worth a bit.

Oh well, it’s part of life. Eventually our to Kids wiil inherit our estate.

Keep on keeping on, Dude.

Looking forward to meeting you at FinCon!

I hear ya man – the circle of life/money!

Very much looking forward to shaking your hand this month – you’re one of the top people I want to meet in person :)

I like that bump! My September was expensive, thank you dentist/TMJ, but I really feel like I’m learning a ton right now and that should pay dividends, too.

We are the same age with growing portfolio’s. As you consider future market drops and “staying the course” I would be interested to know what your asset allocation is, or your plan for that as we get older. Do you have an IPS?

I have nooooooooo idea what an IPS is, but as of now I still plan on sticking 100% into the total index fund w/ VTSAX regardless of what the market does. Then maybe in a decade (or two?) as I get older, diversifying more and picking up bond and/or international indexes as well.

I do like a lot of the 3-fund portfolio options people do with Vanguard indexes, just right now trying to be as aggressive as possible since I don’t plan on touch it for many years to come.

Just found your blog after doing research on Google and wish I had found it months ago!

Quality content and actual practical advice.

Congrats on your growth this month and previous month/year.

Going to check out the personal capital tool you recommend.

Thanks

Thanks for the kind words, Mark :)

I love seeing graphs up and to the right, and that’s exactly what a net worth calculation should look like.

But I’m glad you’re always mentally prepared for a market crash. As I tell friends and family, the p/e ratio of the market right now is nuts. Companies are returning about 2-3% of their capital in returns right now, which is super low. Honestly I’m not sure if the market will correct itself for awhile. Everyone is told to pump their money into the S&P500, which means they aren’t looking at metrics like p/e while investing. The only criteria is “big”. If something comes along and causes people to divest in their 401ks, like job shortages or housing market crashes or something, then we might start to see a dip and a panic as a result.

Is your SEP IRA a traditional or roth ?

Traditional… I didn’t even know you could have a Roth SEP? Haha… awesome.

hi.. i just found your website and love it.. can you link me to the articles you have written on the possible market crash you talk about in this article.. also do you do any type of case study.. I would love to have your perspective on my situation.. Thanks

glad you’re enjoying the site! I haven’t blogged about the market crash specifically, I just know it’ll come and at that point we all gotta be prepared :) we don’t do many case studies on the site, but if you wanna share it in our forums I’m sure people will chime in with thoughts?

http://forums.rockstarfinance.com/