Whelp, it was fun being a half-a-millionaire while it lasted!

Unfortunately with some major changes coming about though, especially in the car department, we took a big hit this month and for the first time in quite a while I’m actually pretty embarrassed about it all… Not enough to stop sharing our net worth with the world, but it definitely doesn’t help when you don’t even want to see it yourself :(

Still, it is what it is, and while we don’t regret picking up the car itself (in fact, we’re loving it! It’s so freakin’ comfortable!) I am starting to regret getting it from a dealer vs. private party and having to rush through it all. Especially after running the #’s and realizing just how big of a difference it’s made! In fact, I’ve been reminded of a few things throughout the past week and I’ll share them real quick before we get to the numbers here…

Maybe they’ll help you avoid paying more than you need to in the future yourself?

#1. Not being in a rush matters A LOT when buying a car. This was the first time I ever bought a car on a time crunch (we needed one within weeks before packing up and moving), so we not only had to find the right car for our family, but also the best deal all in the limited time we had. And unfortunately without watching the market for a long time you’re left with what’s currently up for sale at the moment.

#2. Convenience costs! Because of the time crunch (and lack of the vehicles for sale by private party, or at least the vehicle *we wanted*) we focused our search at dealerships so we can get in and get out and accomplish the mission. We chose Carmax because of how easy and enjoyable it was, but because of this we also paid a premium over what the same car would have cost in private hands :(

#3. When calculating the value of your car – especially for net worth purposes – make sure you’re looking at the right value! This has been the biggest shock so far for us, and mainly because I totally missed it the first time around! We knew going into it we’d owe more for our car than what it’s worth per the above two reasons (and was okay with it), but the part I overlooked was checking the “private party” value of the car in addition to the “dealer” value which of course will always be more, but what we were using to see if Carmax had a fair deal or not. The dealer value was only $1,000 off which as posted about was expected with places like Carmax, but of course when running your net worth reports you don’t calculate dealer values and instead use private party, or even trade-in values, depending on how you’d sell it if/when that time comes.

We plan on keeping it for life, but were quite surprised when we searched the “private party” value this week and saw it was actually $2,000 less than expected! Which is a huge difference! And probably definitely would have changed things, ugh…

#4. Buying even a used car costs a lot more than just the sticker price. Our Lexus itself was $18,000, but once you tack on the dealer fees ($299), taxes/titling ($900) and a warranty if you go that route (we did @ $1,859), you’re looking at a lot more over the price tag. And that’s not counting any insurance hikes you may get depending on the car you choose too ($30 for us) or even the financing fees if you go that route as well (we’re paying 3.45% currently). All things we knew were a part of the deal, but still stings watching it reflected in your net worth.

And lastly, this is further proof that I’m no “expert” at everything money… The media/other bloggers are quick to label us so, but the reality is most of us (or at least me) are just regular people trying to talk openly about our finances in hopes it helps people as well as ourselves. Sometimes we get REALLY GOOD at it and everyone wins!, and other times we suck just as hard as the next person and do our best to learn from it. The key is to take a little here and there and then use it to make the best decisions in your own life as possible and hopefully come out better for it :)

Anyways, all this to say that while we’re still very much enjoying our car and did our best under the circumstances, our best could have been a lot better and we’ll now be paying for it – quite literally. Though I guess it could have been worse and we picked up a car that we hated and/or couldn’t afford? That would have been pretty horrible!

Alright, let’s get down to the numbers now…

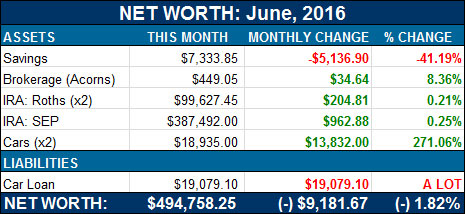

Here’s How June’s Net Worth Breaks Down:

CASH SAVINGS (-$5,136.90): Not *as* bad as it looks, but definitely not optimal. $2,000 of this was for a down payment on the car, but the other $2,300 was for the deposit on our new home. Which thankfully will be getting returned to us once we move out, as well as the $1,700 we put down on our old home three years ago. In general though we just need to be better about bringing home more income and the Mrs’ new job will certainly help with that.

