I don’t know about you, but sometimes I get down on myself and wonder where the hell all my money’s going each month. I know we’re doing well overall and can just peek at our net worth to make myself feel better whenever I’m down (another pro to tracking your stuff!), but in the instant it really only helps so much.

How can we blow through over $5,500 a month??? Where does it all go??

I look back to the way things were 4-5 years ago, and the old me then would have vomited at the site of a $6k monthly bill :( And that’s with a ton of partying and shopping and Lord knows what else I was dishing it all out for then too!

But times change, and as we get older it seems like we’re doing all kinds of more practical and smarter stuff ;) Things like investing, buying homes, setting aside emergency funds, college tuition for our babies, etc, etc. Pretty much all the responsibilities we left for “later” back in the day, haha… And obviously all this is mostly for the good, of course (I’d never return Baby Money!!), but the fact still remains that life becomes expensive over time.

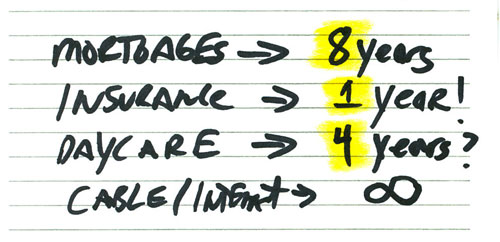

So in an attempt to calm my current – and future – noxiousness, I have written down the 4 main budget busters we’ve got going on along with the dates when they will possibly go bye-bye forever. It only covers about 2/3 of our monthly expenses (the other 1/3 I’m okay with!), but it’s the chunks that get in my way and frustrate me the most.

Here’s what it looks like:

Notice that I didn’t put the amounts of each up there ;) I’m trying to MOTIVATE myself not depress!! Haha… Now it doesn’t include any of our savings or investments/etc (those things we aren’t going to change in the near future), but it *does* help put our most expensive bills in context knowing they’re not going to be super permanent. Except for the cable/internet section which I kinda need ;)

Here are the details on each category:

- Mortgages @ $2,000’ish/mo. — It’s been a slowwwwwwwwwww process as it needs to be, but at the rate we’re going paying down extra (*if* that keeps up), it’ll take us 8 more years to pay it all off completely. Down from the rough 10 it was when we started this mortgage killing a while back. And even if we hit pause for a bit, the second I land a windfall and/or sell a site of mine for hundreds of thousands, you can bet this guy will go away in a heart beat ;)

- Insurance @ $643/mo — Being self-employed can be a bitch. Granted it can all be written off – even the portion that’s for Baby $, which I just recently learned! – but nonetheless it’s still a chunk of money out of my pocket each and every month. The plan here is for the Mrs. to re-enter the work force again once she’s done writing her dissertation (which we approximate to take about a year), at which point we’ll move everything over to her plan. With the caveat being, of course, that she HAS one ;) And a cheaper one at that.

- Day care @ $500/mo — This part’s more depressing. Not that we have any right to complain all the way yet since we’re paying pennies compared to what it would at FULL-TIME (we pay $500 for super part time care (1 day a week), compared to $2,000ish at 5 days a week!), but still – it sucks. That’s a nice car payment right there! And I put down “4 years” just cuz I have no idea how long they do daycare for, or where we’ll be in a few years/etc… If we end up moving closer to home, perhaps this could be wiped away altogether?

- Cable/Internet/Phone @ $200/mo — The 4th largest bill we get a month. But really not as much we can do there unless we get rid of cable (hah!) or the internet (double hah!) or even our home line. Which we need no matter what as our cells don’t always get the best reception in our house, not to mention the need to up our minutes even more if we nixed the land line thereby erasing the point of it. But really this bill I’m okay with in comparison to the others at least. I could live with our cable bill taking the #1 spot in expenses come 10 years from now :)

All this to say that we’ll always have *something* to be worked on when it comes to money, but hopefully as time goes on it’s more in the “savings” department than it is “expenses.” As much as that’s possible, at least. It’s just about being comfortable with everything and knowing there’s a PLAN in the works so you don’t drive yourself cRaZy trying to reach that end goal like I do!

We’ll see if this new motivational note helps me or not, but regardless I’m pushing forward… How does that saying go? I’ve got 99 problems but a Budget ain’t one? ;)

What are your top annoying bills? How do you calm yourself down from budget freak outs? Share your tips below so we can all learn from each other!

