[As part of our weekly column by Mr. 1500 of 1500Days.com – a fellow blogger who retired at 43!]

******

So, I’m financially independent and no longer work, but I still have a load of debt. And I love it. This debt has made me some serious money. I’ll explain all, but let’s back up for a moment.

Mortgage Debt

That debt is my home mortgage. I bought my last home for about $175,000. I had the cash to buy it outright, but didn’t. And for reasons that I can’t quite figure out, a lot of folks, especially in the financial independence community, insist on paying off their mortgage early. I’m in the opposite camp. I never pay even a dime more than I have to.

The main reason I didn’t pay cash for my home was because I wanted to keep the money around in case an opportunity (rental real estate) presented itself. This never happened, but something much more interesting did.

Paying Off The House vs Investing

I never got that rental property, so left the money in an S&P 500 index fund. I love numbers, so let’s run them to see how this turned out:

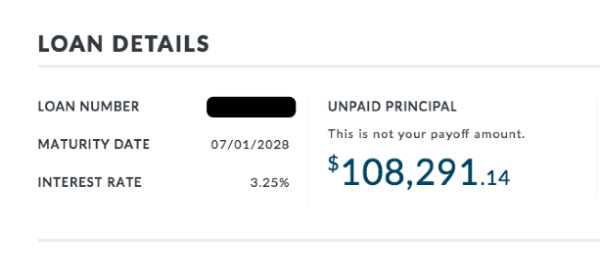

- Mortgage: 15 years at 3.25%

- Amount borrowed: $140,000

- Mortgage interest I’ll pay over the course of my loan: $37,073

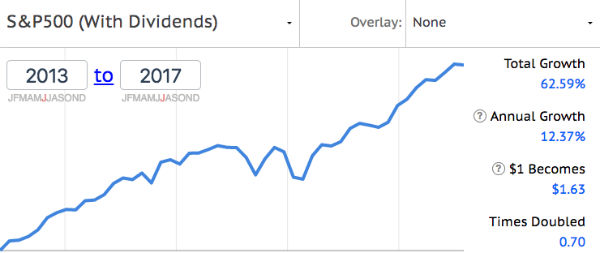

Brace yourselves, here come the juicy bits. First, the chart below shows the slightly above-average performance for the S&P 500 since I bought my home:

In the time I’ve had my mortgage, each dollar I’ve left invested has grown almost 63%. The means that the $140,000 that I left invested is now worth $228,200. This is a gain of $88,200. So now, we arrive at this:

$88,200 (S&P 500 growth) >> $37,023 (total mortgage interest)

Less than 5 years into my mortgage, I’m up by: $51,177

How do you like them numbers?

But! But!! But!!!

I can feel the anger in the crowd:

The market has been on an incredible run!

It sure has, but in how many 15 year periods has the market returned less than my interest rate (3.25%)? I have no idea how to figure this out, but I’ll bet that it’s not common. Maybe someone smarter like Michael Kitces or Papa ERN has the answer. I don’t lose sleep over this.

A paid off house gives me peace of mind!

Why? Wouldn’t a bigger pile of money give you more peace of mind? If the S&P 500 returns for the duration of my mortgage are consistent with past performance (~10% with dividend reinvestment), my $140,000 will grow to $584,000.

I paid off my house early and now just invest the surplus.

That’s OK, but you’d probably have more money if you didn’t pay off your house and just invested the whole lot instead.

Debt is evil!

I can get behind this one a little bit. If you have no self-control and worry that you’ll blow your money on handbags, golf club memberships and cruises, please pay off your house. Don’t even consider doing anything else.

And I Didn’t Even Mention…

Interest rates will go up: Would you feel foolish if you paid off your 3.25% rate only to have your bank account pay you 5%? My federally insured (FDIC) Internet bank account was paying over 5% in 2006. Banks won’t be paying you 5% (or even 3%) any time soon, but the rate trajectory is upwards.

Powder keg: Once that money is gone, it’s gone. Well, almost. You can take out a line of credit against your home, but those rates are variable. See the point above.

Mortgage deduction: This is overrated, but is still valuable to some.

Let’s Reconcile

You’re mad at me. I know it. While I won’t apologize, I will pat you on the back. If you own your home free and clear, you’re in the minority. Only 20% of Americans are in this boat. You’ve done well for yourself. But you and I have different goals.

My goal is to deploy my money in the most effective way possible, even if it means having debt. And by effective, I strive to maximize my pile. A big pile is peace of mind in my book.

