Hey guys! Came across a new tool I think some of y’all will like :)

You know when your HR department gives you a list of funds to choose from for your 401(k) (or 403(b), TSP, 457, etc), but you never know what to invest in? Or how much or what %?

This service I just came across will tell you what to do based on your specific situation. It’s called Smart401k.com, and I wish I had known about them at my old 9-5 ‘cuz I LOVED my 401(k) but hated figuring it out. The only thing I knew was to max out those employer matches to get that free $$$ (best thing ever – you better be doing it!) and the rest I just did my best on before moving along…

If that’s you too – or you like getting 2nd opinions – this post is for you. If you live and breath this stuff and enjoy doing it all on your own, then click here instead ;)

And PS: I got them to waive their yearly fee of $199.95 for any BudgetsAreSexy reader interested in checking them out. So not only is their service helpful, but it’s FREE!

More About Smart401k

I took this off their site ‘cuz it sums it up perfectly:

You don’t need to spend hours researching the funds available in your retirement plan at work. Smart401k Investment Advisers do the work for you, analyzing fund performance, manager track-record, expenses and style fit as a part of the fund selection process.

- Detailed: Your advice is tailored to the funds available in your retirement plan.

- Professional: Smart401k uses a proprietary fund evaluation strategy, incorporating Modern Portfolio Theory and adviser oversight to create your recommendation for your retirement goals.

- Easy to use: Use the list we’ve prepared to make changes to your account.

Smart401k is an independent provider of retirement investment advice. We’re not paid by fund companies to sell their products. We’re a flat-fee, Registered Investment Adviser operating solely in your best interest.

That last part is the key, and my personal favorite: They only recommend funds from the list your employer offers! Because that’s all they CAN do, haha… And they don’t get paid on commissions or anything – just the yearly fee to use them (which again, is waived for those of you reading this).

Now in a perfect world your employer would offer AWESOME kick-ass funds to choose from making their job even easier, but unfortunately that’s not always the case. So the short list of funds can be a double edged sword.

Also – it’s important to note that Smart401k doesn’t have *access* to any of your accounts. They only recommend what to do with the funds available, and then it’s up to YOU to take action. This too can go both ways: Yay for privacy/security, Boo for meaning you have to do more “work.” But fortunately this work will literally take a minute or two :)

Other quick facts: They’ve helped more than 25,000 individual investors so far, advised on over 10,000 different company retirement plans (which is good because it means they might already be familiar with yours), and they’re rated A+ by the BBB (Better Business Bureau).

How Does Smart401k Work?

It’s actually relatively simple and easy:

- You sign up online (use this link to get the free year): Smart401k signup

- You take their “Investor Profile questionnaire” (14 questions)

- You tell them what funds your plan offers

- They shoot you back a recommendation!

- You make the changes (if you want to)

They say it usually only takes 10-15 minutes to sign up online, but I’d give yourself at least 30-40 when you have a nice window and can take your time. It’ll go much faster if you have your list of funds handy too when sitting down.

Once submitted, it takes 4-5 business days to get your recommendations (a real life person/adviser reviews everything) and then it’s emailed over and updated in your account online. Every 3 months they’ll review it and pass along any changes they feel should be done, as well as anytime your plan – or life situation – changes too. Though you’ll have to remember to tell them so because unfortunately they’re not mind readers ;)

Cons?

The only con I can really think of since the $200 cost is waived for y’all (woop!), is that the forms are rather annoying to fill out. And the 14 question profile questionnaire is too. But I really don’t know how you can avoid it since it’s all pretty important things to know or else an adviser can’t advise, haha… And you really do want them to have this info! :)

So in cases like these you just have to suck it up once for 20-30 mins, and then pat yourself on the back for getting it done. And really, in the grand scheme of things, your retirement investments are a pretty damn important thing to lock down. So you’ll be glad you did. (And maybe some of you will actually enjoy it like you did our financial personality quiz?)

UPDATE: I’ve heard that advisors from their parent company – The Mutual Fund Store – will call you to try and get your business in other investment areas of your life too. This doesn’t affect your free 401k recommendation, but it might annoy you if you’re not looking for help in those other areas. The trade off of getting all this for free, I suppose :)

What Does it All Actually Look Like?

