If you’re getting tired of reading about my finances all the time like I am, today you’re getting break ;)

IT’S TIME FOR ANOTHER ROUND OF “OTHER PEOPLES’ MONEY“!

WOO! 💰💰💰

Our series where we showcase snapshots of other peoples’ money in our community, from the older, to the younger, to the single, to the married, to the fabulously wealthy – all in an attempt to broaden our perspectives better.

Last time we featured a Hebrew software engineer on the site, a traveling ICU Registered Nurse, a millionaire who doesn’t feel like a millionaire, and a 64 year old real estate investor who used to be homeless and penniless just 18 years ago, and is now a budding millionaire herself!

The time before that we featured a newbie financial advisor, a risk taker who loves to invest gamble in bitcoin and poker, the budget of my wife circa 1995 (hah!), and then a woman from Kyrgyzstan who only needs $808/mo to live off (!!!).

And today should be just as juicy :)

Up on the docket: a 33 y/o with 3 kids all under the age of 3, a breadwinning pharmacist mom, a 43 y/o half-a-millionairess, a married couple with a million-and-a-half, and a pair of 60+ year old GDINKs (Gay, Dual Income No Kids) living out in the San Francisco area.

All comments and constructive commentary welcome!

******

Snapshot #1: The 33 y/o with 3 kids all under 3!

Background:

J$,

I just wanted to share some good news and say thanks because you certainly contributed to my success!

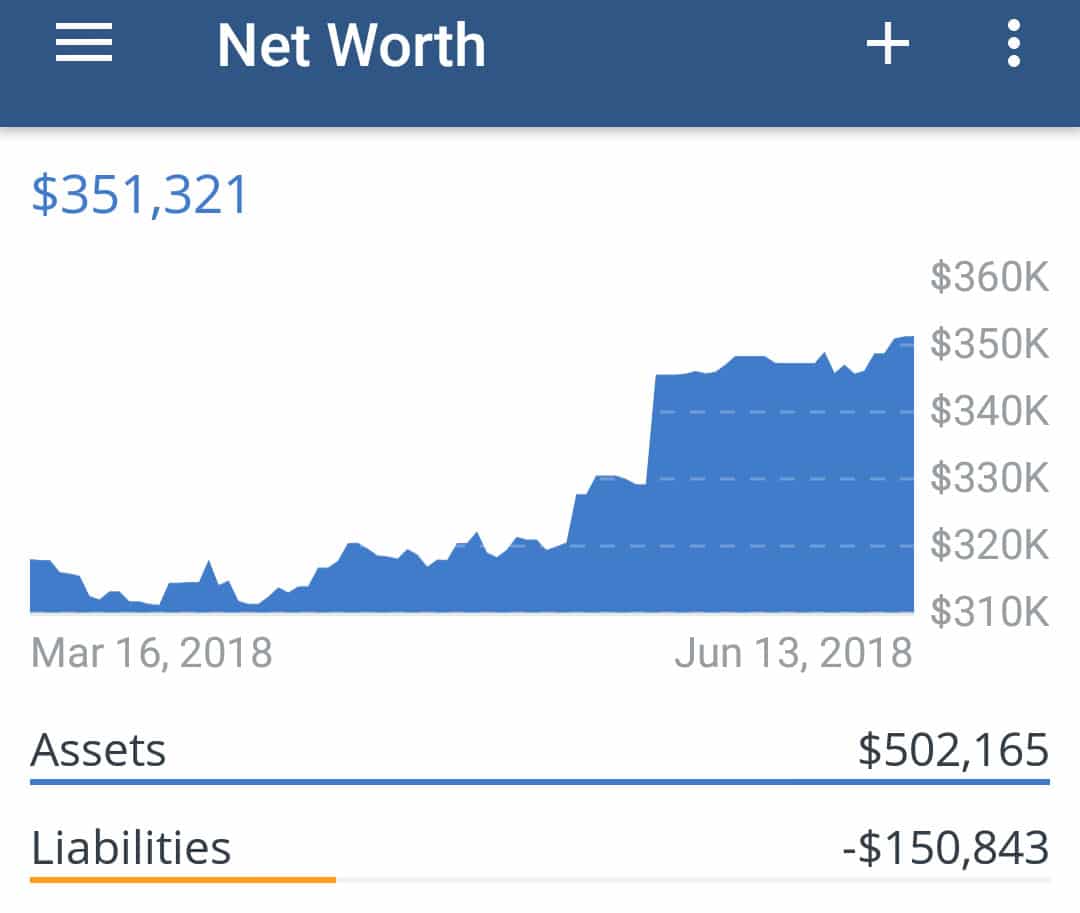

I hit the $500k in assets milestone!! ($353k net worth)

