That was the subject line of a new email I just got ;)

For anyone unfamiliar with the “club”, it was a silly little thing I put together in year #1 of the blog to get people excited – and motivated – about hitting a million dollars, and in order to be added to it you had to share your list of things you’re planning to do to reach it.

#156 on the list was Gene Roberts who had pledged the following on May 20, 2015:

My current projections have me at $1,000,000 of retirement assets at age 52.2 (1/1/2023). Current retirement savings: $388K

Actual net worth of $1 mil with my equity should occur around mid-2021. We’ll see if the markets cooperate. Current net worth: $576K

Here’s what I’ll do to achieve my financial freedom:

– Max out Roth IRA (contributions are good source of emergency fund if needed).

– Max out my Health Savings Account (tax-free triple threat!).

– Save about 21.3% of my gross income towards retirement (includes employer contributions and Roth and HSA above). I invest the remainder in a brokerage account.

– I have switched the amount I was paying ahead on my mortgage and have it going into my brokerage account as well. In the long run this should gain me about $30-40K over paying the mortgage off early.

Pretty solid list, eh?

And then here’s his latest update as of this morning – along with that pretty little graph featured up top again:

Hey J$,

I did a little mid-month NW update.

New high needed another comma, finally. :)

So for at least 1 day I’m a millionaire.

I know it is just a number, but it is sure nice seeing that added digit.

Now if I can just double that retirement balance number, I’ll be golden.

Gene Roberts

*******

Woohoo! Way to go man! The power of The Club right there ;) $576k net worth 4 1/2 years ago, and now essentially doubled with plenty of opportunities to keep growing…

Always cool seeing these updates and what PERSISTENCE gets you over time. Saw this quote online the other day and it couldn’t be truer:

“Never give up on a dream just because of the time it will take to accomplish it. The time will pass anyway.” – Earl Nightingale

The time will pass anyway. Damnnnnn….. Nothing anyone can do to stop it either! So you might as well go All In on yourself!