I got on the phone with them to be walked through it all, and in the process they gave me a dummy account to log into and poke around. I took screenshots of what the important areas look like so you know what to expect.

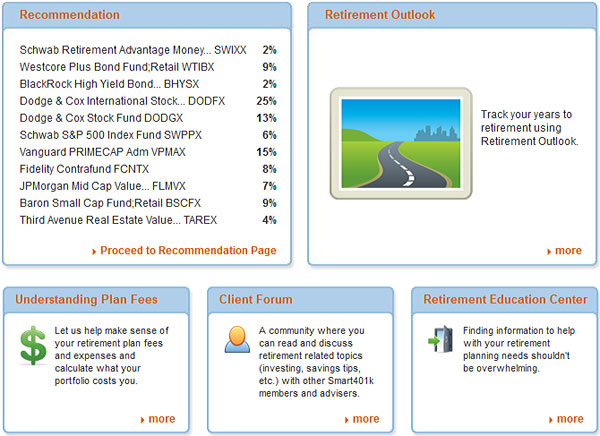

Here’s the one you care about the most – the recommendation part: (this is front and center as soon as you log in – you can’t miss it)

Below this they show you the next steps that need to be taken, along with any additional notes to consider. And again, remember that you’ll have to actually make the changes yourself in your plan since they don’t have access to it.

Below this they show you the next steps that need to be taken, along with any additional notes to consider. And again, remember that you’ll have to actually make the changes yourself in your plan since they don’t have access to it.

Here’s one of the additional notes I liked that was in my dummy account:

- If your plan offers company stock, we encourage you to hold 10% or less of your total portfolio. (<– Good advice!!) Please note that we do not analyze company stock or include it in your recommendation.

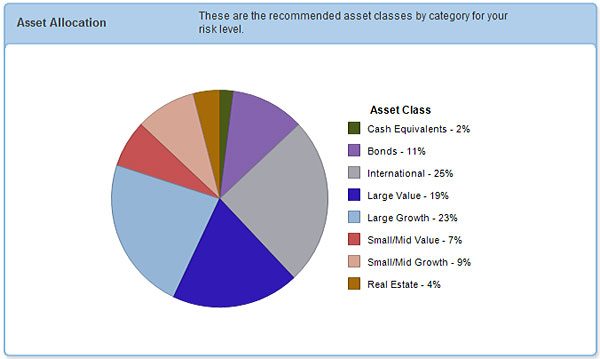

There’s also a tab/page for your “asset allocation”

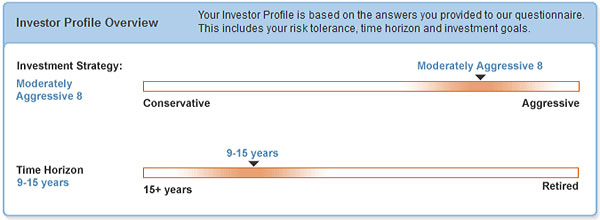

And then a tab/page for your “investor profile” (ie risk profile):

Below this they share information on your investment strategy, your calculated risk level, and then your time horizon to retirement. There’s also an area to change your questions to your profile questionnaire if you’d like to adjust it.

Below this they share information on your investment strategy, your calculated risk level, and then your time horizon to retirement. There’s also an area to change your questions to your profile questionnaire if you’d like to adjust it.

And lastly, this is what the main area of your account looks like:

That’s really all there is to it, it’s fairly simple. There’s a forum you can poke around to check out and ask questions, a retirement education center to read up and learn more about investing/retirement, and then some other links with informational stuff too. But the main areas of interest are those three sections above.

That’s really all there is to it, it’s fairly simple. There’s a forum you can poke around to check out and ask questions, a retirement education center to read up and learn more about investing/retirement, and then some other links with informational stuff too. But the main areas of interest are those three sections above.

