Morning!

Here’s another snapshot of someone’s money that I totally forgot to share 6 months ago ;) Gave me a chance to snatch an update though so now we get to see the before and after which is cool!

Original note below, and then the follow up of where they’re currently at now (bold highlights are mine that really stood out to me):

*******

J Money,

You have a neat community that I have been casually following for a few months. I find myself in a similar situation as your readers who share their stories and a similar perspective. For what it’s worth I’ll summarize my story for you.

I’m a 32 year old California dude tracking my little family’s net worth every month with an aggressive savings goal and our first baby on the books for 2019. Lately I have been all about “sneaky” money. It’s money you save up and exclude from the budget and kinda forget about. Like cash back on a credit card (we pay our cards off every month… credit card debt no bueno). After 18 months our cash back cards have accumulated $450 of sneaky money! We will use that for a Hawaii budget (already booked for next year).

Additionally we are on pace to hit our savings goal of $18k this year. A lot of times that requires sacrifice and sometimes that means navigating a slim budget of $37 per day or less for gas/groceries/unexpected. That can be stressful so we make sure to balance budgets with cutting loose at times and reigning it back in.

Even though it’s difficult, I like to track and look at our budget in terms of daily spending because it really lets you appreciate and understand what you need to do to achieve your long term goals. Of course, in order to pad our expectations from reality I also reserve $900 of contingency each month which we eat up consistently. The contingency has helped us come in under budget consistently too and I’m projecting $2k additional savings from coming in under budget this year (more Hawaii money).

My wife and I both work full time and the baby started daycare at just 5 months (times have changed since our parents generation). We have a combined disposable income of $108k per year, a $160k loan on a $400k house, $50k in IRAs and $60k in the bank. We are saving up for the next house and we might try to keep the current house (built in 2013) as a rental if possible.

In 2019 we hit our stride, but next year will bring new challenges such as a full 12 months of daycare vs 6 this year (Sheesh!). Our savings goal will probably have to come back down to reality next year (I’m projecting $12k of savings for 2020). Thanks for creating a community of goal makers and story tellers J Money, we gotta keep sharing our truth, keep planning & keep the dream alive!

– Joe

*******

And now where they’re at today, 6 months later!

*******

At the end of September 2019 I emailed J. Money because I had just read his blog piece on Net Worth Update Day and I felt inspired to share my story. Now it’s March 10, 2020 and he asked me to give him an update on things…

In 2019 I said that me and my wife were on track to save $18k in 2019… and I’m pleased to inform you that we met our savings goal!

I also said that we planned to take a trip to Hawaii and saved up a budget for that trip separately from our other savings. This trip was our unofficial honeymoon and we arrived in Kauai on the day of our anniversary, February 20th. Ran us $1800 total for 4 nights, including airfare + hotel. We decided to take our now 1 year old daughter along with us. Yes she was fussy on the plane. And yes we had to put our baby to bed at 6pm each night and keep watch over her from across the hotel room while sipping mai tais and watching movies.

Many might disagree, but I feel like these early impressions set a precedence for kids even if our little girl will not remember this trip when she grows up. Think about how many experiences you’ve had in your adult life that you may not remember. The experiences themselves still leave an impression. Besides none of those challenges stopped us from enjoying some hard earned relaxation. Relaxation is important. Don’t forget about it. It’s healthy in our lives and it’s healthy for your net-worth’s long term growth.

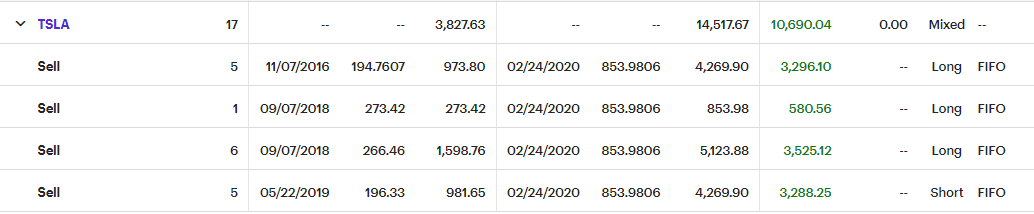

So… something interesting happened before we left Kauai. The night before we were due to fly home I had a sudden and strong impulse to divest some Tesla stocks I had been holding onto for the last few years. This gut feeling checked out with my logic centers as I reasoned selling stock for a profit is never a bad thing regardless if the stock goes up afterwords. Plus I was honestly feeling a little tired of checking it incessantly. So I set an alarm on my phone and woke up at 2am to sell all of it in the pre-market hours.

