Another new month so you know what that means – time to update the ol’ net worth! We’re onto month #118 in a row here for us, and still one of the best moves we’ve ever made for our money.

Nothing keeps you more accountable than knowing where all your $$$ is (or isn’t!) at any given month. So please please PLEASE start tracking this stuff if you’re new here or haven’t taken the time yet. Your wallet will thank you later for it, I promise!

(And if you need help figuring out what, or what doesn’t, go into your net worth, here’s an in-depth post I recently wrote that might help point you in the right direction (though of course go with what makes the most sense to you): Gray areas of net worth tracking)

Alright, here’s how last month went down for us… pretty much summed up in one gif:

(That’s me just going with the flow, haha… and probably exactly how I look on the dance floor :))

How October’s $$$ Went Down:

CASH SAVINGS (-$2,108.17): Had a helluva good time this month, however unfortunately I kinda forgot about the whole “working for money” part again, oops… I still struggle with it after all these years because I treat these projects way more *passionately* than I do *businessy,* and honestly I have no idea how I’ve managed to support my family for so long on these websites, haha… I’m just waiting for the internet police to show up one day and tell me the party is over!

THRIFT SAVINGS PLAN (TSP) (+$612.14): Work it, wife! Her monthly contributions just keep on adding up, and we’re already over $7,000 in just a year of setting it and forgetting it… These guys and all 401(k)s and similar are just money waiting on a platter for you to scoop up… Make sure you’re getting your employer’s FREE matches and just gobble it all up while you can!! Easiest way to make money!

ROTH IRAs (+$2,855.29): A solid jump here too – courtesy of the markets climbing which still shocks me each and every month lately… I’ve had enough of the warm and fuzzies, and just want it to hurry up and crash again so we can get over it! Stop teasing us for so long!

SEP IRA (+$10,723.23): Same scenario here as well… Yay for the increase, but just means more of a drastic drop once the fateful day comes… (Can you tell how I really feel about it? ;) The only thing it’s good for right now is inflating all our net worths!)

