Another month, another net worth report!

This marks the 106th month straight* of tracking all this, so in honor of this memorial occasion I thought I’d list out 106 reasons you need to be tracking it too :) Ready for some fun????

(*Nifty fact: 106 months = 8.33 years, or almost 1/4 of my entire life!)

Okay okay, we’ll only list out 9 for now, haha, but trust me when I say tracking your net worth is GAME CHANGING. If I could leave people with just one tip, it would certainly be that.

Here’s why:

- It helps you know exactly where all your money is at any given moment of time!

- It changes the way you *think* about money as you’re out there in the real world, knowing all your actions will be reflected in your wealth as time goes on.

- It also helps you make (informed) decisions much faster!

- You realize what’s in your control, and what’s not (cash flow vs stock returns)

- You become REALLY comfortable talking and thinking about money (perhaps even *too* comfortable when you catch yourself throwing numbers out loud to friends and it’s met with complete horror)

- You become super confident over time, even if you’re in debt or have a negative net worth (because you’re *working on it* and have a plan vs just keeping your head in the sand)

- You can track future performance better, based on all the months/years of records you’ve collected

- You can easily see how well rounded your finances are or not (look at mine – wayyyy skewed in retirement funds, but super light in other areas #FAIL)

- And lastly, it only takes a handful of minutes to track every month (the #’s always change, but the calculations don’t: assets – liabilities. It’s just copying and pasting (and then reviewing!))

So for the love of all money – please be tracking it in some form or fashion! I’ll be leaving my usual list of ways you can do so at the end of this post, but know you don’t have to be as obsessive (or voyeuristic) as many of us bloggers are with it either. We just want you to track it the best you can and make it *a habit*. And if you have to share it with anyone, do so with your pets – they’re always great at confirming how awesome you are ;)

Now to my own numbers from the month… A perfect example of stuff being in your control, and stuff that’s not! (I can’t even wait to see what the election does to it this next coming month…)

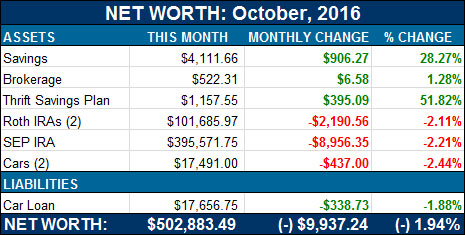

October Net Worth Changes:

CASH SAVINGS (+$906.27): A good month for the most troublesome part of our entire finances – our reserves! It’s taken a hit over the years with major life and business changes, but with the wife now back to work and me finally putting back on my hustle pants, we should start coming out of the woods more here… Never have I realized just how easy I had it back in the bachelor days!

BROKERAGE (+$6.58): Another nice/boring/inconsequential improvement here too, haha… The only nice thing about having smaller accounts laying around is that it’s always easy to see the improvements you make since you’re always putting in more than it is returning/going down :) Such is the case here as we’ve invested over $20 but were left with a net of $6 and change after the market drop. (This account is exclusively powered by Acorns right now btw, which rounds up all our transactions and drops the spare change into a portfolio for us… Been a year and a half so far and we’re up $500+)

THRIFT SAVINGS PLAN (TSP) (+$395.09): Same with this sexy account too! Big percentage gains as we pour in the money from ground level and watch it fill on up… Soon it’ll be taken over by the market fluctuations, but until then we just feed the machine and enjoy the positive territory as we go along :) (And not too bad having over $1,100 already after only a few months – way to go wifey!)

PS: She is fully funded into the Lifecycle 2040 fund which matches her personality/risk levels the best. But really all the TSP options are pretty killer – what’s most important is making sure to get all those free matches if you work for the gov’t too!