****

EDITOR’S NOTE: Many of you of course know I’ll agree to disagree here, but I love me a healthy debate so by all means jump on into the comments and let’s talk about it :) I think Mr 1500’s points are dead on if you’re a more “numbers/logical” type person, however, if you’re a more “emotional” one such as myself, well, you need to do what helps you sleep better at night. What’s the point of having more money in the bank if it makes you miserable?? Only YOU know what’s best for you and your family, so keep all this stuff in mind, but at the end of the day make the calls that are most aligned with your own happiness. No shame in EITHER routes here as both of them increase your net worth! It’s not like you’re blowing your money on crack cocaine!

(It does remind me of another guest post we featured here a handful of years ago though… Hard to feel bad for the guy, but it does prove Mr 1500’s point: How I Lost A Fortune Getting Out of Debt)

Get blog posts automatically emailed to you!

Thanks. You’ve reaffirmed my decision to not pay off my house loan @ 3.1% (thank you financial crisis of 2008) and invest the money instead :)

Claude

I am aggressively paying down my mortgage. My emergency fund is fully stocked, i maximize my tax advantage accounts, I have cash sitting around for some fun, and I invest in a taxable account. I am paying down my mortgage because frankly, I don’t have any other place to put it without increasing my risk exposure…. It is truly excess cash with no other purpose.

^^^ This comment ^^^ =)

I’d love to have my house paid for just because I could use the money to do other stuff and a huge piece of pride to say “I did it”. But both you and Grettman said it. My index fund is growing nicely. I have some “fun” cash laying around, and Im not fretting…

We are trying to pay off our house too. We’re counting down the day when we can say we’re 100% debt free! If everything goes according to plan (none of us lose our job), that day will come in the near future, and I just can’t wait! It’s such a relief to know that even if both of us lose our job, we will still have our house to our names!

Yes!! Love!! Great point on keeping risk levels in check too.

We’ve had this discussion over and over. We know the benefits to both options. We just personally prefer the idea of paying off the house.

Would we make more investing? Probably. Almost definitely. But, this is what will give us more peace at night. We already have a 15 year mortgage, and we pay extra on top of it, with the goal of owning it outright in around 6 years or so. :)

I paid off my home and it opened up some options for us that we wouldn’t have otherwise taken. I took a risk with a job knowing that if I got fired that I wouldn’t get tossed out on the street if I couldn’t make a mortgage payment. On top of that my wife was able to stay at home and take care of her special needs sister and our son. Plus during the period that we paid off our mortgage during the late 2000s, the market only rose 3.6% vs. a mortgage rate of 3.5% For 0.1% we’re okay on missing out on that gain :)

Until now I accepted the “paid off house gives me peace of mind!” reasoning but you just opened my eyes to the “Why? Wouldn’t a bigger pile of money give you more peace of mind?”. You will have the money at your hand generating more money than your payment needs ( and you can still pay it off anytime you want). From this perspective doing otherwise is illogical. Will keep this in mind if I ever will get into the situation. Thanks.

I’m right there with you, BUT … The reason I’m forging ahead with our mortgage pay off is to bolster our reliable cash flow after early retirement. I know I know – I’ve run the numbers to a similar conclusion. But #2, our 5-1 ARM expires in two years so that has me a little freaked.

As for our rentals? No way in HADES are we ever going to pay down those mortgages early. See, a little balance there. Thanks for making me rethink our mortgage pay down strategy. I’m going to go mope over a spreadsheet for a few hours…

I like that balance there :) Pay off the home residence, but leverage the side business debt. Much easier to separate the emotions out of the business stuff vs personal stuff too.

This seems like a Math vs Emotions debate. Since I know what it feels like to have mortgage debt, but don’t know what it feels like to have my mortgage amount sitting in a brokerage account earning me money. My plan is to build up my mortgage amount in my brokerage fund and then make the determination which route I’d like to go.

This is a very compelling case for Math over Emotion, which in most instances is usually the right call.

You’re right and it shows once again conventional wisdom – eliminate all debt – is not always correct. You have to run your own numbers as Mr. 1500 has.

Having said that, I’m ecstatic that I’m FIREd with no debt! :)

Yep, and I admit that the emotions are hard. A paid off home is very appealing, but after considering my situation for a while, I wish that I had a 30 year mortgage instead so I could put even more money to work!

I am in the good debt camp. Over the past 7 years, I could of almost pay off my mortgage debt, but instead, I chose to refinance my mortgage three times and borrow more money to invest. Here’s what I ended up with:

– three extra streams of income

– saved an extra $200,000 over a ten year period

– have an extra $1.2M in stock and real estate assets working to earn me more money while I sleep.

– get a large tax refund every year because of the interest used to lower my tax bills.

Borrowing to invest is not for everyone, but if you put in the time and effort, you will put yourself on the fast track to FIRE.

Nice!! Congrats man! Always a good feeling to know that you can pay off your debts at any time too – even if you choose not to. That’s some empowerment right there!