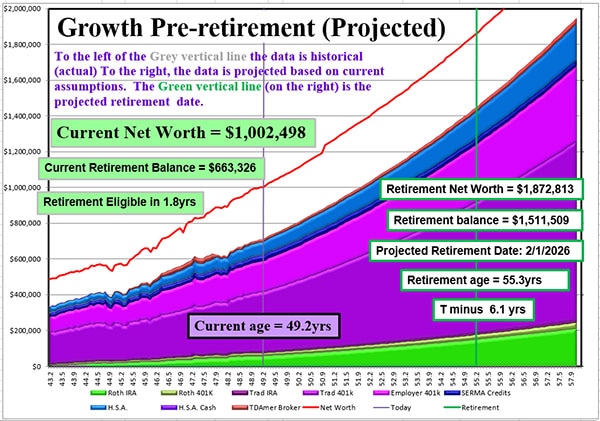

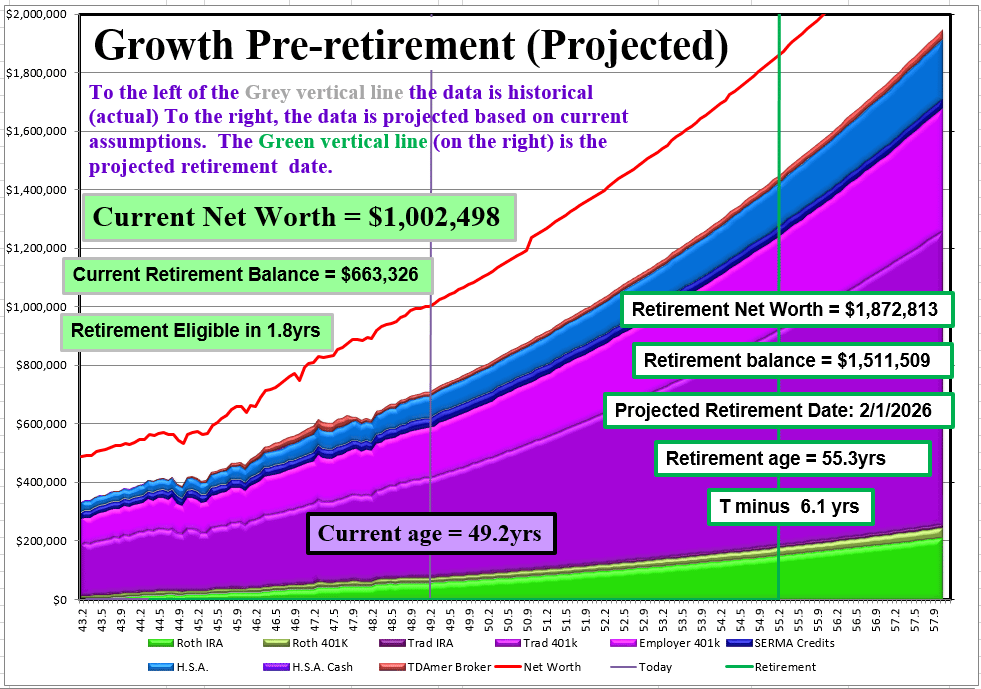

Asked Gene here if he could explain the graph a little, and what the rest of his net worth looks like as well as how he calculates his “number”, and here’s what he passed back.

(Along with a MONSTER of a spreadsheet that I’ll also attach here for anyone interested in downloading/playing around with :))

In addition to the solid-colored parts labeled at the bottom of the chart (what I consider to be my “retirement” accounts), the NW red line includes: home equity, vehicles, checking and savings accounts, and a couple of accounts (money market and additional broker account) that I have earmarked towards paying off the remainder of my mortgage, ideally after they accumulate more (current mortgage is a 15yr fixed at 2.875%).

My “number” is pretty straight forward. I take my budget and pad it generously (like $1,200/month) for discretionary spending. That gives me a built-in ability to immediately cut 25% off my budget with no impact to my non-discretionary bills if the market goes down. This is one of two counter-measures I’m planning to address sequence-of-return risk. Then I apply the 25X (4% rule). That puts me in the vicinity of needing $1,250,000 in non-medical retirement accounts to be confident that my investments will out-live me no matter how long I can hang on.

Of course the 4% rule is just a guideline. It still has to survive my projection assumptions for drawdown. I’ve also run my plan through the Firecalc simulator where it gets about a 90 – 95% success rate.

