With interest rates so low right now, a question on every homeowner’s mind is, “should I refinance my mortgage?” And what about doing a refinance on a rental property?

It takes a fair amount of effort to refi — it’s just like qualifying for a brand new loan. There’s also hefty closing costs and fees… Is all that money and time worth it for a lower interest rate?

Luckily, the internet has smart calculators to help figure all this stuff out!

Let’s run some numbers on my current Texas rental property and see what a hypothetical loan refinance would look like. Let’s also look at a cash out refi, just for the heck of it.

Current mortgage on rental property

- Original loan amount: $136,500 (today there’s $123,235 left to pay off)

- Current interest rate: 4.125%

- Loan term: 30 years (started in 2015, so 25 yrs remaining)

- Monthly payment: $662 per month

I sent all my property info to a mortgage broker, and they were able to send me back a quote for an updated interest rate and closing costs for a new 30 year fixed rate mortgage. This is under the assumption that I have excellent credit (I do!), and that my income could qualify for the loan (I actually don’t think it will). Regardless, here’s the quote I got on Aug 13th:

New refinance loan quote

- New interest rate: 3.65%

- Mortgage term: 30 years (starts a new 30 yrs all over again)

- Closing costs: $7000

- Loan amount: $130,235 (current outstanding balance + $7k closing costs)

- New monthly payment: $596 per month

Now, before you start grilling me and comparing my rate to the killer sub 3% rate you just got on your home refi, please understand that an investment property loan is treated differently than an FHA loan. Investment property loans have higher interest rates (typically 0.5 – 0.75% higher), and banks have a little higher closing costs, too.

All in all, this refinance option would reduce my monthly payments by $66 per month, and add $7k to my overall loan amount for closing costs.

(I’m using a refinance calculator available on Realtor.com)

Is this a good deal? Well, it depends on my investment goals…

The purpose of refinancing

With a mortgage on the house you live in, most people want to pay down their debt as quickly as possible, reduce their overall interest to the bank, or drastically lower their monthly mortgage payment. These are the common reasons people refinance.

This being an investment property, my motives are a little different than a primary residence. I don’t really care about paying off the loan early, nor do I mind about the total interest paid over the life of the loan. My main consideration is increasing cash flow. This is the difference between the rental income and my expenses.

So for me, the biggest benefit of refinancing today would be the reduction in the monthly mortgage payment. This would be an extra 66 bucks in my pocket each month.

But, it comes at a price. I’d have to invest (or borrow) another $7,000 to achieve this $66/m reduction. In the picture above you can see it will take 8 years and 10 months to reach a breakeven point.

At these figures, I don’t think a basic refinance makes sense right now.

Just for fun, check out the total interest paid on the new loan vs. the old loan. If I was to go ahead with this refi, and keep the loan for a full 30 years, I’d end up paying an additional $10,229 in mortgage interest over the loan term. Kind of sneaky!

What about a cash out refinance?

This rental property has appreciated in value since I bought it 5 years ago. It was worth ~$189k then and now worth about $220k. This gives me an option to pull out some of the equity, while also refinancing to a lower rate.

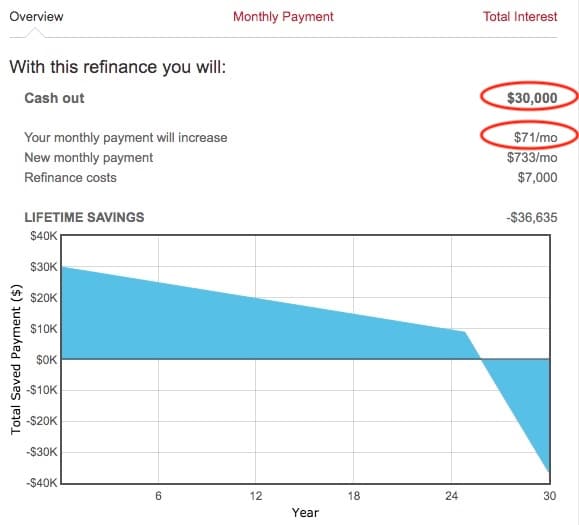

Most lenders will only loan up 75% of the value on an investment property, so I need to make sure my loan doesn’t exceed $165k (75% of 220k). Let’s see what the loan would look like if I pulled out $30,000 in cash:

Cash out refi option

- New interest rate: 3.65%

- Loan term: 30 years

- Closing costs: $7000

- Loan amount: $160,235 (current balance + $7k closing costs + $30k CASH OUT)

- New monthly payment: $733 per month

Now THIS is a really interesting option… Increasing my loan amount by $37,000 would only cost me $71 per month in higher mortgage payments. Where else can you borrow $30k in cash right now and have it cost you only $71 per month?

Is this a good deal? Well, it still depends on my investment goals!

What could I do with the extra $30k if I had it in cash right now? Where would I invest it, and could I make more than $71 per month from it in the long run?

Probably! I could stick it into the stock market and probably make a good return in the long run. But…

Bad news: I probably can’t qualify for a refinance right now. :(

The refinancing process is just as hard as applying for a brand new rental property loan. The loan officer will comb through every single nook and cranny of my financial life, and they probably won’t like what they see. :(

I have a ton of the good qualities needed: My credit score is excellent, my net worth is great for my age, I have plenty of cash reserves, and my overall debt to equity ratio is conservative. But the biggest concern they will have is my current personal income and last few years of work history. I’m just coming off a 2 year sabbatical, and right now my income covers my basic living expenses, but not much more.

I have 5 mortgages currently (for 5 different rentals). And although all the monthly debts are easily paid by the incoming rent, most conventional lenders want to know that my personal income can service my overall debts. Some lenders will take into consideration incoming rent streams as a source of income (maybe at a reduced rate), but it’s a tough sell.

Portfolio loan, private money lending, or commercial loan?

There is some hope. I could make friends with a small lender that favors real estate investing. I could put on a suit and tie, gather all my paperwork, sit down with the bank VP and mathematically prove to them that this cash out refi would only increase my monthly expenses by $71 per month (I can definitely afford this!).

But, since these smaller lenders deal with ‘riskier’ loans, they will want more reward for their investment. They will have much higher interest rates – possibly 2-3% higher – which puts me waaaay back to the start of this whole thought process… Will the new mortgage rate they offer me be worth refinancing? Probably not.

All in all, refinancing is something I’ll constantly evaluate. But at this point I think I’ll keep things as they are. :)

TLDR; Summary

- A standard refinance would save me $66 per month!

- But it would cost $7000, so the payback is almost 9 years.

- A cash out refi looks awesome! I could pull out $30k in equity.

- Unfortunately I can’t qualify for this (right now)

- I’ll be reassessing soon as my income grows/stabilizes!

I know a bunch of you guys probably refinanced recently … Tell me your awesome success stories! Have you done a rental property refinance? Any cash-out stories for reinvestment elsewhere?

Get blog posts automatically emailed to you!

I would think you can do better than this in the current market. I’d honestly try and get low 3’s and little to no out of pocket on closing costs. You would be significantly reducing your cash position for a marginal return on interest rates, and during a pandemic/economic collapse I would probably stay put with the cash if this were my only option.

I’d try to include any closing costs in the loan amount to minimize out of pocket costs. If I wanted to pay cash to save money on a mortgage, I may as well just pay down the existing loan. I think in a few months when my paycheck stabilizes I’ll take a better look and search for competitive quotes. It’s been a good exercise to go through regardless to see what the real savings would be.

Interesting comparisons Joel!

Yes, surprisingly interest rates are still low. Though, I think refinancing depends on the person and their overall situation and goals. I’ve known some to refinance for lower interest rates despite the closing costs needed to bring to the table. On the other hand, I’ve also known others to refinance to pull cash out to buy more properties. So, it’s definitely a personal decision!

I’m trying to be mathematical about it all, but there’s a part of this that comes down to comfortability and overall risk tolerance. It’s different for every person! I know lending is cheap right now, but taking on more debt is scary to think about too.