Hi, agree with you. I think you forgot one important reason: your nominal debt is frozen. This means that inflation is eating out your debt with time, while the earnings of the companies you are investing in get are inflation protected. It’s true that inflation normally leads to raising interest rates, but the principal in real terms just gets smaller and smaller.

This is vicious as it is actually a debt incentive, but if central banks set these rules, it’s fair to play according to them.

My €300k 10year mortgage @1,65% . Yep, they’ve gone nuts in Europe.

Interesting way of looking at it! I’ve actually never thought about that one before. I love learning new things :)

I wholeheartedly agree with taking on debt but understand it is in contrast to many FIRE bloggers. I wrote about my experience refinancing my house. I see it more as rent than ownership and do everything possible to increase cashflow that can be used for other opportunities. You can read about it here:

https://blogsofstuff.com/2016/05/04/personal-risk-management-and-liquidity/

We also made a good profit on selling a house in 2005 and rather that roll it into a down payment on the new house, we banked it. A few months later we were able to invest in commercial property with it that otherwise would never have been possible. We are so thankful for that decision and opportunity.

Cash in hand= opportunity

Hehe I’m in the debt payoff camp, and no I’m not mad at you for speaking your mind and voicing your opinion.

I realized that debt payoff depends one each person’s level of risk tolerance. It’s the same as when some people prefers apples and some like oranges. They both have their own taste and nutrition. One is not necessarily better than the other.

My thought is always that if you’re in a position to have to make this call, there is no wrong answer. Having extra cash is always good and the right move will depend on a ton of factors.

We are opting for both, with a slightly more aggressive payoff and also making sure to dump as much as we can into tax advantaged accounts.

My wife worked multiple jobs in school to avoid student loan debt and is very debt averse. Therefore while we have a mortgage, we won’t have it for its full term. We’ve reached a happy middle ground of paying it down in a reasonable amount of time and investing enough to let us hit our target retirement date.

We still carry a mortgage even though our brokerage account is many times the size of our mortgage. We will likely pay it off in a few years when one of our stocks is finally sold, but for now it is the only liability we carry for the single purpose of the small tax benefit it provides.

I definitely side with the math on this one, we haven’t paid any extra on our mortgage and don’t plan on it for the foreseeable future (if ever). My tune might change if our interest rate was closer to 5% instead of 2.75% (10 months into a 7 year ARM).

I do like J$’s comments – neither is wrong and both improve your financial situation, but one has a very high probability of winning from the number persepective.

For those who have children about to go to an expensive college who are in the margin of getting financial aid, hiding money by paying off the house has a big ROI. But that’s a special case. (Maxing out retirement is also a good place to hide money.)

Ahhhhh yes, another good factor to consider as well. Stealth wealth :)

Well, obviously you can (and should) do whatever you like. I would be very interested to see your post if the S&P tanked and is worth only 60% now. In additon, assume your property lost 40% of its value as well. Now please explain your strategy to your mortgage banker.

Long story short of what you did…you just took more market risk.

Nevertheless, it seems to work out for you, so congratulations!

Kind regards

Harald

Great point!

And I think the S&P will have a big correction and fairly soon. This is just how things work.

If you look at my numbers, even if it lost half its value tomorrow, I’d still be ahead. And I’d have 10 more years for it to grow even bigger.

And if my home lost 40% of its value, I’d still have $200,000 in equity.

But my situation is not important to this argument. I fully acknowledge that you may lose money by following my example, but you probably won’t.

Mr. 1500,

much appreciate your comment!

Honestly, you will be fine either way. There is just more than enough cushion in your bank account :).

However I personally would not recommend this strategy to someone who invests into his first asset.

Assuming he has $100k of cash and his asset would have cost him $100k as well. Now he takes on a 100% financing and invests $100k into the stock market.

In this situation, the borrower has a legal obligation to pay interest and amortization. Now a market correction takes place and his stocks loose in market value (e.g. they are worth $80k). In addition his house is worth only $80k. The borrower still has to pay for debt service and must cover his principal of $100k. Furthermore, his LTV is above 100%. Now, the borrower might have troubles.

To make it short, I don’t want to sound super clever or something else. You have much more experience than I do. The reason why I am quite pessimistic is probably that I always worked in real estate financing, where everyone only thinks in downside scenarios, haha.

Kind regards

Harald

I’ve got a few million dollars that agree with you Mr. 1500. I could easily pay off my mortgage but I don’t… I’m simply going to be wealthier NOT paying it off.

Yes, it’s true that I happen to live in one of the hottest housing markets in the USA, so that doesn’t hurt either.

Once a person’s net worth is ten times higher than their mortgage it really ceases to be an issue.

Drinks on you if we ever meet in real life ;)

Ahh, the age-old debate!