A few quick facts:

- 33, married with 3 kids age 3 and under

- One income household

- Paid cash for the last 3 cars I have bought (the last car I bought was $7,200 paid in cash with leather seats, sunroof and an amazing sound system!) That is an interesting story in itself. TL;DR: I think it was involved in a crime at some point before I owned it…

- Only debt is $147k mortgage at 3.1% with 19 years left

- I have never ‘budgeted’ in my life I tried using YNAB for about 3 weeks before I called it quits

- I max out 401(k), 2 Roth IRAs and an HSA every year (for the last 2-3 years)

- It was definitely a combination of hard work and luck. Luck in that I found a job during the financial crisis in 2008 that was in an industry that not only wasn’t struggling, but at the time was flourishing with lots of opportunity for growth, thereby allowing us to buy a house at a ridiculous price with an insanely low interest rate.

My salary progression went something like this:

- 2008- $28k (not a typo…first ‘adult’ job after college)

- 2009- $29k

- 2010- $30k

- 2011- $50k- new job (during the interview they straight up asked me what I wanted to be paid and at the time I thought that was an astronomical amount…)

- 2012- $57k- new job

- 2013- $62k- promotion

- 2014- $73k-raise

- 2015- $81k- raise

- 2016- $88k- raise

- 2017- $100k- new job

- 2018- $120k- new job

Over that time I worked my @$$ off getting my MBA, and 4 professional certifications, but I do attribute a lot to being fortunate enough to work for good companies.

I picked up a ton of habits/tips/motivation from you and others in the personal finance blogosphere. Thank you!!

– Anonymous

PS: the spike you see in the chart attached is just bringing in accounts to Personal Capital

PPS: other salient facts: in the 8 months leading up to our wedding we paid off $18k in credit card debt because we wanted to start fresh without anything hanging over our heads. We celebrated with a $4 bottle of champagne :) Additionally, I paid my entire MBA out of pocket as the company I was working for didn’t offer any tuition reimbursement.

That salary progression is incredible!! Job hopping gets a bad rap with our generation, but it’s hard to ignore when you see numbers like that..

Also love the $4 champagne celebration, haha… I had to tweet that out when I read it, and within hours it got over 100 “likes” :)

