What up what up!

It’s a good day to sit down and finally start tracking that money if you haven’t already! I’m looking at you, Anthony H.! 👀

Haven’t been paying attention to the markets lately, but apparently it did pretty well this month eh? I used to log on every day and obsess over it, but over time I realized it was completely out of my hands and fluctuated way to wildly to really grasp anything anyways. So now I just check in once a month to update these reports, and then go about my lazy business letting the markets continue to do their thing :) Not a bad idea to follow yourself if you find it stresses you out too! You know your $$$ will trend up as long as you’re contributing to it every month!

At any rate, below is the breakdown of how last month went in the J. Money household… This marks month #127 in a row tracking this stuff, and it really does show that paying attention regularly works! I honestly don’t do much outside of continually saving and investing!

Net Worth Breakdown: July, 2018

CASH SAVINGS (+$1,918.95): A good overall month of spending less than we earned. Something I’m noticing our daily wants tracker is starting to affect! I triple think all extra spending now! :)

SPAVINGS FUND! (+$216.64): A bit larger than normal as I let a $120 yearly service I was using expire instead of renewing it, but I’ll probably be wrapping up this spavings experiment shortly as it’s run its course and I’m more into the *daily* exercises now. $3,800 banked in 9 months isn’t too bad though! I think we’ll end up applying this towards getting that will/trust finally set up to speed up the process even more, haha… Much more fun to think about when you’re getting it for “free!” :)

THRIFT SAVINGS PLAN (TSP) (+$745.76): Another nice bump in this bad boy too, courtesy of my beautiful wife having a beautiful job! She’s been on maternity leave going on 2+ months now, but had accrued enough hours and sick time to cover her most of the way… We did lose a couple days worth here and there, but she’s going back to work next week and the reality of having 3 kids will finally set in! Haha… Time for Daddy to take over and run the daily household – woot woot.

BROKERAGE (+$1,464.77): A sturdy little increase here as well, and much better than it would have been had we left it in our savings account like we did the previous 6 months before xfering it over! All into VTSAX at Vanguard, of course, as with my ROTH and SEP IRAs as well.

ROTH IRAs (+$4,173.19): Same story here too – nothing new added, and just the markets doing its beautiful thing. At least this month anyways :) I’ll be waiting until the end of the year to max these puppies out so we don’t make the same mistake as last year when we weren’t allowed to! Literally the only time I maxed them out early, and of course it was the one year we shouldn’t have, womp womp…