*******

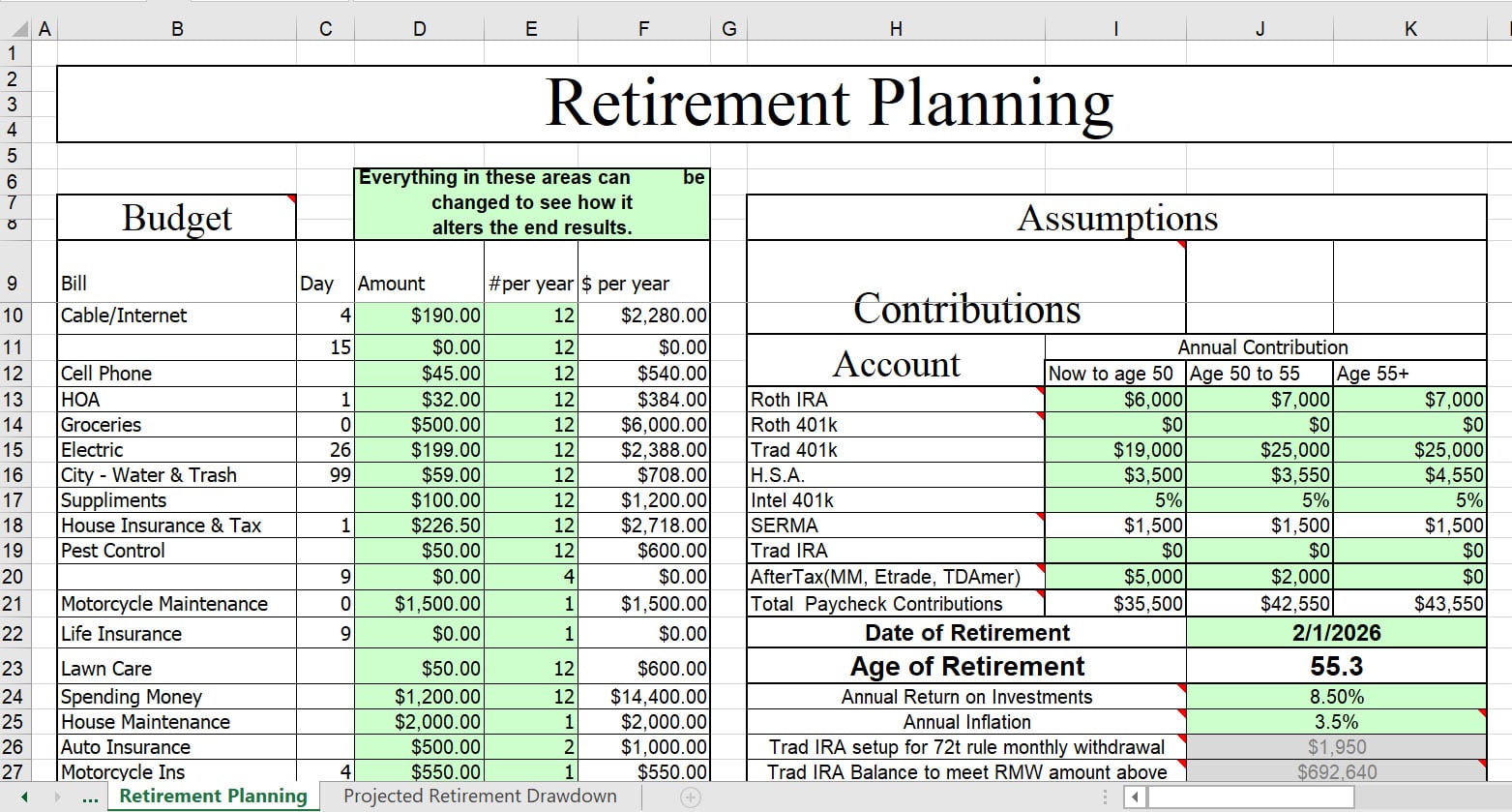

His Monster Retirement Spreadsheet:

You can’t see all the sections here as it would take over your ENTIRE COMPUTER screen, but you can download and check it out here (which includes graphs!) –> Monster Retirement Spreadsheet

Here’s a list of all the sections:

- Budget

- Assumptions

- Projected – and Actual – Retirement Balances

- Non-Retirement Net Worth Accounts

- Credit Score tracking (of *six* reporting agencies)

- Net Worth minus The House

- Date and Age of Retirement

- Date and Ages money will run out

- Projected Growth Graph

- Retirement Drawdown Graph

- Total Monthly Expenses Graph

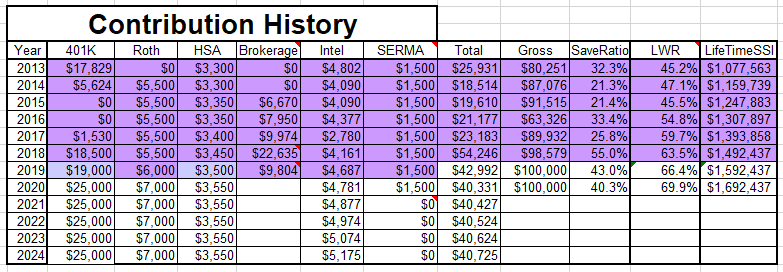

- Social Security Records (SSI Earnings / Med Earnings)

- Contribution History

- Projected Retirement Drawdown covering over a dozen accounts (!)

It’s pretty hardcore :)

Here are my two favorite parts of the spreadsheet (and anyone’s money for that matter!).