******

Snapshot #2: The Breadwinning Pharmacist Mom

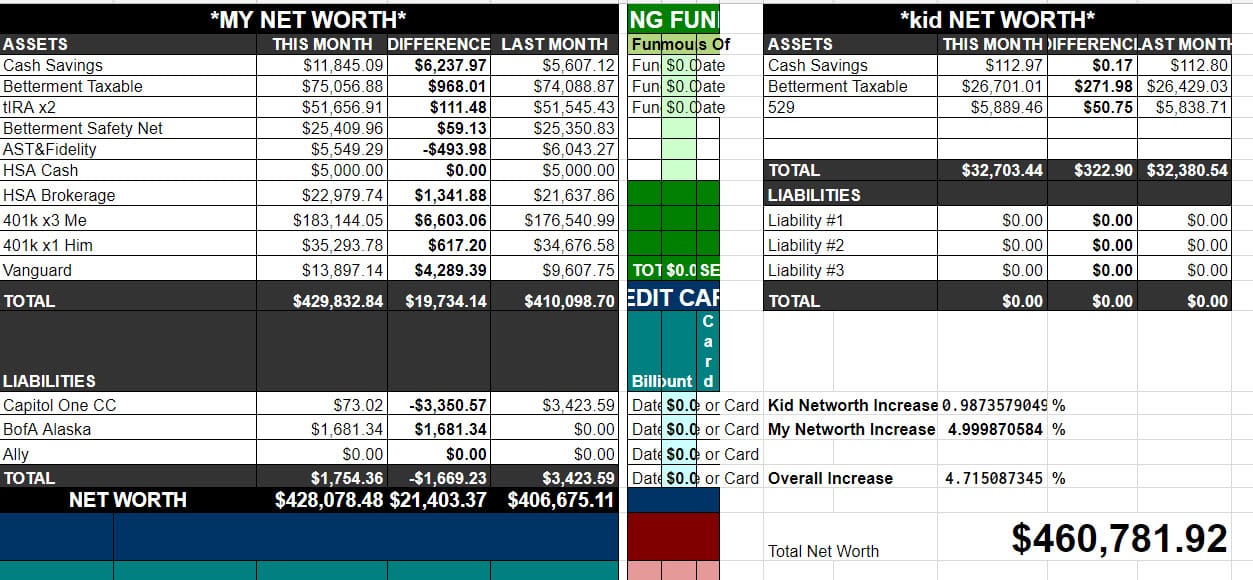

[Click images to enlarge… net worth spreadsheet is the one we give out here on the site :)]

[Click images to enlarge… net worth spreadsheet is the one we give out here on the site :)]

Background:

Paid off my house in 2014. Single (higher) income. Medical professional.

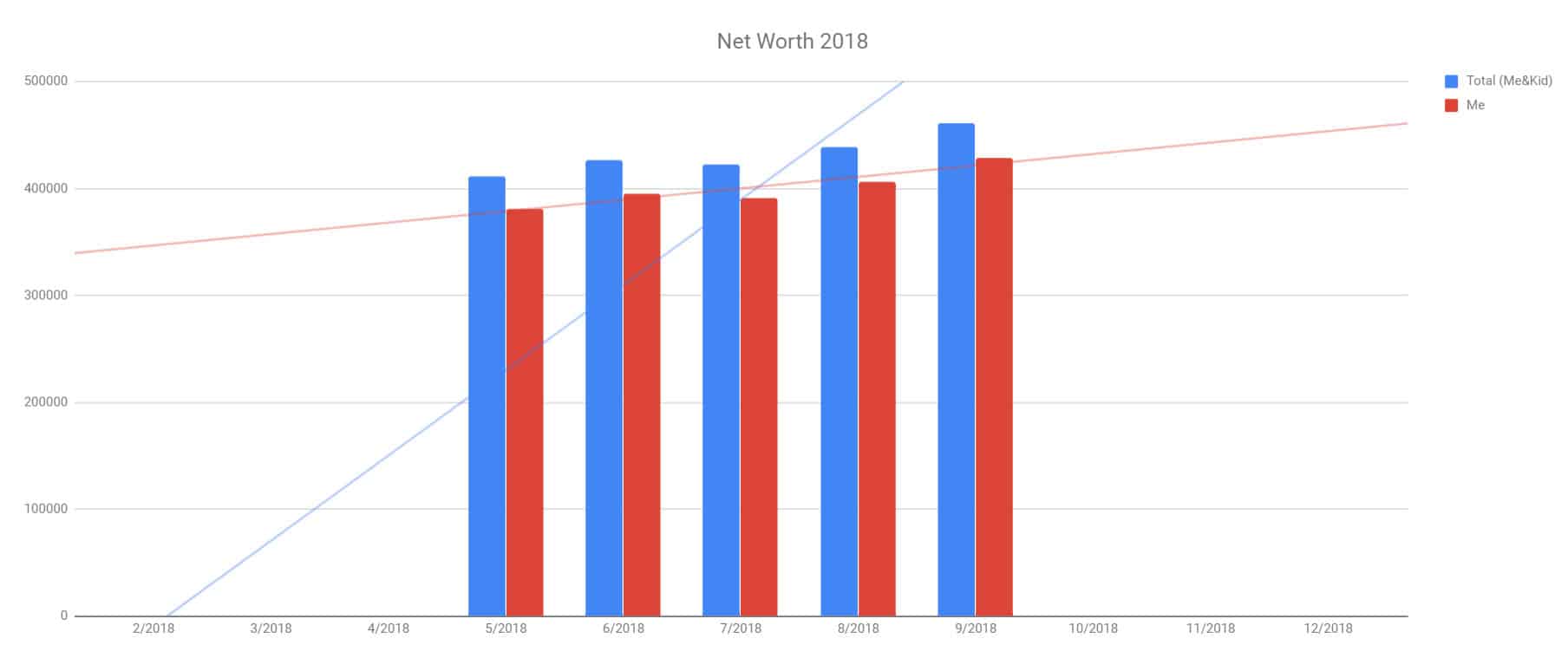

I’ve only been tracking since April. I’ve seen net worth go from $411k to $460k end of April to end of August.

