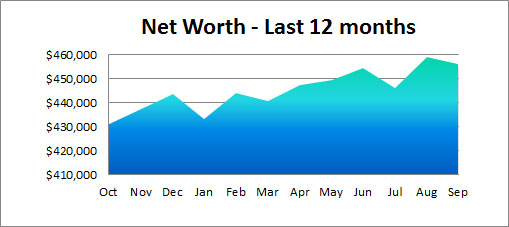

Happy October, hustlers! You ready for the pumpkins and beautiful fall leaves to start hitting ya?? And that perfect whether for jeans and hoodies??? (Mmmmmm….) My all-time favorite season, and what better way to bring it on w/ a little net worth update action :) I wish it were an *increase* to celebrate the turning of tides, here, but nonetheless it’s fun as $hit to track – am I right?

In a nutshell the stock market was lower than usual this month, and thus most of our investments followed along the same way. Mainly because we’re invested heavily in index funds. So when the market’s high, our $$ is high! And when it’s down, our $$ is down. But we’re firm believers in the long term success of the markets, so we just ride the wave until we’re old and gray one day and cash out. Or perhaps even when I’m young and gray if I can figure out early retirement quicker ;)

The only bright spot we had in September was in the cash reserves for once. But only because I offloaded my very last “non passion” site that netted us $8,000. We’re still very much leaking money every month as I work on refocusing and balancing that work/life/happiness trifecta. Ever since having kids I’ve slowly diverted down the path of life and happiness which doesn’t always equate to money ;)

Here’s how September broke down:

CASH SAVINGS (+$3,442.36): A nice increase due to the sale of that last site I mentioned, and hopefully soon more permanent earnings! The master game plan we’re working on is getting my wife back into the workforce once her dissertation is complete and she nabs that PHD status. Once that happens it’s back to making it rain!

529 College Savings (-$105.29): No big change here – just the market doing it’s thang…

IRA: ROTH(s) (-$1,093.59): Same with our Roths. We don’t dump money in here until the end of the year once we know how much extra we have to invest (due to business income volatility).

IRA: SEP (-$5,517.91): Same here as well. This is the big boy we max out every year no matter what as we don’t have 401(k)s or anything anymore, and I need to keep forcing myself to save for retirement regardless of business income… And by maxing out my SEP I get the mad savings with taxes every year too – a nice win-win!

Here’s how our investments have faired since moving to Vanguard (love these graphs they show you!)

AUTOS WORTH (kbb) (-$185.00): My wife’s Toyota continues to go down a little each month as is normal… And Frankencaddy, well, he’s just bopping along as usual hoping to collect another free check the next time a car crashes into him again ;) His engine still purrs nicely, however recently his cup holders have broken off making it quite the ordeal when drinking hot coffee on the road (yikes).

Here are the values of both cars – the Toyota via Kbb.com and the Caddy via JMoney.com ;) Actually, I tried buying that domain before but they are asking a LOOOT of money. So instead I picked up JMoney.biz to reflect *ahem* all my business and blog endeavors. Check it out if you haven’t before!

- Pimp Daddy Caddy: $1,000.00

- Gas Ticklin’ Toyota: $6,177.00

HOME VALUE (Realtor) ($0.00): Haven’t touched this since our realtor estimated it at $300,000. I don’t bother with Zillow or Trulia/etc since the #’s always fluctuate so much. Though, I do sneak a peak at USAA’s home monitoring service which pegged it at $305,000 last month which is pretty close!

MORTGAGES (-$674.80): I forgot to mention this bright spot up above :) Every month – no matter how much income we make or not – we always round up and pay extra towards our mortgages… It’s been such a habit over the years that I don’t even notice it anymore until we do these sexy updates. Give it a shot yourself if you haven’t tried already!

Here’s what’s left on our dang (rental) house:

- 1st Mortgage: $270,597.50 (30 year conventional @ 5.5%)

- 2nd Mortgage: $27,359.73 (HELOC @ variable 2.8%)

And that’s it for September! Nothing too exciting, but nothing too upsetting either. Just another dot in the timeline of our money :) If you’re interested in seeing how past net worth’s have gone (in detail), here’s a list of all 80+ of them over the years: J’s Million Dollar Journey. I don’t play around!

How did you guys do this month? Anything new and juicy go down? I’ll put in a good word for you the next time I meet w/ the money gods… Legend has it those who track their $$ have a much higher percentage of growing it though – so you might want to get on that if you haven’t yet. All it takes is 15 minutes and a pad of paper/keyboard!

#BOOM

![]()

PS: Here’s a list of almost 100 other bloggers who share their net worth too.