*******

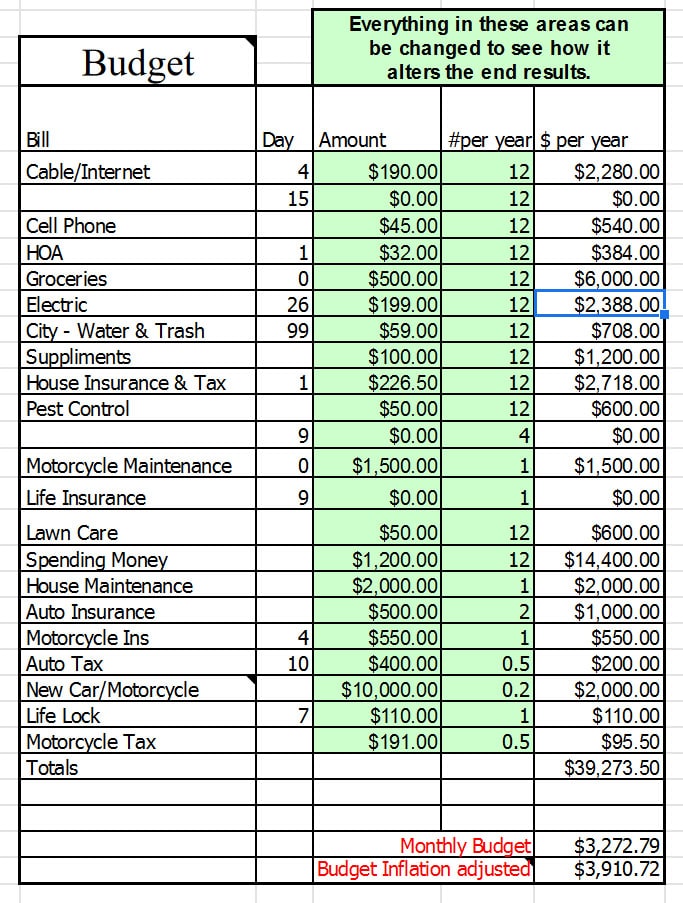

Gene’s Monthly Budget:

Love the “day” and “#per year” columns. Two parts that are often overlooked in budgets but are super helpful to know! Wouldn’t have thought to separate out the #per year category as I tend to just multiply or divide them appropriately in the main $$$ column which tends to confuse anyone who looks at it – i.e. my wife, and occasionally even me ;)

*******

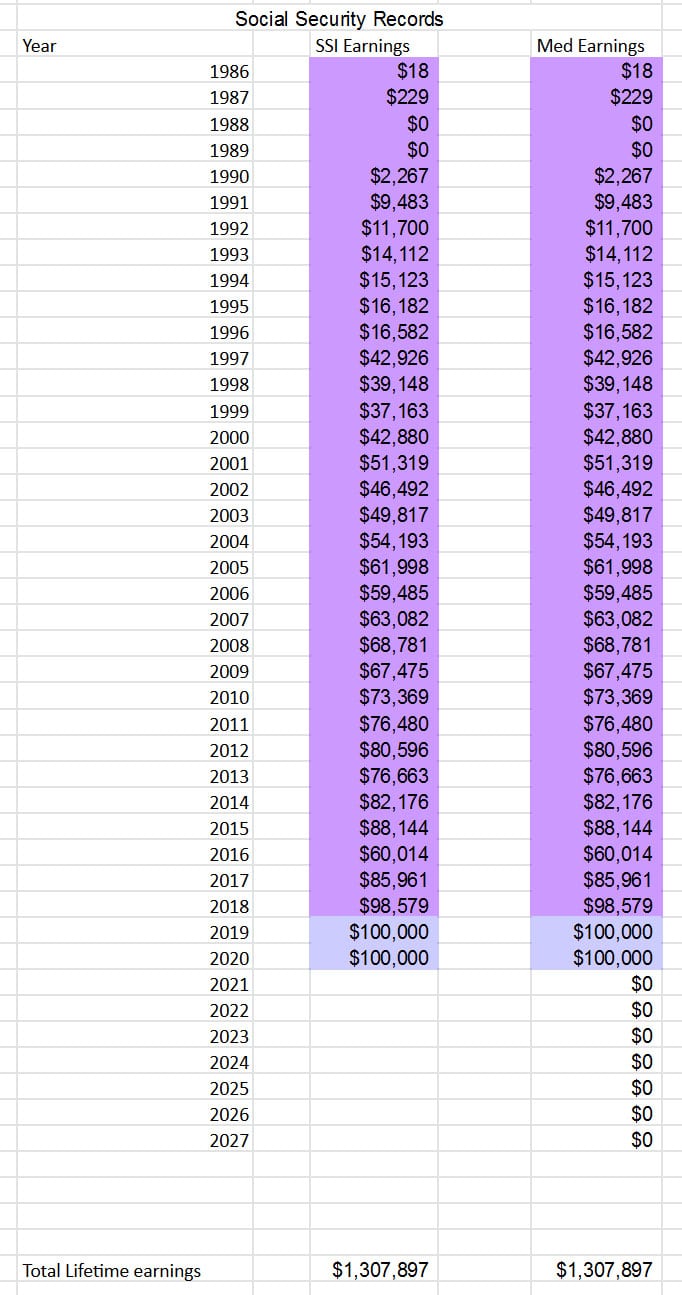

Gene’s Lifetime Earnings Report:

These are just fun to see overall :) And anyone can download these #’s super easily if you live in the U.S. by just going to the my Social Security portal.