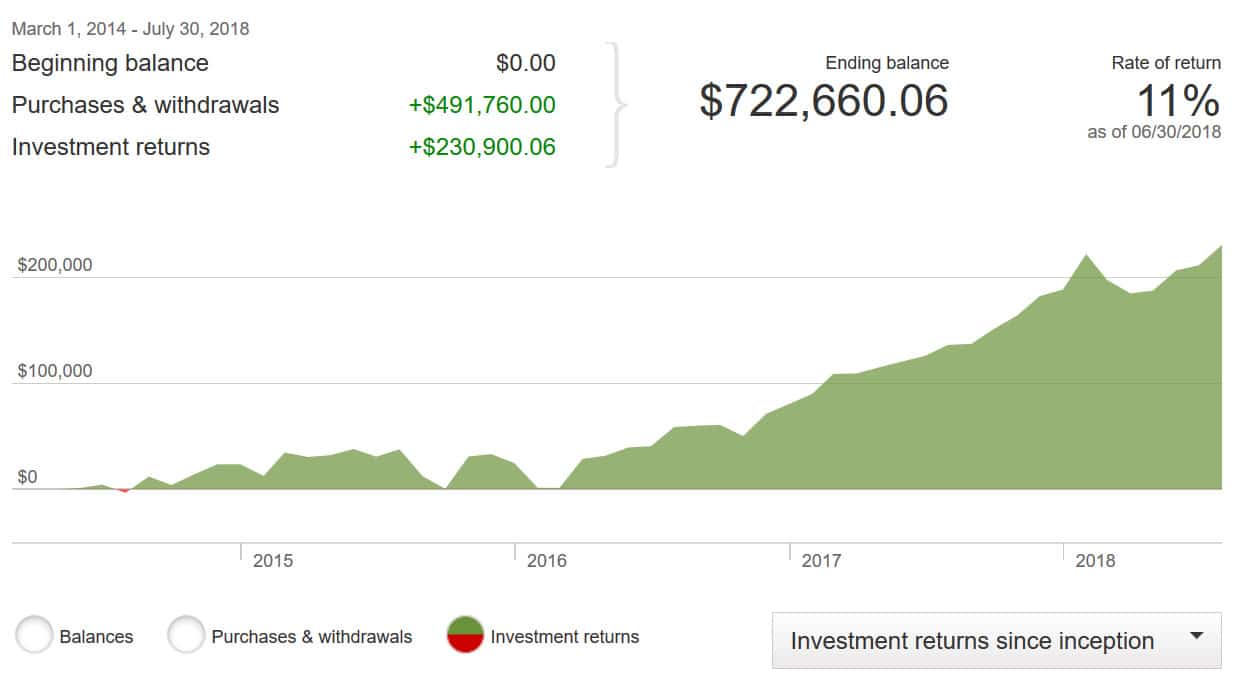

SEP IRA (+$15,478.43): Nothing new added here either (we also wait until the end of the year to max out, as it’s tied to my business earnings), but very cool to see it continue to grow despite not touching anything. Here’s the overall performance below since switching to Vanguard 4 years ago… It would probably still be up even if we hadn’t switched, but not nearly as much as my portfolio was a hot mess back then!

CAR VALUES (-$443.00): Lastly – the cars, which are supposed to go down :) And why many people don’t even include in their net worths as they’re not “income-producing” assets. But I do since they’d easily convert to cash if you sold, and I like seeing an overall snapshot of my money/property at any given point as well. Maybe one day I’ll throw my coin collection on it and really spark a debate! ;)

Here are their values according to KBB, valued super conservatively and all paid off:

- Lexus RX350: $8,565.00

- Toyota Corolla: $2,538.00

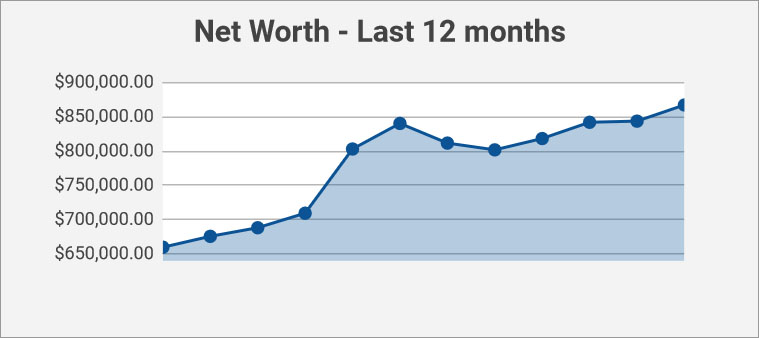

Total change in net worth this month: (+) $23,554.74

Much more fun than earlier in the year when it dropped $30,000! And I believe this is now our all-time high which is pretty cool… Hopefully yours is growing nicely as well! Or else I’m not doing my job here!

Here’s what the last twelve months have looked like for better perspective:

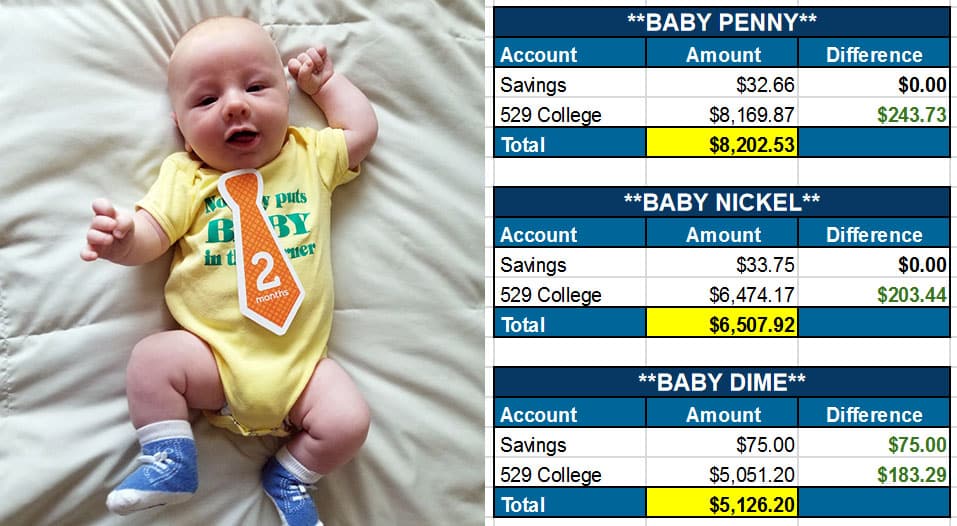

And then lastly, OUR BABIES’ NET WORTHS!

