If you’re currently on the hunt for car insurance, and/or love all things relating to car insurance (and who doesn’t, am I right??), I got something for you that might help :)

(If you’re not in the car mood today, avert your eyes now and check out this fun little ditty instead! –> “Smart“, by Shel Silverstein.)

I just partnered up with a new (to me) company trying to make the whole insurance searching and “locking in” part easier for people, and me thinks you might find it helpful as well.

![]()

They’re called The Zebra (where you can find insurance “in black & white” – zing!), and they’re pretty much a *search engine* for car insurance.

You fill out some data, hit submit, and then it’ll load up a bunch of companies it thinks will be your best options which you can click through and go on your way. And since they’re independently run and not associated with any insurance companies, they’re free to be nice and transparent.

But what I REALLY LIKE that they offer, mainly just because I love taking polls/quizzes/games and seeing how good I’m doing, haha, is their Insurability Score™ tool. Which analyzes a bunch of data you enter, and then spits out how “insurable” you are to companies. As well as how to improve your standing if you happen to not score as high as you’d like :)

Here’s a clip off their site:

“Car insurance companies use more than 43,500 factors to calculate your risk and determine your rates – but they don’t tell you how they do it. The Zebra formulates a number from 400 to 950 which represents your individual level of risk and the financial vulnerability you create for insurance companies – your Insurability.”

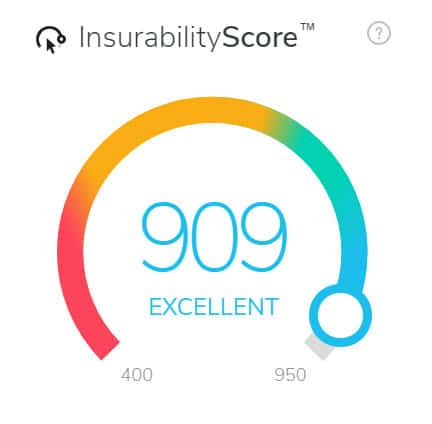

I just took the quiz right now (of course), and here’s what it pumped out for me:

Beautiful! Haven’t changed or looked for different insurance in approximately 20 years (USAA for life, baby!), but it was fun to see where I fell in case the apocalypse ever hits ;)

What was really cool though, was that they show you *how your rates change* with every question you answer as you’re filling it out so you can see how they all play a part. The goods, the bads, and the so-so’s.

I missed it the first time I took the questionnaire (it’s in the upper right hand corner of the site), but I started over and retook it again, just so I can take notes and give y’all the play-by-play ;)

Here’s how it went down, with the starting point being $141/mo for the “Minimum” plan which the below changes are based off… I also included my answers in the first set of parentheses, along with the changed rate as I went along in the second set of parentheses so you can see how it affects one another.

Here we go!

- How much do you drive yearly? (< 7,500 miles) — dropped by $7.00 ($134.00)

- Where do you live? (added address) — increased by $11.00 ($145.00)

- When were you born? (added bday) — dropped by $14.00 ($131.00)

- Married? (yes)– dropped by $9 ($122.00)

- Credit score? (excellent) — dropped by $41!! ($81.00)

- Level of education? (bachelor’s degree) — dropped by $3 ($78.00)

- Own or rent home? (rent) — $0.00 difference (fascinating! thought it would lower it?)

- How long have you been insured? (chose longest period) — dropped by $13 ($65.00)

Then there was a speed round, along with a bunch of check boxes you can check which made it hard to follow/determine all the price changes – but here were a handful more questions I answered:

- Any accidents, tickets, or claims in the past 3 years? (nope)

- Moved in past 2 months? (yup!)

- Currently employed full-time? (yup… at least full-time income :))

- Active duty military or veteran? (nope)

- Do you pay in full at the start of your policies? (nope – but I know it saves you $$$ when you do!)

