The concept of “coast financial independence” can be tricky to understand. Here are some fun comments and questions I’ve received recently…

“So, let me get this straight… if you are spending the exact same amount that you’re earning each year, it sounds like you’re living paycheck to paycheck! How do you grow wealth when you’re not putting anything into your retirement accounts?”

“What happens if you accidentally lose your job or don’t earn enough each year. You’ll need to withdraw from your retirement accounts and you’ll be going backwards!”

“Don’t you want to retire early and stop working?”

“When the stock market bubble pops, your plans will be screwed.”

“I’d love to quit my job and slow down, I just don’t have the cajones to do it haha.”

I’m gonna talk about each of these from my perspective, but I’d also love to hear thoughts and feedback from you other Coast FI or Slow FI peeps out there!

An Important Baseline Is Needed for Coast Financial Independence

First and foremost, Coast FI isn’t the right strategy for everyone. Nor is it even an available option for some people. Intentionally slowing down your path to financial independence or stopping your retirement contributions requires three important things:

- Time: The younger you are, the more flexibility you have in your path to financial independence. Because Coast FI depends on compound interest, a longer time horizon is necessary.

- Existing assets: There has to be at least some amount of money or wealth already sitting in a retirement account that will grow over time. If you’re gonna leave your campfire unattended, you better first stack some large logs on that sucker before walking away!

- You still gotta work!: Coast FIRE lets you reap the benefits of financial freedom early, but it’s important to remember that without actually hitting your full FI number, you can’t stop work completely. Sabbaticals and breaks are OK, but “work” is still a big part of the strategy.

Everyone’s blend of these three necessities is different. If you have more of one, you can afford to have less of the others. It’s flexible. This is what makes Coast FIRE such a unique and personal life plan.

Having a 0% Savings Rate: How Does That Even Work?

I’ll admit, it’s a little scary earning only as much as I spend each year. Living paycheck to paycheck is something I’ve avoided my entire life!

But what allows me to sleep at night is my confidence in compound interest. Sounds nerdy, and it definitely is! It’s also a little risky, which I’ll talk about, too. Simply put, the reason I don’t have to keep contributing to my retirement accounts each year is because the growth of my existing assets does it for me.

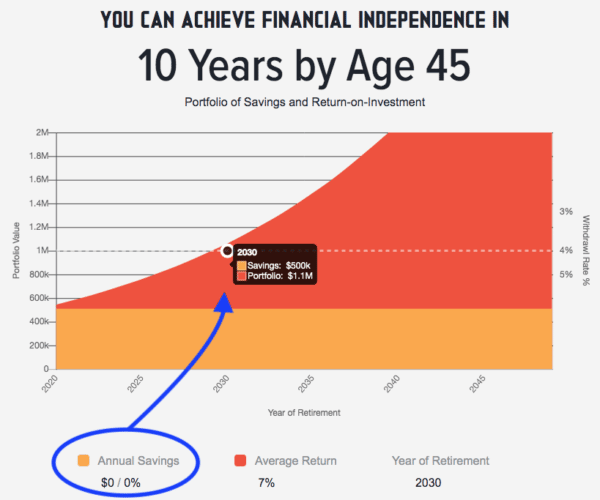

Let’s take a look at a Coast FI scenario using this FIRE Calculator from the awesome dudes over at Playing With FIRE. 🔥 For this scenario, I’ve used the following inputs:

- Age: 35

- Annual expense: $40k per year

- Annual Income: $40k per year (0% savings rate)

- Number needed to hit FI: $1 million

- Current net worth: $500k

Based on a 7% assumed growth rate, someone who is about halfway to their financial independence number can retire in 10 years without contributing anything new to their portfolio.

Some people would call this model conservative, and others would say it’s risky … let’s take a look at what happens when things don’t go quite according to plan.

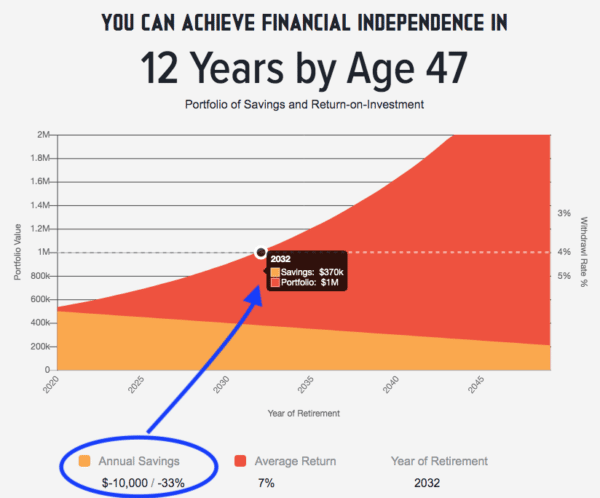

Scenario: What If We Make Less Than We Spend? (Negative Savings Rate)

Let’s now assume that we have trouble keeping steady employment and only earn $30,000 per year instead of $40,000. Unfortunately, this would mean pulling out $10,000 per year from our retirement savings to cover annual expenses.

