Found this list skimming through some old journals last night and couldn’t help but smile :)

First – because it’s just so dang nerdy!!

But second – because it’s amazing what can happen when you actually put things down on paper and then GO FOR IT.

We’re still a ways away from hitting that Double Comma Club, but it’s fun to see how many of these we can now cross off after 11 years of paying attention. Something I completely owe to this financial community here which really woke me up and forced me to realize just how important this stuff is. Especially in getting started *early*!

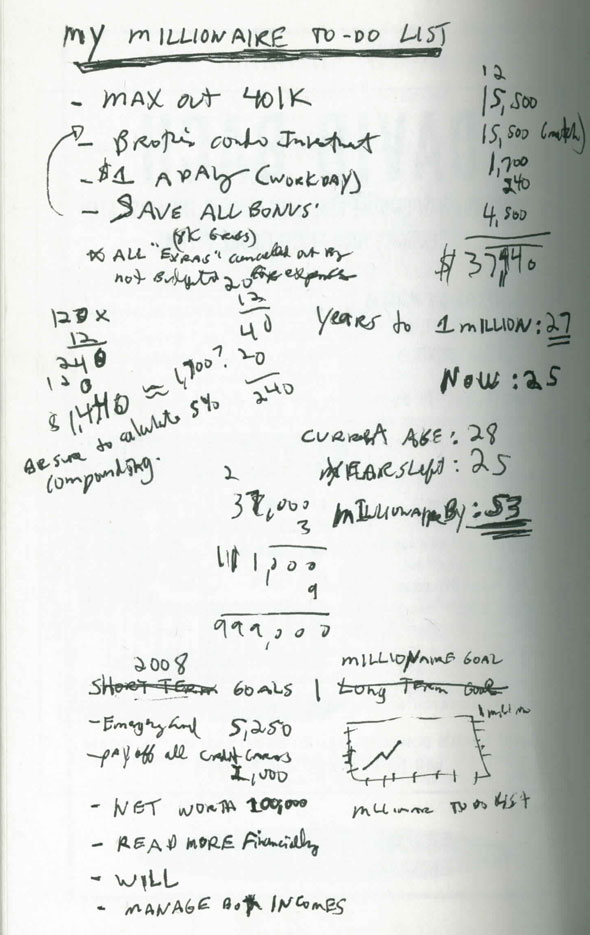

Here’s a copy of the game plan from all the way circa 2008:

Fun to see that top half there when I was scheming to eek out every last dollar from that insane 401k plan back then, as well as other things I’ve long since forgotten:

“Brother’s condo investment” – This was actually a loan I gave my brother when he first bought his condo, but I guess since there were monthly payments coming in to me every month it *felt* more like an investment, haha… He eventually paid me back in full earlier than expected, so I probably only made like $20 of interest off it ;)

“$1 a (work) day” – This was one of my earlier experiments to try and save even more every month, and my guess is that I chose to only do this on *work* days since it fit my daily routine of reading blogs in the morning while at work, and also while I had spare change on me from eating out almost every single day ;) I would have been better off just saving the lunch money, but hey – baby steps! And it opened up the gates to dozens more challenges over the years which I still to this day enjoy doing…

“Save all bonuses” – I’m still rocking this bad boy, though it’s more like saving “extra money” that comes in vs “bonuses” since my current boss is a real a-hole and never gives me any… ;) (for those new to the site, my boss is ME, haha…)

“Years to 1 million” — 25!! Wow!!! Crazy to see how drastically that was cut down over the years, even with contributing much less than $37k most times… Who knew we were right around the corner from one of the best comebacks in the stock market’s history though! Something I purely lucked out with on that one… (though at least I was smart enough to be investing when everyone else was freaking out! Haha… Another benefit of paying attention to money blogs back then! :))

“Current age: 28” — Oh to be in my 20s again! Haha…. I’d give most of it all up to gain 10 years of my life back ;) So long as I can keep my memories and kids! Something good to keep in mind whenever you catch yourself comparing your $$$ to others though – especially to millionaires and billionaires. They may have more money than you right now, but they’re also decades older!! And I bet if you ask them to trade it all back they’d say yes in a heartbeat too.

*****

The second half of this page is also pretty interesting – at least to me ;)

Check out this list of “2008 goals” I was aiming for as if I could really pull them off that year, haha…. (PS: I didn’t!)