- Do you set up auto-pay from bank account? (yes – also usually saves you money)

- Do you go paper-less? (yes)

After all was calculated the final rate it spit out was $98/mo, down $43.00 from the original $141.00 we started at. Not nearly as good as my USAA rate of $63.56/mo!, but it’s pretty hard to compete with them and one of the reasons I’ll never stray :) (Though within minutes after completing the form I did get an email which I suspect was not a coincidence from Geico offering me $63.43/mo — beating them by a whole 13 pennies! Haha…. Good try, Geico!)

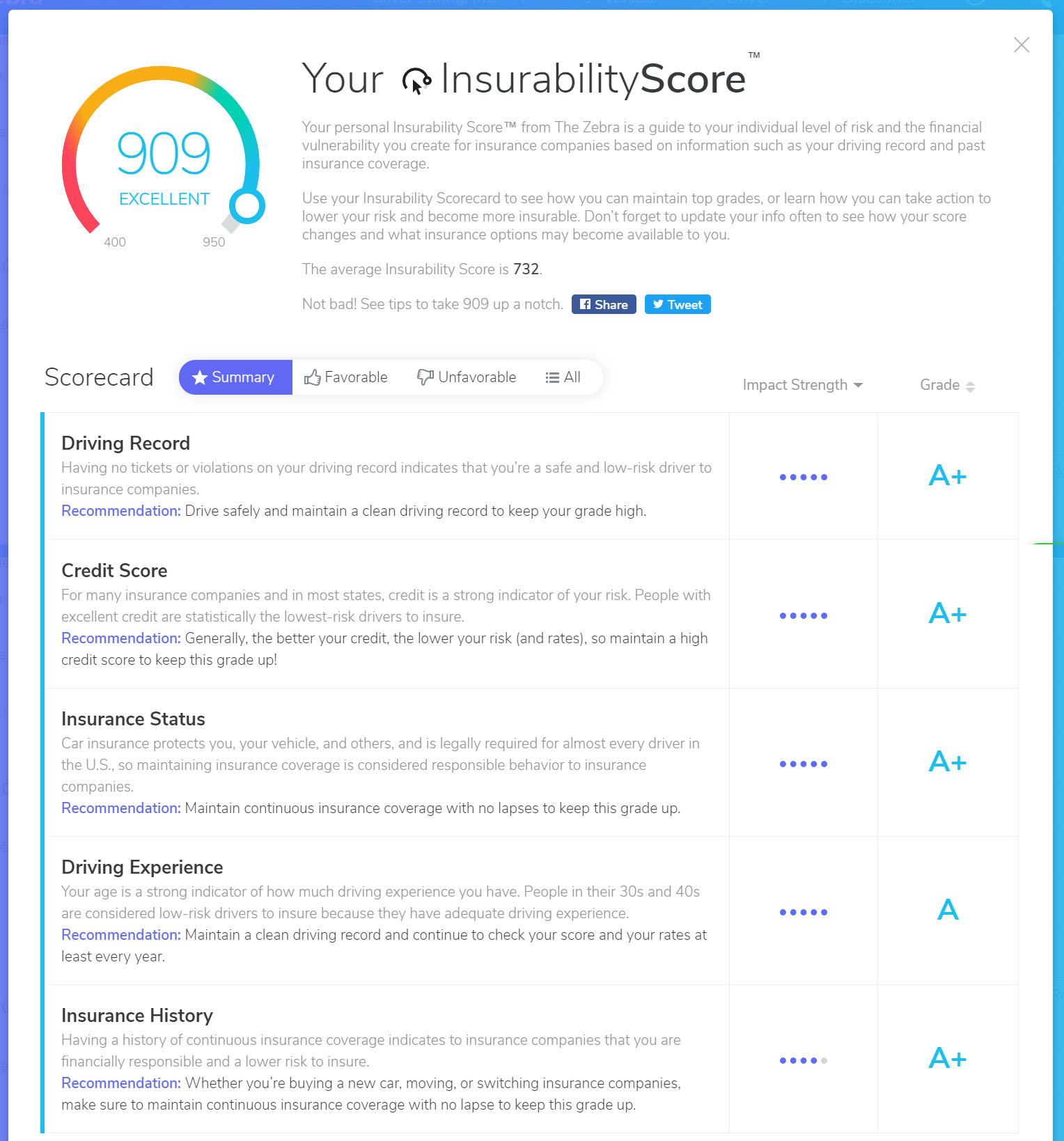

Then when you’re finished filling out the tool, it passes you your Insurability Score™, along with a more detailed *report* that goes along with it.