I think we’re going to take a dual approach: we’ll overpay on our mortgage while investing. Sure, we could pump all of those funds into investments for higher gains. The issue here is that I’m in the more “emotional” camp of wanting to live in a paid-off house. If the market takes a tumble during my retirement, I don’t have to worry about making mortgage payments.

We are in the same boat! We are building up our retirement accounts while we pay a little extra on the mortgage. Neither will make us rich quick, since we don’t have much extra to add to these, but as we progress in life and, hopefully, earn higher salaries, we will eventually pay off the house a little early and then hope to invest in some real estate or put more into the stock market. Our mortgage interest rate is 3.5% so it doesn’t worry me too much to keep it around for a bit, although I’d love to not have to pay a mortgage payment every month.

Interesting that only 20% of Americans’ houses are paid off. That seems a little low to me. Are there a lot of retirees that are still paying a mortgage? I think most people are too afraid to invest the amount their house is worth in the stock market. If they would leave it in cash they might as well pay it off sooner.

This was a very interesting read and not something I had thought much about before. It’s a little too late for me as I have been one of those working hard to pay off my mortgage early and now only have 3 months left to pay it off, but maybe I didn’t go about it the right way. Every spare penny we had went on the mortgage, maybe I should have invested it elsewhere!

No shame in almost having it paid off like that – well done!

Are you going to do an old school “mortgage burning party” in 3 months? :)

My favorite point in the whole thing:

“Wouldn’t a bigger pile of money give you more peace of mind?”

When you consider your assets and debts as one big pool that can each individually be represented by a specific dollar amount, it’s obvious. Your gains will likely outweigh the benefit of early payments, so if for any reason you find yourself in need of being debt-free, you can – depending on tax consequences – probably liquidate a portion of your investments to pay off the mortgage entirely and still come out ahead.

Early payments on a debt like this are fine, but are a purely emotional decision based on irrational hatred for any debt.

“Early payments on a debt like this are fine, but are a purely emotional decision based on irrational hatred for any debt.”

YES! You should have written this post, not me!

I have only recently come around to this way of thinking… For me the problem was never logical but rather psychological. I have a severe allergy to debt. It makes my skin crawl knowing that I have willingly given someone power over the only life on this earth I will ever have.

Anyway, when I bought my house I was not nearly as into my FI journey as I am now. That’s my excuse. I put 3.5% down and took out an FHA mortgage. I had to in order to buy this place as the FHA loan limits were higher at the time and nearly everything in my area is 500K + if you want a regular decent house in a good area. All of the FI arguments don’t hold up here because like I said, I was not at the place I am now in my FI journey. Also, we were going crazy in our town home. Some people love living in town houses, we are not those people.

Long story short, I have 60 months of Mortgage insurance mandatory, I can remove once I get to 78% LTV. So I have about 9 months left to make it, and as of my payment in October I will be there. I put everything spare into the house to make the threshold to remove MIP.

However, after next months payment I’m done putting a penny extra into the house. For 2 reasons. 1. I’ve timed it so that when I am 59 the house is paid off. and 2. I’ll make a lot more money but throwing the extra into index funds for 20-25 years. and 3. I’m sick of choosing to be house poor…

I like to say I’m more on the numbers side, and agree with your last point to deploy your $$ in the most effective way possible. But this can mean different things to different individuals. (Admittedly, I’d also likely lean partially toward the zero debt side as well depending on potential conditions).

We currently have no debt, although we don’t own our home (content renting); we do have about 25% of our net worth in real estate exposure though. If we are to own our primary residence some day (which is the eventual plan whenever that might be), I’d envision us wanting to pay it off as quickly as possible without completely reducing opportunities elsewhere in the other investments.

It’s about finding that balanced approach that works for you.

How do you define “effective?”

And nothing at all wrong with renting. In most cases, that’s probably a better strategy than buying, at least for the bottom line. I only own a home because I pump loads of sweat equity into them which translates into real equity: https://budgetsaresexy.com/this-is-why-i-own-a-home/

“Effective” depends on what I need and/or want it to mean given a set of conditions that can vary throughout the year. Admittedly, this is a bit subjective, but it can also provide objectivity around what “feels” right.

A few examples:

1. Annual and/or Infrequent Expenses: Mrs. BD and I don’t like the feeling once of year of paying our ~$450 annual premium toward our homeowners insurance, which also includes some additional coverage that we feel is warranted. To lessen the feel of having a somewhat larger expense once a year, we save 1/12 of the amount each month via Qapital. We know the insurance is a must and it does feel better to know we have sufficient coverage, so we view the cost as an effective use of our capital.

2. Growth and Income: Mrs. BD and I like to see or feel “progress” in our investments; we’re a big fan of REITs, large-cap value stocks, and other income-producing assets that have the ability to appreciate overtime while also providing some type of current income (which we currently reinvest). We do have other exposure to both domestic (US) and international assets that might only pay out annually, but the more frequent distributions “feel” better (and no – we don’t invest in a particular asset just because of its potential pay-out frequency and/or yield).