Emergency fund: $5,250 — That $5,000 was ALWAYS the hardest for me to hit! It just seemed like so much money at the time, and then as soon as I started investing it only made it harder since more of my money would end up going there instead… Probably because it was much more fun to do than just add it to “savings” :)

Pay off all credit cards: $2,000 — I was never horrible with my money before stumbling across finance blogs, but I wasn’t ever *great* at it either. I was closer to Even Steven with things, with some months having extra money, and others down a few hundred… When I scribbled this one it looks like I was currently down, probably with the upcoming wedding just around the corner…

Net worth: $100,000 — The 2nd hardest number for me to hit! But boy does it speed up from there once you cross that threshold, wow… Here’s a post I wrote on it once which explains why I think that is (and still do to this day): Why the first $100,000 is the hardest

Read more financially — Still doing that one to this day! But have to remind myself that just because you *learn* something, doesn’t always mean it’ll have any real effect on your life/finances. In order for that to happen you actually have to TAKE ACTION or it’s just stuck there in your head! So if there’s something you’ve been over-educating yourself about lately, please for the love of all momentum, DO SOMETHING about it right now!! Yes you’ll probably mess up and it’ll be scary and weird and unnerving, but better to be living it out in the real world than in your head all the time! Some things can only sink in once they’ve become a reality!

Will — And speaking of realities, this is still the ONE major fail in our financial lives, although I swear to you it’s on our list to knock out next month as soon as we’re moved in… You might recall I got serious about this a year ago with Baby Dime coming into the picture, but alas we didn’t want to deal with the hassle/costs of setting it all up only to re-do it again when we moved states, so we decided to risk it for one more year and then knock it out ASAP once the deed had been done. Quite literally ;) And now we’re 3 weeks away to that so you can hold me accountable so long as I still remain alive!!! Knock on wood!!!

Manage both incomes — This one took us a few years to finally get around to, but we did end up combining it all and it’s been rolling smoothly ever since :) Mainly because I *love* managing our money and my wife *doesn’t’* haha… I don’t know what would happen if we both wanted to be in control?!

And that catches us up to today!

A lot has changed over the years, but a lot hasn’t as well. I still max out my retirement accounts every year because it’s the foundation of our wealth (as long as you do just that one thing you will be fine over the years!!), but long gone are the credit card bills or even drooling over what it would be like to be a millionaire one day.

Having more money is nice, but what’s nicer is waking up to your ideal lifestyle and not even thinking about the money! Which is ironically where we’re at now!

So that’s the biggest takeaway here, at least for me… Realizing that I now focus much more on my LIFESTYLE than I do the bank account, even though of course it’s still humming there on the side…

I really do think this line I often repeat here is incredibly true: Life > Money > Things! Teen-me wanted the things, 20s me wanted the money, and now 30s me very much just wants to enjoy The Life :) We’ll see what 40s me wants around the corner, but I can tell you it won’t be chasing the money anymore, that’s for sure…

If anything, I’ll probably be chasing my youth!! Haha…

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Dude, write that will!!!

Come back next month and it will be done!

Maybe you’re using the term “will” generically, but I highly recommend you to look into a trust instead

Yup! I was… We plan on getting both a will *and* a trust going here shortly…

Time to do this thing RIGHT, once and for all!

Please do write about both the will and trust (am sure you will), but i waiting for that post to get information from you to get things going on my end as well :)

thanks in advance

DG.

Just do the will now (plenty of free and cheap options online). Do it for the kids. Seriously. Don’t let perfect be the enemy of a good start (that will make things so much easier on your family).

Do the trust once you move.

It’s fun looking back. Unfortunately, I’m not quite the historian you are, J.

Initially 10 years ago or so, I was just starting to be more interested in retirement and was just thinking in terms of knocking 2 or 3 years off [from 65, maybe 62 or 63].

But I was able to find a note from about 5 years ago that had moved up my anticipated retirement to 58. However, the 58 had already been crossed off and 57 was written in. It is about the same time I got much more into actively planning [thanks in no small part to this very blog – Thanks, J!]

My current plan now has 55 as my “fall back” position. I’ll likely have the $$ to retire by about age 53 depending on what the health care options are at that time. If I do just a little bit better than I am anticipating, I might even be able to punch out at 51.

– Here’s hoping!

Well you know I’m rooting for you, sir!

Maybe you should write down “49” on a scrap of paper right now to really put it all out there! ;)

:) I love your enthusiasm!

However, 49 is only 4 months away and I’m not quite ready yet.