ROTH IRAs (-$2,190.56): Nothing too exciting going on here… Unless you have money to throw in and scoop up some funds on a bit of a discount! (Which we do not)

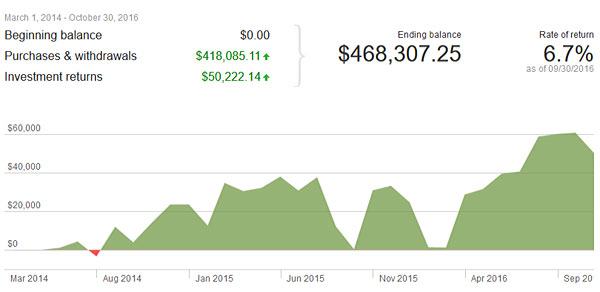

SEP IRA (-$8,956.35): Same with this guy… Although Vanguard just redesigned their dashboard portal so now we get fancier graphs :) Here’s a look at how our $$$ has performed so far since moving it all over in 2014 (we’re 100% in VTSAX – Vanguard’s “Total Stock Market Index Fund” (Admiral shares))

CAR VALUES (-$437.00): Just the cars doing what they do best – losing value! But also transporting us around and making our lives MAGNIFICENT too – so it’s a worthy trade off ;) Here’s how both ours break down per KBB.com (don’t even bring up FrankenCaddy or I’ll start tearing up…)

- Lexus: $13,593.00

- Toyota: $3,898.00

CAR LOAN: (-$338.73): Still restraining myself and not paying off more that the monthly payments (to build back up our cash reserves), but hopefully soon we’ll be back to chopping this down more… You can see how we got to picking up debt again here btw.

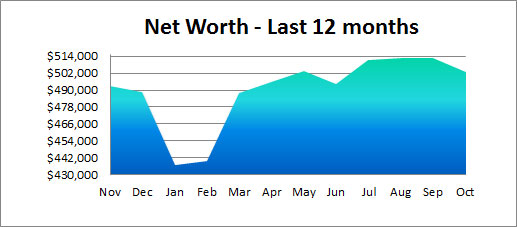

And now a look at how the past 12 months have fared! Relatively calm outside of that dip in January when we offloaded our house, haha… so glad THAT’s over with.

And lastly, a glimpse into how our kids’ money is going :)

And that’s October! How did you guys do? Anyone cross any awesome milestones? Anyone just staring out tracking their money for the first time?

For a look at how we’ve gotten to this half-a-million status over the years, you can see my Net Worth Page here, or to REALLY get your voyeurism on, check out our Master Net Worth Tracker list going on at RockstarFinance.com… We track over 200 financial bloggers ranging from negative hundreds of thousands of wealth, to positive millions! Something for everyone there, haha…

Here’s to a better November!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

It will be interesting to see how the elections go and how the market reacts. I think the market has built in a Clinton win. If Trump surprises with a win then I’d expect a bit more volatility. But what do I know!? I’m just glad it’s almost over!

I think you’re right. Hopefully we don’t get another Brexit style mini-crash, although it would create a good buying opportunity…

Now to just find large piles of cash to get ready to pour in if it crashes!!! Only hours away now!

No milestones this month, but the portfolio definitely took a hit and was down 2% in October but still up 6.5% for the year, so not too bad overall. I agree with your points about tracking your net worth. It’s such a great way to understand where you are and where you are going. I highly recommend it as well.

I’m looking forward to the election being over as well and getting some of this uncertainty out of the market. As a side note, I heard on the radio yesterday that they did an analysis and if Trump wins, they are expecting a 12% decline in equities vs. a Hillary win. If that’s not a reason to vote, I don’t know what is! :)

We had a dip in our investments in October too. It will be interesting to see how things finish up in 2016, given the new President coming in. Did the Lexus value dip after purchase? Let’s hope for a happier November!

Yup – it loses $300-$400/mo. Pretty freaky actually if you think about it. That’s like losing 1/3 of the value of my old Caddy every month – hah!

I couldn’t read while that horrified face was looking at me – had to do some creative scrolling to avoid him! If there is any milestone for me, it is that #5 – horror-inducing comfort in speaking about personal finances. I’ll be giving a talk about our experience of getting out of debt at the main branch of our city’s library next week. My husband had to tell me not to overshare our numbers, and I’ve respected that wish. I’ll be sticking to debt-to-income ratios to mark our progress instead of sharing our actual numbers. Hopefully, that will mean no horrified faces looking back at me : )

Haha… That’s so cool though, Ruth! I hope it goes REALLY REALLY well for you! Those listeners are a lucky group!

Doom and gloom everywhere right now – so many crazy predictions and terrible TV ads – can’t wait for it to be over.

