My friend Christine just reached a pretty huge financial milestone… She and her husband have paid off their mortgage and now own their home free and clear! Woohoo!

This is a life goal many of us strive for, so you’d think everyone would be helping her celebrate. But instead, she’s been receiving some interesting and discouraging feedback! Here’s her story …

*****

My husband and I just paid off our mortgage, 13 years ahead of schedule! Pretty awesome, right? I thought so, too, except that one my subscribers disagreed with me. He replied to my celebration email by saying:

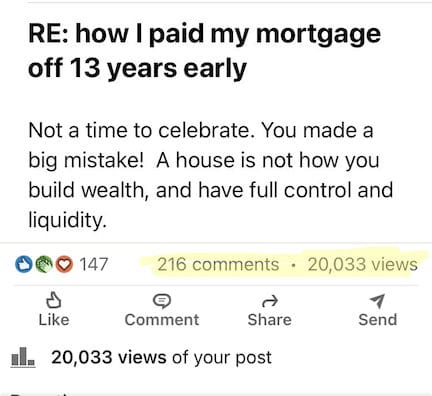

“Not a time to celebrate! You made a big mistake! A house is not how you build wealth, and have full control and liquidity.”

First off, I have no idea who this person is or his level of financial expertise. He could be a garbage man, a middle manager, or a financial advisor! Second, this man knows nothing about my personal finances other than the fact that I just paid off my mortgage early. Third and finally, many financial experts agree that homeownership is still one of the best ways to build wealth for American families.

I hate to admit it, but I really wanted to send him a scathing reply for raining on my celebration parade. But I decided to do something better. I turned it into a social media post that went viral on LinkedIn! I’m still getting comments a week later, and it’s racked up over 20k views!

… But it got me thinking, are there times when you shouldn’t pay off your house early?

When it Might be a Mistake to Pay Off Your Mortgage Early

You Have No Savings:

If your saving account has tumbleweeds blowing through it, then it might be a mistake to pay off your mortgage early. Why? If you have an emergency like a job layoff, major car repair, or big medical bill, you won’t have cash on hand to cover it. And that usually means you’ll be charging it on a credit card.

I like to see my coaching clients accumulate at least six months of their monthly living expenses in liquid savings before paying extra on their home. Plus, your savings will help cover large home maintenance items like a new roof or AC unit.

When You Have High Interest Debt:

My mortgage interest rate racked in at 4.125%. Thankfully, when my hubby and I use credit cards, we pay them off in full every month. What if you’re carrying balances on credit cards with 14% or higher interest rates? Then it would be a mistake to pay off your mortgage before concentrating on your credit card debt.

I typically advise my coaching clients to pay off debts in this order: credit cards, personal loans, student loans, car loans, home equity loans, then mortgages. It just makes sense mathematically to knock out the higher interest debts first because you’re saving more money. Sometimes we’ll do things out of order if it makes sense for cash flow purposes, but 99% of the time, I recommend paying off credit card debt FIRST before paying extra on the mortgage.

When You’re Behind on Retirement:

If your financial planner has cautioned that you’re behind on retirement, you’re going to want to think twice about paying extra on your mortgage, at least for now. One of your biggest assets in saving for retirement is time. The sooner you get started, the better.

The compounding effect of interest and reinvested dividends was dubbed by Einstein as the 8th wonder of the world. Basically, your money is making more money for you, multiplying like frisky little rabbits. Additionally, your retirement accounts are tax-favored, whether you’re investing your money pre-tax (traditional plan) or growing tax free (Roth plan). Tax-favored accounts are a bonus on top of the investment growth.

If you’re behind on saving for your retirement, do that first before paying extra on the mortgage. But I will say this: It’s my goal for all of my clients to be mortgage-free by retirement.

Paying off our mortgage early made sense for us!

In our situation, my husband and I have more than six months of our household expenses in savings, have no other debt, and are ahead of schedule with our retirement investments. So, my “hater” was wrong! This is a time to celebrate, and paying off our mortgage was the right move for us.

What do you think? Is there another scenario where it might be a mistake to pay off your mortgage early?

*****

J Money wrote a post many years ago that has always stuck with me… My Answer To All Financial Debates.