(And then if you REALLY want to get nerdy with it – take it a step further and divide your *net worth* by your total lifetime earnings to get your Lifetime Wealth Ratio and see just how much of it you’ve saved over the years! It’s pretty wild!)

UPDATE: Didn’t catch that Gene tracks his LWR here too! The guy doesn’t miss a thing! (Second column from the right)

Main takeaway today: keep focusing day in and day out and eventually you’ll hit your Big Goals too! Use time to your advantage as it’ll continue to pass with or without you… :)

Big congrats again to Gene for hitting his epic milestone here, as well as always being so kind in allowing me to share his life on the blog as it’s always so helpful to see other perspectives. If you like his style, you might be interested in a few of the guest posts he’s written for us over the years:

- Zen and the Art of Couples Budgeting

- Why Work So Hard Building a Fortune and Not Protect It?

- Dream As If You’ll Live Forever, Live As If You’ll Die Today.

Happy Budgeting!

Get blog posts automatically emailed to you!

I don’t comment often, but this post is awesome.

Way to go Gene and I LOVE the spreadsheet.

Thank you.

It’s been a labor of love as I keep finding more functions I want it to perform.

I’m pretty sure it won’t be “done” until I am. :)

Damn Gene, you nerd. I love it. Great job on the spreadsheet. That is impressive. Very similar to my retirement. Hope you don’t mind if I use and plug some of my numbers in and see how I am tracking?

thank you.

You’re more than welcome to “appropriate” any portions that you think might help you.

Be careful if you set the retirement date prior to 55 years old though, there’s a circular reference I haven’t fixed yet for the 72t rule in the drawdown sheet.

I may not fix it since I don’t think I will have enough to retire comfortably much before I’m 55 anyway.

Excellent post with plenty of detail that needs further study. The one thing that I never really kept a formal spreadsheet on was my monthly/annual contributions that were put into 401ks, Roths, and IRAs. I maxed them out year after year. The problem is the max changed over the years. After 30+ years, I actually don’t have the exact figure of my total contributions, only the current balances. After this post, it’s going to bother me until I find a way to easily backtrack to get that figure.

Hah! Sounds like an excellent project to tackle over the holiday season :)

I started tracking my Roth IRA contributions initially just so I knew what I could take out without penalty in case I needed my “emergency fund”.

Fortunately (or unfortunately depending on how you look at it), I wasn’t as far along in my savings as you when I started tracking my NW and could figure out my contributions.

I track all my contributions now just to get a read on my total savings rate.

I kind of wish I had tracked my net worth all those early years. I’m slightly early retired and in awesome shape now but I never tracked it until Personal Capital came out a few years ago. I wasn’t interested in retiring super early so it didn’t really matter. I knew we were saving much more aggressively than most but I also planned on working until I was 70, like most of the older guys at my corporation who also enjoyed their jobs. In my fifties, the first time I checked my net worth and found out we were millionaires it was a shock, a good one but still a surprise because we had about eight different accounts and except for the 401K none of them was impressively large. I have to admit my tolerance for the negative aspects of work went way down once I realized I didn’t need to be there for financial reasons. Maybe it is good I didn’t know?

I would say so, haha… Most people get a surprise in the OTHER direction! :)

You’re probably right. I know that once I solidly meet my “number”, my tolerance for the day-to-day hassles of the corporate world will become much easier to walk away from. :)

Wow Gene, this is amazing. I love the level of detail, thank you for sharing it with all of us. I love how you also got to 1 million so much earlier than expected! Fingers crossed it’ll happen to me, too. It’s all about discipline!

We want an email once YOU cross it too, please! :)

Awesome post and spreadsheet! Love me some spreadsheets…

That quote gave me goosebumps, bout to print it out and post it on my wall at work.

Happy Holidays!

BOOM!!