Here’s what mine looked like:

(I probably should have lied on some of them so you can see how it recommends changes, but I really wanted to see my score, haha… You can check out their main Insurability page though to see examples of other reports :))

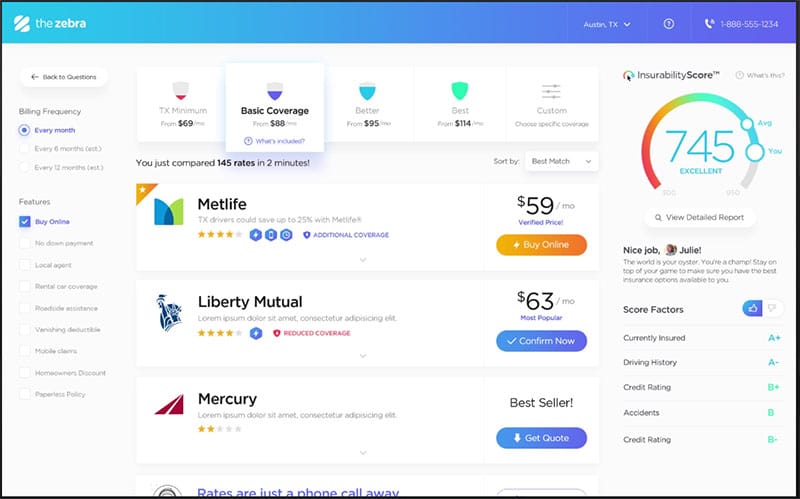

Oh, and then here’s an example of what the “search engine” dashboard looks like too if you want to see what that looks like (I got consumed by the insurability stuff!):

They also have resource pages on all the major insurance carriers out there if you want to compare, which could give you another way to help make your decision easier. Just for fun, here’s one of the pages I randomly selected ;) –> USAA vs Gieco.

**Look interesting? Check out your Insurability Score here**

Lastly, here’s a fun “myths” page that threw me for a loop because I got a third of them wrong!! :)

Which of these do you think are true, and which do you think are false?

- You can negotiate your insurance rates

- Your abilities/disabilities (i.e. vision, mobility) affect your quoted rate

- The color of your car impacts your insurance rate

- Parking tickets affect your insurance rates

- You have to wait until your policy term ends to switch insurance companies?

Here’s the answer key: they’re all FALSE :)

Crazy, right?? I got the parking tickets one and the color of the car totally wrong – which I could have SWORN affected your rates!! I literally would have put money on it. And I now blame my dad for all those times he denied me red cars just because of insurance, haha… YOU WERE WRONG, POPS!!

At any rate – there you have it.

- If you’re looking for help finding new car insurance, give The Zebra a try: TheZebra.com

- If you’re bored or just want to see if you can beat my Insurability Score, you can take their quiz here and then rub it in my face ;) — thezebra.com/insurability-score

A quick warning that there *is* a bunch of data you have to fill out though, as well as providing your email address (which I told them to change so more people would test it out!), but outside of that it’s a pretty neat thing to see. Especially as most insurance companies tend to keep us in the dark about this stuff.

So yeah – car insurance! Something you hate to pay for, until the day you don’t! ;)

Whether you check Zebra out or not though, let us know how much you’re currently paying for car insurance, as well as who you use and why! Just fill out this sentence here so we can all compare easier:

“I drive a _______ in the state of _______, and it costs me $_____/mo through _______. I use them because _________.”

Here’s mine: “I drive a 2008 Lexus RX350 in the state of Maryland, and it costs me $63.56/mo through USAA. I use them because they’re cheap, reliable, and have excellent customer service.”