We are sitting flat right now – 9our contributions are covering the drops ( probably won’t be saying that very much longer)

Will have a little cash sitting in case it gets real weird after the election

The market definitely appears to be on a yo-yo at the moment. Honestly in the long run it’s just noise so I try not to look at my personal accounts too much. The only change for us is I moved new 401 k contributions to favor equity to keep us in balance. Our net worth dropped this month for the same reason as yours. However we did have significant excess contributions last month. We wrote a few weeks ago about my wife going stay at home. Well what I forgot at the time was both her vacation payout and that work had her hang on for an extra month after we stopped daycare. So three months of daycare became surprise savings!

Oh wowwww! That’s the GOOD type of surprises to have too – you don’t get that every day :)

Nice job with the kids’ 529. This is the best time to save, while they are still small. I’m ready for the stock market to crash so we can move on. Right now, I’m afraid to buy…

Our October wasn’t good because we got a negative cash flow month. Our online income and rental income were less than usual so that threw us off. Oh well, we’re still good for the year. Heading off to Thailand next week!

FUNN!!!!! SOAK IT UP, BABY!!!

Last month, I complained that because of the market downturns I only made $4,000 when it should have been $10,000, and I hoped October would make it up to me. Yep, I said that thing.

Well, October was another record high earnings and record low spending month, but because of the continued market drops, I actually lost $414 dollars this month, the smallest change since I’ve been tracking it, and only the second drop in the last 12 months.

The good news is that my debt is significantly lower (43 months to go on the house!) and my cash is higher, and I’m predicting another record earnings with a patent related payment this month. Probably not a record low on spending though. My pool pump is acting up.

At the end of last month, I was at $269,395, but I’m already down to $267,703 this month. The markets hate uncertainty, and they just keep falling.

That is to say, I’ve lost almost $2,000 more dollars in the last four days, between Oct 31 and Nov 4.

Good thing all that matters is the end when it’s time to pull it all out :) Just keep pouring it in and watching it grow (and compound!) over the years! Easiest way to make money yet!

Nice net worth update. Just keep chugging along. You made it to the 500K mark!!!

I keep chugging along as well.

Yeah, I’m excited for a potential buying opportunity but like you I really don’t have the money to plop in, especially this time of year. All my money pretty much has a purpose and none of it is to sit and do nothing for me. I’ll just continue to dollar cost average I guess…

Oh and you better praise the sweet lord that you have medical through the government plans now instead of paying full retail price. Since you are a Marylander now you’ll appreciate this, my premium for my family will go up from 1000.11 a month to 1254.94, for similar but slightly worse coverage. Silver level (HSA of course ). Obviously, I’m happy I make enough to be able to pay it but its also ridiculously unfair that people who try to get ahead and have a non working spouse keep getting slapped down.

I’m pretty sure this was the intention of Obamacare, to make it so horrible that people beg for a single payer system. Well its definitely working on me….

Ouch :(

Ours was about to cross over $1,000 too until the wife got her job! Now it’s down to $450’ish I believe (for a much better plan indeed).

Crazy how much money you need just to be able to live and protect your family.

Thanks for sharing!

We had a loss for October too – as expected. We don’t have a very diversified portfolio right now either (it’s all in retirement accounts), but we plan to change that by buying a rental home within the next few months, which is exciting and scary at the same time.

Oooh nice! that sounds exciting – congrats!

Not much here…just trying to catch up with you!

#10 it’s a fun activity, at least for us weirdos :)

A friend, who knew we were saving for FI, used to make fun of me. “So what do you just sit around and count your piles of cash for fun?” I could hardly stop from laughing “Well… That actually is one of our favorite activities..”

HAHAHAHAHA

Sounds about right.

So, I calculated our net worth for the first time on Oct 31st. I intend to do so the last day of every month from now on.

I was quite pleased with the figures until we realised it almost all comes from the house. We are now on a mission to increase cash savings too and not just focus on paying down the mortgage quicker.

Seeing actual figures definitely helped to clarify my thinking. Thanks for the monthly encouragement to do this. After only a few months of reading it kicked in!

I use Mint, and their trending dashboard shows my monthly net worth trend.

I also get real time net worth updates, if that’s your deal.

I’m a bit of a luddite so typing numbers into excel suits me better than an automated app. However, I have heard great things about mint.

Way to go Rachel!!! Yes – def. changes your ENTIRE mindset for sure. Good part and bad parts, but so much better to see it all than to pretend something is what it isn’t.