Basically, he explains while there will always be a financially “correct” answer to money decisions, sometimes we get a way bigger feeling of accomplishment doing something different. You can’t really fault someone for making progress toward the things that excite them in life. My 2 cents!

Have a great weekend, y’all!

– Joel 🏄♂️

Get blog posts automatically emailed to you!

Awesome post Joel and Christine!

I’ve been wondering whether I should be paying off my mortgage early as well. It’s certainly a question that has stuck with me for a while now, and I think that J Money and Joel certainly hit an important point: paying off your mortgage certainly can be emotionally rewarding and satisfying. I honestly don’t think I’m there just yet when it comes to paying off my mortgage – I’m ok with keeping my monthly payment (especially because I was able to refi my home to 3% recently). However, I know a few people whose ultimate goal was living without a mortgage payment – it gave them peace of mind, and I think if you’re that type of person, it’s absolutely ok to pay off your mortgage early.

Great discussion points!

Cheers and have a great weekend –

Fiona

A 3% re-fi is pretty amazing! I can see why you wouldn’t be super rushed to pay it off.

It’s so funny how much hate we get on finance blogs…. so many problems in this world, but you chose to focus on ripping on someone for paying off debt??? lol… I will say they do make things interesting though :) I still die every time I see this note someone once sent me: ““He says really nice things but looks like a weirdo. But I guess that’s why people like him. He’s like the Miley Cyrus of Finance.””

(And btw – I STILL use that *excited* mantra to this day!! One of my biggest epiphanies!!)

Lol, I know, right J? But hey, I don’t just turn lemons into lemonade, I open up a lemonade stand! His nasty comment got me a viral LinkedIn post AND a guest blogging opportunity!

P.S. The Miley Cyrus of Finance, omg!! Hilarious!

I paid off my mortgage early, and it has been a huge relief. On top of all the other COVID-related financial worries, I’m lucky enough not to have to scrape together a monthly payment that is (approximately) 30% principal and 70% interest. There are still a lot of concerns, but foreclosure isn’t one of them.

I bet that is a big relief, Nora!

We just paid ours off early also and are in a similar situation. We both work in the same industry and that can be high risk. Thanks for writing this post!

I totally understand that! My husband and I worked for the same company for a while and it can be risky having all of your income eggs in one basket. Congrats to you on paying your mortgage off early!

We did a 20 year mortgage and have every intention of paying it off before then. No other debt, on track for retirement, putting money in a 529 for the kids, etc. I’ve always valued the peace of mind that will come from truly owning our house and, in the end, it’s another asset. I know we can get a better return on the market, but like I said…were in track and I think there is a lot to be said for security of owning a home for many reasons.

I don’t begrudge others who feel differently but this certainly seems to be the one of the financial decisions that people get pretty passionate about. I just prefer owning the house as early as possible and using that extra money to invest at that point. If you’re already on track, the rest is gravy!

Yes, there’s definitely something to be said about what financial peace of mind is worth to you, Eric. All debt carries a financial and emotional weight to it. If it stresses you out, it’s best to get rid of it!

Great topic to address!

Honestly, I don’t think there’s a right or wrong answer. It’s different for everyone. What may work for one person may not work for another. It really depends on one’s financial situation. And comfort level.

I have a friend who paid off her mortgage early (15 years). Though, she told me money was really tight during that time for her and her family. They gave up a lot in terms of experiences and time in order to save money to put towards the mortgage.

Some people would be uncomfortable with that situation. But, it worked for them.

For me personally, I’m comfortable with having another source of income pay for my mortgage. Yes, it would be nice to pay it off completely which I’ve thought about. Though, it can definitely be a lifestyle choice. Ideally, you’d want both. But not everyone can have that.

I enjoyed the write-up. Thanks for sharing!

There’s definitely a balance to it! We will be splurging more on travel (hopefully soon), now that we don’t have that payment.

If your mortgage is in the 3% range then there is no point to pay it off early. Why put an extra $5k into paying off your 3% mortgage when you can invest that same $5k for a much higher return. Of course there is risk but you can get some pretty low risk bonds that pay more than 3%.

