In celebration of “America Saves Week” (a real thing going on right now!), here’s a checklist to see how prepared or not you are ;)

Go down the list and see how many you can check off!

Per AmericaSaves.org: (my answers on right)

- Have a financial plan with savings and debt management goals. ✅

- Don’t rely on financial windfalls from gambling or winning the lottery. ✅

- No payday loan, car title loan, or other high-cost debt. ✅

- No credit card debt that is increasing. ✅

- In addition, no credit card debt or unpaid monthly balances. ✅

- Affordable (or no) car and student loan debt payments. ✅

- Save a portion of your income. ✅ (I save most months, but not a *set* portion)

- In addition, save at least 5% of your income. ✅ (I assume this includes investments too?)

- Have an emergency fund to cover $500 of unexpected expenses. ✅

- In addition, have enough in an emergency fund to cover three months of regular expenditures. ✅

- At work, contribute regularly to a retirement account. ✅ (#1 goal is to max it out every year!)

- Outside work, contribute regularly to an account for retirement. ✅ (IRAs)

- Outside work, make these or other savings deposits automatically. ❌ (I do it manually – much more fun, and I also never know exactly how much I’ll have that month due to being self-employed)

- Own home with affordable (or no) mortgage payments. ❌ (don’t own)

- Own home and expect to pay off mortgage before retirement. ❌ (don’t own)

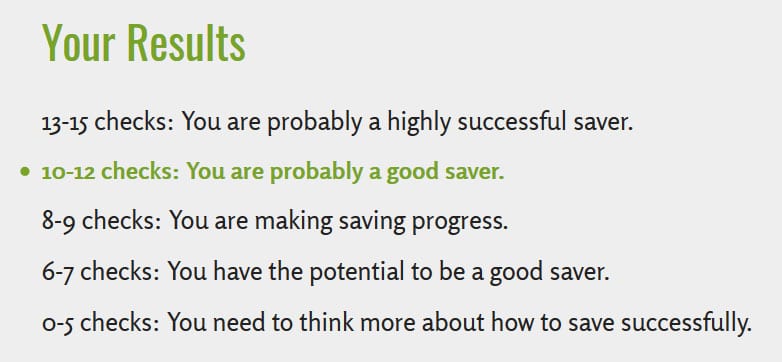

How’d you do?

12 out of 15 here, and once again get dinged for not owning a home ;) (Apparently home equity represents the largest source of wealth for low- and middle-income families according to America Saves… Which would actually make yesterday’s stats on 401(k)s make more sense!)

Here are the results key:

I like all the “probable” statements haha… Are we good savers or not??? :)

Still, a pretty good test to see where you are right now in your journey…

If you’re looking to amp it up a bit though, check out this article on 54 Ways to Save Money!

Also courtesy of AmericaSaves.org, and a handful of pretty creative ones in the mix amongst the usuals… (as well as a couple of resources I wasn’t aware of before!).

Here were some of my favorites:

Designate one day a week a “no spend day.” Reserve one night a week for free family fun. Cook at home, and plan out free activities such as game night, watching a movie, or going to the park.

Calculate purchases by hours worked instead of cost. Take the amount of the item you’re considering purchasing and divide it by your hourly wage. If it’s a $50 pair of shoes and you make $10 an hour, ask yourself if those shoes are really worth five long hours of work.

Place a savings reminder on your card. Remind yourself to think through every purchase by covering your card with a savings message, such as “Do I really need this?” Write the message on a piece of masking tape or colorful washi tape on your card.

Commit to eating out one fewer time each month. Save money without sacrificing your lifestyle by taking small steps to reduce your dining budget. Start off with reducing the amount you eat out by just once per month.

Lower the temperature on your water heater to 120 degrees. For every 10 degree reduction in temperature, you can save up to 5% on water heating costs. (I didn’t even know you could do this?)