I’m excited for your new awakening!!

I’m knocking on the 200k door, but it seems like that last 5k is like the last 5 pounds. It’s been barely budging lately. My hope is by the end of Dec!

I’m like that with 275. Almost happened in September. Almost happened in October. With the markets the way they are, we’ll all be lucky if we tread water the rest of the year.

Enjoy the final push! Once you cross it you then have to wait all over again for another milestone, haha… this is the fun part right now! :)

Our net worth went negative for the first time since starting to track it 7 months ago!!! only went down 0.27% so not too much of a freak out on my behalf. Another milestone is the emergency fund is fully filled!!! woot!

Damn good one, man! Emergency Funds are no joke – you’re def. killing me on that one.

Bravo! Looks like you’re doing splendidly. :)

October was a hard month for our savings, since we moved into the house and something breaks at least twice a week. Sigh. In fact, we were over budget this month by $500, which meant $500 less we got to sock away–boo!

Reason #138 I rent, haha…

Hope you’re in the clear for a while though :)

Agh! All my apps that I use to track my net worth are all screwy this month because I’m doing some rollovers. I know I still know what my real net worth is, but I like seeing that chart going up regularly!

“I can’t even wait to see what the election does to it this next coming month…”

So YOU’RE the reason for the market’s slump over recent days. It’s not because of the US election. Duly noted.

I really like your #2. Knowing our net worth definitely changes our actions, especially mine, as I am the person who manages expenses in the F2P household. We never want to see that number go down based on our actions (controllable vs uncontrollable, as you point out), unless it’s for a VERY GOOD REASON. That reason hasn’t yet to come up and we’ve been tracking for years now.

Hi,

I’ve follow your blog, Mr. Money Mustache, and Dave Ramsey. I’m genuinely confused about something and would love to know more about your rationale – Why do you have a car loan at all? You’ve got $101K in a Roth IRA, which is tax-free, correct? But you are losing money on interest payments on a car loan. Why not pay off the car today, and then redirect that car loan money back into your Roth IRA? Aren’t you paying an extra $5000 (guessing here) to the bank for no reason?

I’m just curious, because you say that you have to restrain yourself from paying more on the car loan, and I just wondered why.

Thanks for the great blog!

I think I can answer your questions

Its because the rate difference between the loan and the potential interest gained from investments.In the simplest terms , if you take out a $5k loan @ 2% interest but then invest that money and gain 5% then its like you are gaining 3% by borrowing the money. There are also other factors beyond that to complicate things even more. For instance that $5k over the course of 20 years compounds and multiplies many times over. Say you get 5% year over year, at the end of that first year you would have $5250, that extra $250 also compounds the next year and so forth…

Another factor is time value of money, which basically means $1 dollar today is worth less tomorrow. Basically if your rate is low enough, the loan amount is essentially 0% or negative, based on the amount $1 dollar can purchase during the loan term. I’m not going to get into a technical analysis just stating concepts.

One more factor (beyond the loss of compounding) is the opportunity cost of spending $17K or whatever he paid for the car all in one lump sum. Perhaps there are plans for that money that have not been made evident to us. Plans that would not be possible without that lump sum.

Lastly, I believe the reason he wants to pay off his loan is because we are all taught loans are bad and we can not deny there is a psychological component to having an outstanding debt.

Thanks Paul. Your explanation is completely logical. I have a very wealthy cousin who started from nothing and now owns multiple apartment buildings, and all because he purposely kept a mortgage. Every time one came due, he would take out a second mortgage on it. He once told me he did it on purpose, but I was young at the time and didn’t understand his rationale. (He retired this year at 50 years old).

Dave Ramsey says that personal finance is 20% knowledge and 80% behaviour, and I think in examples like this, those people with very steadfast personalities – who can withstand temptations – win. If I took out a 5K loan for the purpose of investing it (and my investments are currently making 8%) and then did invest it, it’d be a wise decision. However, I would be tempted to throw it on unexpected medical bills or other impromptu emergencies. The same with people who use cash-back VISA cards – it’s cool if you have the work ethic to pay off the bills at the end of every month. I don’t have that monthly efficiency.

That’s why I like the idea of being cut and dried with this. No debt. Chuck automated money at investments.