You shouldn’t need to spend a lot of time in here once you get the goods :)

Oh, they also make it super easy to talk to a real life human being/adviser too which I LOVE. Their # and email are listed everywhere (1-877-627-8401, info@smart401k.com), and they have a quick “chat box” area too which is what I usually prefer. There’s also no additional fees for talking with them and getting advice! It’s all included in the flat yearly fee which is waived for you for the first year (when the year is up, they’ll ask you if you want to continue or not – you won’t be automatically renewed or charged or anything like that – don’t worry! They won’t even ask for c/c info when you first sign up…).

And That’s That!

So, in a nutshell…

- If you have no idea what to choose in your 401(k), or want a 2nd opinion, Smart401k can help

- As well as with 403(b), Thrift Savings Plan, 457 and small business retirement plans

- You fill out some info once and you’re done (unless changes happen on your side later)

- They shoot you back recommendations to take action on (as well as follow ups every quarter)

- It’s free for a year, but only for BudgetsAreSexy readers :)

You can try it out here if interested: Smart401k service

Questions? Comments? Concerns? Drop them below and I’ll have someone on their team answer any I can’t myself. Again, it’s not for everyone – like those who love researching and thinking/doing stuff on their own – but for the majority of people it’s a great service to consider. I’d sign up myself if I could, but sadly they don’t work with self-employed programs… And they’d probably freak out anyways when they see I’m fully invested in one index fund – hah!

Anyways, hope this helps! If anyone’s used them before, or others like it (are there others like it?), please do share your thoughts with us… I’d never heard of this service before and I think it’s genius :)

—————-

PS: Whether you try the service out or not, do make sure you’re contributing at least up to your employer match to get that free money!! It’s one of the main things I did to grow my own net worth, and a helluva easy way to turbocharge your investments for doing something you should be doing anyways. Do whatever you can to take advantage of these benefits!

ALSO NOTE: As with most reviews of companies I like and trust here, I get compensated when people sign up through my links. But please don’t do that if it’s not a service you want to try out. While I’ll never promote a company I don’t like or find helpful myself, it’s important to do your own due diligence.

Get blog posts automatically emailed to you!

{kind=link}

J. Money, Smart401k.com seems to be an interesting service. I appreciate that you share it with us. I am actually changing the mode of my investment 401(k) and I am sure that Smart401k can assist me with this. Thanks J.

Interesting that they have you break up your allocation among so many different funds. Good diversification can be a great defense play against recessions. I wonder if behind the scenes they do any back-history analysis to help develop that recommended asset allocation.

I’m sure they do all kinds of stuff behind the scenes, but I’ll see if they can chime in here… I did think there was a TON of diversification here too – much more than I’m ever used to – but then again I’m known to over simplify and certainly not an expert! :)

Got a response from the Smart401k team – here you go:

“Most investors understand that diversifying their portfolio is a good thing, but some may struggle with how to do it. To be diversified, it’s not enough to own a “collection” of funds – you have to own funds across different asset classes, and those funds should work together holistically to help you reach your investing and retirement goals.

Finding the right asset mix is not as simple as choosing the right investment categories. Our economic and investment research can determine what types of investments look to be the most promising going forward. Based on this research, we adjust your allocation to those investments that can give you the best chance of performing well in the future. Additionally, making changes to your asset allocation as your personal circumstances change should keep your investments on track.”

Seems like an interesting service/ tool just to check out even if you are preforming other research to see how it compares.

Oooh, do they analyse foreign funds too? I have a Kiwisaver retirement account and would love some advice (even though my returns are approaching 20% over the past year, WOOT!).

Thanks for this, J$. You’re a star.

oh wow – 20% is incredible!

I’m not sure if they do that under the Smart401k part, but they’re owned by TheMutualFundStore.com who does more typical investment advice stuff… Maybe check them out?

Thanks for the review. Any tool that helps demystify the 401k and make investing more accessible to people is welcome! And it sounds like this tool does just that.

I’m loving all of this new technology that is changing how we do things, many times for the better. Now if only the real estate market would get in the game and get rid of the crazy 6% fees!

But back to this service. It looks good but my question is does it analyze the management fees the funds charge? In many cases, the fund offered in 401k plans aren’t the best, so going with the lowest fee fund is usually the first (and best) option.