Cut laundry detergent and dryer sheet use in half. The laundry detergent sold today is usually highly concentrated and powerful. Use the smallest suggested amount, and often you can use less than what’s on the bottle and still get clean clothes. In many cases, using less actually washes more effectively because there’s no leftover soap in your clothes. And tearing your dryer sheets in half gives the same result for half the price.

Organize a neighborhood swap meet. Here’s how it works: gather your friends and neighbors with kids around the same age and everyone brings gently used clothing, books, and school supplies, toys, etc., and receives a ticket for each item they bring. Each ticket entitles you to one item from the swap meet. If you contribute six books, you can leave with up to six new-to-you books. If you contribute seven items of clothing, you can leave with up to seven new-to-you items of clothing. All leftover items are donated.

Start with a goal of reducing your credit card debt by just $1,000. That $1,000 debt reduction will probably save you $150-200 a year in interest, and much more if you’re paying penalty rates of 20-30%.

Participate in a local Investment Development Account (or IDA) program. If your income is low, you may be eligible to participate in an IDA program where your savings are matched. In return for attending financial education sessions and planning to save for a home, education, or business, you typically receive at least $1 for every $1 you save, and sometimes much more. That means $25 saved each month could become several hundred dollars by the end of the year. Find an IDA program near you.

Get free debt counseling. The most widely available help managing your debt is with a Consumer Credit Counseling Services (CCCS) counselor. CCCS’ network of non-profit counselors can work with you confidentially and judgement-free to help you develop a budget, figure out your options, and negotiate with creditors to repay your debts. Best of all, the 45-90 minute counseling sessions are free of charge and come with no obligations. More info here.

Should we add these to our #FIRE Hacks spreadsheet? :)

(Actually, did I already tell you about this?? A reader of the blog put it together after last weeks #FIRE Hacks post and said we should keep adding to it so all the tips are in one centrally located place for people… I haven’t backfilled it yet from over the years, but if you want to download it and see the 17 from last week (or add to it!), you can grab it here: Fire Hacks Spreadsheet (Excel))

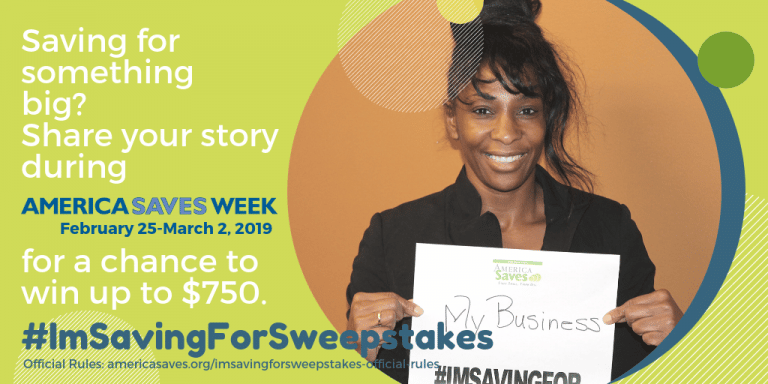

**Lastly, if having an “America Saves Week” wasn’t exciting enough (!), there’s also a $750 giveaway thrown in for a lucky participant who takes their “pledge” and shares it around**

Here’s a sneak peek of the pledge before signing your life over ;)

I [first name] [last name] pledge to save money, reduce debt, and build wealth over time. I will encourage my family and friends to do the same.

I’m saving for: [goal]. Each month, I will save [amount]. At the end of [number of] months I will have saved a total of [amount] to reach my savings goal.

To enter, and for more information, click here: #ImSavingForSweepstakes

Now who’s ready to save America???

Errr…. save, America?? :)

******

UPDATE: Got another resource recommended to me by a reader – “Have you ever checked out saverlife.org? It’s a non profit that rewards people for saving money! You have to save at least $20 a month for six months and they will match $10 for every $20! Only downside (for some) is that they will want to “attach” to the account to monitor that you are actually saving. 😏”

Get blog posts automatically emailed to you!