——————

{Photo by Enokson / Edited by J$}

Get blog posts automatically emailed to you!

My top four are rent, all things car related, food, and day-trips. I’m actually a little bit surprised that something that I actually like spending money on made the list. Although this means that I spend a considerable amount of time berating myself for having fun.

haha yeah! that’s awesome though – I like that day-trips made it in :)

My HELOC debt is the number one thing on my hit list and I have estimated just over 1 year to kill it then I will have money to start saving for retirement.

4 more years of day care? Don’t forget before and after school care and all of the holidays. 1 of my coworkers has 3 young school age children but they still require a sitter for the summer. Mom’s pay covers the cost of the summer sitter but she makes no money the weeks they are in care. She and her husband take some of their vacation separately to save on paying day care for 3 weeks in the summer.

(are you trying to depress me? :))

Great perspective, but I find it short sighted. I would have thought you would have big expenses relating to future goals. I haven’t truly checked out my most expensive money suckers but I’m pretty sure it involves food, vacations, car (maintenance and insurance), and cellphones. However, looking to upgrade our home is going to be a big money sucker…

well two of the four are goals – get rid of mortgage and stop paying such high insurance. we get those two nixed and we’re looking good!

How do I calm myself after budget freak outs? I go shopping. Ha. Just kidding. I am throwing all my cash in my mortgage right now. I can’t wait until I can say adios to that monthly bill. $2,000 for full time day care. That’s crazy. Is that standard in your area. I just can’t imagine!

yup, standard here – and we don’t even live downtown!

way to go on all that mortgage killing you’re doing over there too – you’ll probably beat me :)

Our top annoying bill is my fiancee’s student loans. We just did an update today on my blog and we’re down to under 55k owed so that is a big step for us! Unfortunately, it doesn’t feel like they’re going away fast enough! Hopefully they’re gone by the end of 2016 or earlier!

We feel your pain on the student loans Lance! Any amount feels like too much… Stupid debt!

On the plus side, time goes by reallllly fast these days so in a while we’ll be seeing a “ALL OUR STUDENT DEBT IS GONE!” announcement from y’all :) I’m gonna remember this conversation – you wait.

Mortgage, mortgage, mortgage…as soon as we’ve killed that beast off, our financial flexibility greatly increases.

I know!!! It’ll be a glorious day, my friend!!

We thankfully got rid of our most annoying bills over the last year or so…my student loans and our car loan. It feels so good to be free of those. Those were replace though by my new most annoying bill. Well, to be fair, it’s not a bill yet it’s still annoying – estimated taxes. We just sent ours out on Saturday. I know, it means we made money…but man does sending that check out hurt.

Agreed! Makes you stop to think about it all though, eh? Unlike at a 9-5 when it’s all automated and you don’t feel it as much (I mean, it still sucks there, but it’s much different than writing out a physical check for a massive amount! Bleh)

Just a “heads up”..it gets no better as you get older. I share your pain as I look at the monthly “ebbb and flow” and it can be depressing. Will tell you as you get older the prescription drugs will be a game changer…My dear parents recently have experienced dramatic changes in their insurance coverage concerning prescription drugs. Their plan used to be “stellar”…now not so much. I also share your pain with the cost of health insurance…it is just crazy and seems to cover less and less. It also seems that the “battle” to hold down costs is on all fronts now….just got notices from landline provider…internet/cable tv provider…electric provider….newspapers and magazine….municipal water supplier… that their charges are going up. I deal with it by controling what I can and to focus on the positive…

oh man, aren’t you right. good job on the staying positive front – it’s the best thing we can do! (besides watching our money too, of course)

The one that irks me in terms of the bills is the water bill. I lived in a condo where water was included as part of our monthly association, so when I had to start paying that by myself, combined with the fact that our city is among the highest charged in the region (stupid hills) it just irks me to have to pay that bill every two months.

that sucks :( at least it shouldn’t be *too* big right? Like not a cable bill or insurance or anything? or is it?

Daycare…. at $255/week it really sucks. Other than that nothing really seem that bad!

well that’s good all in all!

Cable’s #1 for me. We’re going to get out from under that one sooner or later. I feel like I’m paying $100 for someone to dump a load of garbage on my front lawn each month!

haha… for years and years and years too! :)

Student loans here, too. I cannot WAIT to pay those jokers off!!