My other question is why so many funds in the example? Yes diversification is a good thing, but you can be too diversified and just be buying the same thing, just in different allocations. In the example, you don’t really need the Dodge & cox fund and the Schwab 500 fund. Just one (probably the Schwab fund) would be enough. In fact, you could easily get away with 4 funds and still be we diversified and not sacrifice and return.

I’m pretty sure they keep everything in account when advising. But I agree they aren’t always the best funds to choose from :( Which is why I’m a big fan of rolling over all old 401k plans into an account you control 100%! So you get to put your $$ exactly where you want!

Here’s a note from Smart401k:

“The operating expenses of each investment option are taken into consideration. However, in some cases, the performance of the fund may justify paying a slightly higher fee. Each fund has its own unique operating expenses. Index funds and exchange-traded funds (ETFs) will usually have lower expense ratios than an actively managed mutual fund. But remember, lower expenses don’t automatically mean a better return. The right actively managed fund may be worth the extra cost. You want to look for funds that have low operating expenses, but not without also considering their performance. Compare multiple yearly returns for the last ten years. Be sure to include the various fees and expenses in your calculations. Small differences in cost grow large with time.

The manager of a fund can be as important as the fund’s holdings. How frequently are a fund’s holdings bought and sold? Remember, more activity incurs more fees. Find a good balance. Does the fund’s manager have a history of investing money successfully? What is the manager’s investing style and theory? Is it risky or conservative?

It is important to understand a fund’s expenses as well as its potential. Gaining the necessary knowledge may seem overwhelming at times. Your financial future is important—you should know what you’re paying for and what you’re getting back.

To be diversified, it’s not enough to own a “collection” of funds – you have to own funds across different asset classes, and those funds should work together holistically to help you reach your investing and retirement goals. Holding a mix of index and active funds is a way to get the advantages of index funds along with potentially the financial upside of active management.”

“The right actively managed fund may be worth the extra cost.”

How about the fact that actively managed funds are trying to beat the market and index funds just try to meet it? And the fact that index funds track the market much better than actively managed funds?

Honestly, this Smart 401(k) service sounds like a cheaper way for someone else to manage your 401(k) for you than a normal advisor service, but still expensive and still actively managing, while in the guise of being a “fancy new online service”. My weighted expense ratio across all of my investments is 0.104%. That means that I would need to have a $191,000 portfolio before I’m paying Vanguard/Fidelity $199/year to manage my investments.

The idea is interesting. The thing I would check is to see how much overlap each fund has. If you invest in an S&P fund and then another large cap fund, the amount overlap is pretty insane. When you are adding more funds that already cover the same investments, you are just paying more expenses for no reason. I guess in the end I would just say, take their advice with a grain of salt and do your own research because no one cares as much about your money as you will.

Agreed :) Unless you don’t know jack about investing (or care to), in which case strongly consider outside – professional – opinions rather than just guessing to be done with it all… Like I used to do like a dummy, haha…

Here’s a comment from Smart401k:

“Investors may consider adding a defensively oriented active fund to their index holdings to reduce overall volatility. There are often times, places and conditions in which the benefits of passive management may be useful or favorable. The active versus passive debate does not produce a clear and decisive position that either approach is always and everywhere superior.”

I think this only sounds interesting with the $200 fee waiver. I can’t imagine paying $200 for a service like this especially because your company has to offer free education opportunities to you around your 401k and the investment company who offers the selection has representatives assigned to your company to help you pick the best options for you. When all else fails, you can always pick a target date fund and call it a day. That being said, for a free option, I would definitely be interested in what smart 401k had to say about the best investment mix for my clients.

I think taking advantage of ANY resources you can for investing – and esp your 401k and other biggie accounts – is smart to do. Whether at your company or online or anywhere really – as long as you actually DO IT :) I think that’s the problem with a lot of this stuff – it’s so overwhelming to people that they just give up before getting on track.

Very slick! I’ve heard about them but have yet to do any in-depth research into how they work. Like Jon said, I love all these new tech companies sprouting up to help people out with their finances in order to manage them better. From my experience, a fair number of plans offer something close to this, but they’re not automated and people often don’t use them. Something like this can make it much simpler to do.