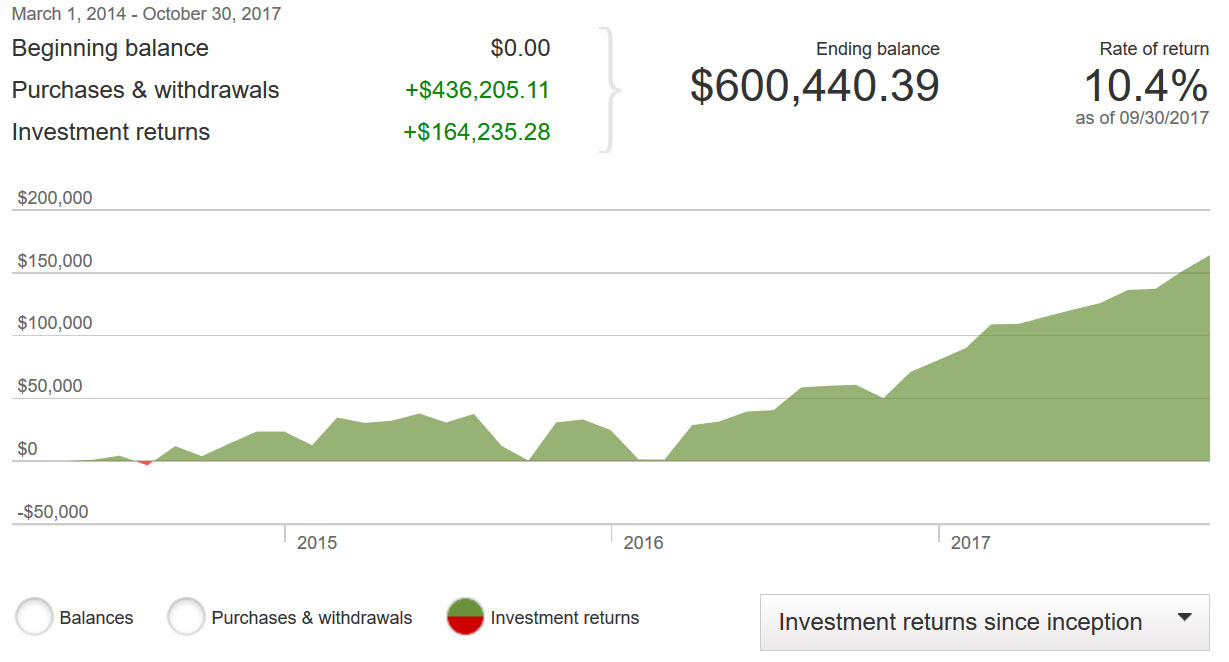

Here’s a current snapshot of our account, where 100% of the money is invested in VTSAX:

CAR VALUES (-$24.00): Nothing too crazy going on here, just the cars doing what they should be doing, albeit not losing *as much* this month as usual… Then again, Toyotas are known to be pretty solid vehicles, so not gonna complain about that!

Here are the current values of both our cars via KBB:

- Lexus RX350: $11,489.00

- Toyota Corolla: $3,733.00

CAR LOAN: (-$470.64): Chipping away each and every month… And not only at my Lexi’s paint job either (womp womp womp….) Here’s another shot at her back side after I decided to try and run over a fire hydrant:

(The answer to what I ended up doing about it, btw? Taping it for the win!! Similar to Hank Moody in Californication, I seem to get this strange satisfaction by riding around in cars with cosmetic imperfections… We’re nowhere close to Frankencaddy levels yet, but we got the first ding out of the way now, so all pent up anxiety has been released and now we calmly wait the future war scars to come ;))

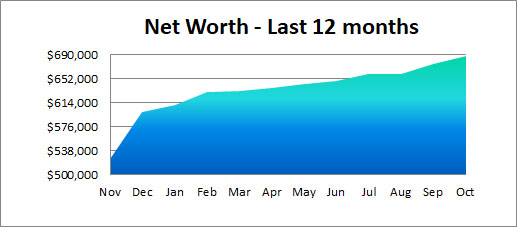

And that’s October! A $12k increase, mainly due to the markets…

Here’s a look at how the past 12 months have gone for a broader view:

And then of course, the values of both my kids’ net worths because we’re nerds like that; (notice I keep the 529s in theirs vs mine – just another of those gray areas you gotta figure out when tracking

How’d your month go?? Anything new and juicy going on?

As always, you can find all 100+ of my net worth updates here if you want to see how it’s progressed over time (almost 10 years!), and then of course if you’re feeling feisty you can check out 400+ other bloggers’ net worths here that we track: Blogger Net Worth Tracker. I’m currently #108 on the list.

And as I said last week, remember that your net worth does not = your self worth! But just like self worth it IS important to gain control over, which then makes you one helluva force to be reckoned with.

So get out there and OWN it!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

That’s a solid increase over the month and year. Is a mill still your target? If so when do you think you will achieve it?

For us we are targeting $4M by 45 years old (9 years from now). We have some expensive community projects we hope to work on once we FIRE.

Beautiful! I’m really shooting for financial freedom more so than $1 million, but we will have to cross that mark to get there so it is very much on my radar :) I think we’ll hit it in my early 40’s (I’m 37 now) and then mid-40s the freedom… unless we keep popping out kids haha…

$4 Million is a helluva milestone!

Your monthly net worth increase is total awesomeness. We’re also enjoying the markets being on fire. No pun intended :) We’re about $11k away from a major milestone I’d love to hit before the end of the year. It’s pretty doable if the markets keep going. Fingers crossed!

ooh nice! are you going to tell us what that milestone is or leave us hanging? ;)

This is one of the reasons why I track my net worth – to enjoy the growth of my money and nurture it. I am happy if the market goes up or down. It doesn’t really matter. If it goes up, I am getting richer. If it goes down, I will be backing up the truck to seize the opportunity. I made a few mistakes during 2008 and 2009. If the next time the market downturn happens, I will be ready.