I began tracking because I wanted to get a better idea of how quickly things were growing and if and when it might be realistic to expect to live more off of our savings/investments vs. work. I have used things link Mint and, since April, Personal Capital, but I wanted something more concrete that let me look at specific savings areas vs. bulk net worth.

I’ve really liked being able to see specifically where the gains are coming in (like, the 401ks) and it helps me cool my jets a bit about early retirement as my non retirement specific savings are not growing nearly as quickly.

Oh, and I DO NOT include our paid off home and property as it’s not useable to me for anything unless we planned to sell, which we do not. I’ve found when I look at what the house is worth regularly and how that effects my net worth, it makes me feel like I’m much closer to FI than I actually am and gets me more focused on that last stretch and calculating “exit strategies” more often than I should.

Best line in there – “Paid off my house in 2014” :) I personally like seeing real estate #’s in the net worth because it gives you an overall picture of where your money’s at and what you’re “worth” at any moment in time, but you can’t argue with her reasoning above either. Fact is – you can do whatever you want with your money, especially if you’re a bad ass and living mortgage-free!!

(The other thing that caught my attention were all th0se 401ks under her name? The minimalist inside me wouldn’t allow for that as I like my stuff condensed all under one roof. Much easier to manage and stay on top of!)

******

Snapshot #3: The Half-A-Millionairess

Background:

I’m 43 and plan/hope to retire around age 62. Not so strong on RE at this time – I’m one of the crazies who likes to work and don’t really have a “side gig” I’d do – plus not enough $ set aside to retire now if I wanted.

But boy does FI sound good to me! If all goes to plan (ha!) I’m hoping to have $2mil when I retire. This would likely set me up to have more monthly “income” than I do now.

Since you’re transparent with your numbers I will be too:

- $450,000 in investment/retirement funds

- $60,000 in emergency fund

- Around $600,000 net worth

I just started tracking net worth after reading all of your posts and the associated comments.

I’m maxing our my 401k and continue to always do this (assuming still at same income/expense levels!). I also plan to contribute the “make up” amount when I turn 50. My emergency fund would probably cover me for about 18 months.

Yep, I’m conservative/chicken.

I’m the only person in the house/only income source… been handed my pink slip in life before due to company changing locations…yep, chicken! Oh, plus I also lost money in investments (50%!) before due to a poor financial planner associated with a bank I used to use (he was brought to court because he mismanaged money and lost people so much).

I’m also throwing extra money towards the mortgage every month and plan to have it paid off by age 55. (Going for the emotional approach – I like seeing that balance go down.). Now trying to figure how to get more out of my savings account. Hoping this is money I won’t need until it’s time to retire.