Lots of what Paul said + my own rule of never touching my retirement accounts no matter what. That alone has guided me through many decisions over the years, and probably the one reason it’s gotten so high! The old me would have been way too tempted to start pulling from it as it’s a slipper slope, so I just made a hard and fast rule that I just leave it alone completely so i never have to think/worry/debate about it ever again. That means I have to pay interest on my car loan of course, but all that was already incorporated into my thinking before I made the decision to purchase it :) I don’t mind paying a little bit of money to borrow some. My investments will more than make up for it anyways!

We had a dip in October but aren’t too worried since we haven’t changed our behaviors. I’m with you on #5 – sometimes I have to stop and check myself…”Is it really socially acceptable to drop personal financial details like this…?”

All this talk of fears of a crash after the election remind me of eight years ago, but it feels like there isn’t nearly as much to fear about the economy as there was back then, just a lot more hatred of the candidates.

Out of curiousity, how are you figuring the cars’ values each month? KBB or….?

Yup – KBB (Kelly Blue Book)

For me, I track a little differently… I figure out what my major, non-negotiable monthly expenses are, such as medical insurance, phone, housing, food, etc… and then I figure out how much cash flow I need to cover those expenses so that I am financially self-sufficient. Then, any work that I do goes to travel and more investing and saving. I’m happy to say that I hit my break even point this year at 42. However, if I had done things differently in my life, I probably could have hit this before 30. Too bad they don’t teach this stuff in college or middle school. As a math tutor, I have always said, we teach kids how to solve a quadratic equation, but we don’t teach them about real world stuff such as managing money and creating a life of meaning.

Ain’t that the truth..

Though playing devil’s advocate, kids could care less about personal finances at that stage, so you REALLY have to find someone to make it fun and cool (and make sense!) so they actually DO care and then take action! I can’t think of any of my old teachers that would have been able to do that :(

That’s why its good to have investments that you have confidence in – they provide comfort in bad times that they will recover. I like holding a lot in dividend ETFs(mostly DVY), so that I have the 4% yield while I wait for the price to recover. Even if it never recovered the yield will work out fine to support me.

Hey J Money, wanted to let you know, if you don’t already, YNAB has a new section for reports to include monthly meet worth and inside it shows your assets and liabilities. Since you talked about it later last year or early this year I have been onto of my money since then. Great blog, keep it coming!

Oh nice! Wasn’t aware of that, but of course I love to hear it! :)

I feel like my past year has been a milestone really. Ive been fortunate because of my real estate investments but a year ago in October I was at $336k and this past October im now at $440k. If I can grow it 100k per year then ill be a millionaire in 6 years! Woot Woot!

HOLY $HIT!

Well done, sir!

My net worth is up 9% this year, but mainly because the stock market is up. You’re right, the more you watch it, the more aware of where your money is going.

Like Primal Prosperity above, I also look at my spend rate, to work out how long I could survive on my savings if I had to. I reached my breakpoint some years ago.

A friend was worrying about her job. I worked out her net worth with her, also her spend rate (She’s been pretty frugal for years). Once I pointed out that if she lost her job and had to live on her savings, that she could live 15 years at her current rate, without having to sell her house. She thanked me, and said she would now sleep better.

It is a simple sum, but so valuable.

What a cool way to help someone!!! 15 years is incredible, haha… she IS frugal! :)

I track my net worth using Personal Capital, but shamefully I can admit that I don’t look at it every month. Since I’m in a bunch of debt it sort of depresses me, but I guess I can enjoy the fact the debt is decreasing. Great job on another awesome month!

No shame in that :) At least you know where it all is when it’s time/you’re feeling brave to check it out :) (And since you’ve already seen it all you still *know* what’s going on with everything – which is the main point of tracking it)

Net wroth went down in October but it’ll go back up eventually. :)

Since the politics genie has been left out of the bottle here…I wait in sweaty anticipation of Tuesday’s results…there is little question in my mind, as I have followed this election very closely, that Trump’s policies will hurt the majority of us…especially in regard to the markets. They know and we know that he is far too unpredictable and his policies are anti-trade and as a result are anti-business in many cases which is not good for anyone…can you say 35% tariff on Ford cars manufactured in Mexico? That’s crazy…

I really don’t want to start a political debate here…so let’s hope for a president that will help us all achieve our goals for financial security with a minimum of volatility and loss.