I like the idea of this service, and I would be totally interested in seeing what they recommend, but only with the fee waived. I feel like I know enough(or think I know enough) to make my own choices for my 401k now…but if you had offered this to me 10 years ago I would have been thrilled!

Yeah, waiving the fee def. helps haha… And even more so when you don’t know jack about what you’re doing :)

Sounds like a slick service, J$! Thanks for the thorough review!

Interesting service, thanks for sharing it with us! I definitely had trouble selecting which funds to invest in for my 401K when I started at my full time job. A second opinion would’ve been nice!

Sounds good, I’ve been wanting to change up my allocation in my 401k. It’s great that there’s a fee wavier. I can see someone paying a one-time fee for the advice (I probably wouldn’t), but not sure I’d pay yearly because not much changes.

I have been using this service for several years now.

When I first started, I was able to compare my gains with those of portfolio recommended by my companies 401(k) management firm (fidelity). Fidelity always suggested the target date retirement fund closest to my retirement date. The Smart 401(k) offered a blend of 12 funds that took into account the fund fees, but not fees charged by fidelity for management. The Smart401k portfolio would also be modified quarterly, mostly by 1-2% in the different funds, but occasionally by much higher amounts based on their view of market conditions.

The Smart401k portfolio appeared to mimic the target date fund very closely with the exception that the drops were not as low and the rises tended to be a little higher on average. The net result for me was that for every 10k invested at the beginning of the year, I would earn back the $200 fee either through increased gains or reduced losses.

I was happy with the service when I was with my former employer. My current employer has only closed funds in the 401(k) which have no tickers and are not tracked on any of the exchanges. Smart 401(k) has made recommendation based on the prospectuses I provided, but I no longer have any means of running a check and balance on them. In addition, my current employer offers a similar tool (at no cost) through their investment wing that has provided me with a very similar suggested portfolio (differs only a few percent in each of the recommended funds). Also, since I started with the new employer, Smart401k has not changed their recommended portfolio, while the employer’s tools have offered slight tweaks each quarter. Another plus to my employer’s service is that I can have the suggested changes and a rebalance applied automatically each quarter.

My opinion: While I had the ability to maintain checks and balances on Smart401k, I liked their service. Now that I no longer have the ability to keep a check on their performance, I am not as much a fan of the service. This is because I have access to similar tools at no charge and because I am restricted to closed funds that do not have tickers that can be easily tracked. The second part leads me to question the accuracy that Samrt401k can provide in their analysis for my situation.

WOW! Thanks so much for the thorough analysis – this is great!! You’re the first person I know now that’s used them, and really fascinating to see how your experience was over the years. Thanks for taking the time to share with us :)

I like the idea of integrating a forum into an investing platform. When working with Vanguard, I always have another tab open for consulting with the Bogleheads lol.

Hah! Great idea :)

Just signed up. Will see and report back how they compare to my own intuition and what Personal Capital suggest my allocation should be for maximum optimization.

YES! Please do! That would be interesting to see indeed :)

I’m assuming we should do this once a year or ever so often with them? Which would mean we would start paying a $200 fee year after year? It doesn’t seem right to just do it once and forget it.

It’s def. smart to watch it over the course of the year(s), but it doesn’t necessarily mean you have to go through them to do so if you find it’s not helpful, or – in a perfect world – learn how to do it on your own :) But yes – you should def. be aware of what’s in your accounts as time goes on, and *especially* at least once to get you going. It’s probably not the end of the world if you set it up well once and then forget about it for a while.

Thank you for analyzing this tool J.Money, it really sounds amazing. I will definitely have a look at it.

I’m glad you found it helpful :) Please do let me know what you think if you end up trying it out!

I will definitely check this out as I started with a new job recently. I’m like you and just put everything in the Vanguard S&P fund they offered, but I’d be curious to see what this company suggests.

Yeah, always good to get other perspectives even if you don’t run with them :) I would bet my life they don’t recommend putting it all into the S&P fund, haha… That’s “too crazy” I hear.