Congrats on the nice net worth increase! I would just enjoy the moment and not worry about the fateful day too much hehe.

We have a Toyota Corolla too and have been loving it so far! It’s energy efficient and not expensive :D

I just read somewhere that Toyota’s are the top car owned by millionaires :) So go us!

Just hit $367000, up $7000 from last month. Hope to hit $375000 this month.

Congrats!

Income statement?

Oh man, I used to publish those but took me sooo much time… and got so wonky once I became self-employed!

I enjoy watching your net worth tracker because it gives me hope. I am always especially intrigued by how much your investments go up each month. My friends and I are having a huge debate at the moment. They dislike financial advisors and only buy ETFs privately; I dislike ETFs that only mirror the market and enjoy having a financial advisor who sometimes gets me higher than the market.

What are you doing? Financial advisor or private ETFs?

In a perfect world an advisor would *always* make you more money than you doing it yourself, but sadly it’s rarely the case so I just pluck them off directly from Vanguard and stick to Index funds :) Or really, index “fund” since I only rock one right now – VTSAX.

I recently confirmed this through a non-financial related field. In the book Thinking, Fast and Slow (an excellent book with a lot of useful info for money folks) the author describes looking at the statistics for fund management. Not only did 2/3 of fund managers not beat the market, but there was no correlation between successful money managers and success year to year. In other words, there was no statistical correlation that showed some fund managers had a knack for it; some people just got lucky some years. Interestingly enough, when the author, Dr. Daniel Kahneman, asked the firm’s top executives how much correlation between who was successful year to year, they sheepishly said, “probably not much.” They were only surprised that it was statistically zero.

That’s because, as Dr. Kahneman explained, a fund manager isn’t guessing a stock’s future value; that person is trying to determine whether people will think that price is too high, too low, or just right. In other words, they’re trying to predict the psychology of others.

It bought home the idea that for the FIRE crowd, the best option really is in index funds. It’s always nice to get independent confirmation of these principles, in this case from a psychologist writing about a psychological principle and not necessarily about finances.

YES!! Love all of this!!! And none of it surprises me of course as once you learn/see this you start seeing it everywhere :)

Not to mention… that author ended up going on to win a Nobel Prize for heuristics: the personal bias that influences every decision we make. Awesome read, I highly recommend it to everyone. I hadn’t even thought about applying it to finance, but you make a great argument for it.

JD

Still a great trend, even though your cash took a bit of a hit – oh well haha. I don’t think you’ve got to worry about the Internet Police coming to shut anything down. We got your back.

I just set revised NW goals with the wife yesterday! :)

We’re having a good run because of the market too. Waiting patiently for that to fall. We are even more painfully close to a big milestone. I was hoping to tell everyone about it this month but looks like well have to save it for December or January.

I hear fire hydrants jump out of nowhere sometimes!

It would be cool if you cross over Millionaire status so you can say you were one at some point in time even if it all crashes and takes a while to get back there haha…

Mine keeps hovering at about $315k. Investments keep going up but I also had to spend $16K last month on 2 new HVAC units. Very good price for what I got but its still a kick in the groin. I do count my house equity for my net work but not for my retirement number. I do not count my 529s which are at about $120k right now. I figure they will inadvertently count later on when I’m still socking away money while my kids are in college.

$120k – wow! That’s a nice stockpile there man, well done!

Those $16k expenses are exactly why I still rent, ugh…

Hey J. Money…Stop asking for the market to crash. Maybe from now on it will go steadily up forever. One can wish, right?

Great Job. You spent some cash, but your net worth is still climbing at a great pace. That sucks about your Lexus. The cost of high gloss paint for a new car is expensive. I don’t know what I would do. It sticks to shell out the money, but it is a very nice SUV to not have the body work done.