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Your September looks so good. With that cash saving, you’re surely on your way to financial stability. Mine is like what I got in the month of August. Hope to increase my savings but I think it won’t be easy as Christmas is coming (Christmas decor and gifts to prepare).

We’re index investors too–in it for the long haul (well, and to win it). I think your Frankencaddy might be worth more than the Frugalwoods-mobile. I clock our good ol’ 1996 Honda Odyssey at maybe $800? But she’s a great car!

My wife would gladly swap cars with you ;) She’s just waiting for the day we get a minivan!

I gotta tell you, I love my minivan! It’s somewhat ridiculous that we own one since we: don’t have kids yet, live in the middle of the city, and have to street-park at our house. But, it’s a very convenient Frugal Hound, Craigslist furniture, and roadside-trash-finds conveyance vehicle. Plus, it’s the car we have and we’re not buying another one :)

Ain’t no shame in that!

We calculate our net worth quarterly, so that’s on the agenda for today since it’s the first day of the quarter. We are also expecting a drop in the value of our assets, primarily because of the stock market. However, we still paid off a decent amount of debt this quarter so we will see how that all balances out. Hope you have an awesome October!!

Just off the top of my head, the market should be up for the quarter. Only really took a nosedive this past month. You may be pleasantly surprised!

Jay

September was pretty much the same for us…net worth down a little because most of our wealth is tied up in the stock market. Like you, we have a long term outlook and aren’t worried by the drops along the way. After all, it’s not wall-to-wall sunshine everyday.

Exactly… need the downs as much as the ups to appreciate this stuff! And, well, to get better deals on stocks too when available ;)

J$ you continue to rock, and the stories about FrankenCaddy are sooo funny! Same thing here… my retirement buckets are down, and I have to say it just gets me so mad every time they are cause it’s SO HARD to put $ away for retirement, ya know?… and then it’s like WAIT WHERE DID THAT &^%$ MONEY GO?! … aarghh. I am trying to retire from FT work between 50 and 55 (am not raising kids) … cause my mom is on her own and she’ll be 80 when I turn 50 so I figure caregiving will take up a lot of time… we’ll see what the future holds! In the meantime, I continue to love the J$ posts!

Keep hustling and investing! The market only really matters when it’s time to cash out – so if you’ve got a ways still it should be much higher/happier at that point :) At least that’s what we’re all banking on, right? So in the mean time you have to look at the downs as great opportunities to pick up more while they’re cheaper!

We were pretty much the same for September since we’re do largely in the market as well. It’s a relief not to have to worry about the day to day fluctuations and just keep chugging along with that long term mentality.

Just wondering, could you get that 1st mortgage rate down lower, or are you not planning on staying long? Usually if you can drop the rate by at least 1% it’s worth the closing costs, and many mortgage companies will do a rate adjustment with a quick phone call and signing of some papers? Have you checked into this? We used to do them all the time when I was in the mortgage biz. Impressive numbers as usual, my friend. Thanks for being a constant inspiration. :-)

We refinanced a few years back when we took advantage of some program, but now because of it we can’t refinance again :( Mainly cuz we’re barely above water and would literally have to bring $60k+ to the table to make it happen – which we’re not going to do. Plus the house is now a rental so I’m sure it’s stricter/harder?

But you’re right – 5.5% is crazy high these days. Though better than our 7% it used to be! :)

Oh yeah, the rental thing definitely makes a difference. Probably best to keep it as is.

Still look good J, even with the markets roller coaster ride. I have to get at our numbers, but expect big changes with our recent events.

We have a similar strategy to yours. We mostly invest in index funds and we are prepaying our mortgages (primary residence and two rentals). We’re also in it for the long haul so we don’t stress too much about the ups and downs.

Thanks for the reminder! I hadn’t updated my NW over the weekend since we were traveling.

The little payments to a mortgage make such a big deal. We’re close to cutting off our PMI payments but are going to roll over the ~$85 a month into principal payments. Doing this will cut off 2 years and 8 months off of the mortgage. We’re also going to continue to throw any leftover money at the principal too, and hopefully get out of PMI even earlier (target is 5 months early right now). Would love to pay off the whole f’er in less than 10 years!

YES! Great idea!! You will be The Man if you can do it in less than 10 – I’m rooting for you :)

I wore a hoodie for the first time this Fall! I felt so BA with the hood up.

And I just got a new freelance writing gig. This one gig alone will pay for all my living expenses. I’ve written for them before so I believe we’ll continue to work together well and it’ll be a long-term relationship.

So that’s good.