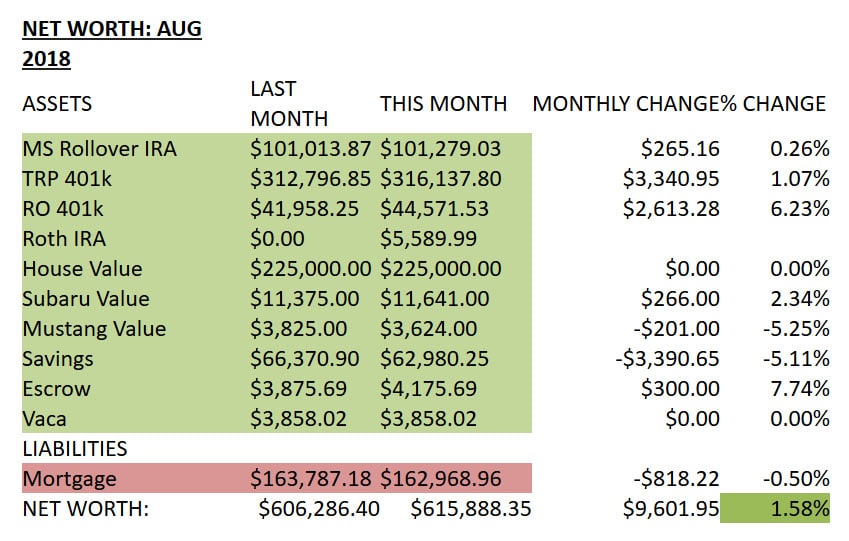

(As you can see, I’ve broken down my savings into savings, escrow and vacation fund. Savings recently took a hit but that was because I needed the money to max out a new Roth. Not quite sure how the value of my Subaru increased this month. I also am very conservative when it comes to the value of my house – I stay with a number that is close to what I paid for it instead of market value. I’m still learning more as I continue to read your blogs (and everyone’s comments) but have so much more confidence now regarding managing my own retirement money.)

A half a million net worth is already impressive, but a half a million net worth ALL BY YOURSELF?? Even more so.

I know we like to throw around #’s here as if it were all our own (for example, I’m always saying MY net worth and MY retirement number), but half the time we’re really talking about “our spouse and our’s net worth” in this community. Just something to keep in mind when you’re trying to compare yourself to someone else, even though you’re not supposed to ;)

And then of course there are tons of other factors too, like where you live in the country/world, what you do for a living, how many kids you have or don’t have, how old you are, how old you were when you *had your money epiphany!*, etc etc..

So basically, you can never compare yourself to anyone fairly.

******

Snapshot #4: The Married Millionaire-And-A-Halfs!

Background:

Hello J.Money!

Long time reader here!

I am contributing our snapshot. No one in real life knows our net worth, but this is anonymous internet land, right? This doesn’t include our HSAs ($64k). Mint doesn’t seem to link that company so it doesn’t show up in the screenshot.

We are 42 and 40 years old, no kids, married now for 6 years, live in the US.

About 5+ years ago we were at $476k combined retirement. Now we’re at $1.5M in just savings. All income, no gifts or inheritances. We feel very grateful to be able to save like this. We have a variety of pre-tax and post-tax retirement accounts which we max out. No we aren’t doctors or lawyers.

We don’t use a budget. Our debts (mortgage and auto loan) are a small percentage of our income – total 11% of our gross income. This leaves flexibility for the other categories.

August’s paycheck included our cost of living raises which is always good time of year. CoL raises aren’t guaranteed and vary year to year. It all goes to savings because we were already living on the previous take home income. We are trying to build up the cash reserves more which will eventually go into a brokerage account. Several other retirement accounts maxed out, so this is our next focus while continuing to track our expenses.

I made a spendy purchase last month (seen on credit card). After borrowing a friend’s mandolin for over a year and learning with YouTube (free!), I decided to get my very own mandolin because I enjoy it that much. It is pretty nice! I will have it for the rest of my life. Since it was $$$, I like to rationalize in my head, “That’s like one year of eBay sales!” I have a sporadic eBay store as my side hustle.

-Anonymous

I know what you’re going to say before you even say it – THEY DON’T BUDGET???? WHAT THE HELL IS WRONG WITH THEM??? *Goes to change the name of this site to NotBudgetingIsSexy.com to see how much faster my money grows* ;)

In all seriousness though, they’re killing it! So good for them for figuring out how to manage it all in their own way – no one said budgets were mandatory if you’ve got $hit down. (And maybe they used to budget in the early days like I did, and then moved to a more relaxed “net worth budgeting“?)

It’s so much fun peering into everyone’s lives here, right??? Let’s do more!!

******

Snapshot #5: The 60 y/o G-DINKS

Background:

My husband is retiring in June 2020, so we are focused on completing all upgrades to our house by then. We don’t plan to access Social Security until 70 to be able to take the maximum benefits. I will also “retire” in six years in 2024.

For both of us retirement means stepping down from high-earning full-time jobs to part-time consulting for a few years. We have no set time to liquidate the rental property since it essentially pays for itself.

My husband’s retirement benefits included paid medical coverage which makes retirement planning simpler. We both have long-term care insurance. And one dirty secret — we don’t have updated wills.

Oh yeah, and we are DINKs, so college and childcare aren’t in our budget. I’m 59 and my husband is 64.

