Bugger! I just found out my rental property in Texas needs a new roof!

There was a nasty hail storm last month that ripped through the area and smashed a bunch of cars and houses — unfortunately, my rental property was one of them. 🤦🏻♂️

The good news is that nobody was hurt, and insurance will cover the replacement roof cost (~$10k). The bad news is I still have to pay the insurance deductible (~$2k) and figure out the claims process and stuff.

Surprisingly, dealing with insurance isn’t as bad as I thought it was going to be. Since it’s my first time filing a claim like this, I thought I’d share some notes, numbers, and things I’m learning along the way. This might give any new and aspiring property investors out there some insight into what it’s like being a landlord.

But before we get to the boring stuff, here are some fun facts I just learned while googling hail storms. Did you know…?

- There were 4,611 hail storm events last year (2020) in the US. 🌨

- 601 of them were in Texas! By far the most of any other U.S. state.

- ALL these events had hailstone balls larger than 1 inch in diameter!

- About 24 people each year are injured and go to hospital for hail hitting them 🤕 Ouch!

- And sadly, 4 people have actually been killed by hail in the last 20 years.

- The world record for the largest hailstorm was in 2010 near Vivian, South Dakota, where 8-inch diameter (~20 cm) hailstones fell from the sky! Daaaaang!

This is the hail that hit my rental. The biggest stones were about the size of golf balls!

When Disaster Strikes Your Rental Roof, What Happens Next?

My property manager emailed me and said there had been a huge storm in town the night prior. Whenever this happens, she gets a million phone calls from every roofing company in town asking if they can go out and assess all of the roofs of the properties she manages.

Because roof assessments are free (or at least that’s how it was offered to me), I was glad to have someone go out to see if there was any damage at my duplex.

It’s pretty cool actually … roofing companies these days use drones that fly over the house with cameras to look for damage. They can zoom in, take photos, and sometimes even provide a repair quote the same day.

For my place, they determined that a whole roof replacement was necessary. There were no massive holes or water leaks into the house (thankfully), but the shingles were bashed so hard by the hail they need to be replaced.

How Insurance Claims Work for Your Rental Property

I’m no expert in this area. (And actually this is a great side note for new real estate investors — It’s OK if you have no clue what you’re doing… Owning rental properties is mostly about figuring stuff out as you go along. As long as you ask good questions and are willing to learn, every problem you come across is figure-out-able.)

Clueless, I called the 1-800 number for my insurance company (Travelers), and asked about the claims process. Here’s a simplified overview:

- They ask basic info about the disaster.

- 24 hours later, a claims person gets assigned.

- The claims person schedules a visit to the property.

- They write up a report and tell you how much $$ they think the damage will cost.

- They send you a check for that amount (minus deductible and stuff I’ll explain in a bit).

- You use that money to fix whatever happened.

- If the repair cost ends up being higher, you call back and ask for more money. If not, you’re all good.

Pretty simple, right?

How Much Insurance Will Pay for My Roof Replacement

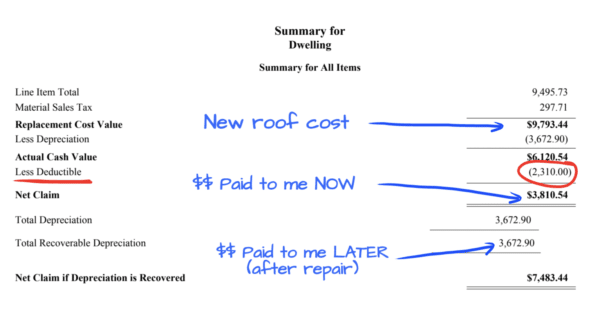

My claims dude also used a drone to assess the roof. He emailed me this assessment and summary afterward, and also called me to walk through and explain it:

The depreciation line item can be a little confusing. But really all you need to know is that it is “recoverable.” Meaning it still gets paid to you, but only after you go ahead and complete all the repairs. The adjuster posted me a check for $3,810, and I’ll get an additional $3,673 after the roof is fixed.

All in all, my total out-of-pocket cost should be $2,310 (which is exactly my policy deductible). Kind of a bummer that I’m out 2 grand, but it only puts a small dent in my $15k+ rental property emergency fund!

What to Ask Your Insurance Company If You’re Thinking About Filing a Claim on Your Rental Property

Since this is my first property insurance claim, I took the opportunity to interrogate my claims guy and ask him as many questions as possible. Here are the main things I asked, as well as his responses:

How bad is the roof damage? Do I need to replace it right now? (I asked this to understand if there was a time limit in which I needed to make the repair). He said there are no holes or leaks into the units, and advised me to hold off on making the repair until *after hail season is ove.r* Great advice! He said there is actually no time limit on my policy to make a repair.

If I file a claim, will my insurance premium go up next year? Unlike car insurance, property insurance typically doesn’t go up for your individual policy after a single claim. Property insurance rates are more tied to the general area and fluctuate based on how many claims are filed in the whole region. (This is nice to hear, but honestly Texas and my small town have been getting hammered the past 12 months with disasters. My insurance premiums will go up regardless, so I don’t really know why I even asked this!)

What if the new roof costs like $20k, instead of $10k? If my new roofing quotes come in any higher than the estimate I was given, I can submit them to Travelers, and they’ll adjust my claim. The max I will pay out of pocket should be my deductible — $2,310.

What if the new roof cost is *lower* than the estimate? If I can repair the roof for less than the $10k, Travelers will actually lower my second reimbursement. It doesn’t matter how low or high the repair cost is — I will be out of pocket $2,310.

