This one’s for all you Aussies today ;)

Alaya stops by the blog to share her journey tracking her net worth so far, which is once again a testament of how powerful doing this one simple thing can be! And she’s only two years into it!

Thanks for taking the time to spill it all for us, Alaya.

And I caught your Drake reference there, too ;)

******

Hi J,

This month was my second complete year of tracking my net-worth, which I started soon after I discovered your blog!

With the end of your tracking, I thought it was a good time to share the beginning of mine!

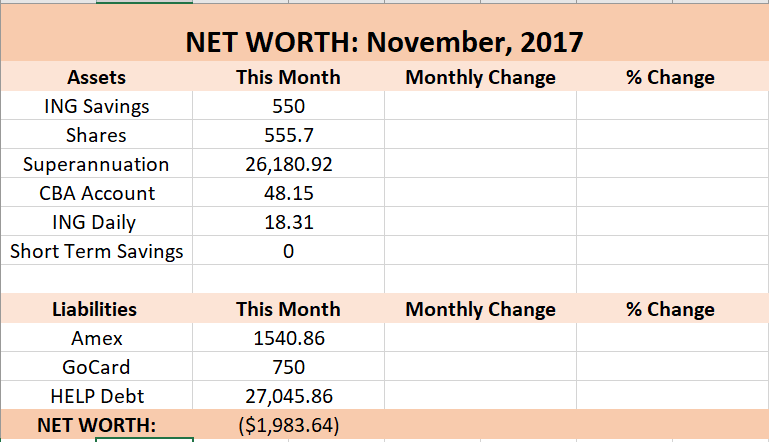

Here is first my net-worth, at the end of November 2017 with a negative net-worth of $1,983.

[FYI: 1 Australian Dollar equals roughly $0.69 in U.S. dollars at the time of this writing]

I was earning $65k per year before tax (AUD); and had just ended a toxic relationship where I’d depleted about $10k of savings to support him and his business. I’d also never had a credit card amount due at the end of the month, but as the relationship started turning unhealthy; these Credit Card debts were a “moving out and starting a new life” debt! A price I’m happy to have paid!

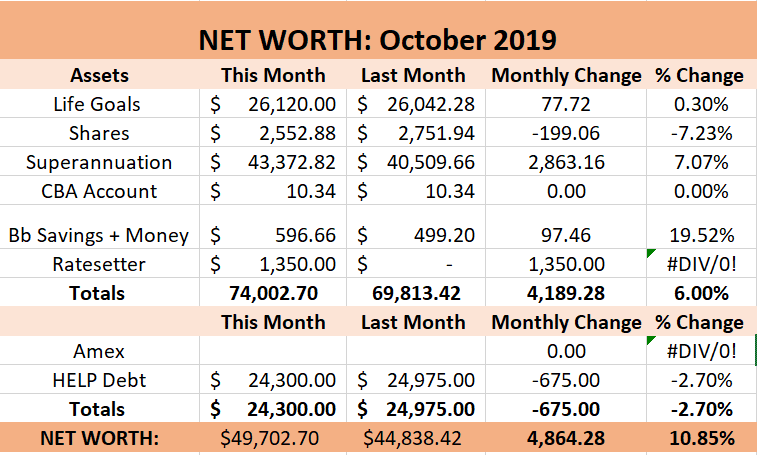

After two years, my net worth now looks like this:

… Low key annoyed I didn’t quite hit the $50k mark!

- My Life Goals Account is a cash account.

- Superannuation is Australia’s version of a retirement fund, and my employer pays a contribution equal to 9.5% of my salary. I am not contributing any extra currently.

- BB Savings + Money Challenge is an account for the 52 week challenge to see what extra on top of my Life Goals I can save! (Again, read from your blog!)

- Ratesetter; which I’ve just opened and trialed this month. I’ve locked in $1k at a 5 year investment with a 7.8% return. If I feel comfortable after a few months, I will look at transferring more across.

