I got this email from a friend, so of course I had to check it out :)

There’s no real point in comparing your own wealth to someone else’s, but of course it’s a fun way to waste a few minutes on a Monday :) And who knows – maybe you’ll get a boost of confidence from it? We’re usually a lot more well off than we think we are, unless your name is Nate St. Pierre.

(I got his permission to share this with you FYI – I’m not that mean ;) He says that philanthropy doesn’t pay well, and I remember from when we ran Love Drop together. Great dude who follows passion over $$$, for the better or the worse… He also once fooled the internet into thinking Abraham Lincoln invented Facebook, but that’s for another day.)

Anyways, here’s the calculator: Wealthometer.org

You just have to enter four things – which most of you nerds will know off the top of your head:

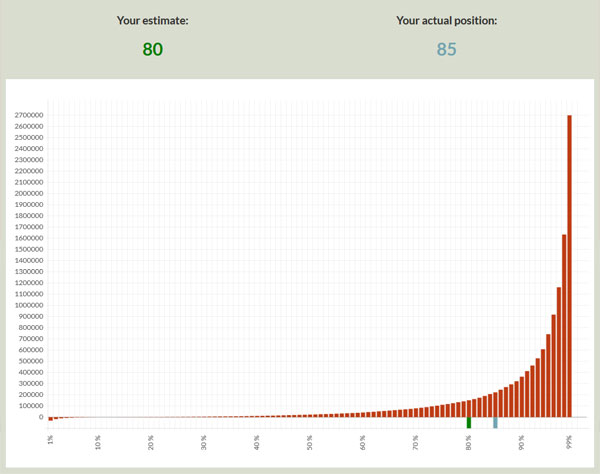

- How wealthy you think you are (I put down 80%)

- Total amount of “real” assets (home, vehicles, etc – I put down $306,000)

- Total amount of “financial” assets (savings, 401k, etc – I put down $475,000)

- Total debt (I put down $292,000 – our mortgages)

- And the number of people in your household (I put 2 because babies don’t count, right?)

If you track your net worth, you’ll find these numbers there too. Or you can just guess, doesn’t matter.

Here’s where I landed compared to others in the U.S.:

“Your wealth is $244,500 per household member, which is more than what 85% of the US population own (blue bar). This means that 85% of US residents are less wealthy than you. At 80% a green bar at $151,244 marks your initial estimate.”

85% – I was close! You’ll notice “the 1%” (ie 99%) is in the $2,700,000 range. That’s quite a stretch from 14% lower at $244,500! I don’t think that’s a game I want to try and beat, haha…

You’ll also notice that you can still have debt (or, as my friend Maria prefers to put it, “negative wealth“) and be better off than others too. It just depends on how much debt you have. You might have been wealthier as a baby, but you know – life happens ;)

The calculator then goes on to account for some other fascinating stuff like taxes, but sadly I wasn’t smart enough to continue. If it were mine, I’d have chosen to incorporate a few different variables instead. Such as:

- The level of what you plan on doing about it. (“Don’t give a $hit” all the way up to “I’m a hustla, I’m a, I’m a, I’m a Hustla!”)

- A place to choose what phase of life you’re in (“graduating with tons of debt,” “starting a family and babies eating all my money,” “Old, gray, and how do I use this mouse again?”)

- And of course, the amount you need to reach financial freedom. AKA early retirement. AKA the only thing that actually matters with money.

This would paint a much better – and blogworthy – picture, spitting stuff out like:

“Everyone may be wealthier than you, but you just graduated college and are a hustla, hustla, hustla baby! Unlike those older than you who don’t give a $hit…”

or

“Congrats! You’re worth $2 million dollars and better than 98% of everyone! But guess what? You’re old and forgot to have a life. Why don’t you stop working already?”

or, less drastic

“You’re as average as they get at 50% w/ your (maybe) affordable house and 2.3 kids, but you sure are living life, right? RIGHT? Who doesn’t want to be average? (RIGHT?)”

You could have a lot of fun pumping these out ;) And I bet people would pass it around the internets much faster too… Hell – anyone know of any good developers? I’ll jot this down right below my “where the hell is your podcast?” note on my big list of ideas, d’oh.

But, back to the point… which is….

Oh, yes. It’s fun to see where you rank amongst other fine Americans, Greeks, Italians and others you can compare with in this calculator, but at the end of the day what matters most is what it means to YOU. Does it make you happy? Stressed? Pissed? What are you going to do about it? What’s one thing you can start today to get you a tiny step closer to your goals?

