Happy July!!!

Ready for a new month and new goals??! Got your net worth all tracked up and ready to motivate the pants off you??

If you’re still invested in the market it should help after last month’s blood bath :) Down $40,000 for us, and now back up $35,000 just weeks later! Thank goodness we ignore the hype!

Outside of that, nothing too exciting going on over here… Although there was that one time when I realized I’d been forgetting to set aside tax money for the past three months and had a nice surprise when I went to go pay our quarterly taxes, haha…. Nothing like logging into your account expecting to see thousands and instead find cobwebs up in there! ;)

We also started making extra payments on our mortgage, but not sure if I’d exactly categorize that as “exciting,” haha… More on that below…

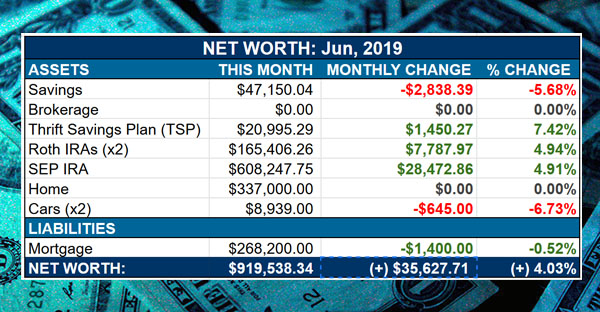

June’s Net Worth Breakdown:

[This is part #137 of our Net Worth Series, where we share our real life #’s every month in hopes it motivates YOU to track yours as well – no matter how scary or awesome it gets. And in case this is the first time you’re seeing these – it definitely gets scary up in here ;)]

CASH SAVINGS: $47,150.04 (-$2,838.39) — Another month of losses for us here! Though technically we actually *earned more* than we spent, but then of course had to rectify that tax deal which certainly didn’t help any… As well as the extra payments towards the mortgage. Still, at the end of the day the net effect was a loss, womp womp…

BROKERAGE: $0.00 (n/a) — Nothing new here, I just like seeing the stark difference compared to yesteryear’s $50,000 before picking up the house ;) You have to force yourself to feel the sting sometimes so it sinks in more!

THRIFT SAVINGS PLAN (TSP): $20,995.29 (+$1,450.27) — BOOM! A nice increase on top of an nice automated contribution from my wife each and every paycheck… It was just a few years ago when it was at $0.00!

ROTH IRAs: $165,406.26 (+$7,787.97) — Double BOOM! And without lifting a finger, at that :) The power of compound investing at its finest…

SEP IRA: $608,247.75 (+$28,472.86) — Quadruple BOOM! (It gets to skip Triple BOOM since it’s such a leap in growth ;)) And again, nothing new added here while the market just does its thing… (though of course it’s been on a helluva temper tantrum these past few months!)