And I’m thinking of downgrading cars. We’ll see. I’m envious of your Frankencaddy!

Wow – nice man! Way to score that gig!

Happy October!

Even with the down market, all of my net worth numbers went in the right direction. Assets are up, liabilities are down. I can’t wait to get on the positive side of zero!

September was a trainwreck for us…. Replaced the plumbing in our bathroom, surprise new water heater because the old one broke, and I needed to replace the tires on my car. We were able to pay all of this with cash, but our emergency fund took a beating. On the plus side, I switched insurance companies and chopped our car insurance payment in half, our homeowner’s insurance premium decreased by $100, and due to a mild summer our monthly utility bill is decreasing by $50… So we should be in pretty good shape going forward.

I’m glad there was a happy ending to that comment :) Just remember that’s what Emergency Funds are for! It sucks, but so much better than throwing it on a credit card!!

I use the same strategy of dumping $ into the IRA at the end of the year because of my income volatility. I didn’t earn much this year, so it looks like I only have a couple thousand as of now and I know I’ll need some of it for taxes and I REALLY want to invest in myself in some other ways, so I’m struggling on what to do.

J, shouldn’t you qualify for an Individual 401k since you’re self-employed???

Yeah, I believe I could get a “solo 401k” just haven’t looked into it since my CPA said a SEP was good for my situation… Others here have commented that I’d actually benefit more from a solo 401k though, I’ve just been a bad blogger and haven’t spent the time researching :)

September was okay for us, but not the greatest. We had a few thousand in unexpected expenses pop up, and that was not fun.

I may start doing a net worth update. It would be in percentages since I want to keep some privacy (I already post my income updates!), but it would be fun!

I bet your readers would EAT IT UP. The more you disclose the more they like it :) Though I totally get the privacy. This is why I’m semi-anonymous here still.

Time to turn that cash into investments. Buy the market while it’s down. Think of it as a discount.

Jay

Yo J$

Enjoy the net worth updates, but why are you still paying 5.5^% on your mortgage? If I recall correctly, you should be able to refi just the house mortgage (and they wont bother looking at the HELOC) and knock that down into the 3-4% range.

Look into it, as it should save you a boatload of cash.

We refinanced a few years back when we took advantage of some program, but now because of it we can’t refinance again :( Mainly cuz we’re barely above water and would literally have to bring $60k+ to the table to make it happen – which we’re not going to do. Plus the house is now a rental….

Believe me – we really wish we could!

Nice, I just did my monthly total. Up a little bit but over a major mark over all. It’s been stagnant this year, but it’s been a good run and we’re so much further ahead than several years ago. I scroll up on my monthly list and see where we were just 3 years ago and we’re 150% ahead and it makes this last year seem so much better.

yes! a great benefit of tracking it over the months/years – you get to go back and compare and feel good!! :)

Have to do my net worth update tonight! I’m not looking forward to it too much because the stock market has been down and we’ve had a lot to pay for in the last month. Taking our honeymoon trip soon and we had to pay all the bills for that. Plus our property taxes and home insurance bills are coming it! Meaning next month won’t be great either. Still got 10% savings and investments in but nothing extra!

10% is better than 0%! Or negative cash flow like the state we’re in ;)

We all have ups and downs J in the stock market madness. The good thing is in the down months our investing dollars buys more shares. So heres to gettting more shares my friend.

It’s always inspiring to watch you kill it J! This has been a tough couple months financially for me (income) but my motivation to get ahead and stay stable financially is in large part because of reading sites like yours. I really appreciate it!

Awww well I’m glad these posts (and others from bloggers) are helping out. I’m always inspired by yours too – esp with the volleyball stuff – so we’ve got a great community here indeed :) I’ll send some positive income vibes over your way, okay? If it makes you feel better, my income is down by over 50% too! It’s not fun, but it’s only a phase… True hustlers like us will overcome it :)

Yeah, my investments all went down this month as well. That didn’t stop me from surpassing the $150k mark this month though :D That net worth of yours is going to take a nice healthy leap the next time the market turns around again though, so keep up the great work!

Congrats! $150k is a GREAT milestone!

I have definitely sacrificed money for a personal life and as my grandfather in law used to say “you never see a Brinks truck following behind someone’s funeral procession” so I feel good with that choice. You are fortunate that you got a great head start before the kids so you have some breathing room.

I count my blessings every day for all those years of working 24/7 before kids! You never know how life will change so it’s good to hustle/hoard money whenever the opportunities arise.

Looking good J. I think it’s just fine to divert to the life/happiness route for a few years. The kids won’t be young forever, right?