3. Personal well-being / growth: we spend a lot on personal fitness and well-being. I’m a huge fan of Orange Theory Fitness (OTF), as I found it motivates me and holds me accountable. I feel better, stronger, and more motivated, which equates to gains and personal dividends in other areas of my life. It’s not cheap, but I find the investment an effective use of my money.

Overall, I believe effective translates to having a productive and meaningful use of funds, allocated toward a specific purpose that offers meaningful return (in one way or another).

All great points! Congratulations on your financial success.

You said it well at the end of your article… “But you and I have different goals.” At this point in my life, paying off the mortgage is the right thing for our family.

Best of luck with the next steps in your journey!

Using that logic wouldn’t it have been better to do a 30 year loan instead of 15?

Yup :) He chimed in in the comments above that he had wished he done that instead.

Doh! I knew that I forgot to include something in the article! &^%!!!

My financial situation is close to about 50% split with mortgage-debt and assets. I have about a quarter-million on either side of that ledger. I don’t have the cash to pay it all off today, so I’m being patient about what I want to do in the future. Do I just let my 2, 30-year mortgages pay themselves off? Or do I rush the process and pay them off in 10 years when I can pay them off in one lump payment? It would be cool to see my rental property cash flow me $1,300 a month if it was paid off, rather than the $620 it cash flows me now with the mortgage. That would bring me a lot closer to financial independence. I see it from both sides, so I am just being patient and trying to listen to what God inspires me how to handle my personal situation.

I too side with the math. As you said, unless you cannot control yourself with spending, having “good debt” at a low interest rate is bennifical. I owe about $30k on a house that was appraised for $226k in 2012. I am not in a hurry to pay it off either.

Am I missing the part where capital gains taxes are taken into account? That $288k in an investment account isn’t going to be $288k after taxes unless you’ve also planned in advance to have an incredibly low income at the time you sell and end up in a bracket that is not assessed capital gains. But even LTCG is 15%, which is where most of that would likely be. Still ends up more than the mortgage payment, but that math should not be ignored.

Please don’t forget that past returns are not guarantees of future performance.

I have 29 years left on a relatively big 30 year mortgage (3.5% rate and I to get to itemize my deductions and get some of that back, though Donald may be impacting that soon). I would like to pay enough to make mine essentially a 15-year mortgage, but am holding off because I want the cash available to me.

Once my fixed expenses go down (i.e. my 2 younger kids exit daycare) I’ll probably be investing extra and paying the mortgage extra. There’s no magic math to know what’ll happen the next 10-15 years with the market. While over a 30-year period the market generally has gone up several percent, the same isn’t true for any random 5-10 year period.

Good point on the taxes!!

Even with long term capital gains (15%), I still come out way ahead. Also, by the time I sell these stocks, I’ll be under the capital gains threshold (something like $70,000 for a married couple), so I don’t plan on paying them at all.

You are a stronger man then I. I am sitting on a 2.85% mortgage and a 3% school debt and worry about both. I know I can make more in the market but am tempted to pay both off….well to each there own. You could also look at debt pay down as investing in bonds- a safer asset allocation….just saying…Then you could do 20% debt pay down and 80% index fund investing.

I have always enjoyed reading your discussion to not paying off the mortgage early. As I’ve said on your blog previously, I think you’ve made an excellent choice regarding your mortgage, and I would do the same thing if I were in your shoes. For us, October 19th will be one year since paying off our mortgage. While most things have not changed (still side hustling/saving/investing hard), some things have (more aggressive in my investing style and when certain people tell me to buy a bigger home I “LMFAO” in their faces). The thing I love about this discussion is either way you go, you can’t lose! You will either have an investment account with a considerable amount of money in it, or a mortgage free home.

Yup – there are much worse decisions you can be making in your life, haha…

For all 15-year S&P 500 return periods from 1871 to today, investing beat prepaying 98.9% of the time.

In the best case scenario, making your purchase in August of 1982 would have left you with an *extra* $1,790,263 at the end of 15 years because of the incredible 19.27% average annual returns over that 15 year run.

In the worst case scenario, making your purchase in October of 1929 would have left you worse off by $44,398.31. The average annual return for that 15 year run was 0.36%

Ultimately, investing vs prepaying is the same as any other kind of investing – it all comes down to your risk tolerance. I don’t think we can paint a picture where investing is better than prepaying for *everyone* (short of rates so low that the market is guaranteed to win).

If being $44,398 worse off is no big deal to you, then by all means, the upside of investing is incredible. If being $44,398 means you can’t afford to pay for your kids college or something else really important, then the conservative route may be better.