And of course you can always access that money if an emergency arises. Meanwhile its tough to pull equity out of a home, especially when dealing with financial issues.

I paid off my mortgage at a time when I had higher-interest debt and not a whole lot in emergency funds. But I was single and really afraid that one serious emergency would cause me to lose my house. Although I knew it was not financially smart, the sense of security this gave me was priceless.

“Good decisions aren’t always rational. At some point, you have to choose between being happy or being ‘right.’” Great to hear you chose happiness, I would do the same thing to sleep better at night!

Love this blog post. It’s always a polarizing topic in the personal finance world. It’s a shame Christine received this response, given the commenter doesn’t know her full financial situation.

This is actually a topic my wife and I have battled before. It comes down to 2 things for us, priorities and financial planning. We’ve decided to make it a priority to be debt free as soon as possible. We hate debt and the lack of financial freedom (monthly payment, ugh!) associated with it. We’ve also made it a priority to execute proper financial planning for the long-term that will set us up for a successful and rewarding retirement. Without this planning, we would not be in a position (nor would we feel comfortable) to pay off our mortgage early. It’s important to note we’re planning to each retire around age 55, so we’re not on an extreme “FIRE” plan which I understand makes our situation different than most people reading this.

However, not all decisions we make are “final” per se. We’ve learned that when situations (life, economic, etc.) change, that we must re-evaluate and take action. For example, when the pandemic began in March 2020 and the stock market plunged we decided to stop our additional principal payment on our mortgage and to invest (buy-low) in the market. We did this for 10months and put the money in a separate brokerage account. Our plan is to let this money grow over the course of our remaining mortgage and to make a large “pay-off” with these funds once the funds grow to where they match our remaining mortgage balance. I can’t tell you how excited we’ll be to make that final payment!

AWESOME move buying low last year! I agree that plans can change and adjusting on the fly can pay off big time.

Also glad to hear you and your wife have regular communication and are on the same page about it all. That foundation is needed first before making swift changes.

Congrats again!

We paid off our house in 10 years on a 30 yr loan and that was 12 years ago. Not paying a bank interest on money that I didn’t need to borrow anymore has been great the past 12 years. I understand the compounding if I had invested the extra payments instead of paying the loan. We chose to pay off the loan per our financial decision.

I guess we shoulda bought a vacation home and bought a boat with a new truck for towing instead of paying extra to the home loan. Then we can go into further debt. Isn’t that the American Way? Ha ha.

We all make choices and do what is best for our situation. Kudos to paying off home loans and kudos to those who invest the extra payments instead of paying off home loan.

It’s not too late to correct your mistake from 12 years ago… If you refinance your home right now, you’d probably have enough to buy TWO boats! ;)

I think a lot depends on age, as well. If you’re young and will have your mortgage paid off well before retirement, invest aggressively and carry the mortgage if you don’t have enough to pay it off early. If you’re closing in on retirement, make every effort to have that mortgage paid off before retirement. Being mortgage-free during retirement equals a much smaller withdrawal rate from the retirement funds you spent your younger years (hopefully) growing aggressively.

Agreed. The longer the time horizon, the more it makes sense to invest excess cash elsewhere.

I say congrats on your accomplishment! If that is what you wanted to do as a goal then you should be happy. Why people want to burst others bubble is beyond me.

We will own our home a few years before retirement and I look forward to it! Our cars will also be new and paid for. Goals to have so that you enjoy retirement your way :)

Wow….perhaps some are jealous that you CAN pay off your mortgage. We paid off our mortgage and worked like crazy to cut 16 years off the loan. We saved over $280K in interest that is in our pockets, not the banks. That isn’t a bad thing. The new tax laws meant that we were getting no tax benefit from paying interest either. To all those that think having debt is good, go for it! Borrow, borrow, borrow. Keep banks in business. The rest of us will be just fine.

$280k saved is no joke!! Congrats!

We paid ours off in 5 years and would do it again in a heartbeat. One less (big) thing to think about. Taken to their conclusion all these money gamers should never be more than a couple years into a mortgage before refinancing to pull the money out and invest. That would make their spreadsheet spit out the biggest number…

But we’re also super lucky and privileged to have bought at the bottom, be ahead on retirement, and certainly have no other debts. Love it!