And yes, October was tough on us too…we’re down quite a bit since we are near the end of our savings journey and have a lot of money riding in equities.

I’m really surprised no one has chimed in here w/ your comment!

But I am glad – it’s gotten crazy out there already :)

Tracking my money is one decision I never regret. It helps me manage my money well and develop a kind of positive thinking with regard to money and debts.

I had a $10k drop this month, too! It was a bit of a punch in the gut, but it always makes me feel a little better to know it’s not just me!

I came out flat for the month (-0.03%). I guess that’s pretty decent considering I took a big trip this month.

I’m hoping to hit the 6-figure club by the end of the year, but no increase in NW this month made it a bit less likely. We’ll see what happens by Dec. 31st.

I’m predicting you hit it on my birthday – December 26th :)

In addition to the reasons you listed, I also have a tenth reason to track your net worth-it acts almost like a money diary. I’ve tracked mine for about 15 years now (at least once a year, and usually every few months) and sometimes I’ll go back through it looking for how my money’s life has changed over time.

Oh look, that’s where I got my new job! There’s when we sold the condo and bought our house. Look, that’s when we refinanced the mortgage. That’s the year my husband almost died of septic shock and everything took a huge hit. Aw, look that’s the year we got rid of all the debt except the mortgage! (All these are what I think about when I look back over the numbers)

Even though there’s no words in it, the net worth snapshots are like your moneys story. And they can help make sure the story it’s telling is the one you want to have-and if not you can take action to change it.

YESSSS!!! Great addition!!

And very similar to *blogging* too. So fun to go back over the years and be reminded of how everything was, and (hopefully) how far you’ve since come :)

Thanks for chiming in!

Congratulations on 106 months. I’m at 82 months of tracking myself, so looks like you’ll always have two years ahead of me. Tracking your net worth really is as easy as you say, it’s just copy/paste and updating the numbers in my Google spreadsheet. It takes about 15 minutes each month.

82 is pretty impressive too, sir.

The markets have been fluctuating crazily lately but that’s all good as long as we have some cash to deploy. I have been a bit busy buying up great ones lately. Good time to buy!

Mine didn’t drop too badly (less than $1k) but it’s still irritating to know it didn’t go up. I hit my initial target for the year, but I don’t think I’m going to hit my revised target. Sad panda! At least I’m still over $100k. I’d hate for it to dip down below that.

Almost similar % and numbers decline for me this month with less networth.

Well not much you can do about the IRAs. Mine is down too but since I have way less in mine the number doesn’t hurt quite as bad. :)

I completely agree – tracking my finances has been huge for me. I’m not a big spender but seeing it in black and white allowed me to see where my downfalls were. I can’t wait until the end of the year to see how far I’ve come! Last year was my first tracking so this is my first to compare it to. And #5 is soooo true!!

J –

Lost a few handful of thousands due to the market swings. My HSA and 401K have a contribution coming up on the 10th, hoping to capture some of the investments at a discount. Dividend reinvestment should be “okay” this month, but December will be the big one. Thanks for sharing the update, looks like you’re starting to see how much cash you can save now every month, good stuff.

-Lanny

The discount parts are the best!

It just dawned on my that time has really flown by, was it seriously October 2014 when you made the switch to Vanguard VTSAX ??

2 years gone by just like that WOW

Right??

And just think – in a cple more years we’ll come back and be like – “Remember that time we thought 2 years ago was old?” :)

Some days your the hydrant and other days your the dog. Life is not about perfection but constant improvement and hard work. This is especially true with our finances.

Hah! Love it.

October was so volatile for my portfolio. It’s been quite a ride this year. Hopefully I’ve paid the last of my big (thankfully not major) medical bills and can return to filling up my IRA.

I hope so too :(

Hey!

I have been reading many of your posts the last couple of months but I never comment because I am just lazy unfortunately haha.

This post hit home. I have been doing the net worth calculation for my own self the last 5 years and I am very happy with the results.

I started my first business in 2009 and through a stroke of luck, made it big (for my age atleast).

However, I used to squander money uselessly and in 2012 I realized that although I was earning enough, my net worth wasn’t really increasing.

I have changed all of that now. I bought a couple of houses, put them on rent and have been very careful with my money.

I have even started a personal finance blog so I can give other people tips about this.

Thanks for bringing things into perspective :)