My wife and I discovered the FIRE movement about three years ago. We’ve always been decent budgeters, savers, etc., but three years ago was when it really clicked for us… “We can retire early!”

It all came down to us figuring out our “FI number” and realizing it was reachable in our 40s.

Why the 4% Rule for Retirement Doesn’t Always Work

Most FIRE enthusiasts follow the 4% rule of thumb to figure out how much money they will need for retirement. It’s pretty simple, you just take your annual expenses, multiply them by 25, and there you have it — that’s your FI number.

That’s a great rule when you’re first starting out, but as you grow older and life throws you more changes, you realize that your FI number is actually a moving target. It changes as your future expenses change.

The reason my wife and I don’t have an exact FI number is because we don’t know what our exact future expenses are gonna be. There are too many variables. And not just small variables, BIG ones, like:

- We currently don’t own a home. We’ve accounted for rent, but this number could change drastically.

- We don’t know which city we’ll live in. Heck, we don’t even know which country we’ll live in.

- Health care costs are a huge unknown.

- We don’t have kids yet. No clue how much they will cost.

Each of these expense variables has a 25x impact on how much we need to save for comfortable retirement. So, instead of shooting for an exact magic number, my wife and I are mostly shooting for a “range.”

Here are our thoughts and some rough calculations…

Figuring Out Our FI Number: Constants and Variables

Before jumping into what we don’t know, here’s some of our living expenses we kinda do know. These are annual expenses based on what we reckon will be a fairly comfortable lifestyle for us.

Food: $6,000

Booze: $3,000

Internet: $840

Phones: $1,200

Cars: $2,400

Gifts/Charity: $5,000

Pets: $2,000

Amusement: $1,200

Travel: $5,000

Miscellaneous: $2,400

TOTAL: $29,040

I’m a round numbers guy, so let’s just call this $30,000 per year in fixed and constant living expenses. (Yes, this number will increase with inflation year after year. At this point, all I care about is Year 1 numbers in retirement.)

$30k x 25 = $750k needed in retirement funds to cover these expenses.

OK, so now we have to add in 3 x variables… Housing, health care, kids.

Housing and Future Rent Guesstimates

Since my wife and I aren’t ready to buy a house, we’ll include monthly rent in our living expenses. This is where ranges come in, depending on the city we want to live in and size of our house.

Low estimate: In Los Angeles, we can happily rent a 1 bedroom apartment in a good area for ~$2,500 per month. (We pay less than this now thanks to a sweetheart deal, but that won’t last forever.) So, total annual would be $30,000 as a safe bet.

High estimate: I don’t think we’ll ever live in a McMansion, but if we need an extra bedroom and wanna be in a good school district or something, let’s say it’ll be $4,000 per month to rent a place. That’s $48,000 annual in rent on the high end.

Low rent: $30k x 25 = $750k needed in retirement

High rent: $48k x 25 = $1.2 million needed

If we get the warm and fuzzies and want to purchase a home somewhere, as long as the monthly payments and expenses are less than $4k for housing, we’re covered.

Health Insurance and Health Care Variables

This one is the toughest for early retirees to figure out. Last year we had an awesome post from the Dragons On FIRE about healthcare in early retirement, which is a pretty thorough guide to trying to work out future healthcare costs.

Free option: For my wife and I, if we end up moving back to Australia, we could potentially get by paying $0 for healthcare. 100% of Australian full time residents have Medicare, and pay nothing for hospitals and doctors appointments. (Private health insurance is also an option, and apparently the average cost is only $2000 per year per person!)

“Cheap” Healthcare: Last year I spent some time evaluating health insurance vs. having no insurance and paying out of pocket for care. My wife and I skated by for almost 3 years without insurance, only paying ~$4k during that entire time ($3k of which was government fines). Per the “national average” for us, our costs apparently would be about $4,000 per year (including fines).

Anyway, I know many of you are going to disagree with this, but I’m gonna use $10k per year as our low annual estimate. This would cover either a basic high deductible health plan (HDHP) premium with low care use, or living without insurance and paying $10k out of pocket per year for fixes.

High healthcare budget: Also in last year’s post I calculated a HDHP insurance plan for my wife and I and worked out that it would cost a max of $20,400 per year. This covers all premiums for the policy as well as maxing out the family deductible every single year.

Low healthcare: $10k x 25 = $250,000 needed in retirement

High healthcare: $20.4k = $510,000 needed in retirement

Future Kids Cost

Quick update on our foster/adopt process: We’ve completed all the pre-approval Zoom classes and most of the onboarding homework. A social worker came and did 1 home inspection so far, and we’ve got a few more inspections, as well as interviews and more qualifying stuff to get through. All in all, I’d say we’re 50% of the way through the county approval process.

If we decide not to have kids: Then our cost is $0 and it doesn’t really affect our FIRE number at all.