See what I said about where you live?? Those mortgages could buy 5 or 6 homes in other parts of the country! :) It’ll be interesting to see how much more they can pay off and bank too before they pull the trigger on going part-time… Gonna be hard to retire with some big mortgages on the books like that, especially in San Fran, yeah?

Though they do have that rental property which I assume is what was cut off at the bottom of the “assets” section there (it’s missing about $1,000,000 worth). And good they still want to do some side consulting to help pad the income!

I asked about the multiple accounts everywhere as it seems like a lot, and here’s what they said:

The multiple accounts made sense before we got married. There is one checking account for the rental property to keep everything separate. All the bills and condo mortgage go through that account. There are two business accounts — checking and savings — for my consulting business. The savings can go away. There is a business credit card for all tax deductible expenses and we each have a personal credit card and a single joint credit card for household expenses. The investment accounts are all set by our financial guy but I will ask about consolidation.

Excellent idea indeed to talk to their financial guy as 15 investment accounts sure seems a bit complicated! And only a few of them actually has money in them?

Super excited for these guys over the next few years though as I’ve been friends with them for a while now and they’ve got the biggest hearts in the world. This was the first year they put everything together and started tracking their net worth closely, so I hope they keep doing it to be able to reach those not-too-far-off retirement goals!! Better to have the epiphanies now vs later when it’s too late!

******

So there you have it! All kinds of different finances out there!

Anything really stand out to you with these? Do you find yourself resonating with any of them in particular?? Anyone want to share their *own* finances with us and we’ll make you famous in our next round of these?? :)

If so, email me here!

Big thanks to everyone for opening up today and giving us some inside peeks… I know you can’t talk about this stuff in the real world, so we do our best to be a “safe space” here so we can chat and learn from each other! So please do share any and all constructive criticisms/thoughts if any are brewing!

Thanks guys!

And if you missed the other two rounds we’ve done, here are links to those again:

- Round I: the newbie financial advisor, the risk taker who loves to gamble in bitcoin and poker, the budget of my wife circa 1995, and the Kyrgyzstanian who only lives off $808/mo

- Round II: the Hebrew software engineer, the traveling ICU Registered Nurse, the millionaire who doesn’t feel like a millionaire, and the 64 year old real estate investor who used to be homeless and penniless and is now a millionaire herself

Happy lurking ;)

Get blog posts automatically emailed to you!

This is so interesting to see. Very different patterns of wealth building leading to similar result: growing net worth. I felt sorry for the guys from your third case; managing so many accounts must take so long that if they put all this effort in making more money their net worth will probably rise even further. Great one, Jay.

Glad you enjoyed, Maria!! Miss seeing your face around these parts :)

What resonated for me is that though these stories are fascinating, we shouldn’t use them to compare to ourselves. Though there are some similarities I can find in several of them, not one is close enough for me to use for comparison and even if I could, what would be the point?

We’re all on our own journey but it’s good to have company on the way. Keep them coming!

Very very true.

These stories are really great. Everyone is on a unique journey and they are doing very well.

Really nice job. Maybe the last couple can move to a cheaper location. Housing is crazy in some area.

One note about all the retirement accounts: 401k’s (and other plans through the employer) have specific laws that protect them from bankruptcies and civil lawsuits. You can do an IRA rollover, and those protections are kept – as long as you keep those funds separate. As soon as you mix the rollover with contributory accounts, they lose those protections.

Now, disclaimer time: I’ve had a couple of financial planners tell me this is true, and several that have no idea what I am talking about (including the one at Personal Capital). I can’t find anything on the IRS website, or any lawsuit precedent, that makes it absolutely clear to me (but it’s all legalese nonsense to me :) So if anyone can find a definite answer, please, please share! For now, just incase it’s true, I keep all my 401k rollover accounts separate.

Interesting – haven’t heard of that one before? I definitely did not think about that when merging all of my accounts years ago :) Would love to hear how accurate that is or not myself as well.

Interesting to note about the comparison idea. I think whenever someone is reaching toward a goal, it’s easy to get lost in how far one had gotten so far. This happens for me all the time on this FIRE journey. I know I have more time to go in front of my than behind me, and sometimes it seems like I will never reach it.