I’m continuing the tradition of adding a recent pic of Baby Dime to these to remind us there’s more to money than just numbers :) I don’t know who sent us this packet of paper ties to use every month, but they’re absolutely brilliant as they remind us to snap more pics! Something we don’t do nearly enough of after having babies #1 and #2, haha… Is that bad?

(Baby Dime also got his first savings account this month, in order to deposit a check in his name :) We tend to only keep $50 or less in them, with all extra $$$ going right into their 529s for tax-free growth)

So that’s how our month went! How about yours? Anything good going on? Anyone start tracking it for the very first time?

I sound like a broken record here every month, but I seriously believe doing this one thing will change both your finances and your life. One of the top 3 things I ever did for our money for sure, which has probably accounted for 80% or more of our success! (The others being maxing out our retirement accounts every year, and then taking monthly challenges to continue staying conscious).

So yeah – tracking net worth works! And it’s much easier than budgeting! ;) (But still good to do if you don’t know where the hell your money is going…)

XOXO,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Looks like a new all time high. I love it when that happens!

I tend to only closely track my net worth twice a year so I’m not overly focused on the ups and downs of the market each month.

It’s always nice when I see yours going up though as mine is usually tracking in the same direction.

Twice a year – you’ve got patience! I don’t think I could go that wrong without my curiosity getting the better of me but I’m definitely over checking it daily :)

Same-we used to track Net Worth monthly and just switched to every 6 months. We still track income and spend on a monthly basis…if we control our spend in FI then the networth should take care of itself.

Still quietly crushing it! Well done. I haven’t tracked my monthly yet but I do watch the markets carefully and July seems to have been one of the better months this year. Let’s keep it up!

I’m up ~$5k this month, which seems blah but at least it’s up. I checked and I’m up ~$17k since January and ~$42k since this time last year. I also got a late start at this game, so again…up is up! I was at an all-time high about a week ago but end-of-month bills dropped me down, as did a market drop a few days ago.

Today is day one of my no-spend month!!! Yay! Internal discussions already started this morning (Hm, I could really use that new face cleanser I saw at Lush)*(You don’t need a new face cleanser, you have a nice one you like that is half full. Use it up first.)

What does the last line say on Baby Dime’s onsie? I can’t figure it out…

GOOOOOOOD LUCK on your no-spend month!!! One of the best challenges I did back in the day myself! The trick is just *not* going into stores or onto Amazon or really anywhere at all, haha…. Except for work and on walks :) I think I even left my wallet at home a couple of times too just to double make sure I wouldn’t spend!

“Nobody puts baby in the corner” – the shirt ;)

Oh, of course it says that, my morning brain wasn’t working yet.

Baby Dime is absolutely adorable. So precious!

I’m really impressed you’ve been churning out posts regularly despite taking care of three kids. We are having our second one in a month, and my hubby is stressed out every day.

I will say your patience does get better with each kid over the years :) But going from one kid to two was def. harder than people let on! Don’t listen to anyone! Haha..

Baby Dine is adorable! When is the baby mohawk coming?

Big increase the past month, must mean the market is doing well.

As soon as he gets some more hair! Although if he’s anything like his two brothers he won’t be having any of it, womp womp…

My goal was to get up to $435,000 to be on track to hit $500,000 by year end. I actually got up to that, but then the market sagged a little, and I settled back at $433,000. We’ll see how the rest of the year goes. With my history of barely missing goals, I’ll probably finish the year at $497,000 or something.

There could be worse endings to goals :)

Loving all that green! Your savings (cash accounts and investing) is phenomenal.

All around, professionally and personally, well done J!

Thanks man! How is your journey going?