One of my friends has been refinancing every year the past couple years. (I actually think they’re losing money on the closing costs, just to shave a tiny % off their rate and lower their payments.) Makes me cringe.

Congrats on your progress Alex and being debt free! Have a great weekend!

In general, I feel like if you are almost done, pay it off. But with a low interest rate, there is no point in paying it off early if you miss the opportunity cost of the cash being in the stock market, your business, or other investments that make more. There is more risk though.

A math-based case for paying off your mortgage early when pursuing FIRE via the 4% rule:

Case study: Someone has a mortgage at 3% interest amortized over 30 years. They are considering using their monthly cash surplus to : 1) Pay off the mortgage early, or 2) Invest in a low cost index fund. What should they do?

This is actually a trick question. You are missing a piece of information, and you can’t answer the question without it. What you need to know is: What is the goal, the highest net worth possible, or FIRE as EARLY as possible?

Most people would simply compare the interest rate of the loan with the expected return of the index fund, or perhaps with the 4% rule. I.e. if you think the index fund might average 7% over the long run, or that you can reliably count on withdrawing 4%, then paying off a 3% interest loan does not make sense.

If the goal is to maximize NET WORTH over the long run, then the previous conclusion is correct.

HOWEVER, If the goal is to reach financial independence AS EARLY AS POSSIBLE, you are looking at the math incorrectly. What you should be looking at instead of the loan interest rate is the MORTGAGE CONSTANT compared to the 4% rule. This is simply your loan payment (P + I) divided by your loan amount. For a 3% 30 year loan the mortgage constant is 5.8%. This means that for every $100,000 of loan you will have a payment of $5,800 per year.

According to the 4% rule (of thumb) you are FI when your invested net worth reaches 25x your annual spending. If you keep the mortgage, this means you will need to save an extra $145,000 ($5,800 x 25) to make the loan payment on every $100,000 of borrowed money!

This effect gets exaggerated even further as you pay the loan down (same payment on a lower amount owed), but let’s ignore that for now.

On a $300,000 loan, you need to save an extra $135,000 to cover the payment with the 4% rule vs. just paying the loan off. If you are saving/earning $45,000 per year, paying off the mortgage will get you to FI 3 YEARS EARLIER than keeping the mortgage and sticking the money in an index fund.

I don’t know about you, but I value my TIME more than my net worth. If given the choice between only index fund investing, or index investing AND paying off the mortgage, I’d pay that sucker off.

Cheers!

I’ve been waiting for years for a blog post as great as this on the topic of “when it makes sense OR NOT to pay off your mortgage early”.

Thanks for posting this! We are in a very similar situation to the author. We have about $ 30,000 left in our mortgage (home value is $ 300,000) and are ahead on all of our other goals – retirement, emergency savings, college savings for kids.

The way I look at it is you have to be both offensive (saving a lot) and defensive (minimize your debt an monthly expenses too) with your finances. If you save a lot and have $$$ that is great, but you also should have low monthly expenses.

Like the author of this article my wife and I hope to have our house paid off in the next couple of years, and that gives us more defense if I am laid off of my job, or some other “emergency” occurs. It is nice to know in the event of an “emergency” that you have a paid off place to live. The author of this article was great to explain that paying off your mortgage does not always make sense, but if you are ahead on your other goals….. why not??

Personal finance is just that personal. There’s some people that finance rental property after rental property and as soon as they loose their jobs they loose everything. Owning your house gives you comfort in knowing it’s yours and you can get by at any old job to eat and make sure the taxes are paid. Who cares what others think!

Great post!

We paid off our mortgage seven years ago and have never looked back. It was an unbelievable feeling when we got the release of lien from the bank. I should have framed it ;-)

You might be tempted to take out another mortgage at some point after paying it off, but we have resisted that idea and instead set aside the money we were paying for the mortgage in a savings account. We use the cash to pay for repairs and other expenses. This means we don’t have to put emergency expenses on a credit card, which is great!

– Mark

Congrats!!! My friends framed their title paperwork after paying off the bank. Such a great feeling!