We’re down a bit in September, but I’m not worried. Actually, the stock market going down is great for us because we still have many years left in the market. It’s a buying opportunity.

I haven’t ever tracked my net worth before, but I do track my debt totals and my EF savings. Perhaps seeing my net worth number would help me too. Something to think about I guess :)

I think it would :) It’s always motivating to see the numbers go in the right direction over time whether they’re in the negatives or not.

Check out the bottom of our Blogger Net Worth List – some of those guys are in the $100,000+ negatives and still track it!

http://rockstarfinance.com/blogger-net-worths/

Love your site. Congrats on the sale.

I don’t know that much about buying a home. I’ve been renting for years — dropping $1725 for less than 500 sq ft.

I thought (could be soooo wrong) that if someone was planning to stay in a house long term (or not planning to move at all) that good idea to pay down mortgage quicker by extra payments, but I thought if you weren’t that the appeal wasn’t so great. Since you were going to sell. Probably missing something there.

Off to update my Oct numbers. Thanks for the reminder.

Glad you like the site! Thanks for stopping by to comment :)

I’m not sure if how long you live somewhere really determines whether you pay down your mortgage faster or not, as that decision depends on your goals and priorities, but I do know that it does go into the decision of whether to buy a house vs rent. If you’re only gonna live somewhere for a couple of years it usually doesn’t make sense to buy, but if you’re staying but for a half dozen+ then it prob does.

At the end of the day though it’s a personal decision so as long as you stay true to what’s good for your own situation then it’s all good :)

You’re truly an inspiration. Sorry to see that your net worth took a hit last month, but almost half a million isn’t too shabby lol The markets seem to be heading in a correction, so your index portfolio may take a little dive, but it’s only a hiccup in the grand scheme of things.

You know, ever since we got close to this “half a million” territory it’s been a lot harder to complain about stuff :) It’s nice to be more relaxed and soak it in after working for so long! Just gotta make sure I don’t relax *too much* since we’re still a long ways away from the dream of early retirement…

It’s cool that you do this for your readers. By being completely open and honest with us, you are giving a boost of motivation and showing that saving and frugal living are worth it. Thanks for sharing!

I’m glad it comes out that way as it’s exactly why I continue to post it all these years :) That, and the fact it holds me accountable since I know I’ll be blogging all my dumb mistakes to the world! Haha…

What is your process for deciding how much money to put in your SEP? Do you just leave “X” in your cash for “uh oh” money and put the rest into the SEP?

SEPs are based on a % of your business profit for a year. So I pretty much watch how it’s going throughout the year and do my best to have a rough amount stashed (usually just in my savings account) so that when it comes time to invest I can just xfer that puppy right on over… And the beauty of SEPs is that it helps save mad taxes too – which is why I max out the most I’m allowed to put in there each year no matter what that amount comes to :)

I’m always inspired by your updates, and this one is no exception – especially the way you are calm and collected by the drop in net worth.

It’s an inspiration how you are always focused on the big goal, and always have a plan or two in progress to get you there.

Personally I’m at the seriously considering a side hustle stage, but haven’t yet come up with an idea that’s more profitable than my day job. I dream of being location independent, and working from coffee shops etc, so I’m going to put more focus into this area now..

I’m calm and collected cuz I’ve seen how the market goes over all these years and I know I won’t be touching it for quite some time :) Much easier when you understand that!

As for side hustles – yeah, totally worth exploring. I’d start with the stuff you love or are passionate about first and then just see what happens. Almost every single person I know who’s successful with hustles or location independent jobs started things out as a hobby or just because they really enjoyed it, and it wasn’t until after when opportunity hit that their biz started to explode. Rarely do I come across anyone who was 100% in it for the money as you typically burn out before you get close to that goal in the end.

So think about all the stuff you enjoy and would probably do for free anyways, and then see if you can make any $ off that in the beginning. Worst case you fail but still have fun, and best case you hit your dreams! And potentially those you couldn’t even have conjured up because your path takes a wild turn while out there hustling in the real world :)

I had no idea you could make money blogging, and DEFINITELY would not have thought I’d be doing it full-time as a “real” job one day, haha…You just never really know with life…. the trick is just starting and then seeing what happens.

Your personal finances are so complicated! You have a whole lot to get your head around, but it looks like you’ve got it figured out. I would have a hard time taking all of these details into consideration on a regular basis. “Every month – no matter how much income we make or not – we always round up and pay extra towards our mortgages… It’s been such a habit over the years that I don’t even notice it anymore.” THAT’s the kind of personal finance I like. Not intimidating. Auto-pilot and smart : )

Complicated? All I have are savings, investments, and then a house? Haha…