That’s why I take the stance that as long as you’re doing at least one of the two – making prepayments or investing, you’re at least headed in the right direction :)

I love how nerdy we all are here with #’s, haha… Thanks for running them against the time periods there :)

YES, I was waiting for someone to run the numbers! Chris, you’re my new favorite person in the world.

Sorry to be a party pooper. But that calculation vastly overestimates the probability of beating the mortgage. For example, in 1982 nobody would have given you a mortgage at 3.25%. That was the peak of the Volcker fight against inflation with mortgage rates around 20%. A fairer comparison would be to look at real (inflation-adjusted) equity returns and see when they beat a 1.25% real return (3.25% mortgage minus 2% expected inflation). Equities still outperform that 1.25% real return threshold over 15-year windows 90% of the time. No longer 99%.

But that’s still overstating the success rate. The point-to-point return over 15 years is less important than the sequence of returns. If there is a large enough drop early during the 15-year window you may still fall behind with the equity portfolio plus mortgage.

Totally fair point. I answered the question of how many periods beat out 3.25% but not what percentage beat current mortgage rates. Pretending that mortgage rates and market returns are completely independent certainly isn’t realistic. Thanks for pointing this out!

Hi Carl!

I wholeheartedly agree with all your points! Awesome post, as usual! And thanks for the mention and the compliment! I’m blushing here!

I once wrote a post asking whether debt is more like cigarettes (bad in any quantity) or alcohol (good for you in moderation, bad for you in excess). I think you and I agree that it’s the latter.

https://earlyretirementnow.com/2016/12/28/seven-reasons-in-defense-of-debt-and-leverage/

I would most definitely endorse investing over accelerated mortgage payments while still young and accumulating assets. Spreading out your equity investments more evenly reduces that dreaded sequence of return risk!

In retirement, though, the sequence risk impact is reversed. Not having a mortgage is a hedge against poor returns in the first few years of retirement. But, as usual with insurance, it’s gonna cost you on average. It’s really a tradeoff and depends on people’s risk aversion and flexibility in retirement.

ERN! I was hoping that you’d chime in! And I’m glad you brought up the sequence risk. I’ll mitigate that by having a little cash on hand once my wife stops working. So, having $30,000 would allow me to pay the mortgage for 2 years. Maybe I’m thinking about all of this too much?

That would work. One other option would be to a) have a $30k HELOC b) pay down the mortgage with the cash you have now.

Because the cash probably earns less than 3.25% (especially after tax) you “earn” the difference (carry) in return every year (tax-free!). If you need cash simply tap the HELOC. Probably the HELOC interest is higher than 3.25% (closer to 4.75%) but remember, you tap the HELOC only when you need it (maybe <20% probability) while you earn the carry with the mortgage vs. cash interest rate all the time!

The danger with this is (as you pointed out above): interest rates are on the rise. Maybe, eventually, your cash will earn 3.25% or more again!

Best of luck!

ERN

Thank you for validating my mortgage debt philosophy, Mr 1500. I totally understand the emotional side of having a house paid off. But I sleep just as well with a fast growing pile of other assets as well. Assuming they keep trending in that direction of course haha. To each their own!

I agree with this post 100%. I realize that there is no price for peace of mind with a paid off mortgage, but the numbers would say not to pay your house off almost every single time. I personally maintain no debt outside of our house, but we have not paid one extra cent towards our mortgage. At the end of the day, I’ll take the overwhelming statistically unlikely risk of my mortgage interest outpacing my investments. Plus, the flexibility associated with having that extra cash on hand has paid metaphorical dividends as well.

It’s not to say that everyone should have a mortgage though. If you are retired and on a fixed income, having a home that is paid for can be the difference between retirement success and retirement failure.

But as long as I’m working, I’ll pay off the house as the payments come due and not a minute earlier.

We have been in both camps on this one. We paid off our 15 year mortgage in 3 years, from 2010 to 2013.

It felt great. We invested so much (80%+ savings rates some months). We slept great, as others said.

But as the AA members teach us, this too would pass.

Everything reverts to the mean, and our debt-free euphoria wore off. Turns out, making decisions for emotional well being, at least in our case, ended up being short-term thinking.

After weighing the numbers and seeing that rates were low, we took a cash-out refi 30 year mortgage on the house, and re-invested the funds. (We’d definitely had been better off just not paying off the house, but this was still superior to leaving six figures tied up in the house indefinitely.)

And that’s the real opportunity cost that most folks don’t want to enter into the analysis. Keeping huge sums tied up in a house that pays no dividends and for which the gains can’t be tapped until you sell, for decades, has a pretty staggering cost.

With our new house, and new mortgage, our plan is (if we actually leave the workforce) is to leverage up one last time while we can…

Fascinating to see the contrasts here! Good for you for making moves when you realized a different route would have been better – that’s hard to do!