Sallie Mae owns my soul

My top money sucker currently are my student loans. I’m paying around $5,000 or $6,000 a month because I want them GONE!

woah, you are hardcore! I love it!!

damn michelle that is huge…

Interesting. I have a smart phone that enables wireless calling. That is why I do not have a land line. Would cutting out the land line soften the bill enough to spend $$ on a newer phone if your current one does not have this feature? also calls made via the wireless feature do NOT rack up your minutes.

well that’s cool! hadn’t really researched that route much, but if my service is spotty on my smart phone wouldn’t that still affect the wireless feature?

Mortgage, HELOC, kids sports and activities, food are where most of our money goes. Paying $125 per day for daycare is A LOT – good thing you’re so happy with them! Going rate is usually $45 per day here.

I know – it blows :( Hopefully wherever we move it’ll be much more normal!

My biggest bills are lot rent, savings, school and (soon to add category) investments. My internet bill got cut in half by calling customer service, and cell phone is prepaid plan with minutes only. I only have basic bills like food, gas, electricity; I don’t have cable or other not needed things. I can’t say any of my bills freak me out because I don’t spend a lot of money on them.

However, if I look at the full amount I will be spending on school it freaks me out (bachelor’s plus master’s). When I freak out, I talk about our budget with Mr. FBS and he tells me how stupid I am (not really haha). He actually talks me down from my budget freak out by telling me I want to go to school no matter what, so I should just look at each day and what I am accomplishing instead of the full bill. That usually works, until I get stressed out by school and I think of how much I could be investing instead of paying for school.

haha…. he’s def right though – you’re gonna be SO WELL OFF once you have that degree for the rest of your life! it’ll more than make up for it so keep on truckin’ my dear!

I guess my biggest monthly expense is gas at $250 to $350 a month. We have a paid for house, we have never had cable. When our child was young, I only worked one day a week so day care was not high, and when he got older, I worked from home. We are now a one income family with just my husband working. We are blessed with low cost insurance from my husband’s job. It is awesome being debt free. I love your blog.

thanks! I love how well you guys are dealing with your finances over there – a paid off house is incredible – way to go! come by and say hi more often :)

PS And by the way, congratulations on paying down on your mortgage. That is awesome. We saved $140,000 in interest by doing this.

Wow, you pay a lot for daycare! Do you live in a higher cost area? Our two biggest expenses are the rent and food costs. Things would be so much cheaper if we didn’t have to eat LOL>

haha for sure. and yup – we live in the DC area which is just insane with cost of living.

By far our biggest expense right now is the mortgage, but we are dumping half our income on it each month (by choice) to pay it off about 23 years early!!!

After that is gone (next year?) our biggest expenses will be property taxes and food.

Yayyyyyyyyyy!!! GO YOU!

Worst Bills I have are utilities (130 a month), car insurance (80 a month) for a car I drive about 1000 miles a year, and gym membership (60 a month) for a gym i use but not as much as I would like to!

not too bad at all, way to be killin’ it over there.

Well. I am killing it, but if things go the way they are, I am about to inherit a lot of debt from my gf (fml #studentloans)

Yikes! I guess she’s worth it though? :)

For me, they’re

1. Student loans

2. Rent

3. Food (Hard as I try, it’s always tough for a single guy)

4. Transit (Though I’m glad that I have no car payments, insurance, or gas to pay for)

I’d say mortgages too, but I’m getting rental income that covers that. Also, my credit card bills aren’t very high, but I am paying more each month to those than anything else to knock them out as quickly as possible.

nice! I’ll be learning all about rental income too here in the next few months once we move – all exciting (and scary) stuff. but stuff that will help with future endeavors!

Being that we don’t have kids yet and work for large companies, 2 of your 4 don’t pertain to us. Our top 4 bills each month are the mortgage (which we don’t currently have a plan to pay it off), loan payments (will be done in the next few months, woo!), utilities (which will go on forever) and food for the month (will will also go on forever).

the going on forever parts are freaky, aren’t they? :)

Our largest bill is also housing, at $1325. Of course, we have to housemates and my mother-in-law works “from home” at our house, so we are actually only paying half that ourselves.