I’m eerily at peace with the scratches right now so it’s all good :)

Thanks for sharing again! Can’t wait to get it if debt so we can start this!!! Thanks for the reminder at the end!

I get that net worth is a good snapshot of your financial health, but I struggle in using it as a goal for myself since my net worth is largely out of my control. The stock market is 100% out of my control and the value of my home is largely out of control apart from me making some improvements and keeping it in good shape. I tend focus more on what I am putting into my 401(k) and Roth IRA every month rather than the overall value of my investments.

Yup yup, just depends on what you’re trying to get out of it all. I know some who check it weekly, and others who do it yearly – whatever turns you on! ;)

Ha – I’ve noticed before that we track similar numbers, but today I can see how close they are. I don’t think I can post a picture here as proof, but my net worth as of today on Personal Capital is $691,662, up around $11k in the last 30 days.

Keep plugging away!

Wow! I’m gonna have to start including my coin collection and marbles to try and one-up you! ;)

You joke about the marbles. But maybe you should include them if they’re worth this much: https://www.bostonglobe.com/business/2014/10/20/for-marble-have-you-lost-your-you-know-what/8fTIioRogDClmSBmntUonI/story.html

It’s a good thing I’m not drinking anything right now as it would have been spit out across my entire screen here!

You are getting some huge gains from staying invested in the markets. Can you share if you contribute a standard monthly amount of cash to your retirements and 529s?

I try to keep my investment contributions routine as possible, but some months it can be tough to hit a contribution goal if I deviate from the budget.

Thanks!

Oh, sure!

I add in $50/mo to each of the 529s (two kids).

And then for my SEP IRA and ROTH IRA I actually invest in one lump sum each year because my income is so varied from my projects… I totally recommend spreading it out across the months if you can though and then automating! It was a lot more fun doing it that way, and you get to take advantage of dollar cost averaging :)

I’m doing a big dance this month because we are *finally* not bleeding tons of cash every week, I won’t have to write a reno check for at least another week, we have cash in our pockets, we’re only paying for one Bay Area home right now instead of two, (though we are still paying for one here and one in SoCal) and we are now in the phase of home ownership where we can take the work slowly (and more cheaply) instead of being super rushed every day.

Gotta tell ya, it feels SO GOOD.

The cash and total NW are finally perking up so first I’m focusing on the smartest ways to eliminate mortgage debt (& to reduce our monthly payment), and researching where we should be investing our money to grow it like those crazy bean plants we’ve been sprouting from JuggerBaby’s daycare gardening project.

YAY!!!! Well done, friend! And so nice seeing you again in person last weekend – it felt like it was forever since we last saw each other?

Just curious – the chart WAY at the bottom shows a monthly income at $20k – is that where you guys are sitting?

Hmm… you mean in that Personal Capital snapshot? Nah, that’s not mine – just a stock one to show what Personal Capital looks like when you use it :) I still track all my $$$ through spreadsheets the old school way.

Amazing net worth and solid growth. Nicely done sir!

Congrats on doing so well J$!

I keep thinking the same thing with the stock market. It will obviously have a big drop at some point (which is making me keep too much cash in a savings account). I know it’s folly to try to time the market, so I agonize over this every day.

I love the TSP (my wife is a federal employee (or federal agent, like I like to say)). We have it invested in one of the lifecycle funds, and the returns thus far have been solid. Absolutely awesome, set-it-and-forget-it investing. (The only thing were’re considering here is to put the money into an even more aggressive fund).

Nice! And totally agree w/ the more aggressive route, but my wife likes the “safer” lifestyle one too so she’s there as well :)

I fantasize every now and then about cashing out all the $$$ and then in a year adding it back in, but I know damn well that I will pick the two worst days to do it so I don’t even dare attempt it haha… As long as I get decent returns I’m fine – I don’t need to make a killing. (or lose a killing!)

I have to confess, I have been nervous about the market as well. Glad I’m not the only one.