- Age: 35

- Annual expense: $40k per year

- Annual Income: $30k per year (-33% savings rate)

- Number needed to hit FI: $1 million

- Current net worth: $500k

Looks like even if our savings rate goes into the negative every single year, it only adds two more years to the FIRE timeline. Even though we’re withdrawing $10,000 from the portfolio each year, the compounding growth more than makes up for it.

Retiring at 47 instead of 45 is not a huge deal, is it?

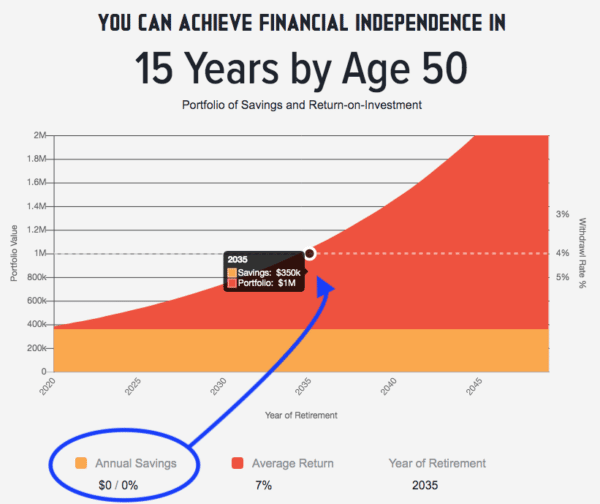

Let’s now take a look at if/when the stock market shits the bed.

Scenario: What If the Stock Market Crashes 30% Right Now?

Let’s say the stock market crashed 30% next month, which brings the portfolio value down to $350,000. What does it mean for the growth timeline?

- Age: 35

- Annual expense: $40k per year

- Annual Income: $40k per year (0% savings rate)

- Number needed to hit FI: $1 million

- Current net worth: $350k (Down 30% from $500k)

If there was no immediate recovery after a crash, and we still assumed a 7% annual portfolio growth, the timeline now extends out to age 50 to achieve financial independence.

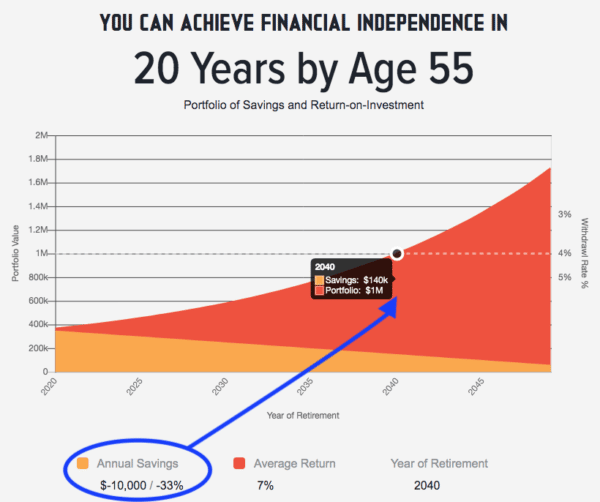

Now let’s look at one last scenario … with both the poop hitting the fan and a lower income vs annual spending.

Scenario: What If the Market Crashes 30%, AND There’s a Negative Savings Rate?

- Age: 35

- Annual expense: $40k per year

- Annual Income: $30k per year (-33% savings rate)

- Number needed to hit FI: $1 million

- Current net worth: $350k (Down 30% from $500k)

Wow — looks like even with these factors, financial independence can still be achieved before traditional retirement age. You can see why a long time horizon is necessary when pursuing Coast FI. If your situation changes or things start to go wrong, time can correct things naturally, as long as you have enough runway.

Work, Work, and More Work Is Part of Coast FI

Three years ago, I would have probably looked at the charts above and thought, “There’s no way I want to work for another 10 years, let alone 20!” Many people feel the same when they first discover the FIRE movement. “Retirement” is the ultimate goal for those who don’t want to depend on work.