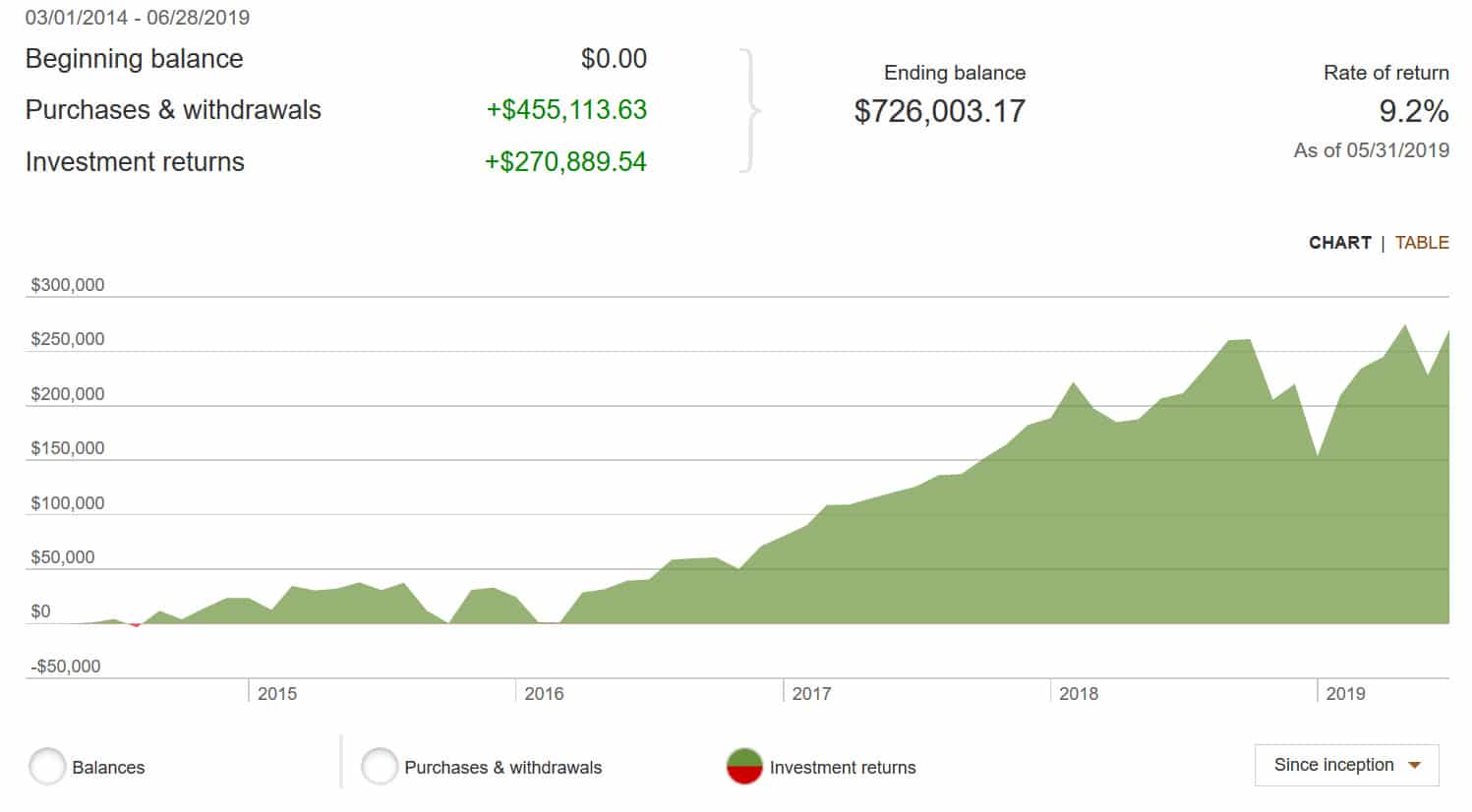

Here’s an updated snapshot of our investments over at Vanguard:

(All our money here is in VTSAX after realizing it was the perfect strategy for us some 5 years ago…)

HOME VALUE: $337,000.00 (n/a) — This will remain flat for the next half a year or so until we re-evaluate it with our realtor which we find to be a more pleasant (and accurate) experience than tracking the Zillows et al ;) We did this with our first house we owned, and the valuation at the end came within a thousand dollars, I want to say, of the final sales price. So I highly recommend this route!

CAR VALUES: $8,939.00 (-$645.00) — Finally making up for all those *increases* the past two months! Haha… Either that or I clicked the wrong button this time, but my money is on the updated algorithm (or I should say, my money is LOST on the updated algorithm!)

Here’s what both are worth according to KBB.com:

- 2008 Lexus RX350: $6,777.00 (-$241.00)

- 2005 Toyota Corolla: $2,162.00 (-$404.00)

MORTGAGE: $268,200.00 (-$1,400.00) — There we go!!! Daddy’s not playing around! Haha… It still kills me a little that we’re paying the higher interest at the 30 year level vs the 15, but as you can see we’re still set on paying it off as early as possible ;) And just an FYI that these #’s here are estimated as I’m still waiting for online access to our account since having our loan servicer changed out (they already “sold” our loan within days of closing!! We’re a hot ticket! Haha…)