Your turn!

********

This post was in partnership with The Zebra, meaning I was compensated to talk about them today… Something I only do for companies I like and think will help our community here! Loved their insurability analyzer the second I saw it, and thought it was a fantastic exercise to take whether you’re in the market for insurance or not. It’s always good to know where you stand in the different areas of your financial life!

[Photo up top by Nick Baker on Unsplash]

Get blog posts automatically emailed to you!

We drive a 2009 RAV4 and a 2014 Kia Forte in the state of NY and it costs us $70/mo through Allstate. We use them because they’re affordable, give multiple insurance discounts, and have friendly and responsive local customer service.

Great! They always *seem* friendly based on commercials alone (hah!), but have never used them before (or actually known anyone to use them?) so that’s good to hear they’re pretty solid :)

Hey Liv,

I used to use All-State as well, but they kept raising my prices every year. Even after calling, and telling them that I had no choice but to switch based on the same insurance at lower prices, there wasn’t anything they could do :(

I switched to Geico with the same coverages – saved about $200 every 6 months.

Wow this sounds like an insanely useful site! Especially since I’m about to be shopping for car insurances. I currently pay $256 twice per year to drive a 2005 Honda Civic on my dad’s family plan in Ohio. (Cheapest for everyone but I’m finally getting kicked off once this old girl bites the dust haha).

Haha… Could be another decade with that Civic! They last forever! :)

I’ve heard of Zebra but haven’t checked it out. Do they require a Social Security # to get your credit score? We froze our credit due to Identity Theft so no one can check our scores.

We have a 2013 Ford Focus & 2016 Ford Fiesta. Full coverage on both cars with Geico for $101 per month. We like Geico as they have low rates, give multiple discounts & great customer service. A few years ago they went to my husband’s job to replace a cracked windshield.

We’re in North Carolina

They ask you to self-report your range (in the fair good excellent ranges) – minimal PII was requested

Hey Debbie – ran your question by The Zebra team and here’s what they said — “The Zebra does NOT require a SSN and will never ask for it.”

Hope this helps :)

Our old Toyota Corolla’s nickname was Zebra because it was so old, and the exterior black paint was peeling off!

We just switched our car insurance from Liberty Mutual to Progressive, and the payment was cut by half.

Nice! On both accounts, haha…

I used to have a friend who painted his car like a cow, and then took it further by installing a majorly loud “moooo’ing” horn and would blare it all around college campus. People loved it :)

Getting pains in my stomach laughing if that guy took his car on a world tour what would be the reaction from people around the world. I can bet South Asian kids would act crazy.

I am totally going to play around with this. Insurance is bananas in IL (for cars, for houses, etc.). I feel like I do a pretty good job of calling around and price shopping at least once a year, but this just makes me feel like I’ll be a more informed consumer. Thanks for the tip!

Great! Hope it helps!

I just did the Insurability Score mainly for fun and came out with a 940 which I’m feeling pretty good about. Still, most of the insurance companies listed wanted me to go to their site where I would have to re-enter all of my information for a quote. I was hoping to get some guesstimates so I wouldn’t have to do that.

Weird – they’re def. supposed to give you guestimates in their portal… Maybe something’s funky with where you live? You KILLED my 909 score though – pretty impressive :)

UPDATE: Ran your note by the Zebra team and here’s what they shot back – “If you go through the process, your quotes should appear on the same page as the score in which case you would NOT need to re-enter the information. However, some insurance companies do not pre-populate with your information.”

I have a 2006 Altima and pay about $350 every six months in NJ. I saved about 50% when switching from my last insurer. If you have not searched for new insurance rates in the past year, I highly suggest it. Don’t let procrastination cost you money!

Nice dude! I agree – even when I called my old All State agents about price increases making their premiums to high, they couldn’t even do anything about it. Next thing you know I was on the search :)

TOTALLY.