Average cost of raising a child in the U.S.: Based on 2019 numbers, the average total cost that middle-income parents will spend on a child from age 0 – 18 is $284,570. If my wife and I adopt a child, I can safely say our expenses will be lower than this, because the state provides free healthcare, a small monthly stipend per child, a TON of support for education services and stuff like that. For our estimate purposes, I’m gonna go with an annual cost of $12,000 per child.

Cost for 1 kid: $12k x 25 = $300k

Cost for 2 kids: $24k x 25 = $600k

Alright, let’s add this all up…

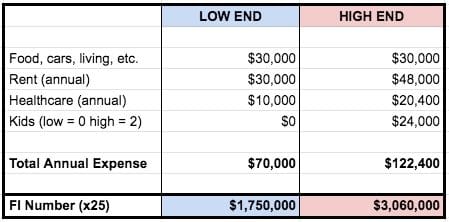

Annual Expense Totals and FI Number Range:

On the low end, it looks like we would need $1.75 million in assets for retirement. We’d live in a modest rental, have no kids, 1 dog, have subsidized or cheap health care, and do all the regular living stuff we enjoy doing today.

On the high end, we would need just over $3 million invested. We’d rent an upscale or bigger home, have a couple kids, a dog, max out our healthcare plans every year, and still enjoy the modest lifestyle we have today.

That’s a pretty huge difference in FI numbers!

Kind of scary to think about… the life decisions my wife and I haven’t figured out yet could have a $1.3 million impact on how much we need to save. And it might be 5, 10, or more years before we are even ready to make these decisions.

Coast FIRE: Options, Flexibility and the Messy Middle

I know a couple in their early 20s who have their entire life mapped out already. They have a dream house picked out, know exactly how many kids they want, plan to vacation in the same spot each year, etc.

On the flip side, I know some people in their 60s who still haven’t figured out what they want to be when they grow up! Having “plans” makes them feel boxed in, so they never commit to anything.

My wife and I are somewhere in the messy middle. We like planning, but we’re also open to change.

Adopting the Coast FIRE mentality means not only is our retirement timeline up in the air, but our magic FI savings number is uncertain, too. As uncomfortable as that may seem, my wife and I are confident that if we aim high and keep trying our best, we can handle both deliberate and unexpected changes as they come along.

[Read more: Slow down … FIRE is not a race]

Anyway I’ve been asked a lot recently, “What is your FI number?”… And this is why I don’t have a great answer. Somewhere between $2-3 Million? 🤷♂️ As life goes on and things get clearer, you’ll all be the first to know.

Do you all have a specific target mapped out? Or are you within a wide range, too?

Get blog posts automatically emailed to you!

Loved reading this passage about your FI number – and I think it’s so accurate that one should always remain flexible and make adjustments along the way. If there is one thing I learned in finance, it’s that nothing is static. It always changes, and you’ll have to be ready for the change.

PS – It’s so exciting to hear about the adoption process! Good luck!

Cheers,

Fiona

Thanks dude – foster/adopt is still really scary to think about. I’m amazed we haven’t been scared off yet. :)

I can really relate to this post! We have 3 kids and one was our foster child. We know our expenses now, but it is difficult to estimate when the kids will leave the nest and how much our budget needs to be then. What is our FIRE number???

This might sound cliche, but I think this is the reason side hustles and small income hobbies are such a great thing in early retirement. If you accidentally haven’t saved enough, or unplanned changes are sprung on you, you can possibly close the gap with a small side income.

Glad to hear about the kids and foster to adopt worked :) Any chance you’ll foster more kids again later in life?

Very cool about the adopting process!!! You’d be an amazing dad!!

One of my fav things about your blogging was when you shared funny stories about kids. :). I’m looking forward to experiencing some of that fun stuff!

I didn’t see anything mentioned about transportation in this list. It is usually one of the major expenses. Do you always plan to live in an area where you walk everywhere? You would also need to account for any public transportation.

Hey Chris! I put $2400/y for cars, and $5k for travel. Maybe I’m kidding myself, but I don’t think we’ll need more than this. Maybe if we moved to the country and had long commutes. Transport has never been a big expense for us. When we road trip, sometimes I include gas/car expenses in our travel budget.

Lovely post. I think flexibility is critical in financial plans, especially for younger people.

We adopted a toddler a decade ago (best thing we ever did) and found having one kid isn’t as expensive as people say.

We don’t live that frugally, just sensibly. I think costs escalate if you buy lots of new clothes and toys and go crazy on extra curricular activities and hobbies.

Travel can get expensive and is less flexible with more than two kids – unless you like camping.

In our mid 40s I discovered FIRE and played around with our numbers and realised we couldn’t fire in U.K. (where we were living) or Australia (where I’m from) for a looong time, so we looked for low cost of living countries. I worked out that if we sold up we could lean fire in Thailand immediately. I can’t tell you the joy this bought me seeing I had an exit from my job! A couple of years later we reached lean fire in Portugal/Greece. Another year on we moved permanently to Greece. Quit jobs and live a good life without working (aged 48). We’d have to work at least another decade to achieve this in U.K. or Australia, and I just don’t want to!