But my view toward work and early retirement has changed over time (and is still changing). I envision work being a big part of my future, no matter how old or how much money I have. If I’m going to be working anyway, I might as well discover or create positions that I really enjoy. This takes time to figure out, and possibly means starting from scratch in some industries. Coast FI gives me the flexibility to earn a low income for a while — maybe even many years — and still have a comfortable retirement nest egg later.

A fun thing to think about … In 20 years, I’ll probably be working on a project or doing a job that isn’t even invented yet. Just like ~20 years ago, blogging wasn’t even really a career. The unknown used to scare me, but now it kinda excites me.

The Opportunity Costs and Flexibility in Coast Financial Independence

There’s a bunch of opportunity costs that come with slowing down retirement savings and pursuing coast FIRE at a young age. I’m experiencing some of these costs right now, and let me tell you — it doesn’t feel great :(

First, I’m choosing to work part-time through some of my “higher potential income” work years in life. This isn’t a huge deal, because I’m still confident in the math that I don’t need a massive income to achieve early retirement. But, it hurts thinking about lost opportunity, regardless.

Another opportunity cost is not being able to take full advantage of buying more stocks during market dips. Earlier this year when the stock market tanked, my friends were all socking away excess income into their 401(k)s, Roth IRAs and other investments. I didn’t get that opportunity because I had no excess earnings. We’ll inevitably have crashes and dips in the future that I can’t take advantage of, either.

That said, Coast FI is flexible. If we wanted to get back onto a more traditional FIRE path, that’s always an option. I envision some big income years for me and my wife and some zero income years in our future. Time will tell how it all plays out!

Coast FI Takes Confidence!

One of the last comments I heard was “I’d love to quit my job and slow down, I just don’t have the cajones to do it haha.” After digging deeper, I found out this person is actually already past their FI number. They could stop working anytime, and have enough money to live the rest of their life. All the math and FIRE spreadsheets in the world couldn’t convince this person to quit their job, and that’s totally OK!

Everyone has different levels of comfort and confidence. At the end of the day, we need to follow the FI journey that makes most sense for us individually. Whatever keeps you stress-free and sleeping well at night!

Any fellow Coast FI peeps out there with 0% or negative savings rate? Am I the only idiot trying this?

Get blog posts automatically emailed to you!

Joel,

This was a great post – and I learned something new about the coat financial independence movement.

I am of the same opinion as you: I see work being a part of my every day life – regardless of my age or wealth status. Honestly, I think I would not be fulfilled if I stopped working entirely. Work is just a way of life for me. Like you, I have the mindset that since I’ll be working for the rest of my life, I might as well do something that I really enjoy!

That’s where I stumbled upon blogging… what an incredible experience. And honestly, I wish I found it earlier. Better late than never, I guess!

The Millennial Money Woman

They say if you really enjoy what you do then you never work a day in your life. Whilst I’m still not 100% there yet myself, I’ve caught a glimpse into what this actually means and how to live it myself. Sounds like you have too with writing/blogging! Cheers MMW :)

Nice article, Joel! Coast FI is an interesting subset of FIRE. Assuming this strategy allows you more time to “live” now, you’re basically enjoying some of the freedom of retirement earlier—before retirement. It’s not for everyone, including me, but I’m always impressed when people think through interesting, sound financial plans that make sense for their own lives. Cheers

There’s definitely a bunch of unknowns within Coast FI plans. Some people are OK living with uncertainty, while others want a more stable or predictable FIRE path. Either way, we all gotta figure out what’s best for us! Cheers Ben, have a great week!

Interesting topic. Like yourself, I don’t think I could completely stop working. Instead if I did slow down, it would be something I enjoy much more and probably work part time. The coast FI is interesting topic.

Previously, I had thought about the concept in regards to our rental properties as if we simply do nothing they are positive cashflow and in around 25 years they will all be fully paid off. Giving us a nice retirement savings if we sold them.

As for actually trying the 0% savings I can’t pull that trigger but good for you! The math makes sense and I wish you the best and looking forward to updates!

Thanks Fred. In all honesty, the 0% savings will most likely change. It’ll go up, down and sideways as we navigate work opportunities and take time off. Some years we’ll have a huge income/expense gap and be able to sock money away. Some years we might take completely off. I’m not sure what the future holds, but I doubt it will be linear like the graphs. :)

Love the rentals idea! If you snowball your positive cashflow now they’ll take much less than 25 years to pay off :)

Wife and I have been on the path to FIRE for about 5 years now. We are only about 4 years from hitting our goal. But with our 1st child born this year, we have decided to cut back on work hours to spend more time with the baby. It will delay full FIRE by a few years but it’s worth it to us.