Love another new service that makes it so much easier to get to our goals! It’s def one of the most confusing things about starting a 401k is knowing which funds to invest in and all.

Thanks for another great product review J$!

Glad you liked, friend! Hope you’re well over there :)

I signed up yesterday. Today I received an email from smart 401k via @mutualfundstore to call them back via an 800#. When I called the 800# 888-561-5487 there were a ton of ads and I couldn’t figure out how to reach the person who emailed me. The ads made me think the company got hacked as it was not professional. I now wish that I gave them no info.

Yikes! Sorry to hear – I’ve forwarded over the note to them. Def. not good :(

Hi Andrea –

Smart401k is under common ownership of The Mutual Fund Store and as such representatives from The Mutual Fund Store may reach out to new Smart401k clients to assist them with the onboarding experience. The call back number that was provided was 877-561-5487 vs. 888-561-5487. We apologize for any confusion, but rest assured your information is safe. Thank you for trying the Smart401k service and please let us know if you have any additional questions.

Thanks for the great review. It’s always nice to know where best to invest your money. Recessions are real and this investment can save you.

Signed up about a week ago and just got my recommendations yesterday. Really looking forward to this over the next year. I did, however, receive 3 phone calls so far from them asking me to set up a free financial consultation even after telling them no the first time. I’m fine with a few annoying phone calls if it’ll help me make a few more bucks in my portfolio, but thought it was important to note here.

Ugh, yeah – that can be annoying, sorry. Hopefully the recommendations and quarterly updates make it worthwhile!

Thanks for sharing. I was just talking with a friend the other day about needing to really look at my investment options for my 401k. Currently, I have a target retirement fund, which isn’t the best, but it’s easy. One of my financial goals this year is to better understand retirement investing and become more active in investments.

Target dates could be good just depending on what the other options are and your goals/etc. Let me know if you end up trying Smart401k out, and what they recommend in comparison :)

I signed up and they called me afterwards. They said they were setting up a consultation and that I could have another 401k right-sized, and that the company would NOT try to sell me anything. TheMutualFundStore.com called to set up a consultation. I show up and BOOM, they try to sell their services right off the bat. They weren’t interested in right-sizing a portfolio they couldn’t make money from. Now I’m dodging their calls to meet a 2nd time. Their admin fees are too high, and there’s of course (naturally) no guarantee of returns. So I pay the original admin fees on the funds themselves, THEN yet another mgmt fee? No thanks!

Jeez…..

I wish they would set up those calls *after* helping people figure out their 401k stuff first – I’m going to shoot them a note to ask. The service they’re providing here – Smart401k – for free should be all handled first. Then if people like what they’re about and want additional help w/ outside investments, great! If not, also great. I feel like all the calls are confusing people… I’m sorry about that.

Update: They’re holding off on follow up calls for the time being – thanks for all the feedback, guys! This should make the user experience much better :)

Anyone have any updates with this? I signed up today my 401k at the new job has only lost money so I’m hoping this will help.

Hey Pam – it usually takes a few days for them (Smart401k) to review and get back to you fyi :) As for losing $$ in the markets lately, you’re not alone – we’re all losing more or less these days. Just the way the markets go. It’s possible that you’re also not invested in the right funds for your goals too, but try to not let it discourage you. The $$$ is for the long haul and the beauty of it going down right now is that you can scoop up more for cheap each paycheck! So hang in there :)

I just got my quarterly results and for the first time my account is up. Last quarter it was down over 8% this quarter up over 6%. Thanks for the tip and free hook up.

Congrats! Just keep in mind the markets fluctuate like crazy though (as evidence of this week – having the biggest drop in a start of the year ever!) so it’s more of a long term thing than short term. Like, 5, 10, 20, 40 years :) So I’m glad you’re seeing a nice jump here, but don’t be too discouraged when future quarters are down. Which they will most definitely be. But the nice thing is that you now have an extra pair of eyes on your account to help you weather the storms :)

I just used this service from Lendtable and it is literally can’t miss for those who cannot afford to budget out enough from their paychecks to take advantage of their company’s 401(k) company match. They lend you the money to receive your full match and then just take a percentage once the money vests. Would highly recommend!