Can even be a nerd about it and set calendar items to pop up every 6 months to double check as well :) No way you won’t be getting the best deals by keeping that rotation going!

There are basically 2 options for car insurance.

1. If you can get USAA go thru them.

2. Geico is a close alternative (hearsay, sometime the price is marginally better)

3. Everything else sucks…

I have Geico and pay a shade over $700 a year for 2 cars with full coverage. Back when I have Allstate I was paying double my current rate for the same coverage.

Here’s a fun fact about Geico too — It was a former USAA employee who started it ;)

https://en.wikipedia.org/wiki/GEICO

“GEICO was founded in 1936 by Leo Goodwin Sr. and his wife Lillian Goodwin to provide auto insurance directly to federal government employees and their families. Since 1925, Goodwin had worked for USAA as an insurer who specialized in insuring only military personnel. He decided to start his own company after rising as far as a civilian could go in USAA’s military-dominated hierarchy. Based on Goodwin’s experience at USAA, GEICO’s original business model was predicated on the assumption that federal employees, as a group, would constitute a less risky and more financially stable pool of insureds compared to the general public.”

I drive a 2012 Sienna and pay 59.33/mo with Ameriprise through Costco. If you haven’t checked out their auto and Home policies yet, you should! We saved hundreds when we switched to them; customer service has been excellent. My score was 912 and the lowest monthly rates offered through Zebra were in the 90s.

COSTCO??? What *don’t* they get into these days??? Haha… never even heard of that, but nice find! (And for beating my score too :))

I drive a 2012 Highlander, hubby drives a 2006 Mazda tribute_ in the state of NY, and it costs me $60_/mo through Allstate_. I use them because they are cheap and have a good reputation.

Nice! I loooooooved my Highlander when I had one years ago… My wife was so mad when I sold it to get rid of car payments, haha… (that, and I switched to a hoopty :))

I drive a 2013 Chevy Malibu in the state of Ohio, and it costs me $72.22/mo through USAA. I use them because THEY ARE THE BEST!

I will NEVER leave USAA willingly. They have to kick me out, and I refuse to go without throwing a major tantrum lol.

Sounds about right :)

I drive a 2017 Honda CRV in the state of Ohio and it costs me 58.73/mo through Hartford. I stay with the because their rates are low and they didn’t raise my rates after I totaled my car a year ago.

Ouch! Glad YOU came out of it okay too!

Ohio’s representing nicely today too haha…. there’s like 3 or 4 of you guys chiming in!

I drive a 2017 Prius in the state of Texas, and it costs me $108/mo through USAA. I use them because they have always treated me well. I thought I would be paying more for them than others, but the quotes given were more expensive for less insurance. I have ALL the coverage! My score was 940

Why is everyone beating me today??? Haha…

It gives you a goal :)

I’m glad none of you live in Louisiana…

I have a 2012 F150 (full coverage) and 1992 Mustang (liability) and insurance is $135/month. My sister and I (28 and 32) are both still on our parent’s plan, with like 10 vehicles total with State Farm.

My wife has a ’13 Ford Escape (full coverage) with Geico and pays $107/month.

Doesn’t help that if you get in a 3mph fender bender in Louisiana, your chance of someone claiming neck injuries and suing is like 85%. So many injury lawyer billboards/commercials in Baton Rouge… sucks.

That does suck :(

At least y’all have some old beautiful cemeteries though :)

“I drive a 2016 Honda CR-V and my wife drives a 2013 Ford Focus in the state of Wisconsin, and it costs us $126/mo through USAA. I use them because of all the same reasons J-Money listed! They’re absolutely amazing.”

I’d just like to point out that I’m originally from KY, and my wife’s car cost us this much ALONE through USAA. Car insurance is expensive AF down in the Bluegrass.

Great resource! I checked mine and it wasn’t even close though… like you, we use USAA and they just kill everyone else, price-wise. The customer service is stellar, too. The one area I know of with USAA that I need to address at some point is investments – we have everything through them, and their fees for our Roths and SEP IRA are pretty high compared to Vanguard..

