“A budget is simply telling your money where to go instead of wondering where it went.” – John Maxwell

Good morning, money friends! Hope you had an awesome Christmas weekend!!

Today I’m gonna run through a quick overview of my annual and monthly budgeting process. It’s super simple and doesn’t take me much time — about an hour at the start of every year and 20-30 mins each month.

Maybe this will help some of you in your 2022 planning (or maybe you’ve already got a solid budget process nailed down? 🤷♂️). Either way, it never hurts to see how others do things and maybe borrow some tips/tricks to incorporate into your system.

At the end of this post, I’ve included a few budgeting tricks I use to save time, keep it fun, and make sure I stay consistent!

**And for those of you who really want to make budgeting SEXY… check out this old gem we published way back in the day… Introducing Strip Budgeting. As J. Money would say… “Hubba hubba!” 😍**

Start With a High-Level Budgeting Process

I like to think about budgeting as 3 separate activities that happen throughout the year:

- PREVIEW: (annual, takes me about 1 hour) At the start of each year, I envision all my expenses and things I want to spend money on. The total $ is my annual budget.

- REVIEW: (happens monthly, takes about 20-30 mins/mo) At the end of each month, I review our spending, compare it to the budget, and check to see if things are on track.

- COURSE CORRECTIONS: (as needed along the way) Throughout the year, life changes. So I make modifications to either my numbers or my spending habits.

If you don’t currently have a budget or are looking for a new template, here are a bunch of free budget templates and spreadsheets. Or, here is the simple one I use. Nothing fancy, I just created it in Google Docs.

OK, here are my annual and monthly activities broken down:

How to Set an Annual Budget (Your Year in Preview)

At the start of each year, I try to set an annual budget number. This is a forecast of approximately how much my wife and I plan to spend in the upcoming year.

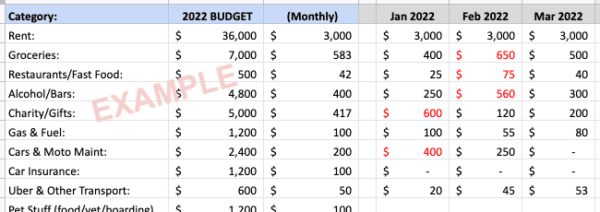

We have about 20 spending categories, and each one gets its own assigned budget. My basic template looks like this:

![]()

First, I forecast all our fixed expenses. These are the things I already know the exact cost of… Like rent, insurance, car registration, internet and phone, etc. Since I already know how much they’ll cost, I just stick those numbers straight into the budget. Easy.

Next, I look at all my variable expenses. These are things that can be high or low depending on the month. The best way I’ve found to forecast variable expenses is to look at how much I spent in total the prior year. Then, I adjust a bit for inflation, or upcoming life changes.

For example, in 2021, I spent $7,015 on groceries. Some months were low (in March we spent $331) and some were really high (July we spent $1,027). Since I can’t predict which will be the high and low months next year, I really only care about the average and total.

- As for inflation, if I were to buy the exact same groceries next year as I did last year, they might cost me ~5%+ more. So Instead of forecasting $7k for next year, maybe I want to make it $7,500 to be more realistic.

- As for life changes, my wife and I might have a kiddo or two next year… so maybe I want to add another $1k to cover them for food, too?

Anyway, you get the point… after thinking ahead a little bit, I assign an annual budget number for each category, and divide that by 12 for the monthly number.

Lasty, I try to plan for large, isolated expenses in the upcoming year. I assign numbers to these based on how much I think they might cost.

For example, here are some isolated events that I need to budget for in 2022…

- Weddings: I’m invited to 3 weddings next year, and in one I’ll be a groomsman. So, I’m going to add a $2,000 budget line item for “weddings” to cover gifts and travel. Since I won’t have this expense every year, I keep it separate from my regular annual travel/gifts categories.

- New (used) car: My wife and I might buy a minivan next year. Maybe I’ll add $20,000 as a budget placeholder. (Or maybe we’ll just make our kids suffer in the Prius – haven’t decided yet. 🤣)

Everyone’s numbers are different. Everybody’s life goals are different. It behooves you to make your budget as custom as possible to YOUR life, income level, and desires.

A successful budget is more about knowing yourself than it is about the actual numbers. If you build a budget based on what everyone else does, a) you won’t have any fun, and b) you’ll be living their life goals, not yours!

How to Do Budgeting Every Month (Month in Review)

After our annual budget is set, I do monthly check-ins.

My wife and I use Mint.com to track all transactions. (I highly recommend others check out Mint, Personal Capital, YNAB, or any automated software that tracks transactions.)

First, I download all our transactions from Mint and sort them by category. Then I total the categories and stick them in my budget spreadsheet. Each month has its own column in the sheet. Looks like this:

For the most part, I’m not really concerned about small variances in our spending vs. budget numbers. (We are not on a tight budget.) What does concern me, however, is a trend of overspending.

That’s why I like having all of my numbers side by side in a budget spreadsheet. At a glance, I can quickly tell if we are slipping into bad spending habits that need correction.

How to Adjust Your Budget (Mid-Year Course Corrections)

It’s unrealistic to think that we’ll spend exactly what we budgeted for every month and year. Budgets aren’t exact. They need wiggle room.

Here are a few adjustments and things my wife and I do mid-year…

First, if we underspend consistently, this is AWESOME! It means we accidentally budgeted too much. Underspending in one category can sometimes cancel out overspending in another category.

When we notice consistent overspending in a category, before trying to correct it, we ask ourselves these 2 questions:

- Is this spending in line with our values in life? (My wife and I are trying our best to do values based budgeting.)