I treat mortgage debt as a bond allocation. After my emergency fund is set I have a choice bond or mortgage for the safe portion of my portfolio. Since this portion is all about piece of mind it makes logical sense to choose mortgage.

That makes sense!

I used to be in the firm pay off your mortgage camp but, in recent months, I have softened. One reason may be that I am finally eligible to attain a loan again (after putting 4 years distance between now and my last short sale) but it may also be that I now understand what your money invested can achieve. That being said, I am still struggling with a dilemma. Here it is:

I own one condo free and clear netting about $600/month profit. I now have my eyes on a seasonal (only open half the year) property that I may possibly pull the trigger and buy. It is super cheap (around 30k which is about 10% of my NW) but I can’t decided if I should get a loan or just buy the damn thing. I like the idea of keeping my money invested, however I HATE the idea of having a loan again. Maybe this is a good, small amount to rip off that bandaid. Decisions, decisions…

Maybe you should try out the loan so you can see both sides of it since you already have one paid off, and then see how you feel? If you love it you’re good, and if you hate it you can just pay it all off in one swoop :)

This is something I’ve always struggled with – I hate the feeling of being in debt, and worry about finding myself neck deep in a mortgage should something happen (job loss, etc.), but I know that it makes more financial sense to take advantage of opportunity cost. I compromise by splitting the difference – putting a large chunk towards investments but still putting a little extra towards my mortgage principal.

I’ll need to re-assess my situation next month – I’ll have topped up my emergency fund, and I’ll be getting a raise, so there will be more expendable income to work with. I already invest the equivalent of 20% of my gross income (10% from me into a Roth 401K, 10% employer match into a standard 401K). I need to decide what to do with the rest of my available funds: put more towards my 401K to take advantage of employer match, start an IRA, pay down my mortgage, or something completely different like saving for a down payment on a rental property. After reading your post, I’m inspired to run the numbers and see what makes the most sense!

It’s a good problem to have :) And with ANY of those options you list your wealth will grow, so congrats on getting to this point!

With our current house we have firmly been in the “we’re not paying an extra dime” camp, throwing all our excess cash into investments instead.

I’m still not sure what we’re going to do about the next home though. That is going to be a home we acquire early in our early retirement and I am somewhat tempted to avoid a mortgage to help protect us against the sequence-of-returns monster. The jury is still out though.

I have seen this argument many times and I come down on the investing side as well. I’m curious of your thoughts on what you will do come August 2028 when the mortgage is paid off? Considering that you’re already not working for money, do you refinance the house to invest more or do you go forward with lower monthly expenses? Does a cash out refinancing prior to payoff make more sense to invest sooner?I haven’t read much discussion regarding what to do at the end of a mortgage that wasn’t paid off early.

Oooh, thought provoking and scary. There are a lot of variable at play here, but cash out may be an idea. We’ve also thought about refinancing to a 30 year now. Dunno.

What I do know is I just totally punted on that one!

I’m torn… my house is paid off and yes that makes me sleep better at night. But then I look at the fact that i have $375k in home equity that is earning 0%! My house will appreciate regardless of having a mortgage or not. That money is not working for me. I guess it has not bugged me to the point that I want to go take a mortgage to invest though….

I love this. All debt is not evil. It can be a great tool to use to accomplish your goals. I have no interest in accelerating the payments on my 30 year fixed mortgage. One thing I am thinking about is to refi my 30 year into a 15 year mortgage with a better rate. I’m curious if the potential better rate may make the accelerated payment schedule worth it.

I live in a mortgage-free house, and the peace of mind is worth it to me. I think most people are in the don’t pay off your mortgage early camp. But I don’t think most people have the same amount of money invested, earning a bigger return. Instead of putting extra cash towards a mortgage, they’re spending it on their lifestyle. Mortgage payments can eat up an emergency fund really quickly during a job loss.

Yup, if you’re not going to be paying off your mortgage you better be using that extra money smartly in other areas! Can’t skip that second part or else you really get yourself into trouble :)

I was just discussing this topic with my partner. I have a bunch of different payoff variations on my FiRE spreadsheet. From paying it off in 3 years, to paying it off in 15. I’m leaning towards paying it off early, but really splitting the funds between mortgage and investing. Since I can’t really know what the “best” option is, hedging on both seems like a reasonable middle ground.

I really do like the idea of not having a mortgage during FiRE. As it means a downturn in the market means a less drastic effect, if I’m not taking out a mortgage payment during a loss.

And right now I’m most concerned with liquid cash flow until 59 1/2.

Appropriately used leverage is sensible. Debt is neither good nor bad. It just is. Knowing how you as an individual reacts and/or relates to debt is the more important matter.