I know :( I started with all my investments there, and eventually just sucked it up and moved them all out to Vanguard because it was all adding up… You *can* actually invest in Vanguard funds through USAA, but the fees to do so are crazy high per transaction. Been a few years since I’ve moved my money out and def. not going back :) So now I have all my accounts w/ USAA except for investments haha… (and business banking, since they don’t offer it yet (!!!))

Awesome site and fun to play around with the inputs to see what the real drivers are. Also had a good laugh at the GIF at the end!

Hey thanks! I was pretty proud of myself for that one ;)

I use Geico primarily because I drive American cars and Geico offers mechanical breakdown insurance, which I’ve used 2 or 3 times. I moved from State Farm specifically for this reason. I’ll check Zebra to see what other companies offer mechanical breakdown insurance because it does come in handy for those expensive repairs.

Did you just basically say American cars are crap? Haha….

Why do you keep using them then?? :)

Interesting find! I don’t particularly want to be haunted by insurance companies so I probably won’t try it, unless I use a fake name/email address though :)

“I drive a 2014 Mazda CX-5 in the state of California, and it costs me $103.76/mo through Amica. I use them because they offered cheap “gap” insurance when I bought my new car and had a good rate.”

– I paid my last bill in full when I got it, so I had to take that and divide it by 12 to get the monthly cost

– When I bought my car, the dealership wanted to “fold in” a $1500 cost for “gap insurance”. The way it was described – you walk out the door with a $x loan in a brand new car. Two months later, you’re in an accident and the car is totaled – insurance pays out the value of the car – which isn’t going to cover the amount you owe on it.

YES this is exactly why buying a new car is financially unsound. But – since I was doing that anyway, gap insurance seemed like a good idea – but not for $1500!

Amica was the only insurer I found that offered gap insurance (something like $7 a year) and also had reasonable rates otherwise. I’ve been with GEICO forever until I switched to Amica – the next time I renew I will confirm that my loan balance is less than my vehicle value and shop around again.

Interesting – never even heard of Amica before? Sounds like a misspelled “America!” Haha…

But good idea on that fake name/email route ;) I always say I should do that one day but then I never do… Although I suppose I’m already fake since I use all my “J. Money” accounts for stuff, haha… (Spoiler alert: it’s not my real name!)

Geico — $141/month for 2014 Hyundai Sonata & 2003 Hyundai Santa Fe (just made it to 200K miles & hope to make this baby last another 50-100K).

We live on gulf coast of Florida, downtown, 4 blocks from bay. Have had Geico since moving to Fla 20 years ago. Been meaning to shop around, your article has lit a fire. Zebra-ing now.

P.S. this is my 1st comment on ANY financial blog (and I follow all the good ones). my friend, you (and all your hard work) make me happy :)

Heyo!!! Compliment of the week right there – thank you! :)

I’m bummed! I just Zebra-ed. My score was 923, but the lowest quote was almost DOUBLE what I’m paying now with Geico. For same coverage as now, quotes were $262-$309 (compared to current Geico $141). It’s probably the whole “Florida thing”… hurricanes, TONS of uninsured drivers and kids who would rather steal cars than swim in the gulf. Oh well, it was worth a shot to save money. Thx for the Zebra referral!

Oh jeez, haha… sorry it didn’t show you anything better! Damn car stealers! ;)

“I drive a 2012 Piazzo Typhoon (cheap Italian scooter), in the state of California, and it costs me $97.00 a year through Foremost Motorcycle Insurance. I use them because USAA wouldn’t insure me my first year, and no one else has been able to beat that rate yet.” But when I did drive a car it was $70 a month or so through USAA. :)

BALLER!!

I drive a 2010 Toyota Prius in the state of Ohio, and it costs me $70/mo through Progressive. I use them because customer service is good and the price is affordable.