Total change in net worth this month: (+) $35,627.71

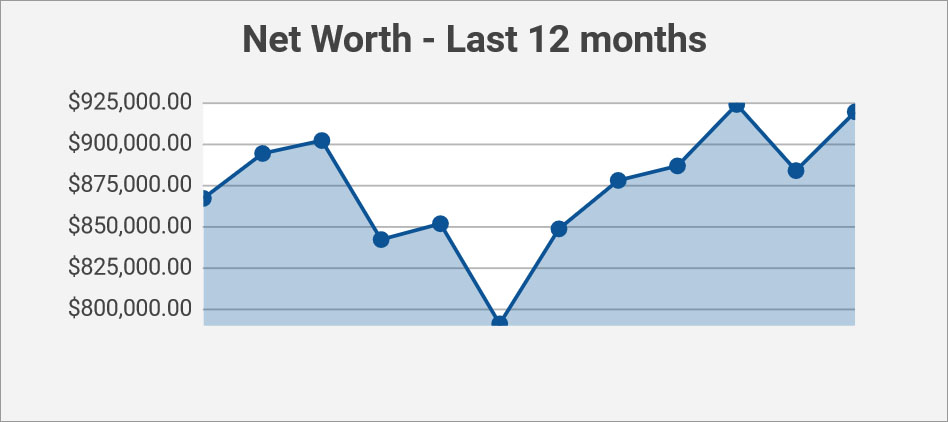

And then for better perspective:

So basically, about $50,000 more since this time last year :)

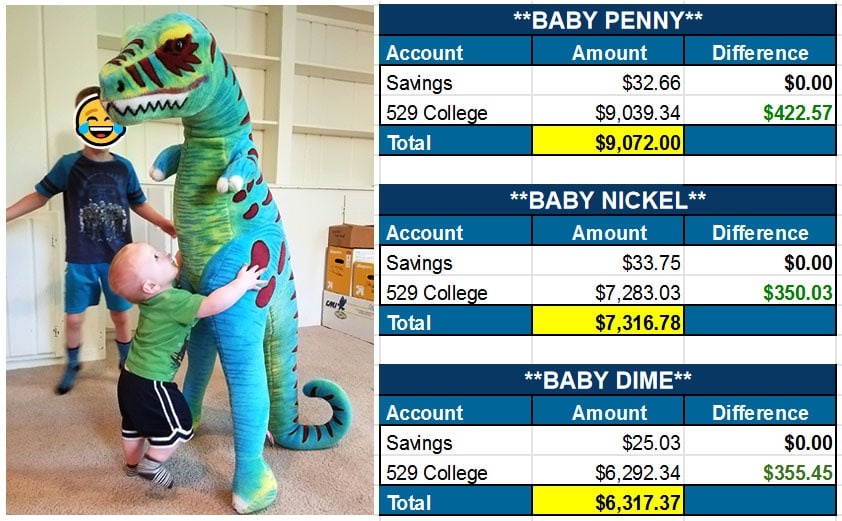

And then lastly, here’s how our kids’ money is looking these days:

[Ain’t nothing getting in the way of Baby Dime’s money! Haha…]

And that’s June!

Hard to believe we’ve already done over 130 of these reports over the years, but then I realize I’m almost 40 now and it’s spanned a good 11 years ;) So please don’t think this stuff happens overnight!! It rarely does! And anything you do for that long should see good results in the end…

So keep on tracking and stacking, my friends!! This is YOUR LIFE and you deserve to have a good one!

Some excellent resources are shared below for any new people to the site…

How did your money behave last month?!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Man, look at you J$ barrelling down the double comma club! I can’t believe you’ve already had 130 of these reports… impressive. I’m only a few years in, but I’m keeping consistent.

June was especially good to us because we had an influx of cash. In inherited ~$16k from an account that I didn’t know existed until a few months ago. Even though it’s 15 years later, it had been sitting there growing. :)

Love seeing equities back up, but we’ll see where volatility takes us the remainder of the year. Cheers!

Wowww that’s cool!!!

I’ll trade you my # of reports for your # of dollars over there? ;)

My sentiments exactly!!! Look at J to the Money, making it rain in your bank accounts! I love it!!! Two snaps for you!!

My investment philosophy was to keep it simple. I wanted it to be as exciting as watching my nail polish dry! I prefer index funds. Especially 500 index funds. I really like VFINX. Watching it grow from nothing, I mean absolutely $0 to over my first $100k was awesome.

Like Michael, I love seeing equities back up. But when they go down, it’s time to buy more.

Until next time,

Miriam

Congrats on hitting that first $100k!! Super exciting!

I find overpaying my mortgage is super exciting!

I hope I get there too!

Probably too focused on all the new debt still on this side :)

But like equity, J! :)

Actually, I was paying ahead for several years.

But I got lucky enough in my refi timing, and in 2013 got a 15yr fixed @2.875

I’m currently getting 2% in my MM. So paying ahead only saves my less than 1% which doesn’t highly motivate me.