I’m just over here crushing on Baby Dime. I miss those cute days but not those sleepless nights. I just calculated our net worth and we’re up from July but only because July was so bad for us. Not back to up to our all time high but moving in the right direction again. July is the month we kissed all credit card debt goodbye! Moving on to the car and that payment will be out of my life by early November. We have some big goals to hit by the end of the year!

Oooooh no more credit cards – that’s gotta feel good! Love that you’re on a mission to kill it all this year – huge step forward to wealth building :)

I started tracking in June and my net worth was up almost $4,000 in July…not bad.

Good job tracking it all! A lot easier to update it monthly too right?

Ha J you are literally working on these when the clock stricks midnight… they keep coming earlier and earlier

Well, I actually cheated and ran the numbers yesterday mid-market as I don’t get on my laptop at nights anymore :) Just happened to be good timing w/ my writing schedule here!

Looking good! The kids are doing particularly well. Their net worth is higher than a lot of people. :) We did pretty well in July too. The rising tide lift all boats.

Haha yeah… always reminds me of Jason Fieber’s post the other year when he wrote about being worth more as a baby :) You ever read it?

https://www.dividendmantra.com/2012/03/were-you-worth-more-as-baby/

I literally just started listening this morning to a podcast Jason did with Radical Personal Finance. I heard him mentioning how he was worth less than when he was born and found that very striking when framed like that. It’s funny how you now brought it up the same day.

It guess it was meant to sink in :)

Very nice J Money! I just found out yesterday that I am getting a huge raise – biggest of my life. I’m still in a bit of shock over it. Grinning from ear to ear knowing that FI is going to come that much sooner now! (Since of course I won’t be upping my spending at all : D)

Oh hell yeah!!! Huge congrats, man!

Thanks J Money! Congrats on another successful month!

Good stuff! Ours grew about 2% this month, which is about standard.

On another note, I check my work 401k 3x a week and update in a spreadsheet. Has a pretty graph with a nice upward trend since inception (fall 2013). Also include values for how much money I’ve personally invested out of my paycheck, as well as my employers match, which is a generous 11% overall (6% match + 5% pension alternative)! It’s really cool to see how “little” i put in, but with company matches and interest, it grows so exponentially. nice to track when trends are up; i assume i won’t track as frequently when they’re down lol

Haha yeah – not nearly as fun to look at when it’s down, but it is to keep *investing* during those times and picking stuff up cheaper! So maybe just look at the new shares you’ve picked up during the crashes :)

I’m up $7 in investments this month, which I think is impressive considering how little investments I have (at least in my perception).

I just put in $100 into my son’s 529 from his “job.” The little guy is only 4 months old, but he’s part of a vaccine study that pays him $100 for each of his regular vaccine visits. I feel a bit guilty putting that money towards my own debt or investments, so I put it in his 529 instead.

I’ll take the tax benefits from it, though.

HAH!!! This is great!! A hustler before he even speaks or crawls! :)

Baby Dime looks so happy he has a checking account now! :) He’s very cute.

I hit the 200K milestone this month. It took me 48 years to get to 100K and only 2 years to get to 200K. Coincidentally (not!), I started tracking my net worth 2 years ago. Lol, so I definitely think it works.

I also use Personal Capital but sometimes it makes me sad when it tells me I’m behind others my age. I started using Status Money and that makes me feel a little better about where I’m at when compared to my peers. Lol. Both are fun though.

Look at you doubling your money like that!! The first $100k is def. the hardest – I wrote a post on that awhile back:

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

(And please do your best to not compare to others!! I know it’s natural and we all do it, but everyone’s in different places with this stuff (and have different advantages!), and you are doing fantastic right now. Keep it up! :))

Beautiful upward trend Mr J! You are rocking it (or is the copyright gone too?? ;-)

Cheers!

Hey, Jay! I’ve become a net worth disciple since January — I’ve seen about a 1.0% growth each month. As of today, I’m at $687,719.46 (+$15,151.90), which combines my savings/investments: $44,181.32 and retirement: $643,538.14. Feeling great about it, though I’m being cautious on the savings side — mostly FDIC insured CDs (1-2 year) at 2.0% and higher, and only about $2,600 in a Vanguard investment (VGSTX). On the retirement side, I did set up for auto-rebalance every quarter and will increase my contribution by 1% in the new year. Thank you, Guru! :)

You da man!! Bet it feels great checking it every month too, right?