I’ll offer up 3 if you can’t think of any:

- Walk into HR right now and increase your 401(k) percentage by 1%. You won’t notice it, and your money will grow like the dickens (if you don’t know what funds to put it in, check out my review of Smart401k – it’s free (for you))

- When you get home tonight stay away from the TV and instead spend one hour brainstorming ways to make extra money. If you already do that because you’re a rock star like that, then go around the house and find something to sell on Craigslist/eBay instead. That should only take you 20 minutes.

- Find the bill that pisses you off the most and call them up and ask if there’s anything you can do to lower it. Literally just ask them that and see what they say. If they say nothing, ask for a manager. If the manager says nothing, hang up and call the next worst expense on the list ;)

- *BONUS* If you really want to be on fire, create a spankin’ new spreadsheet and list out every single debt you have – including balances, %’s, due dates, etc, then create a new tab and put down all your bank/investment balances, and lastly a third tab labeled “net worth” where you subtract your total debts from your total assets to see where you’re at. Going forward, add anything – and EVERYTHING! – to this sheet relating to money!! You can put down account info, goals, dreams, random calculations that turn you on – whatev. You’ll be amazed at what happens once you see it all in one spot. I’ll make y’all a template later if you want me to, but start jotting stuff down today.

Okay, I’m off to the beach now to make some sand dollars castles with my boys… I’m supposed to be on vacation, but couldn’t lock down my tasks ahead of time so here I am typing to you :) While my $$$ is in the 85th percentile, my work habits are leaning towards that old man w/ the $2 mil… And I definitely don’t want to be that old man with the $2 mil.

So *my* task today is to shut down the computer for a while and appreciate the stuff money gets you. Like hanging out with humans you love. I’ll be back later to see how you guys fair on this thing.

Here’s the calculator again: wealthometer.org

Share below and we shall discuss!

UPDATE: Fellow reader Gene Roberts found this calculator too which is neat: shnugi.com/networth-percentile-calculator. It uses more current stats, as well as an option to compare net worths by age range :) This one put me at 82% of the general population, and 94% of those my same age.

Get blog posts automatically emailed to you!

Interesting website, I underestimated my wealth by a bit but I was still pretty far down in the chart. Ended up around the 30%, but I think it would be more useful to see this broken down by age like you said. Comparing myself to those that have had years of working and saving head start isn’t the best gauge.

I do plan on getting two more car insurance quotes tonight and hoping that I can lower that amount :)

Smart! It’s amazing how drastic insurance can be sometimes. Good to call around since it would mean savings *every month* for quite a while! Especially since most of us don’t ever go back and check on it here and then ;)

I estimated 70% and my actual was 68%. I think it’s awesome that I was able to come so close, which to me means that I have a good idea of what my net worth is and how that compares to the rest of the population. I don’t think I would have been anywhere near as close with my estimate a year ago. I feel good about how much I have learned about finances in the last few years.

Congrats! Tracking your net worth does wonders, doesn’t it? One of the best things you can do for your money (and your brain!).

Hey, I have to share my wealth with my kids?? They can’t even work yet : ) Even with the kids we are pretty high so I shouldn’t complain.

Sounds like a beautiful life :)

I hadn’t really put much thought into my guess of 9% (should’ve know a little better than that).

But I was shocked my actual was 93%.

I suddenly have stronger opinions on capital gains and off-shore accounts. :)

JK. Warren Buffet for President.

Haha… WB for P indeed.

My favorite part of your post was reading the three things the wealth meter could have spat out had it accounted for more variables. Any chance you’d take a crack at what it should of said for you?

It would have said:

“You’re a hustla! You’re a, you’re a, you’re a hustla! But good thing you have kids cuz now you’ll slow the eff down and realize there’s more to life than money. Also, stop pretending like you’re so close to early retirement when you’re still a million+ off, you dummy.”

I think it needs some fine-tuning still ;)

Pretty neat little tool there. I read your post first so threw in a number of 85 as an estimate…came up with 89%.

I’ve been needing something to fuel my liberal guilt…

Hah

That was interesting! I wish I could calculate my own numbers as well, but I live in Europe, so it makes it harder to do. But I made some estimates and it was fun :)

We’ll have to tell them they need to expand ;)

I did my score, I guessed a 60 and got a 62 so not too shabby

I estimated 91% and came in at 93%. Pension funds are hard to calculate. I put down the amount that is in there, if I took it as a lump sum. Paid over my lifetime,however it should come out to much more.