I am still saving that extra and hoping to get an opportunity to invest it and “run-it-up” a little more before paying off my mortgage.

I can relate to this. When we refi’d to a 15-year loan we somehow managed a quarter point lower even than your superb rate; it gives us a hard payoff date of October 2030, which line up neatly with when we should be able to comfortably pull the FIRE trigger. There’s something oddly comforting about knowing the best financial move for us is to NOT pay that off early. ;)

That is oddly comforting, haha… way to go, gentleman!

My new net worth is 961.7K – up 13K this month.

Another new high. :)

Over the last 12 months, I am up $101K. That’s more than I make in a year, so yea!

Pretty incredible when you look at it that way!

I fell just short of my goal. What is it with being just short of a round number? It seems like net worths prefer ending with a 9 instead of a 0. You got $919,000 and I got $539,000.

haha… kinda like all those sales you see that always end in 9s! something so alluring about them! ;)

I got $559,097.92!!!! I’d like a few more 9’s in there!

Particularly in the front, right?? :)

So motivating! I can’t wait to see such a big climb in my net worth! Currently I’m -$50K or so.

I do have a question that maybe you/any readers could help me with.

I currently have a Roth IRA through RBC bank. Can I also start investing in VTSAX? Or is that also considered a Roth IRA?

Should I transfer my Roth over to Vanguard (if VTSAX is a Roth)?

Thank you in advance!! :)

A Roth IRA is a particular account type with particular tax rules and contribution rules. Other account types are regular brokerage accounts, IRAs (not Roth), 401ks, and Roth 401ks.

These accounts can hold any kind of investments, as long as the investment bank you are using offers it as an option.

VTSAX is an investment fund that can be held in any of these investment accounts.

With a 401k, traditional or Roth, you’re limited to what your employer allows and the investment bank they’ve chosen.

With an IRA, traditional or Roth, you can choose the bank you use. So, if you really want to invest in a particular fund and RBC doesn’t offer it, you can move your account to someone who does offer it.

Well said, G – thank you!!

And glad you’re looking into index funds, Leila!

Yay for progress! Glad to see your accounts rebound like that.

We haven’t calculated our net worth yet for this month, but we made a nice extra payment on our debt, so I’m anticipating a decent jump, especially if our retirement accounts behaved anything like yours. :)

Congrats! Extra debt payments sure speeds up the process! :)

Killin it!!

Almost at that nice big round number!

I like what you’re doing with the kids accounts on the side. My wife and I may be incorporating something similar to ours in the future!

Keep up the hard work.

-Chris

Cool! Be sure to check with your state and see if they offer any tax advantages to opening up 529s with them. That’s where ours are parked :)

J- I’ve been reading for nearly a decade and can report that for the first time ever, I have surpassed your net worth number. We clocked in at 938k this month thanks to the market surging back.

So…race you to the million mark??

Wowww you must know my life story by this point! haha….

But you’re on ;) Let’s hit it before year’s end!

I’ll asterisk this by saying your kids’ net worth is kicking the pants off of my three. How old do kids have to be before they can legitimately “earn income” and open Roth IRAs?? Sounds like a great topic for a future blog post!

An interesting question indeed! And one I don’t know the answer to just yet, other than “as soon as your kid can earn money” which I’m sure is a (very) gray area ;)

Narrowly missed a milestone for the second month! Actually TWO milestones: debt under $29k and net worth over -$14k.

I would have made the net worth milestone if we hadn’t gone camping. But I totally passed the stranger test there. (If a mysterious stranger said “I can guarantee you a month-end net worth over -$14k or I can give you a camping trip and guarantee you a month-end net worth just under -$14k” I would still have picked the version where I go camping.)

And mileage-wise I’m at… hm, apparently I’m at that deli I’ve been wanting to try. Is this a sign?

A sign that you’re good at ENJOYING LIFE!!! Couldn’t say I’d do anything differently in your shoes! :)

Nice going. How do you like the new home? Paying down the mortgage is great. I’m sure 15 years will fly by.

Our net worth increased quite a bit too. Let’s see if it can hold up for the rest of 2019. I’m very nervous about the stock market.

Haven’t moved in yet but close! It’ll be nice to finally USE the house we bought, haha…

How’s your selling going?! Any luck this month?