It certainly does, Jay! Thanks for the awakening!

I’ve been tracking my yearly net worth for a while now but just started monthly updates and it’s been very motivating! I recently started a job after many years in grad school with pretty stagnant net worth so I’m enjoying that each month now is a record high :) Started the year at 17k, have since paid off debt, and I’m up to 32k (almost 2x!) with a goal of 40k by the end of the year.

That’s what I’m talking about!! Congrats on the new money and new job and especially that new degree! :)

We were up by 2.74% in the last month.

We also just had our 1 year anniversary of tracking our net worth :) The growth since we started tracking is crazy! I’m glad we started taking it seriously, but I can’t help but think of where we could be if we had started sooner.

1 year – wooo!!!!! Party time!!!

We had a pretty good month last month. We accidentally raised our net worth by more than normal…..I know what you’re thinking….accidentally RAISED your net worth? Here’s the story: I went to pay down one of our credit cards by a hundred, but somehow, the box for “pay off entire balance” was clicked…….so instead of $100, I paid over $3000, but that debt is now at zero. I didn’t even realize it until the next day when I noticed our checking account was negative by a few hundred dollars. I know that I could have called the credit card company and had them reverse it, but after assessing our financial situation, I let it be, moved some money around and enjoyed the relief at having that debt gone! We had $500 in a savings account at the same bank and $1600 in an account at Ally online bank that I immediately moved, and the rest was already in our checking account because my husband and I had worked a lot of overtime in the previous month. I was planning to pay off a larger amount on a different debt at the end of the month with the overtime money, but the joy of not having to deal with this stupid credit card anymore cancelled out my disappointment at not being able to pay down the debt I planned to.

Crazy, but it worked out. I don’t think I’ve ever had over $3000 in my checking account in my life, and randomly at the time that I do, I accidentally drop it down to nothing…. Plus is was nice to know that we could weather something like this and still be okay. (And don’t worry, we still have some in savings, so I didn’t even have to completely deplete my emergency fund)

What a happy accident! Congrats on being CC debt free. That’s major!

Thanks! It was a heart-attack moment followed by peace :)

Wowww yeah – what are the odds on that??? Did you end up getting dinged by your bank for the withdrawal? If so, you should totally call up and plead nicely to have it refunded as a special gift for you paying off your credit card ;) (and being a superb customer of theirs over the years too, of course).

Fun note to see today – def. wasn’t expecting that! Haha… (and how crazy it is that it can be mistakenly done like that? You’d think credit card companies would go out of their way to make it SUPER hard to do so they keep getting paid?!!)

I think that because I noticed it immediately and moved money from a savings account at the same bank, I caught it soon enough that the bank might not have even known. I submitted the payment on day 1, the withdrawal happened on day 2, which is also the day I noticed it and moved money…. I think because of the way banking books work, with all deposits counting before withdrawals when the close books at the end of the day, I barely made it by without a charge.

I haven’t noticed a charge yet anyway. Time will tell, I suppose ;)

Hey J, another all-time high for me too! :) $875K – up 15K!

It’s been entertaining watching our balances (J$’s and mine) tracking upwards so closely.

I’m expecting you to pull ahead, but so far I’ve managed to keep up.

With Mrs $ back at full time employment it is only a matter of time, though.

Heyyyy there you are, sir! Been a while! Guess you were hustling to keep one-upping me. I see how it’s going to be ;)

I think I’ve been tracking about as long as you have, and I remember thinking just how rich you are when you hit 100k. Ha! We hit 1,482,000 this month, which is an increase of $65,000. That might be among our top 10 monthly increases of all time. I’m getting nervous though. What comes up must come down.

WOW – 1.4 mill – nice!! How does it feel rolling around as a millionaire (and soon to be multi-millionaire) these days? :) Confetti and dollar bills falling from the sky every day, right??

Hey! I just found your website last week and started following it, and though I’ve heard of Personal Capital before, I didn’t want to sign up myself until I started reading a bit into your archives, ha ha. Now I’m hooked and checking it daily!

I’ve gotta say, I’ve never been one to think about our net worth much, but I’ve been really inspired by your blog to start looking at it more frequently, and I already feel much more motivated to save (I was already motivated to pay down our mortgage early, but the savings could use some work!). Thanks for what you’re doing!