Can I choose the roofing company? Yep, I get to handle the repair and choose the company to work with. (Well, actually my property manager will do this).

Is the new roof cost tax-deductible? And do I pay income tax on the insurance reimbursement? THIS is such an interesting grey area… I asked the claims person, who quickly said I should consult a tax professional. But, from my initial research online it looks like a) I do *not* pay income taxes on the $7k reimbursement checks, and b) I *can* claim my new roof repair as a deduction for property expense. Seems shady — I’ve got a call with my tax guy this weekend anyway and I’ll bring it up.

Whelp, that’s it for now! Happy to answer any questions if you have any, or if any of you experienced real estate peeps have advice for me on how to handle this insurance crap better – I’m all ears!

TLDR Summary:

- Hail storm smashed my rental property roof! Booo.

- But property insurance is covering the repair. Woohoo!

- I’m only out ~$2,300 (my policy deductible)

- Waiting until Aug to do the repair (when hail season is over)

- Reminder to all: Owning a rental property is not really “passive income” because it actually requires work/effort to maintain.

Have a great week!

– Joel

Get blog posts automatically emailed to you!

Happy Friday Joel!

Sorry to hear about your roof… that’s never fun. At least you have a cooperative insurance company that seems to make the claim filing process fairly easy, so that’s definitely good news!

When I first read about the cost of roof repairs, I was astonished by how expensive they can be! It’s incredible to see how expensive roofs can be.

By the way – I can’t even imagine an 8-inch diameter-sized hailstone!!

Cheers,

Fiona

I’m definitely surprised how easy it’s been to work with Travelers! I hope they don’t drop me after this :(

Another good reason to wait until hail season is over if possible is that roofing companies will not be as busy, demand will not be as high, and some may offer incentives to complete your roof which they wouldn’t during the time of year they are in demand. In 2016, when the ZOMG Hail storm seemed to rip up half of South Texas, I HAD to have mine done as it crashed through my skylights. I was at the mercy of any roofing company’s time schedule on the first-come/first serve emergency. Some people with damage that could wait had to wait almost a year for availability.

Questions for your roofer you/your property manager needs to have for you are:

How long is the roof warrantied for? Do they have a guarantee on their work? What kind of lifetime roof are you willing to pay for based on the number of hailstorms that go through.

PS – Did you own this home in 2016? Was the roof damaged/repaired/replaced then? If so, was anything warrantied? That does not disappear with a new homeowner. Would this be covered, even partially, under that warranty?

Hey SL! Yes we owned this place in 2016 and I recall a storm back then but there was no damage to the roof. Great questions about the new roof warranty and whatnot – I will ask when finding the new contractor when we’re ready to replace.

As far as busy roofers and costing more… from my understanding even if it does cost less in a few months, I will still be out my full deductible. The insurance company won’t let me ‘profit’ from this claim. I’m going to wait regardless, but cost isn’t my concern.

One thought on home insurance claims. My uncle had the unfortunate situation to have multiple natural disasters hit his home in a relatively short period of time. After the second claim, his insurance company dropped him and he had to get the expensive “untrustworthy person” insurance for a few years until he could get back on the normal one. He asked my cousin, who sells insurance, about that and my cousin said that is the industry standard. So just be aware if you’re making smallish claims and maybe save your two claims for the big expenses.

Thanks for the advice Laura! It’s funny how insurance is supposed to help you sleep better at night… but the more I read and learn about this industry, the *less* good I feel about it all haha.

I was going to make the same comment. I used to sit next to a colleague who was a former claims adjuster with many years of experience, and he gave me the same warning when I had to file for my roof damage in 2017. I ended up with a full roof replacement, as well. I just made sure to have an arborist come out that year to assess the 4 Bradford Pears that were on the north side of my house, since they were nearing the end of their short life spans and are known to develop rot spots and split in large chunks. One was likely to strike part of the house if what we were looking at did turn out to be a rot spot. Such a claim would have resulted in our insurance likely being dropped. (We ended up having to have the trees removed in late 2019, and only just now planted new trees). That being said, we did everything right, but the insurance company still decided to mostly pull out of the state and out from the agent who wrote the policies here about a year and a half later. So, we ended up having to pay for higher rates anyway since we had to find another insurance carrier and had the claim on our record. Once it falls off we will more aggressively shop around. As far as being out the deductible, our roofer offered a cash discount (completely legal) and we actually didn’t end up out any money. Our deductible was $1000, though. I think it still worked out well in the end, since our roof would’ve otherwise cost $10K (ranch home). Best of luck to you on your roof replacement. It was fun to watch the work.

We’ll see how it all goes. I have multiple policies with this provider, I’m not sure if that makes a difference price-wise but if I have to change ins companies I’ll probably swing all my policies over at the same time.

Good call on the “cash discount” – I’ll ask when I start getting quotes, although I’m not sure it’ll actually help me pay less than the full deductible.

Cheers J!

Yep, Texas is getting pretty well known for its natural disasters. I live in the Houston area and we get hit by hurricanes (and the recent freeze) all the time. I can’t wait to retire and moved to San Antonio to get out of hurricane alley! Of course then I’ll have to worry about hail storms. I guess there is no city safe from natural disasters anymore?

According to Redfin…. “Detroit, Indianapolis, and Buffalo are among the least disaster-prone cities to live in. What’s more, these are also among the most affordable for housing”.