Gotta love when the market rebounds like that! Who’s knows what’s actually gonna happen each month, which is why it’s great to not worry about it and just keep investing! (<— reminds me of Dory from Finding Nemo, substitute investing instead of swimming! :) )

This is true :)

Net Worth crossed the €30k mark, and I’ve opened my 1st investment account (even though there are no Vanguard funds here). Crossing fingers the NW really starts soaring in the coming years :)

Work it!!!!

That 1st investment will be the start of a fun and profitable journey throughout time! :)

Our net worth finally crossed the $400K mark! Yahoo! Up close to $80K this year thanks to the market rebounding, trying to max 401Ks and paying $5K extra on the mortgage pretty much every month. If we can keep this dizzying pace, we will be reaching $450K by the end of the year and that amazing half a million next year. Double our net worth since we got married 4 years a go. I would say finding Mr/Mrs Right has a higher impact on net worth than we like to admit.

I get the whole interest issue. We did not have enough to put down on the house since the money was locked in our old one when we bought this, so we got stuck at 4.25% and PMI and 30 year mortgage. Got PMI cancelled as soon as we could but still stuck with the rate. Paying it off intensely, since we max out 401K and at this point I think it will give us better return than the market where we are at.I know some folks won’t agree but I would rather have a paid off home and that money out of the market so when it crashes in the next few years we can pour it in if we so decide.

Killing it with those monthly contributions!! That’s more than some people put in every year – or even YEARS! And no shame on that housing strategy – hard to complain having a paid off house ;)

I’d been tracking our home’s estimate value via Zillow, but I think I’m going to stop as soon as we get a reappraisal (we’re hoping to get approved by our lender to get rid of PMI thanks to our house *hopefully* reappraising for a lot more thanks to a hot market). Once we get that number, I’ll just leave it there until we get a new one, since Zillow’s numbers are all over the place! They’re actually responsible for even more fluctuation in our net worth lately than our investments, which should tell you something.

Are you planning on doing a monthly spend-down report of your mortgage payoff like you did last time, or just include the numbers here?

I like the re-appraisal route :)

And yup, will probably do some sort of reporting on the mortgage pay off stuff… Haven’t thought too much about it yet as step one is just *getting into that house!*

Yeah, it’s been a good month, J-slice! Doing good over here too. Well, at this stage, a low market means stocks are on sale and in a big month means we’re earning!

Maybe you posted this before my time, but what was the end goal FI number again? Or are you keeping that super secret? And, it occurred to me, what will FI look like for you? Will you keep doing BAS?

Interesting I received an email today from my FIRE’d friend, Poky Pedal Bob, about make his withdrawals from his account right now because the markets are up. It makes some sense on the surface but I can’t help but think about the fallacy of market timing. It’s his money and I wouldn’t dream of telling him what to do with it, but I couldn’t help but think about how I would handle this situation when I reach FIRE. Is it better to simply take a set amount every three months, or once per year, or try to take advantage when the markets are up?

All great questions indeed! I feel like i’d just continue taking out a monthly withdrawal as I currently do now which would help average out losses/wins over time, but I haven’t really given it too much thought to be honest. Still a ways away from being truly independent, even though I’d like to think I am at times :) (our “number” is around $1.7mil, but it seems to fluctuate depending on life events (babies/moves/etc) so I don’t pay too much attention to it currently… Kinda just going with the flow and saving/investing as much as I can until we get closer to it for real! And to answer your question re: what I’d be doing once we finally hit it, it would probably be close to what we’re doing now: working on projects that excite me while spending time with my kids and learning/reading/growing! Though I’d probably cut back on the time working on the blog since so much of it does revolve around maintenance and other boring stuff, haha… But we’ll see…)

I somewhat suspected that would be your answer – that you would basically do what you’re doing, just a little less of it. That’s my plan too – other than a few things I’ve had to put off for time, I see myself doing almost all the same things, just more of them at a more relaxed pace! I even will probably freelance for my current day job, I just won’t be required to work 40+ hours per week and can take assignments as I want. I think that’s the ideal situation to be in pre-FIRE.

Totally. The world waits for you now instead of the other way around – a good place to get to!

2019 year to date June 30 has been a great period. Wipes out the atrociously bad last half of December 2018!

Totally.