Then I think back to four years ago. Living in an apartment I hated, just started my current job by moving back to my hometown, NO savings, and had JUST discovered Mr. Money Mustache. I still had student loans too. Today, four years later, no loans, living in a house via a mortgage that is roughly the same as my crappy apartment was, and building my investments. My boss laughs because I’m the only one not hovering over our mailboxes on pay day, since I only need about 50 percent of my income to survive. I also make more than $6 more per hour than I did then, especially thanks to a recent raise (and more work). I am still evaluating what the new income will average out on my paychecks (I am paid twice per month, not every two weeks, which means the checks vary a lot) but I know it will get me to my goals sooner because I am not spending more.

So I have to remind myself that, once I secured my housing, that I’ve only been saving/investing for about 2 1/2 years. I just need to stay the course and keep letting my little employees earn me more money!

Yeah dude – you have found your path and are well on your way now! It’s nice not worrying about your paycheck every other day!

It’s awesome seeing people from different walks of life and comparing their stories. They’re all impressive and I especially think the 33 year old with 3 kids is killing it, and they’re only in their lower 30’s! Major kudos. Your kids will thank you for setting a good example to them from such a young age!

It’s great to see that it’s possible to get ahead with a budget. I’ve never used a traditional budget because our expenses (especially medical) vary so much from month to month that it was driving me crazy. Glad to know I’m in good company with a few of these folks!

Off topic a bit but when I read this today on Investopedia: “The S&P 500 is looking very weak and negative and that is putting fear into investors,” said Michael Matousek, head trader at U.S. Global Investors. “With the markets going down people are increasing their allocation towards gold.”

So that, plus the fact that VFIAX and VTSAX were down 3.29% and 3.24% respectively I will choose…to continue unwaveringly dumping money into both…forever.

I actually hope it goes down more. Let’s get this deep correction (a normal healthy part of the system) out of the way so we can stop hearing about it. But then what will the traders and media folk whine about?

Just had to vent Bro.

Peace

Haha, you know it man…

And as a coin collector, it’s actually double the fun as we see a surge of new people come into our hobby, as well as an increase in the value of all our gold/silver coins :) And Lord knows our hobby can use both the boosts!

Hear, hear! OG homeboy Warren Buffet said it well: “When others are fearful be greedy. When others are greedy, be fearful.”

I’m a little bummed my wife’s bimonthly $1k 401k purchase went through on Monday instead of, say, yesterday… and mine won’t hit til next Wednesday. Hmpf.

Really appreciated reading about other people’s money journeys and realize never to late to start . Since I started reading your blogs I’ve been coming across new information. Saw “Betterment” in Snapshot #2 and was initially thinking is that a name she just gave accounts then thought to google it. Noted “The Half-A-Millionaire” wrote about feeling more confidence – while completed a net worth spreadsheet at the end of September for the first time, I’m feeling a little more confident about my financial situation.

GOOD!!! And it should only get better as the months tick by now as you’ll be able to see the growth over time and get even more confident! It’s super empowering!

Thank you so much for spotlighting different households! We’re a SIK household and I love seeing how other families with kids are doing. We have four munchkins and paying for four soccer camps, college tuition, and weddings can really slow down (but hopefully not derail) your progress.

So glad you enjoyed it :) We’ll be doing more if you ever want to pass along your own snapshots!

holy crap I am obsessed with this idea!! it scratches my fascination itch reeeal good. I like seeing all the possibilities and I am inspired by so many people here in internet-land (hi married millionaire-and-a-halfs). my personal net worth snap shot is in the negative but reading through everyone’s snapshots is a humbling reminder that this journey to FI is a wild one but definitely worth it. AND I’m confident that I will be positive one day. Consider me a long time lurker of Other Peoples Money :)

I think we should feature you next in the series :)

Hi there AK and thanks! :) You will be in the positive for sure!

i’m so down!! and thank you for the support @tmc !! :)

I agree with you, job hopping has a bad rep but people need to understand that there are cases where it’s acceptable.

I love these reports. Having been through highs and lows with my personal finances, I can relate to a few of them. It’s helpful to see that others are in similar situations and it’s helpful to see what they’re doing about it. Thank you for sharing!

Good!! Glad you enjoyed this, man!