Pensions! What are those? :)

Mine said “Do you have a rich uncle? No? Better sell a few of those kids…”

Actually, its not quite so bleak..but it definitely motivates me to earn a few more bucks this week!

HAH! I *wish* it pumped back real talk like that ;) We all need a good push every now and then!

What a neat idea. I like it, but I probably won’t try it as I don’t want to see my dismal numbers, haha. :)

Divided by the number of family members!? That is weak sauce…just over 50.

time to put your kids to work :)

I have no idea how we end up at 76% on my income and unsteady freelance income. We don’t even own a home.

maybe that’s exactly why – you don’t own a home! no upkeep, mortgage, etc ;)

Cool tool. My guess came in pretty much spot on.

Too bad it doesn’t stratify you by age bracket.

Guessed 12%, actually made it to 50%. That’s awesome for me. Shows I’ve been making progress.

Either that, or everyone else in the country is slackin’!

(let’s go with your answer though :))

This is fun (in fact, I’m late getting ready to go to the gym because of you :)). I under-estimated by about two percent. (And I filled it in £s rather than $s). I’m not going to share the number but it is embarrasing in a good kind of way. Still, I’m much older than you, kids….:)

Way to go 1%! ;)

Well, my dear; you are several points out ;).

I like the suggestions. I actually negotiated a lower bill recently. Never did that before in my life. Received a $560 bill for 15 minutes of pathology related to a skin cancer removal. Insurance wouldn’t pay any of it saying it was out of network. No one ever told me it was out of network. It took 4 months but my persistence paid off. They cut the bill down to $280. A 50% reduction. You don’t know till you try!

There you go! Especially with medical bills – they know exactly what they’re doing and that it’s all negotiable if you call and pester them. The whole thing’s a racket.

I thought I would be below 10% because I don’t make a lot of money but I have no debt so I scored 55%. That just goes to show you, people who probably make 2,3,4 times more than me can be riddled with (bad) debt.

Indeed! Debt is the silent wealth killer!

(ooooh I need to trademark that)

I estimated 70, came back at 78, of course it does help that it’s just me. :) if I had to share my numbers with a dependent or two, then I probably wouldn’t be as happy with the number.

I was dead on at 45%. What makes me happy about that is that I know exactly where I am…no surprises.

YES! Great takeaway!

Guessed 70, came in at 97!! I don’t live in the US but in Europe though, so possibly not really an exact comparison? …

PS I did a currency conversion. :(

Awwwww

hi J. Money! … thanks but why “awwww”? Isn’t 97 good?? … :( I was not at all expecting it myself and my immediate thought was “That can’t be true – are the rest of them broke?” …

Oh, I thought you did the currency conversion and your # was lowered or something.

Yes – 97 is incredible!!! Of course! And yes, it also means the rest of the country is not doing as well :(

no sorry, I’m just failing to express myself clearly! I don’t live in the US, as I said, so I translated my net wealth into US dollars using a currency converter then ran it through the wealthometer. At which point it said 97. I must admit I thought 70 was optimistic!

The data that the wealthometer is based on is from 2010. I found another site that has similar calculations based on the same data source but from 2013 surveys.

http://www.shnugi.com/networth-percentile-calculator/

I drop from 93 on the wealthometer to the 83rd percentile on the shnugi site.

You can also select a specific age group to compare yourself to.

Nice find.

I’m at 82% on that one compared to the majority, and then 94% for just my age.

Thanks for sharing :)

Yes I drop too, to just over 92. Still pleased!

Its a cool tool, but your kids should not go into the calculation, because per person division is not a real representation of where you are financially. In retirement you can gift your kids some money for estate purposes, but calculating your stance per person today is off to me. When your gone it gets divided by person at that point. Morbid I know but realistic.

I didn’t include my kids when calculating it – just my wife. It would be better if they explained it a bit to clarify, but oh well. Still fun to take :)

I guessed 80% since I knew I was a little behind you anyway, but apparently we’re at 84%. This doesn’t make me as happy for us as it makes me sort of depressed for 83% of the rest of us…

Yes, that is the downside here. In life – and the world – in general :(

J$,

I’m glad I’m not worth less than a baby anymore. I guess it helps I can feed myself without crying for food. Thanks for the mention! :)

Always good to run these types of calculations for a little perspective. Easy to get lost in the noise when you read all these financial sites where a lot of us are socking away thousands of dollars every month. The average person just isn’t doing that.

I also like globalrichlist.com. Even better perspective, in my opinion, because it includes the world.