This was interesting to see since there are several smaller sticking points in this type of analysis that make these kinds of mortgages different than your standard mortgage. I knew the interest rates were higher for investment properties, but I didn’t know about the 75% LTV limit on the amount most lenders are willing to lend.

Well, I just learned another new thing… Apparently when you cash-out refinance lenders require 70% LTV, not 75%. (Not sure why my guy didn’t tell me this – I could have gotten screwed if I actually applied). Yes thee sticking points are frustrating. But I guess if it was easy, everyone would be doing it!

Here is another possibility. My Mom has owned rental properties for 40 years. She took a home equity loan (HELOC) on her primary home & used that $$ to pay off her first rental property. The HELOC was a much lower rate of interest as it was attached to her primary home…since rental properties are commercial loans they command a much higher interest rate. I’m not sure if you have equity in your primary home but just thought I’d throw out a possible option.

Thanks Debbie – Great info, and congrats on your Mom getting creative to pay off the rental mortgage! Unfortunately, I rent where I live so I can’t get a HELOC. But I like the idea of using cash-out to pay down other mortgages at higher interest rates!

Have you been following this new 0.5% surcharge that they’re trying to tack on? For any refi mortgage loans sold to Fannie Mae/Freddie Mac staring Sep 1?

Nope, this is the first I’ve ever heard of it. That ads like $650 to my closing costs and another 10 months to my breakeven point. Dang!

It has been pushed back to a Dec 1 start date as of this week. That fee was why interest rates were moving back up. They dropped for now, but you can expect the same to happen as we get towards Dec.

Cheers J. That was on my news feed this morning too and I think it’s good we all have another few months to figure out if it’s right for us and close!

Have you considered a no cost refinance. The interest rate will be higher to pay for the closing but it still might net you a savings. I made that move five years ago, although I since have paid it off. Another option might be to cash out refinance your primary residence at a lower rate and use those funds to pay down the investment property.

Hey FTF! I can’t cash-out refi my residence because I rent where I live. Love the idea though and think anyone who qualifies should consider that. (Be careful of tax consequences for peeps out there with Jumbo loans on their primary res! Only so much interest can be claimed)

I looked at no-cost and both these scenarios have the closing costs added to the loan balance, so would cost me nothing out of pocket. I didn’t know about the interest rate increase option, but my guess is the gap between my current one and the new still won’t justify it. (not right now anyway – I’ll keep evaluating as time goes on!)

Joel,

You may have heard of Dave Ramsey. He went bankrupt by financing rental property in the 1980’s. I think his plan makes the most sense of any, and so he would tell you to become debt free and pay cash for rentals. I personally used his plan and turns out he is right! When you have no payments all your income stays in YOUR pocket. Many people poo poo his plan but it really does work the best. Best wishes to you and your family:)

Hey Elizabeth! Thank you! I’m familiar with Dave Ramsay, and I even had the pleasure of meeting his daughter once at a financial conference. She’s an awesome speaker!

While I look forward to paying off all my debt one day, it’s not my priority (right now). Low rate loans I can use as leverage to boost my investment returns and grow my wealth at a slightly faster rate. I do pay a lot of money in interest, but I actually get to keep more money at the end of the day relative to my starting principal.

I fully realize that if I over-leverage or only focus on maximum profits, it will be like a house of cards and could come crashing down. But I’m constantly evaluating these risks and have a pretty conservative mindset compared to most real estate investors. I’m comfortable with the debt for now.

Congrats on your paid off rentals! Buying in cash is a solid strategy and glad to hear its worked out well for you. I love hearing everyone’s different experiences and viewpoints.. Thanks for sharing!

Joel

Joel, thanks for the insight on your refinance. We are refinancing our primary home from 4.5% to 3%. I can’t believe the difference in two years. We plan to keep paying the same amount under the prior loan to save on interest and payoff the loan much earlier.

YES!!!! That’s so cool to hear. Congrats Timias.

I think you can do better than $7,000 of closing costs. I refinanced a rental property in Texas and the closing costs (including title insurance) were only $3,500.

Mind shooting me over the lender or broker details? Great to hear you got it all done!