- If overspending continues, will it majorly derail our life goals or financial plans?

If we are overspending on stupid crap that doesn’t add value to our life, we try to cut it out ASAP. This requires being more mindful during the following months, checking in with each other more regularly, and perhaps even starting a savings challenge of some sort.

But, if we are overspending on things that DO provide us a lot of value (and it’s not majorly derailing our wealth-building journey) we allow it to continue.

For example, I mentioned we spent ~$7k in groceries this year (but we only budgeted for $6k). I realized we were going to blow this budget a few months ago, so my wife and I sat down to discuss it… We agreed that groceries and food is what we LOVE spending our money on. (We host a lot and enjoy buying premium ingredients for special occasions). In this case, we agreed overspending was OK to continue, instead of switching to beans and rice for the rest of the year to cut costs.

To compensate for overspending, we try these types of things:

- Reduce spending in a different category. For example, we might cut back on mid-week drinking for a month or two. This could save us a few hundred dollars, and we could put that toward the overspend on groceries.

- Pick up a temporary side hustle to cover some costs. This year when Cooper had ~$400 in vet bills, I was able to cover those unexpected costs with additional contract hours at work.

- As a last resort, we break into our emergency fund or pull from investments. We really haven’t ever had to do this, but it could happen if we hit large unplanned expenses (like our car completely dying or a medical emergency).

Automation, Saving Time, and Keeping Budgeting FUN

One of the main objections I hear about budgeting is, “I just don’t have the time!”…

Maybe some of these things will help:

- Automate your expense tracking! Sign up for Mint, Personal Capital or use your bank’s online app to categorize your transactions. It saves manual tracking.

- Limit your cash transactions. Since you have to track cash purchases manually, instead try Venmo or PayPal, which can be tracked via automation software.

- Round things to the nearest hundred dollars. Instead of calculating every single cent, try rounding numbers to save time.

- Limit how many categories you have. For example, I used to track hotels,flights, airport food, and Ubers all in separate categories… But that took too much time, so now I stuff all that type of spending into a single “travel” category. Much faster, and arguably the same thing!

- Budget consistently. The more you do it, the faster you’ll get at it!

All in all, you can make your budgeting process as complex or simple as you would like. Do yourself a favor and choose the latter. 😉

As for keeping things FUN, try some of these hacks:

- Set up monthly rewards for when you beat your budget in certain categories. Having a reward system will keep things enjoyable and make you want to track progress.

- Budget over a date night (for couples). You don’t need to be hunched over a computer while budgeting… Get out of the house and have discussions while you walk, exercise, or over a delicious meal somewhere.

- Create colorful and engaging charts to attack debt, track savings goals and chart progress. Check out these free budget printables.

- You can woo your partner with a nerdy powerpoint presentation, like this guy does each year ;)

- Sometimes just calling it “budgeting” can set a negative tone. Sometimes when I want to talk about spending with my wife, I just say, “Babe!… I just reviewed our spending and let me tell you all the ways we kicked ass this past month!” This is how we have budgeting conversations without actually having budgeting conversations.

- Earlier I mentioned Strip Budgeting… I was kind of kidding… but maybe it’s worth trying anyway? Haha!

*****

Whelp, thanks for reading this long-ass post on my budgeting process. Hopefully you got something out of it.

Whatever your budget process is, I truly hope you are set up for success in 2022. Please let me know if you need any help, have any questions, or just want to geek out on spreadsheets. Personal finance isn’t just my job, I genuinely enjoy helping others save money, make money, and live more intentionally. Let’s chat!

Have a great last week of the year!!!!

Joel

Get blog posts automatically emailed to you!

I’ve found that bothering with all the detail isn’t value-added time. I set three primary targets every year:

1. Target spending limit

2. Minimum saving target

3. Target investment corpus value

All of the details of what we spend money on are capture by my bank and Simplifi. My investments are tracked in Personal Capital. I find managing these 3 numbers to be all I need to meet or exceed my long-term objective.

Love the simplicity! One of the biggest excuses I hear about budgeting is “I don’t have the time for it”… But if you create a simple system and boil it down to just a few total numbers, it becomes very quick! Thanks for sharing, Dan!

Do you not track income? How do you account for reimbursements? For me, this really shows up with medical expenses since we must wait on dental reimbursements so monthly expenses can get wacky.

Hey Mary! No, funnily enough I’ve never tracked income. I mentally note when/how we get paid, but our income has always been higher than expenses so it’s never had to be fully accounted for.

I rarely have reimbursements either (and if someone owes us, they usually pay within the same month) so I haven’t had to worry about that. Maybe things will change when we have kids with all the bills and stuff.

Can you just create an ‘accounts receivable’ line item with anything that needs to be reimbursed and then add notes to follow up wach month? This would keep it seperate from your regular spending.

I have been using Mint for a decade and absolutely swear by it. I love going back through my old transactions and seeing which merchants take the most of my cash. Spending up about 6 grand this year compared to last year’s shutdown environment!

The merchant breakdown is fun, but scary! When I look at specific retailers like (starbucks) I feel sick seeing how much I’ve spent in total over the years!

I like it, very actionable.

I think a Prius a perfect car for a family of four, as long as the persons sitting in the back are not taller than 1,5 m.

When we were looking for a new used car, I tried to sitting the back row, but could not sit upright with my 1,74 m.

Then I ruled that car out, because our older kid was already 1,5 and only 9 years at the time. But the car was meant to last 10-15 years.

Yeah with 2 little ones we should be able o get by for a while. But if they grow fast, i think we’ll need to upgrade!