I personally love the peace of mind having a paid off house gives me. If I got in a serious car wreck or suffered a serious illness I would not have to worry about losing my place to live. Here is a question: If you had a paid off house would you take out a mortgage on it to put in the stock market? HELL NO!!! Paying off your house early is not a math problem, it’s security and freedom.

Love this perspective Elizabeth!!

There is an opportunity cost with all debt versus investing the surplus cash, but debt often carries with it such emotional and personal baggage that I don’t think you can necessarily always look at it that way. I personally have avoided debt by paying for a car in cash and aggressively paying off student loans, which as compared to market returns has proved not to be the optimal decision.

Yeah it’s funny how people’s opinions of debt change depending on the asset you borrow against. One of my family members took out a 0% car loan, which people would advise to pay off ASAP, even though the debt isn’t really costing anything.

I love the peace of mind of having my house paid off. I hate debt. When I was a teenager, my Dad suggested I could pay out my car repair expenses, as I went to the same shop that he did. I just couldn’t do it, since I had the money and couldn’t handle having that hang over my head. My husband and I paid both our first home and our current home, off early. The first one was a very low price and was owner financed and the owner told us if we paid it off early, he would take some off the principal. However, on our current home, I was working at a high stress job and wanted to quit working. I worked aggressively on paying off the house and not shortly thereafter I was able to quit working. I currently have a very part-time job working at home.

I believe there is debate in this space because there are those who want to treat the decision as either purely mathematical or emotionally. But as many above have commented, the variables needed to make the decision are far messier. I have had to deal with my own version of the author’s critic (I’m not convinced it isn’t the same person! lol). In my opinion, the failing of the pure math argument is that it does not overlay Risk Analysis and Maslow’s Needs Hierarchy on top of the financial math. So long as the real return of your investments remains above your interest rate, you are in the money. But shelter, food, and water are the large base of the Needs Hierarchy for a reason. Depending on your specific risks, it might not be wise to rely on the ability to liquidate investments if you suddenly find yourself jobless, hospitalized, or disabled. In my experience, all of those conditions tend to converge at once. You are more likely to lose your job during a recession and the stock market is often not performing that well during such a time period. Then you lock in losses in principle as well as incurring enough fees and penalties that could bring your real rate of return to at or even below your home interest rate. Because let’s face it, you’re probably going to pull from tax deferred accounts prior to retirement years since those were the most efficient to be contributing large amounts of money to in the first place. That combination is especially familiar for those who went through the Great Recession during their working years. I believe the author’s questionnaire above for conditions that you might want to meet prior to deciding to pursue early home payoff are highly valuable, since I wouldn’t ever advise anyone to focus so intently on one leg of financial stability that they ignore all the others completely. There is an additional one that I would like to add, however. I don’t want to get too much into it, but I believe there will be many who can relate to it. In addition to meeting the above criteria, are you concerned that an existing or highly likely to exist medical, genetic, or mental condition could flare up as a result of an external trigger and endanger having a roof over your head for either yourself or your loved one(s)? There are deeply personal risks within the answer to that question that can, and in many case absolutely should, override the opportunity cost of investing vs securing a shelter. And for a subset of us, that answer could be the difference between feeling safe enough to seek help/leave a situation or allowing the circumstances to escalate and end us. Whatever your decision, your choice is valid.

Huge Congrats Christine on paying off your mortgage early.

I paid my final mortgage payment in 2019 and it’s a wonderful feeling. When I bought my house, I was 31 years old and I didn’t want to be paying on it until age 61. I wanted to pay it off in 21 years, but it took me 23. I’m not missing that payment one bit.

With 3% mortgages, this may not seem to make sense, but I wanted the freedom to save more or retire early and now I have it. Money creates freedom and so does lack of debt.

Freedom > money! That’s awesome Bret, congrats!

Thanks Bret! I’m so happy to join you in the mortgage-free club! You are so right about lack of debt giving you more freedom and options.

We paid off our home recently, too! I enjoyed this post immensely because it made me feel even more assured we did the best thing for our financial future. We use the $ which would be going to the mortgage towards investments, and all of that is helping to grow our wealth. Thank you for sharing!

Congrats!!!!

That’s so awesome Annie! Congrats!!