I drive a 1999 Mustang convertible (husband has a 1991 Turbo MR2) in the state of North Carolina, and it costs us $45.83/mo through Progressive. I use them because the prices are good and we have had no problems with them when we did have claims. We do not have full coverage because we own our older cars outright and would never receive replacement value for them if they were totaled. However, we do have personal liability coverage increased to $500K. Our Insurability score was 936, and the few quotes Zebra showed were WAY higher than what we are currently paying.

Oooooh I used to want those Turbo MR2 bad growing up! Can’t believe they’re 30 years old now?!

Yeah, he got lucky and bought a Master Mechanic’s project car. So the body of the car is old, but almost everything under the hood was new when he bought it. He was able to buy it for $4K only because he was likely one of the few people around who could take it and finish putting it back together.

sounds like a damn fun hobby :)

I got around the same score as you as well J, around the low 900s. One the top car insurance recommendations zebra offered is one were have, MetroMile at around $85 a month. It’s a pay per mile insurance where they charge you based on how miles you drive a month. They give you a base rate of $40/month then charge you like 6-7 cents a mile and that would be the monthly rate.

It’s a great insurance rate for drivers like us who don’t drive that much.

Oh wow – never heard of that setup before? Thanks for sharing it!

926!

I drive a 2016 VW SportWagen in the state of MD, and it costs me $95/mo through Allstate. I use them because once they pile on the multi-policy discount for also having home insurance with them, I haven’t found anyone who can beat the combo.

Zebra quoted double what I’m paying. I don’t get a 50% discount on the car for having home insurance, so I don’t know where that number came from.

That’s an interesting catch actually – that they can’t tell if you have other types of insurance w/ these companies that could lower it drastically! I’d imagine once you clicked over to the insurer’s site though and went through the process it would all come up and be included, but yeah – only if it doesn’t scare you off initially :)

J$ Interesting tool I will have to check it out.

Quick question for you… you put that you pay $63/m, which is nice. How are your coverages? Liability, medical, uninsured/underinsured? I used to strictly look at price until a friend got into a tight spot who had poor coverage. It ended up costing him a lot of money due that poor coverage. I agree price is important but proper coverage to “safeguard” your net worth incase you are sued is financially smarter.

Totally! Very important considerations!

I didn’t include just to keep the post more focused on the tools here, but if you’re specifically asking me I’ll have to go look it up now :) (It’s been a while!)

Here we are:

— Comprehensive and collision coverage with a $200 deductible

— Car replacement assistance ($10 extra for 6 months),

— Bodily injury @ $300,000/$500,000

— Property Damage at $100,000

— Uninsured Motorists Bodily Injury @ $300,000/$500,000

— Uninsured Motorists Property Damage @ $100,000

— Personal Injury Protection @ 2,500 per person

— Medical Payments @ $5,000 per person

And then I have Umbrella Insurance as well that helps cover all REALLY crazy situations….

My wife’s car insurance is a lot different too since her car is much older and not as valuable, but yeah – hopefully this gives you a better look :)

Interesting site, but I don’t like that they made me give an email and phone number to see my score. I just want to look, not get sales calls. Fortunately I was able to use a burner email and phone number.

My number ended up being 915 with a rate of about $50 – $140 depending on coverage. It did look as if what was included in their “minimum” did not include the legal minimum required for my state, namely uninsured motorist insurance.

I drive a 2010 Honda Civic. I was paying $163/month with Liberty Mutual, and JUST changed over yesterday to $115/month (knocked down to $105/month paying in full for the year) with Geico – same coverages. To avoid the 5% fee on the total premium for leaving a policy early – I’ll start this up in June 2018 (2 more months of the higher rate makes more sense than the 5% fee).

Grateful it was suggested to shop this rate with Geico, another carrier offered me a lower rate, but I had an outstanding issues from 2016 that needs 2 years to wipe off my insurance record – argh! Motivation for even safer, more aware, driving!!

Good job!! Now the more fun question – what will you be doing with this $50/mo in savings? :)

Didn’t get asked all those questions… and with popups disabled …couldn’t get to the questionnaire…seems i’m within the range that everyone else is paying… that’s good i guess?