Heyyy very cool!!!! Congrats on starting down the journey and enjoying it so far! It should only get better as time goes on! :)

Congrats on the new high. +23.5k! I can smell the million already, you’ll probably get there sooner than you think.

I’m far away from a million dollars but I’m surprisingly close to be able to live from my monthly cash flow from investments.

Investing to buy your own freedom is very motivating to me, there’s no turning back now!

I’d take hitting hitting financial freedom before a million dollars any day! Way to set your life (and lifestyle!) up like that so far!

July 1st- $698,688.61

August 1st- $712,404.96

+$13,716.65

All in Vanguard Total World Index fund. Hopefully at some point they’ll offer Admiral shares.

We never thought in our dreams that we would have this much. 20 years ago we just graduated college with student debt, credit card debt, car payments and had a small apartment. Now a paid off home and in the black on our way to a million.

What year is your corolla? Toyotas are mini tanks that last forever.

Paid off house – nice!!

Our Corolla is a 2005 :)

Hit an all time high – but does that really count when you’ve really only been tracking your net worth for 3 months?! :)

Still playing around with my tracking spreadsheet but I think I’m getting it closer to what looks good and what will help me. I paid off my furniture bill this month so only liability at the moment is the mortgage (which I’m working on paying off early). Thought I wasn’t going on vacation and was transfering banks (better interest rates – oh yeah!) and didn’t want to set up a bill pay account for the furniture bill so opted to take the hit from savings and jsut get rid of it (it was 0% but opted for seeing one less bill). Then the next day booked a vacation!! Oh well.

Markets were good to me this month too – various investments (401K and IRA) were up a total 2.65%. Net Worth = $606,286.40; +2.08% change from last month.

Tomorrow’s adventure is to set up a ROTH IRA at Vanguard. Now, do I just put the $5,500 in it all at once or do monthly payments for the rest of the year????

An age old question indeed :)

Here’s an article that made a lot of sense to me on it, and I’ve seen other similar ones circulate the community here: http://jlcollinsnh.com/2014/11/12/stocks-part-xxvii-why-i-dont-like-dollar-cost-averaging/

(in a nutshell it says if you have the money now drop it in, and if you don’t then dollar cost average)

Thanks J. For the link. I feel like to get me going on this path, and since I have the $5500 already saved and earmarked for this, I should just do it in one move and take the leap into starting a Roth. I can always re-evaluate how I want to contribute next years money. (After I read a few more of the posts in that link)

Totally! Just *starting* is the most important. And nothing’s ever permanent with this stuff, for the better or the worse ;)

I see millionaire status if this bull run continues into 2019. I think you should add the baby funds into your Net worth, until they turn 18 and it is out of your hands. Until then you manage it and it can be counted as a total family fund. Just a thought.

Haha yeah, I actually did include it all for the first handful of months, but then it felt weird and figured if any of the $$$ came back to me over the years then it would just be a nice addition to the net worth :) Vs the opposite of taking hits whenever it gets distributed later!

Dude youre almost at a mill!!!!

Hi! I’m at the very, very beginning of the journey myself with loads of debt so this was my second month tracking my net worth and it went up almost $6,000!!!

This will not be repeated every month because I “found” a small 401k I contributed at a former employer that I was just letting hang out in no man’s land. I grabbed it and pulled it over to a traditional IRA resulting in the giant increase.

So I did about $1300 on my own which is not bad with all the debt’s interest working against me. Just wanted to report in because I’m super stoked at the change!

YAAAASSSS good job!!! $1,300 in itself is huge – and even more empowering since it was fully in your control – well done :) You’re gonna have a great time watching you wealth grow and that debt go down over time!! Keep going!

Question for you – Did you ever consider only having one 529 for Penny, Nickel and Dime to save on the fees? Someone suggested that to me for my children awhile ago. At least in my state you can use the account for whichever child needs it.

I didn’t at first when we only had one kid, but over time some people have recommended it to me too :) I think you’re right that many states will allow you to use it for multiple people, but for some reason I kinda like having it all separated out like this… Depending on how much you contribute every year and if you’re getting tax benefits that would affect it too. (I.e. if you max out the tax benefits every year you’d want separate accounts to reap the most benefits vs just one account where you’d hit the cap faster)

I love you dad! ;)

Haha…. how the hell have YOU been, man?