Also, if I walk away before 51 [when I qualify for retirement @ my company] I’ll be leaving $33,000 in retirement healthcare benefits on the table. Sticking it out another couple of years to keep that seems reasonable.

Okay okay, 49 1/2 then ;)

So great! We found our 1st “Debt Snowball” list from 2005 ! Eye opening for sure!

Heyyyy very cool!!! I want to see please! :)

I love a good list! I was planning on finishing my KonMarieing/MarieKondoing (?!) on Friday and part of that process will be cleaning out the old journals I have in a box under my bed from when we moved two years ago. I wonder what I’ll find…! Sometimes I find old To Do lists and old goal lists and find that I have, indeed, checked most things off. I feel like writing them down solidifies the intention somehow. I haven’t made a big goal list in a while (Damn you Netflix download feature! Some of my best list writing what done on long haul flights after I’d ran out of movies!) but I think I need to! And I need to write a will too. Good reminder!

Writing things down def. makes things more real! Same with telling someone about them too, especially if they’re the type of people who will keep bringing it up and asking you about it later, haha…

I’ve been writing monthly financial updates (now including net worth) in my journal, so they will be around to look back on. It’s already fun to look back on past references to money, like an entry from college (~ four years ago) in which I was eagerly looking forward to the paycheck that would put me over $1,000 in the bank, or an entry from high school (~ 10 years ago) where I was excited at the prospect of having “way more money than I thought”– $430– left after buying my first laptop. (My grandpa had given me $200 toward the laptop– “THANK YOU AMAZINGLY, GRANDPA!”)

Not sure what future me will think of my short term plan from a couple months ago that I totally did not stick to… (Basically I changed which goal I was going for at the last minute.)

Love it!!! That’s a lot of tracking over the years, such a great habit :)

You’re not the only one putting off doing the will. We need to get it done this year too. Ugh..

It looks like you found the ideal formula: Life > money > things. It’s great and you won’t need to change it anytime soon.

Make a commitment to do it along with me, please!! That way it’ll be a lot more fun than sucking it up all by myself! :)

Great list J Money! Part of me wishes that I had written down my plan when I started this journey — but part of me likes that it has been an ever evolving process as my outlook transforms in the face of new information. Yay! the fundamentals haven’t really changed much for me – reduce expenses, grow income and save and invest as much as I can. I do think back to when I first started and remember getting excited about getting to that first $10k. Now it seems so far back in the rearview mirror haha

I did something similar back in 2014 (not even that long ago, but kinda is?) but I scribbled a bunch of goals and steps on scrap paper when I was trying to get my financial sh!t together. A lot of it had questions marks because I had no friggin’ clue what I was doing or if it was the right move. It’s cool to look back and see how far I’ve come and what I’ve learned since. Good to know I’m not the only on keeping scrap papers related to finances and investing!

I think you should share it on your blog too! :)

So cool, J. Reading back through old journals is so fun! And sometimes cringey, but not in this case :)

I have a few pages like this from back when I was trying to figure out how much to stow away in my 401k. It feels pretty amazing just a few years later to be able to max that baby out!

– Jules

Well a hearty congrats to you too, then! I think you should now write about it on your blog :)

This reminds me of some of the old excel spreadsheets I sometimes stumble across. Although my 08’ Mac just died do I probably won’t have to bear the embarrassment of some of my crazy ideas back then. Almost amazing how fixated you can get on something, then look back at it with a totally different perspective.

Haha yup….

But I still think you should break out that hard drive to recover those puppies so future you can have even more laughs ;) I did it recently with all my old computers and it wasn’t too hard to figure out!

https://budgetsaresexy.com/learned-getting-rid-of-1-thing-every-day/

It’s always great to review old lists and/or goals and see how much we evolve! I would say you’ve evolved nicely :)

The first $100k – I’m getting there and it is a slog but it seems way more fun then the intense debt pay off I did.

Life > Money > Things is an awesome inequality!

If you can crush all that debt you can DEF soar through to $100,000! Not worried about you in the slightest there :)

J $ – need you to share your knowledge, tips and experience regarding wills. I still haven’t done one since I moved States. I also need to push the parents to update theirs.

Regarding writing down goals, I do but I don’t keep those pieces of paper so I can’t go back and compare – thinking I should start keeping them for the fun of going back in the time capsule and see what I thought and where I’ve gone financially over the years!!

Yeah!! It’s fun – try it out! :)

And will do re: wills… as soon as we sit down to start knocking them out I’ll be sure to write about it…