Car payments are about $240/month, but that will be paid off in 18 days!

Third is groceries, currently at about $250/month.

Utilities eat up most of the remainder of our monthly costs, coming in around $300 for electricity, water, sewer, gas, satellite, internet, and 2 cell phones.

For $2000 per month, I’d quit my job and be a stay-at-home dad. I only made about $1000 more than that last year!

Awesome on your car payments almost being gone!! I swear it feels like they just started up?? Time goes by f-a-s-t boy, whew.

My four biggest money suckers are 1) Mortgage – though I can’t argue with the amount at around $700/month, 2) Private School Tuition and After School Care – about $300/month, 3) Gas – it’s so expensive now at around $250/month!, and 4) 401K at about $225/month for my contribution. But I can’t complain because my company matches the first 7% at 100% and puts in an additional 4% of my salary too! Gotta love free money!

hell yeah!! I’m about to write a post on my love for 401ks too – damn good free money!

My top money bill is probably eating out and we only go out once a week. We need to relax and try new food though. I’m not going to cut that out.

I hated paying for daycare when our kid went. Your location is super expensive, sorry about that.

Next year I’m thinking about finding a co-opt preschool. It will be affordable and I’ll have a bit more time to work.

Top is mortgage, second is daycare (Full-time), then cell phone bill. The others are Ok, but I am not a fan of paying that much for my cell phone. I know daycare is not permanent, but it will be for quite some time. That is a lot of money.

Daycare at $800 a month is our largest, most annoying expense. Twice my mortgage (live in the south, bought a cheap foreclosure)! Food is our second largest expense, I don’t know why we can’t get this under control! Next would be health insurance, followed by TV/internet. Going to cancel TV package soon and just stick with Hulu and Netflix.

man, isn’t that crazy??? double your mortgage for daycare?? Jeesh…

It is beyond awesome when one of those huge bills goes away. Our daycare bill was gone when my youngest started Kinder last fall…but we will have to pay it for both over the summer. Just made our last car payment last month too.

congrats! lots of nice financial changes going on over there :) gotta feel good!

Mortgages, Food, Saving for Adoption, Baby Stuff………..i’d love to get those mortgages knocked out but that isn’t happening any time soon. :(

adoption can’t be cheap either :( but at least the payoff is well worth it!

Mortgage is above and beyond everything else. Well, mortgage and condo association cost combined. Right now am on track to pay down in 20 years instead of 30, but in reality have a savings account I am trying to grow so w/in the next 5-10 years I could pay the whole thing off if I wanted to.

that would be quite the feeling! knowing you can pay it all off anytime you want – I like that. a lot.

Time to eliminate the mortgage! Seems like that will free up the most money so you can build wealth quickly. What a free feeling it is!

workin’ on it ;)

I’m still in school (well, between undergrad and grad) and completely unattached, so my expenses are still pretty low. Rent doesn’t make it on the list, as I own/manage a condo and the rent I charge covers my mortgage payments. I just moved back home so I’ll have some rent to pay but it’s still minimal. I think she is going to charge me $200/month for rent + food, haha… a slammin’ deal considering I usually spend about $100 on groceries anyway. My biggest expense by far is food though — eating out. Doesn’t help that I LOVE to do it. However, I will say I don’t go out to eat unless I’m with a friend – if I have no plans I usually just go with something quick at home. I categorize coffee + coffeeshops under “eating out” in my budget though, and that makes up a pretty hefty portion of it too (and will even more since I quit my Starbucks job).

Next on the list besides Eating Out, would probably be my phone (ew). I know it’s not bad compared to others, but I recently switched to a smartphone from a pre-paid so I’m still adjusting to the change. It’s super convenient though, and I love it. But that’s a leap from about $25/month to about $80.

Last on my list… massages. I get one about every 4 weeks, and they’re usually about $80/hour once I factor in tip. Yes, extremely expensive but worth it in my book. I could find cheaper alternatives, and might soon. I’ve stuck with one local company just because when I started with them, there was a therapist that I clicked with and whose style I really liked. She has left but I’m still with them… the other therapists are good too, but none as good as her! :(

Well you threw me for a loop on that last one! Haha… but if massages are in your top 3 money suckers, then by all means enjoy every last one! Man, you are ROCKIN’ the living situation and have your expenses crazy low – good for you… You should start a finance blog ;)

Mortgage is definitely our biggest money “sucker”, then property taxes ugg. No kids yet so childcare isn’t a part of the equation (thank goodness given the expense).