Good luck with your adoption plans. You’ll be amazing parents x

Thanks for sharing Sunny and CONGRATS on reaching FIRE and enjoying a non working life. One thing I’ve worried about with moving back to AUS is we’d have to adjust for the exchange rate for making portfolio withdrawals – and this changes over time. It could screw us if the USD gets weaker and weaker and that’s where the bulk of our assets are.

Thanks for saying your adoption was the best thing you did. Wife and I are hearing this more and more and it’s very encouraging to know all the hard times and struggle are worth it. Have a great week Sunny!

Yep, currency is a risk, but we will just stay nimble. Got half in GBP and half in AUD but spend in Euro! Handy to have the two different currencies, so just draw from the one doing well at the time we need to exchange. Coming up for house purchase, so hoping £ / AUD continue to rise! X

“$12,000 for annual children’s expenses”

My current bosses spend over $12,000/month in children’s expenses (day nanny, night nanny, private school).

I’m soooo excited about your journey on foster parenting. I want to have 2 biological and adopt FIVE!!! Do you want newborns or older children?

I still don’t understand FIRE. I want to change the world and leave a legacy. I wanna build cities and bring Reformation to many areas. One can’t do that “living on interest”. I’m not stopping til I’m a multi-millionaire…not just in assets…but bringing in that income on a continual basis. I want to be able to write out $50 million dollar checks.

Have an AMAZING week. Happy President’s Day!!!

Love the attitude Angie! 7 kids!!? That’s a big family! My Dad is one of 10 kids (all biological) and it’s amazing how close large families are. I have 20+ cousins just on my Dad’s side and love our gatherings. You have great goals!

Wow 12,000 a month!! They must have a huge income. My kids (2 kids 6 and 8) maybe cost a couple hundred to 400 tops a month. The 400 month would be I signed them up for one sport (ice hockey, ice skating lessons, swim lessons, dance they’ve done it all). Granted college is already paid for and we haven’t got to braces yet.

Sounds like that darned Al Gore is back with his fuzzy math. Millennials these days just can’t commit to anything.

Who is Al Gore? Just kidding. ;) Love you Gladys.

We buckled down and really started pursuing FIRE around 2016; our projections back then have been completely blown away (invested assets are 71% above where I expected to be in February 2021, or about three years ahead of schedule). Meanwhile our routine expenditures have somehow decreased. So we’ve stopped focusing the number — originally $891k with a paid-off house in 2030 — and instead are looking harder at quality of life.

We’re thinking about each going 60% at work in a few years, if my wife can maintain her employer’s health coverage. That means four-day weekends all the time and still easy saving for things like a car or vacation or new roof as needed… all without touching investments. It absolutely helps that we’ve decided on no kids and only have nine years left in our mortgage. I’m excited instead to be the cool aunt and uncle who host our then-teenaged nephews in Europe or Mexico for a week or two every year. :D

Everybody loves the cool aunt and uncle that retired early and are living a happy and free life!

Congrats on crushing your timeline and it’d be great to go part time at work. Easing into ‘retirement’ is sometimes a better transition than a cold hard stop. I think it’s smart that you’re focusing on quality of life and making more plans around that. Being close to FIRE means making decisions and not having to worry about the financial consequences. Have a great week Adam!

This is one thing that late starters have as an advantage over the young ones pursuing FIRE :) We are past that stage of wondering if we will have children or not and other life changing scenarios. But totally agree that the FI number is constantly evolving to cater for unforeseen events and good to plan for as much as we can. Cheers!

Very true – FIRE gaps and goals are a little more clear cut as you get older. Have a great week LateStarter, hope all is well down under!

People’s situations can change in the blink of an eye and FIRE numbers can change along with it. I just want to know what it feels like to be financially independent, that is my number one goal.

Maybe my FIRE number will change after some time as well? Hmm.

Hey David, from what I hear, the feeling when you’re FI is the same as when you’re not FI. There’s certainly a freedom associated with reaching that milestone, but you can feel much of that freedom *on the journey* well before you reach the FI point. Or so I hear!

Hi Joel,

At some point numbers become hard for the brain to comprehend. Once you start talking about numbers in the millions the comparisons seem immense. However, us fire walkers have to keep in mind that compound growth is a game of exponential increases. Your two numbers 1.7M and 3M are vast when viewed from a linear mindset of a person toiling away one year at a time. However, viewed from the lens of exponential growth, your delta is just 75% from 1.7M to 3M. Once you reach 1.7M your job is no longer your portfolio driver, instead the portfolio becomes its own driver (as long as your leave it ALONE). On my fire walking journey the first million was the hardest. After that the beast took on a life on its own, and it seemed no matter what i did the numbers kept doubling every 5-7 years (give or take). That is all to say, I do not think you two numbers are that different. If you want kids and a house, you just have to work another 3-4 years (which does not seem like much of a cost given the returns).

The problem eventually becomes letting go once you make your number…when there are so many other things to save for.

NZ

Thank you. This is exactly what I needed to hear.