We are in the process of deciding whether to pay off mortgage early or putting money in the market. We have $2000 extra per month that we can: 1) put all of them in the mortgage; or 2) put $1000 into mortgage and an extra $1000 into the market. Our mortgage is $223,000 with 27 years left, interest rate at $4.875%. If we put all $2000 extra each month into mortgage, we will pay off our house in 7 years as opposed to 11 years. However, after 7 years, we will be able to put all $3500 a month into the market, after another 4 years, we will have put $168000 into the market, with market rate of 10%, we will end up $188,160 extra. On other hand, if we put $1000 in the market while paying an extra $1000 a month into mortgage, after 11 years, we will have put $132,000 in the market, with market rate of 10%, we will end up $147,840 extra. Can someone help me point out where i go wrong in my calculation? Thanks, H

Also, this might not be the best place to put this comment, but I love this website and have learned so much from JMoney and other regular commenters such as Mr.1500, Mustard, Frugal Asian Finance, BITA,…so just want to give a sincere thanks to all of you.

– From a “ghost” regular visitor- frequently here but never comment.

H

Haha… I’m glad you’re enjoying it here, man :) And the other blogs too – they’re all great!

I’ll let others chime in with your dilemma up above, but I will say you’re doing a fantastic job to have $2,000 left over every month – that’s great! And any of those options will help grow your net worth so I’m a fan of whichever one excites you the most. That’s the option I always go down when I’m torn between routes – I pick the one that’s most fun for me at the time :) It’s not like you can’t always change routes later too, right?

Yes- I think I just want to get the math cleared out, since everyone talked about how much more money they will earn if they invest instead of pay off the mortgage early, but no one mentioned about if they pay off the house first and put the mortgage money into investment. And I’m glad that you answered! Thanks JMoney.

PS. We only save $2000 on normal months, although it is always a battle between should we save or should we travel every year—never seem to have enough money, new car, fix the lawn, new carpet…the joy of parenthood and ownership!

Just think of the additional benefits if one was paying ahead on their mortgage before maxing out all tax advantaged space (401k, IRA, HSA)! Once you factor in the tax benefits plus the investment returns the difference is dramatic.

I’m not clear on what you mean, so are your recommending paying ahead on the mortgage or maxing out tax advantaged space?

Max out tax advantaged space.

Interesting and timely article. I’m fairly new to this blog but learning a lot. I have a 30 year mortgage and I’m two years in. My home’s tax value has gone up $12000 in one year. I was of the mind to make more money to pay it off sooner but now, maybe a home equity line of credit to invest??? Thanks for presenting another point of view.

I’m with the math. As others have pointed out:

1. The S&P 500 historically grows at an annualized rate of close to 10% (with dividends reinvested).

2. If you have a fixed-rate mortgage at 3 or 4%, you come out way ahead by investing the money.

3. If you factor in taxes (the mortgage interest deduction, as well as preferential rates for long-term capital gains – or even better if the money is in a tax-advantaged account like a Roth IRA), the benefit of holding the mortgage debt is, in the long run, enormous.

4. If you factor in inflation, and at least theoretically, the value of your debt shrinks over time.

The only caveat would be that one must have the discipline to invest the extra money consistently. But if that discipline’s there, I’d much rather invest the money than pay off the mortgage.

Very interesting look at an “asset” when most people do not have a clue about the true carrying cost.

Most would only consider their 3.5% mortgage, when they probably had another 2% in property taxes, .5% insurance and repair & maintenance of 1-2%. Total carrying cost 7 to 8%.

Consider what a couple in their 50s, who are empty nesters, might be able to generate for their retirement if they downsized their home, invested their equity and their monthly housing savings into their 70s. I understanding the fear of being thrown out on the street, but I too agree that a pile of money would soften the landing.

Yup, owning a home is no joke! I was one of “those” people who only factored in the mortgage when buying our first – and only – house years ago… Home ownership is quite the commitment! :)

Ah yes, the classic mortgage versus investing debate. I’ve personally taken a hatred towards debt, but that is probably because we are trying to knock out the remaining balance of my wife’s 401(k) while I just purchased a home. So I saw my balance sheet get turned upside down compared to my very liquid, investing heavy balance sheet. That being said, I’m aggressively paying of the high interest rate student debt so that only have a mortgage loan and car loans left.

That being said, once I only have a mortgage remaining, my decision to invest or pay-down my debt will change drastically. I have a fixed 3.89% mortgage. As you show, that will become very low in a rising interest rate environment. Sure I’ll make some extra payments here or there, but I want to play offense and increase my portfolio at that point just as much as I am going to want to play defense and see my debt load decrease. I hear the peace of mind argument that you suggested in your post, but I will also have peace of mind from a very large portfolio with a fixed rate mortgage that is well below the current interest rate environment.

Bert