Best regards!

Now if only you can come over here and teach my real baby how to do that :)

I estimated 85% Came in at 95%. Only me in the household. Tracking the right way!

Nice!

98%. Can I out my 2 kids on CL? :)

Hah!

Well, my numbers are way off. Good thing I like living in the now than beating my head over saving every cent. However, my play time is somewhat over. We are buckling down to live the life we want before we retire – thanks to you! And Go Curry Cracker. Now with 4 kids, my early retirement puts me at around 60 yrs if I’m lucky. But until then, we decided to move to our ‘retirement’ destinations through our jobs. We homeschool the kids which allows us to take off season long vacations (and pretend we are retired) meanwhile make sure we don’t accumulate more debt (and we’ve been good at this for the last 5 years -whew!). Hoping to have a few 3 month long vacations in our future to check off that bucket list, while living in our ‘retirement’ destination dream location. And maybe then, working til we are 60 yrs won’t feel so bad. Thanks again for sharing the wealth of knowledge.

I LOVE THAT!!! Such a great idea with moving there sooner than later, that’s awesome. No shame in working even when you don’t have to either as long as that’s how you enjoy spending your time :) I don’t think I’ve gone on a vacation for more than 10 days since graduating college haha… Great goals to have!

I liked that a lot. I did not know how that was going to be figured, and our income is nothing to get excited about. I guessed us to be 43 percentile but we are 70! I feel a bit rich :D

And if it were compared to the *world* vs just the country, you would most certainly be rich! :)

This was fun but the best part was spotting a challenge requiring so little effort. Upped it 2%. Thanks for the mid-year push.

Great idea :)

I gave myself a 75 and it gave me a 72… :( better start earning and investing more!

Interesting Blog. Fun way to keep your mind out of work for few minutes and feel good about yourself. It’s a fun way to see your financial stand and appreciate what you do.

Too good to be true! I got 80% in this. But my son is only two, and i am still in my early thirties. What could be the implication if it was true?

it sounds like you’re on a damn good path is what it means :)

Great article and thanks for sharing. I love the direct action on how to increase your wealth. You are absolutely right, if you brainstorm ways to make money, you will stumble on ways really fast. Heck, that Xbox, etc. may look great on your shelf, but if it is collecting dust, then maybe it is time to move it along. Turn that dust collector into cold hard cash which will eventually turn into an income producing asset.

I agree with another point you made, there really isn’t any point in comparing your results to others. What benefit does that get you, none. Seeing there rate sure as hell won’t improve yours. If you want to make the most of this tool, you compare your results against yourself and find ways to make yourself better. Use your results, learn from them, and find ways to improve. Pick up some ideas from others who are more successful and see if they will improve your wealth. Sorry for the mini rant over here haha

Great post and hopefully others learn something new like I have today and find a new way to reach financial freedom sooner. Have a great weekend!

Bert, One of the Dividend Diplomats

Thanks for stopping by, Bert – love seeing others’ opinions whether they agree with me or not :) Cool blog name too – going now to check it out.

J$!! I work in HR and I can assure you we don’t have time to be messing around with your 401(k) percentages. Act like a grownup and activate your 401(k) online account and fix your contribution percentages there. That way you can track your $ after each pay, too :)

Hah – yes, that works too. But for those who suck at 401k stuff, I doubt they even know you can do it online or what their passwords are/etc. Hopefully when they get to HR y’all will school them so they don’t need to come back! :)

Wow, definitely gives some perspective. I guessed we would be around 58 percentile, but came back at 60 percentile. We are aggressively paying off our student loans and will be done with about 2 years. So once that is gone, it looks like we would move to the 71 percentile.

Rock on! Helluva good goal to work on!

I estimated 10 because I figured, I don’t have much saved other than my 401k and we just bought a house last year so I thought the mortgage would drag us down. Turns out, I am at 46%!!! Way better than I estimated!! That pretty much means I’m literally in the middle, half have more than me, half has less. That makes me feel good, since I’m usually struggling to make the budget work, that I am actually doing better than I thought compared to the rest of America. I was surprised to see that 10 means having -$564. Negative money! That means everyone under ten percent has more debt than money…..That makes me feel pretty good about where I’m at :)

I’m glad :) Though def. sad such a large population has negative wealth! Millions and millions of people – freaky!

Why are they asking about taxing wealth?

It takes a lot of effort and planing to accumalate wealth.

Why do I owe it to anyone?

Taxing income from wealth is a different matter.