I’ve gotten America Saves emails for a couple of years now. They do a lot of giveaways (if you save $20 per month, they’ll give you $10, up to six months in a row). It’s obviously a program geared towards lower-income folks, but I love the fact that this program exists, and is encouraging people to save. The small town I came from in SC has more Payday Loan outfits than churches (and that’s saying something in the Bible Belt). Thanks for posting the savings checklist! I got 14 out of 15, because I’m a homeowner, but I don’t save in an IRA, just taxable accounts. :)

Nice!! You could probably get away with counting 15 out of 15 too since brokerage accounts similarly get the job done :) Wild on that payday loan/church ratio though, ugh…

I’m 10 but with a few tweaks I could probably get to a 13 within a year.

Here is a fun fact that “big detergent” doesn’t want you to know. The only reason they have indicator lines or pre-measured cups built into the lids are to get you to use more detergent than is required. High Efficiency washing machines only need at most 2 Tbsp of detergent to operate adequately. Using more is probably wrecking the insides of your machine prematurely, also, it leads to build up of sludge. Don’t believe me? Next time read your user manual, a small load = 1 Tbsp of HE detergent, a large load 2 Tbsp. 1 bottle should last you a very long time, but big detergent doesn’t want that info getting out…

Oh wow – that’s wild! But I totally believe it…. We do a lot of things we probably shouldn’t out of habit or what we’ve been taught over the years… I’ll see if I can find our manual when I get home today! But I can’t say I’ve ever seen one before, haha…

Looks like some people have heard about http://www.saverlife.org but it’s a cool resource to add to your savings! They match $10 to your $20 for six consecutive months! They also have a lot of tips and other information about the benefits of saving. There’s a few contests as well!

Love it! We need as much help as we can get in our community!

Well, I don’t regularly contribute to an IRA ($250 to a Roth in Mr. Bogle’s honor last month; before that not since 2016). But we do max out our 401k plans, so that helps. Otherwise, according to that checklist, we’re in great shape. And we just had a tankless water heater installed last week, to be switched on TOMORROW when Washington Gas comes out to connect our line; I’m looking forward to slashing our energy bills!

…and I think after this detergent talk I’ll install a light fixture above our washing machine. The basement is pretty dark around there, and I’m sure I invariably put in too much detergent just because I can’t see the markings that clearly. oops.

But then the light energy will offset it!! :) Very cool about the tankless water heater though…

Too funny you made a Roth deposit in honor of Bogle, haha…

J- Actually, you got 14/15….Since you don’t own a home, you can check off the last 2 items as they’re done, or N/A or whatever.

I got 12/15….A ways to go yet but it’s a work in progress….I dunno if we’ll pay off the home before retiring as we have 2 mortgages (own a rental property, mortgage a rental and mortgage a home). We will probably pay off the rental mortgage in 5 years, but not the home. We’d have to sell a property to get rid of the home mortgage.

Such a great little portfolio though!! And these tips are more for *individual* savings/debts too vs “businesses” – at least from my perspective – so I think you’re fine :) Actually MORE than fine!

Why not make the backwards Google Sheet so it is live? Everyone can view and check back on it as you add to it overtime.

Thanks for the list.

Not a bad idea :) Marking on my “ideas” list!

It seems that (especially in high property tax states) it’s becoming better NOT to own a home. !! We basically lost all our tax credits for home ownership and the money you are putting into your home could possibly be better off put into investments (although rent is high here too…)

Along the subject of taxes– My tax professional mentioned if you have several IRAs, etc it affects your deductions. I haven’t had time to research yet but something about the caps affecting one another and you have to use the lowest cap for the year?

Hmmm… can’t say I’m aware of any cap stuff or home owner tax stuff since I rent, but it wouldn’t surprise me if it’s all wonky right now with everything going on :( Shouldn’t change your reasons for owning a home or investing in multiple IRAs I wouldn’t think? Since you don’t do those for tax reasons primarily? (or even secondarily?)