J –

Making MOVES. Collect any big dividend checks for the quarter end that were reinvested at all?

Also – thoughts on a potential refi for you in July if rates cut? Could be worth and knowing you – you’ve probably already calculated your point when it makes sense.

Can’t wait to hear. Keep KILLING it.

-Lanny

No idea on either actually! Haha…

I always forget to look at the dividend section of Vanguard, even though I know they do roll in :) And refi we’ll certainly be taking a look at but first just want to be moved in and unpacked which feels like it’s taking forever, haha… only a matter of days now though!!

Got a net of $563k….I took lowest values of our properties and didn’t include cars or collectibles or jewelry. Just cash values of big ticket items and investment accts. It makes my life simpler.

I can get down with that… whatever keeps the ball moving!

Hello, Jay Wow that is some great numbers $$$.$$$, I´M also working my way to the million, and putting money in different “pockets” and trying to pay out my mortgage, so I can free up more money. Exciting to follow your journey best regards Christian from Denmark

Denmark – cool!! Nice to e-meet you!

Our gains were mostly market gains and a little bit of cash saving.

Perversely, I’m a little annoyed that the market is up this month because I’m itching to buy more index funds / stocks and I want a deal, darnit ;D But I’m sure there will be a little drop I can catch later. Just gotta be patient since I’m testing out lump sum investing for a year or two. (Cuz why not? I’ve always done dollar cost averaging and I want to try something new for a bit.)

haha go for it!! but only if you report back your findings, please :)

you will have no problems finding a dip sometime soon!!

My net worth jumped up a little over $10k this past month. So, a nice recovery from the down $4K the previous month. I’m also paying extra on my mortgage, it’s the only negative line item in my net worth calculations and I can’t wait to see it gone!

Haha… that’ll be a fun one to see gone for sure :)

Our lender did the same thing when we bought our house. I just figured it was because they are a small-town bank and maybe they don’t hold on to mortgages, but honestly, I don’t know the reason behind it. The bank that bought it from the first bank was then bought by another lending company so our mortgage has been under 3 different companies, technically, and we’ve only owned it for going on 5 years!! Haha!

A popular house! :)

I have been following your blog for at least 4 years and I’m so happy to see you guys so close to the million and I loved reading the end of this post seeing your kids college funds!! I’ve always wanted to blog the tracking of my net worth (have been doing it since 2014) but instead have just kept it to myself! It’s one of my favorite things to do month-to-month and to see the way it changes! Hitting the big 3-0 this month and hopefully 350k nw as well!! Thanks for sharing your story as always!!!

A big fan!

Oooooh very well done!! That’s a lot of money for your age! I was around $140,000 as I turned 30 :)

If you ever want to share your story/numbers with us here on this blog, just shout and we’ll make it happen! Should be very proud of yourself!

This is the year it happens.

When/Where is the million dollar party you will no doubt be throwing?

;)

Your house! I’ll supply the fun if you supply the beverages :)

Fun fact: you have $794k in your retirement accounts (not sure how to account for the TSP, but included it anyway). At a 4% withdrawal rate and assuming 2080 hours a year, you would “earn” $15.27 an hour, which is more than the minimum wage is set to be in California after all of the annual increases that are coming.

wow – that is fascinating! what got you thinking along those lines? have you calculated your own hourly earnings too? :)

Yup, every $52k is another dollar an hour! I’m past minimum wage, for now…but need to keep growing to keep pace as it increases in my state. I’m not sure why I’m thinking along those lines since I’m not an hourly worker…it’s just fun!

yeah it is! HAHA…

if you ever want to write up something about it I’d be happy to feature it on the blog once I’m back in session :)

neat way of thinking about things!

Great job at having a positive net worth! I am curious to know why you are financing cars when you could have them paid off? I’m a Dave Ramsey guru and follow those guidelines to be out of debt. You have a positive net worth, however, you don’t own your cars or house.

We do own the cars (both are 100% paid off), but def. not the mortgage…

Yet :)

Just picked up the house two months ago so it’ll take a little time…

Hey J, thanks for sharing your progress. Indeed, last month’s bloodbath was a tiny blip of 7%, something that I took advantage of. I was wondering if you hold individual stocks or buy the index ETF? I have written some articles on choosing great companies and would love for you have a look. https://onceamillenium.com/how-to-select-wonderful-companies/

Cheers!