My intuition paid off as coronavirus fears tanked the market in the coming days. What can I say, sometimes you just get lucky!

[click to blow up]

[click to blow up]

I sold my investment of $3,827.63 in Tesla stock for $14,517.67 and took a profit of $10,690.04. It’s important to note at this point that I am a complete amateur at this stuff and don’t necessarily recommend stocks as your side hustle. Any money I put in the stock market is money I am comfortable losing. I have capped myself at $6,000 for now and I don’t invest more than that at any given time outside of my retirement portfolio.

So what did I do with the profit? I stuffed it into a high yield savings account of course, lol. I opened the interest bearing account with Etrade for 1.75% APY in January, and transferred money from our brick and mortar bank account. I was apprehensive about moving such a large sum of money over the internet but I clicked the button and called our bank to give them a heads up. It was much simpler than I thought it would be. The interest will give us an additional $1k of income this year in case you were curious.

Before we left for our trip we decided to take our daughter out of daycare and restructure our work life balance to cover her care ourselves. Suffice it to say we are going to save a lot of money this year that would have gone towards daycare. It’s basically a mortgage payment.

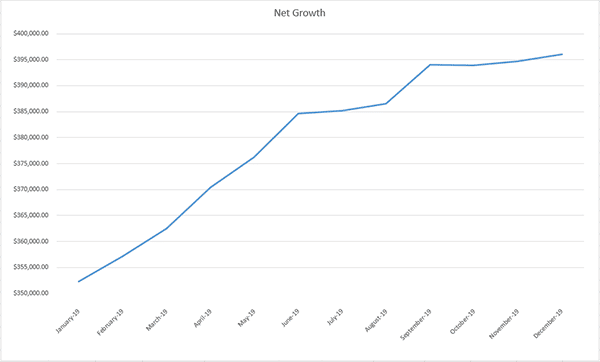

So let’s take a look at how 2019 ended and how 2020 is shaping up considering these new developments.

![]() [click to blow up]

[click to blow up]

As you can see, we had a large amount of money sitting in a checking account for a long time not making any interest. Yikes! We live and we learn, and you can see below that as of March 2020 the money has moved from checking to Etrade.

![]() [click to blow up]

[click to blow up]

I didn’t track net worth for a few months there from December to February. I am currently projecting $34k of savings instead of the $12k of savings I was anticipating for 2020. The additional savings is due to the profit we took on stocks I wasn’t expecting, and the savings from the daycare I thought we would need.

We bought our house in 2013 for $305k, it is now worth $430k (that’s California for you) and we owe $155k. That makes up the lion’s share of our net worth, but we have achieved meaningful savings in the last few years by setting goals, tracking our net worth and adhering to our budget.

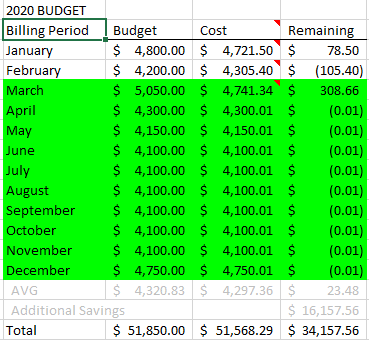

I told J. Money in September how I like to track our monthly budget frequently and relay that info to my wife in terms of how much we can spend on a daily basis to achieve our goals. Here is what that budget looked like for 2019:

And here’s the budget for 2020:

Thanks for reading! Mahalo!

– Joe

*******

So looks like a solid net worth of $400k’ish and growing! Not too bad for a couple in their 30s! And $100k more than I had at that age too ($314,246.43).

Did you catch all those parts I highlighted?

“Any money I put in the stock market is money I am comfortable losing.”