My top money bill is my friends. I love them, but they aren’t the most frugal people every and always want to do something to spend money, and because I love them, I let it happen.

HAH! Not a bad thing to spend money on though :) I miss my group of friends :(

Right now our mortgage is coming in at just under $1000 a month plus we put an extra $417 or 5k a year on it. Since we will aim to pay our mortgage off in full in early May and hopefully have it all settled by June that will be a big relief off of our shoulders and worth every moment we spend budgeting to do so.

The other big one for us, like you is the Internet, Cable, Home Phone and Cell phone. Every time we look at how much it costs us each year we just shake our heads.

I just renegotiated our services last week all in for I believe $152 (off the top of my head right now) which is only a few dollars more than we pay now. I have to call and negotiate each year for this deal and refuse to pay over $200 a month.

I’ll cancel before we ever do that. The problem is they hook you because when you get rid of one service then you have to up another OR they grab more money from you for dropping a package to a lower level because now we would have to pay for outlets at $7.95 each that we didn’t with the other pack so we bloody well should just stay with what we have or quit it all together.

Budget Busters, you bet they are but certainly we have choices whether to keep them or get rid of them. Our home insurance and life insurance is fairly cheap. Since we have been smoke free for just over a year now our life insurance policy cost was cut in half which was nice but not as nice as having our health back and savings from not buying smokes. Cheers

Good for you!!! I bet that was tough as hell giving up – but great ins in all departments for that :) And same with your mortgage being gone soon too, you are doing so well!

These days it gets no better at all when you have grown older especially in retirement. You still keep growing but your money may not be. That’s a bummer. Your dilemma if I can call it that is something not be dreaded upon.

Rent ($900/month), car insurance ($220 per month), and food. It’s pretty scary how much we spend on just living somewhere… I really don’t know how people have extremely huge houses with big mortgages.

We are going to be buying a house pretty soon. Really don’t want my expenses to increase, so I’m trying to figure out ways to decrease our expenses now.

Yeah, I used to want a big honkin’ house myself but not anymore – it’s too much “stuff” for your head. And wallet, really. I liked it when life was more simpler so I’m slowly trying to get back to that type of stuff :) Which usually includes nixing extra costs too – woo!

Stupid cable bills. I’m dying for the day Google Fiber comes to my neck of the woods. Did you know that it is free ($300 installation charge only) if you pick the low bandwidth option?

Woahhh what is that??? Never heard of before! Going to Google right now…

As we get older, we do realize where have our money gone every month and how we can fully maximize our income aside from setting aside for savings. I wouldn’t mind spending quite a lot on buying a house.

By far I hate my electricity bill. We obviously didn’t think about how energy inefficient our home is. We spent over $300/month during the winter on electricity for a 1700 sq ft house. OUCH!

Yikes! At least you have some time now to tweak here and there before the next winter season hits :) I’m sure it would help in the Summer days too!

Obviously can’t do much about the housing and insurance, but here’s my ‘communications’ setup:

Basic cable: DUMPED

Basic internet: $30

Netflix streaming (no delays on cheap internet): $8

Airvoice Wireless cell plan: $10

Google Voice home line: $0

Every bit of savings helps.

Nice! That’s a hell of a set up, my man.

Thanks, you have a hell of a blog! I just found your Panera post from a 4-5 years ago and that was amazing. Keep up the great stuff

Hah! It’s gonna happen one day, I promise you… I will own Panera outright :)

I totally freak out trying to figure out where my money goes from time to time. What helps me is going over the budget. I add up how much i actually am saving and how much for debt repayment. And how much i pay in taxes and insurance! Then i look at my discretionary money and it isn’t a lot. Then i usually feel better. :)

Right now my most hated expense is my car payment. I love my car, and I’m happy with the purchase and expense, but the payment is killing my cash flow. The interest rate is 0.9%, so it seems silly to pay that off when i could work on my student loan, or mortgage instead.

yeah, car payments are no fun at all.. esp with other debts with much higher %’s! I’d probably do the same in your case, unless the amount left was small enough where you could get a “win” sooner than later by paying it all off and feeling good.