It’s great having the flexibility of a FIRE nest egg to keep growing even if we stop contributing for a period of time.

Spending more time with your kid… I can’t think of a more noble cause! It’s why you pursue FIRE in the first place, to give you choices and flexibility. Congrats on the baby!!

Howdy, I’m on this same path.

After fully funding an emergency fund and my retirement account – based on 7% growth over 25 years and ignoring potential social security payouts – while cutting back drastically on lifestyle creep – I pulled the plug.

Walked away from all work for 4 months to spend time with family (of 5) and hardcore exercise before accepting a persistent offer to provide insane niche value for an ownership stake that will start paying out in 1-2 years.

Went from significant income to a base salary of peanuts. In return I have a balanced family/work life, great health, great sleep, and now drive in a company founded on strong ethics – one that will likely provide the equivalent of an independent FI income stream within a few years.

Sure, assuming I never earn another penny above bare minimal living needs I’ll not be retiring until 62… But at the old gig I was on a path to die far earlier than that (even if FI was then 6 years out).

Pulling the plug has freed me to pursue opportunities where I provide the most value on my terms – and in return this greater risk provides for a chance of greater reward (not solely monetary).

Money’s a tool, and I prefer to use it rather than worship or be used by the pure pursuit of it.

I hope you’re keeping a journal or writing a book about all this Chris. Health, happiness, family, balance… I wouldn’t trade it for a million dollars. :) Cheers, and thanks for sharing!

We are doing something similar to this, or at least plan to in the future. I’m 30 now and continuing to invest but by the time I’m 40 will hopefully be to a place where I have invested all I need to to get where I want to be when retirement comes. At that point continuing to invest wouldn’t make a huge impact compared to the compound interest, so I plan to stop investing and start living in a little more freedom, sort of a pre-retiremnet where I’m still working but also able to travel and do things I didn’t do as much before.

Nice one Shane! At some point your money starts working harder than you do, and growing faster than your contributions. Glad to hear you’re putting in the hard work early, so you can reap more freedom and benefits later!

Not disagreeing that this concept works and that you are working to effectively get more freedom early and knowing that you will likely have some income coming in. Just concerned you are not accounting for inflation correctly here. In 20 years you would likely need more than $40k a year to support current lifestyle. I think with the FI calculator you can’t enter the inflation directly so you need to account for this by lowering the expected “real return”. So I would suggest trying this with 5% vs 7% to account for the inflation in the timelines (which is the default equities return in the calculator).

Great point Lucas. These figures were to prove the concept, not the exact dollar amounts or timelines. I should probably write a whole other article about inflation, estimating returns (underestimating vs. overestimating), and also how $1M is probably not enough for many people to retire with.

I enjoyed the post, nice way to shed some light on Coast FI. The reality is that most of the people who hit early retirement aren’t doing nothing and I’ll bet you a bunch of them make some money doing things they enjoy. For me it hasn’t been about the work, I enjoy having something to do especially something I am passionate about. Its the choice, you have the freedom.

I’ve noticed that too Matt. Early financial independence brings about creativity that keeps people working and spending time doing things they enjoy. :)

Joel,

I’ve been interested in CoastFI for a while. It’s more or less what I planned to do back in 2012-2013 when I left the corporate world. I had enough money back for a good long FU, but not quite enough to say it was time to retire early.

Jenni and I ended up taking a lot of trips between then and now, and I haven’t worked more than maybe 1100-1200 hours per year since–I ended up running a couple of businesses, and things worked out better than expected. We reached FI in 2018, but I could have kept that Coast sentiment going for a while.

I think the most important part is ensuring you’re doing what’s healthy/what you can maintain over the longterm. Set yourself up for success.

Congrats! I think slowing down towards the end of the FI journey helps with the lifestyle transition too. If you’re enjoying what you do (and if it’s healthy/sustainable) then it doesn’t matter really when you cross the FI point. Cheers for sharing Chris!