YES! Great mindset to have!! You can never bet the farm on something your livelihood depends on no matter how promising it is. And since stocks *rarely* go down to $0.00, you’ll typically come away with at least something in a worst case scenario anyways. But in a best case?! Well, Joe’s already relishing in that one! ;) And he means “stock picking” here vs retirement accounts when he’s talking about it all being “extra”. With retirement accounts of course you want to be much more conservative and play it for the long haul.

“…selling stock for a profit is never a bad thing regardless if the stock goes up afterwords.”

Yup. Even though we’ll STILL get pissy when we don’t max out those rewards as if we had a crystal ball!! Human nature can suck, lol…

“I like to track and look at our budget in terms of daily spending because it really lets you appreciate and understand what you need to do to achieve your long term goals.”

This is a great idea, particularly for those who don’t like (or get much out of) the typical budgeting methods. You still have to know what you generally want to spend each month in order to break it down to the *daily*, but it’s much easier to comprehend sometimes when it’s in the here and now. If you know you only have $40 to spend today you’re going to be much more focused! And feels more real than a future “month from now” type deal.

I actually did something similar the other day when I was having a down day w/ my projects… I calculated how much I was expecting to earn for the year, then divided it by 261 (number of working days in a year) to see how much I was earning *that day* and if it would make me feel better :)

It did! Came out to about $475, and I quickly acknowledged that I’m fine with as many crap days as life wants to pass my way for that, lol…

“Lately I have been all about “sneaky” money. It’s money you save up and exclude from the budget and kinda forget about.”

The best kind of money! Which somehow feels BETTER than salary income, even though it’s substantially less?! But having that extra freedom within your finances can help keep you sane and motivated as you go…

NOT EVERY DOLLAR NEEDS TO BE ALLOCATED!

It’s perfectly okay to have some flexibility built in as you roll down the river of life… You can’t predict every last move anyways!

“Before we left for our trip we decided to take our daughter out of daycare and restructure our work life balance to cover her care ourselves.”

Probably my favorite line of the whole conversation… Yes because it saves crazy money, but also because it means more QUALITY TIME with your loved ones -and- proves that you ultimately HAVE CONTROL OF YOUR LIFE and can adapt when you deep down truly want to!! Which is huge! Most people just sit around bitching and wishing instead of figuring out a way to make those wishes come true…

So I’m genuinely and thoroughly impressed with you two, and wish y’all nothing but continued success! Thanks for sharing your journey with us! Feel free to send over as many baby pictures as you want, please :)

Questions/comments/thoughts?

Get blog posts automatically emailed to you!

Hey J,

Just a comment on the selling the stock thing for a profit.

When Facebook’s IPO came out I wanted to buy some, but it was going up so fast that I didn’t get in on a purchase. Then they had all those problems and the stock dropped to $15 per share, I decided to make the purchase (I was doing this inside of my IRA). I purchased 750 shares for $15,000 (about $19.50 per). I told myself that when the price doubled I would sell 1/2 to get MY money back and let the rest ride. Well the price did go up to 38 and I sold 300 shares to get most of my money back. Since then it has gone up and down, but you can’t be sorry when you get your money back and still have a large investment that is doing well based on what you paid for it.

Yeah I think I’ve heard a similar idea before. I think that’s a really smart approach because it provides a little safety net from losses. Will have to try that out!

That is a good route – hadn’t heard of that one before :)

I instantly grabbed on to the idea of “how much do I spend a day” because it’s the complete opposite of my no-spend day/month challenge. What an eye-opener! Hmmmm, it’s definitely worth some more thought. Thank you for sharing and giving me a different perspective.

Happy to share! It’s worked really well for us! I allocate a monthly budget, update the costs weekly and calculate a real time daily spend limit based on how many days are left in that period.

It’s nice to see a six-month update! Ours, if I were to dig for such a thing, would probably be pretty flat at best. These market gyrations are wild. At least we’re got another half dozen $K of the house paid off. :)

We don’t (and won’t) have kids, so my opinion here is worth less than the time it takes to write, but I’m wicked impressed that they were able to pull their daughter out of daycare and make it work. That can’t be easy… and has got to feel priceless.

I feel you on that. We were on the fence about kids and then had a surprise pregnancy. It was scary but luckily it worked out. We love her to death!