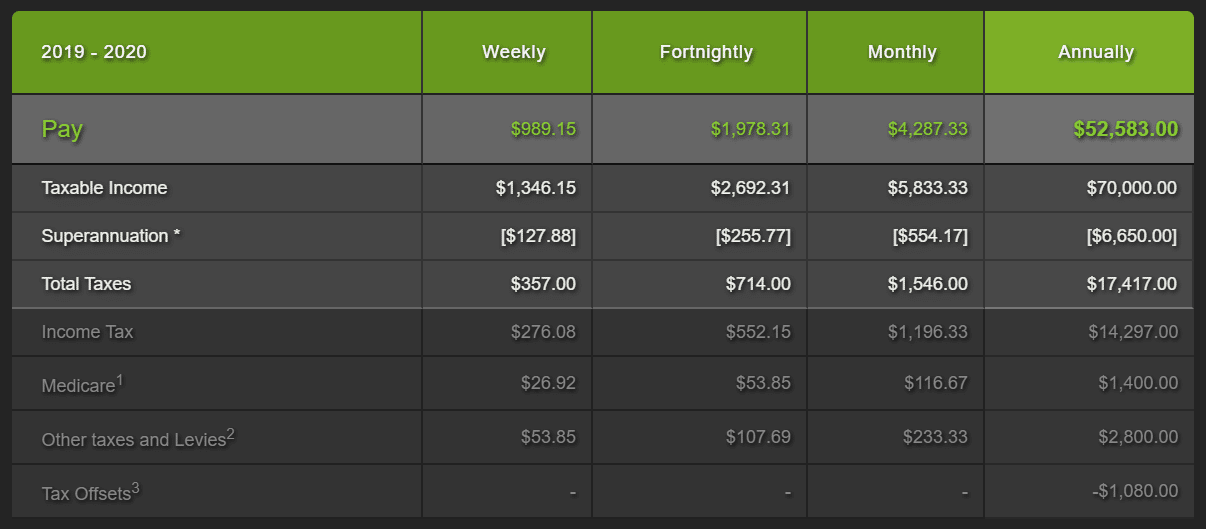

- HELP is Australia’s version of a University loan. Its through the government, there is no interest, but it is indexed once a year to inflation. My employer takes extra tax each fortnight to cover my compulsory payments. So my pay is spread out like this:

(credit: paycalculator.com.au // click to blow up)

(credit: paycalculator.com.au // click to blow up)

The biggest jump in my net worth was due a retention bonus I received, which was $10 grand cash after tax. I know there is lots of fat I can trim from my budget; and I could increase my savings ratio.

My goal for 2019 was to double my net worth (I ended 2018 at $16K) and to double my cash savings (ended 2018 at $11k) which I achieved both by July.

I have also had some big spends such as paying for my Post Grad Diploma Upfront ($6k), planning a proposal for my boyfriend (woot woo!) which I spent $1,600 on one night’s accommodation (which I would never do at any other time) and multiple of our friends weddings, engagements and hen’s parties which I’m estimating at $3k this year after accommodation, travel and gifts.

Which leads me to my setting my next goals! I’ve also just started a new job where my salary will jump to $85K! (And after the higher tax rate to pay back my HELP Loan, the difference per fortnight will mostly be taken up in tolls and petrol travelling a fair distance for my new job)

I am very much in a transitional stage so won’t rush to goals that might not be relevant or realistic in a few months, but instead focus on “challenges” for the next few months.

I think what’s amazing is that, tracking the net worth is the only thing I’ve been consistent at over the last 2 years. My goals have changed many times, my attitude fluctuates often – but checking my “net worth” maybe twice a month (after each pay) surely keeps me refining, trying to ensure (to the best of my ability) that each month is at least going up.

So, ending with a massive thank you!! You have surely kept me interested and motivated in my finances over the last few years, and helped keep me accountable with your challenges, tips and general chatter about $$.

Much appreciated;

Alaya

******

So much to love about this!

- Australia’s got it on lock with that Superannuation and interest-less student loans, WOW!

- “Life Goals” account – very smart, because Alaya’s right – our goals are constantly changing and it’s great to stay so flexible

- Money Challenges – always good to push yourself time to time 💪

- And then probably the best piece from this entire thing – ridding yourself from a-holes! Which you can do at any stage of your finances/life…

Well done, Alaya…

You’ve officially earned yourself a Sexy Saver Certificate circa 2008.

Print it out and send a copy to your mother!

Get blog posts automatically emailed to you!

Well done Alaya! And congrats on your proposal!

I’m an Aussie too (but haven’t lived there for 15 years) and am forever grateful of our uni fees system.

Seeing your B1 cell jump from 550 Aussie Ds to 26,120 has brought me so much joy this morning!

Why does 1/20 sound so much closer than 5%? Not that I know about it from experience, I’m still negative (but only four digits negative now! Less than a mile from home!).

Awesome job, Alaya! And I love the orange color scheme for the spreadsheet, it’s eye-catching but not alarming. (By the way if the divide-by-zero error bothers you like it bothers me, all you have to do is wrap the formula for those cells with IFERROR( at the beginning, and ,0) at the end. That’ll just put a zero in the cell in place of any error.)

Good formula tip!

Way to go, Alaya! And I had the same takeaways, J. I can only imagine how different MY net worth would be right now if US employers contributed the same to retirement or the government offered 0% interest student loans. probably to the tune of at least several hundred thousand (I’m in my 40s). I’ve had measily retirement contributions from my company(ies), though I’ve been saving at least 10% consistently. And now that the student loan is history, I don’t like thinking about it, but it was in total about $80k.

Anyway, the best investment was that “kick ‘em to the curb” payment! I’m sure that gave you the mental space to do greater things, as well as getting rid of a leech! Well done!

Great word for debt – leech :)

This comment makes me think of your 60 words for money post….maybe you should do 60 words for debt… ;-)

Kari

Ooooh…. challenge accepted!

This is awesome, Alaya! I just started tracking my net worth in the last 1.5 years and find it to be both fun and motivating. I had a very similar experience as you this month with my 401k – it got to just below 50,000 and I simultaneously rolled my eyes that it wasn’t *quite* at the 50k mark, but also did a little happy dance about being essentially 1/20 of the way to my million in savings goal. Wishing you the best on your journey.

Thank you!

At least it really pushed me to see what extra I could scrimp and save in the last month!

Thanks for sharing this – really interesting to see where others are at with their journey in cutting down debt & increasing overall net worth!

Congratulations Alaya, what an amazing increase in net worth!