For years I’ve been very aggressive in the stock market. I.E. 90%+ of my holdings were equities (in index mutual funds for the most part).

But I’ve been concerned about where the market is heading. And keeping in mind that I am hoping to retire in about 5-8 years, I have been incrementally reducing my market exposure. But you don’t have to pull completely out of the market.

Since the election last Nov, I haven’t invested any of my deposits I’ve been setting aside in my retirement accounts. This isn’t a huge deal as I carried very small cash balances before. Even now that accounts for less that $25K (less than 5% of my total).

My investment allocation at the beginning of this year:

65% S&P – 25%Russel 2500 – 10% Vanguard Bond Agreggate

July:

65% S&P – 35%Bond (got out of the Russel 2500 because while it goes up more when the market is rising, it also has more volatility and can drop worse when the market goes down)

October:

50%S&P – 50%Bond

While not getting out of the market completely, I feel the need to protect some of the last few years of market increases before the market drops.

I am somewhat conflicted about this. I KNOW that attempting to time the market is a fool’s errand. But with my time horizon for retirement under 10 years I just can’t stay so highly invested in equities.

Additionally, if the market does drop and I not only avoid the loss on half of my holdings, but shift back into equities afterwards, I may even be able to retire a couple of years earlier.

Oh man, I don’t blame you. It’s easy for people like us to say to stay in with decades still left in the game, but if retirement was right around the corner i’m not sure what I would do either! I’d like to think i’d have the balls to ride it out, but would I really?

Just came across this post a few hours ago – pretty close to what you’re talking about here and I bet it helps you!

http://awealthofcommonsense.com/2017/11/considerations-for-cashing-out-of-the-stock-market/

Nicely done man! I agree there will be a correction but it could be tomorrow or in 5 years or 10 years…

We have got to get a picture of the taped up Lexus.

I’ll try and remember it for the next round up :) Though it’ll look exactly how it sounds! Haha…

Nice update! And congrats on the steady progress.

It takes a while to get going, but then you’ll continue to ride your momentum forward.

On your question about anything new or juicy, my wife and I just decided to reduce our retirement contributions for the next 4-6 months. (I smacked myself on the back of the head a few times even initially contemplating this…). Overall, we realized we needed to focus on something before now (we’re both 33) and 25+ years away from “traditional” retirement age. More to come shortly.

Thanks again for the ongoing posts!

– BD Mike

Well dang – way to leave us hanging! Haha… what did you invest the money in now?? Gold? Real estate? Rare monkey breeds? :)

Awesome 5 figure update! I know what you mean by waiting for the markets to crash already- every “little dip” that comes I’m like- is this it?! Am I ready! But then the markets keep going up… Mr Market is being such a tease right now. 20+% YTD for S&P500, crazy sauce!

Just 15 months ago I was multiple thousands in the negative. At the end of October, my net worth is just under $20k on the positive side now. Wahoo! The first 100k is the hardest they say.

BOOM!! And I bet a lot of that was from your own doing vs the stock market, yeah? That’s exactly why that first $100k is the hardest – takes the most level of effort until you have enough for your worker bee dollars to take it from there!

You’re killing it man. I’m nervous about the market to be we all know it’s fruitless to try to predict and fruitless to be worried about things you can’t control. Slow and steady man, and you keep chuggin along

Nice increase! I’m up almost $9,100 myself for October, a mix of the market and a big chunk of debt reduction.

Oh, and I drive a Toyota, too! #98Camry

YES!! Have you seen this car ad that went viral yet?

This dude made a video of his girlfriend’s ’96 Accord she has up for sale and it’s gotten over 4 million views on youtube haha.. (and also messed up the ebay listing so they had to re-list it because people kept jacking up the purchase price too much :))

But this is pretty much you in that Camry!

https://www.youtube.com/watch?v=4KlNeiY4Rf4

Whenever it happens, this will be my first crash with skin in the investment game. I’m hoping that I’ll have the blasee attitude and approach you’ve mastered.