Thanks, this is a great article. To be honest, I did not even think about such proportions. Your graphs clearly demonstrate what is difficult to explain in words)))

Took me years to get m head around it. (And even longer to get my emotions in line with Coast FI!). It’s important to note too, as others have mentioned, that all the graph data can be manipulated by inputs. So everyone has to create their own numbers and path that they are comfortable with :)

I didn’t realize this had a name! I’ve been thinking hard about it lately; the product I support is evaporating at the end of the year. Before picking up some new skills I was concerned about my continued employment. My wife is now making enough to support the entire household if necessary, so nothing panicky. And we’ve tipped $500k in invested assets… so like your example, it’s only a matter of time.

Assuming her company continues to do well and she still enjoys her work, I’m kinda looking forward to both of us dropping to part-time employment in five or six years. Four-day weekends with company-sponsored health insurance sounds like a dream to me!

Sounds like a great plan :) Remember it might not work out so linear in real life. You might have years where you both are fully unemployed and traveling, and some years when you both want to work full time. The good news is most of the hard work is done (Congrats on passing 500k!) so now you can afford to start thinking about lifestyle vs. money when making decisions. Cheers for sharing Adam!

I had no idea there was a name for that approach, but I’m considering this as an option in a few years. I’m working on getting training to start as a financial coach and would love to grow that, plus some other supplemental income steam perhaps like freelance writing, to a point where I make enough money to support my family in a live on the road type of situation. We’d love to have a big RV and travel the country seeing all it has to offer. My kids already homeschool, so that side of things won’t be an issue. Living that lifestyle is worth pushing out FI since that what I wanted to do once I reach FI anyway. If I can grow my coaching business plus other wise things to a point where we can exactly live off my income on the road, I would consider pausing retirement investments so we can live the way we want now instead of 15 years form now. That would likely mean my retirement investments don’t reach FI level until 65 or so, but that’s OK. It’d be doing something I’m passionate about for income now, while traveling and doing what I love with my family.

It’s so great to hear you’d prefer to be doing something your passionate about while traveling with family vs. trying to retire earlier. Those freelance and consulting gigs provide a lot of flexibility!

One quick note of caution… The reason I’m quite relaxed about my timeline is because I have a pretty big buffer on FI dates. If things go wrong, my timeline is pushed out a few years and that’s not a huge deal. But, if my timeline had me retiring at 65, and things went wrong, it might push my real FI retirement date out into my 70’s. This scares me. Not because I won’t *want* to work at that age, but more because I might not be *able* to work at that age. Something to think about!

It’s funny; before I knew coast was a movement, I was suggesting it to younger friends who were thinking ahead to having a family and taking time off work.

This could solve so many problems in that regard and protect against worst-case scenario-divorce. Think how many- usually women- take time off for family obligations. And all too often, face a divorce after being out of the work world for years.

If you use those single years to get that nest egg (in your own name. cough.) then stay home for few years… that cushion is there to protect you. If things play out as you’d like, then you have covered your half of the retirement cushion:-)

Not only is this a “worst case” protection, but I think it would give a stay-at-home parent a little more confidence in the situation, which is better for everyone.

Of course, that’s assuming you keep that money invested and don’t allow it to become a slush fund during single income years. But even if you do… it would be like having a part time income while staying home if you are careful about withdrawals.

Hey Ms. B! That’s an interesting take! :) I don’t know about the protection against divorce bit, but I can definitely say that building a nest egg early in life (either when single or as a couple) gives much more flexible work options for a couple later in life. For my wife and I, we can both work, one of us take time off, or both take time off. Whatever scenario we choose is probably financially possible if we make enough income to cover our expenses together. Thanks for reading and have a great day!

This sounds more like a “backFIRE” strategy – one that young folks will regret.

For several years, I was a manager hiring and firing people in a up-and-down business, seeing thousands of resumes and I would have just thrown away any resume of someone that didn’t look like they were trying as hard as they could while they were working. It was OK with me if they had taken time off or slowed down specifically to raise their children, but any resume that looked like they were putting in minimal hours to get by would not get thrown away without a second look.

So I would caution people that anyone doing this needs to realize the risk of a long term hit on their earnings and even their employability in their field. If you take non-challenging jobs and take lots of time off, who gets promoted? Who gets let go in a downturn? If you are looking for work, how do your accomplishments, job responsibilities and salary history stack up against your peers?

If you are “near FI” or “already FI” there is little risk to your financial future if you get let go, so slowing down is a great idea. But it seems really odd to list being young as a good indicator of who should consider this strategy. They are not FI yet, they need to work and this strategy makes them look like less desirable employees.

Thanks for sharing your experience and cautions to young folks! All great points. Before leaving any career or field it’s important to consider how time away might negatively impact the chances of jumping back in (if you need to).