DIGIT & “CHALLENGE EVERYTHING” ACCOUNTS: I decided to simplify stuff more and just condense all our savings stashes into one main place for these updates going forward. We’re still utilizing Digit and the Challenge Everything account for now (over $5,000 saved w/ Digit so far!) but the minimalist inside me didn’t like seeing all the extra line items anymore :)

BROKERAGE (ACORNS) (+$34.64): Nothing new going on here other than Acorns doing its thing and investing increments of money for us every time we swipe our card! In theory it would be better to have $0.00 going in as it would mean we’re not spending as much (hah), but hey – at least a few dollars gets put away in the process ;)

IRA: ROTH(s) (+$204.81): Same deal here – haven’t touched it and it actually EARNED money this month despite the BREXIT madness – imagine that?! I feel bad for all the people who pulled out and then didn’t put back in fast enough :( That’s the problem with freaking out about this stuff – you can never time the market in either direction!

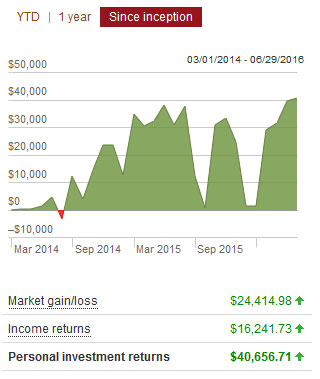

IRA: SEP (+$962.88): Same here as well… Here’s a snapshot of our Vanguard account that shows its performance over the two+ years since moving over into strictly index funds… VTSAX, specifically.

(Up down, UP down UP down….UP!!!)

AUTO VALUES (+$13,832.00): Looks a lot sexier than it is of course, but technically yes – our car values indeed went up when we took on the Lexus. I already miss Frankencaddy, but at least she’s continuing to bring smiles over at the National Veterans Services Fund where we donated her! It was nice not having car payments for 8+ years too!

Here’s how our two cars break down via KBB:

- Lexus: $14,811.00

- Toyota: $4,124.00

AUTO LOAN: (-$19,079.10): The whopper of the year… I’ve already laid out most of my thoughts on this, but needless to say it’s going to take some good hustling to knock it all out. A challenge we’re def. up to though or else we wouldn’t have taken it on to begin with (I make mistakes, but at least they’re somewhat calculated! :))

And that wraps up June! What a crazy month…

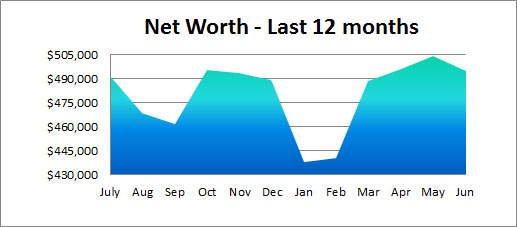

Here’s how the past twelve months have gone so far, for those graph lovers out there ;)

And here’s our boys’ net worths too:

That’s the end of net worth update #92! How did you do this month?? Survive BREXIT and have the stocks to prove it? :) Anyone else buy a car or a house or anything else that changed up your net worth a bit?

If you like reading these, you can see all other 90+ net worth updates here, as well as our constantly growing Blogger Net Worth Tracker over at Rockstar Finance which now has a staggering 227 net worths being featured on it ranging from (-) $532,304 all the way up to (+)$2,305,563! A perfect feast for number lovers!

See ya back here on Friday, friends… I’m ready for the new month, you?

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

It happens to everyone. Plus, you’ll be keeping the car forever so you’ll get your value out of it. You’ll be back above $500 million in no time.

Yeah, I guess since we’re keeping it forever the values don’t matter much in the grand scheme of things, just sucks knowing we didn’t get the best bargain we could have out there :(

Hehe, exactly… suck it to the last bolt! :-)

Very informative. We bought a used Lexus ES 350 last year and love it. I’m fighting the SUV urges so far. Once you have a kid everyone starts telling you how you need one…

Everyone likes to tell you a LOT of things once you have a kid! Haha… We survived just fine for four years with two kids in a regular 4 door car so you have plenty of time to not upgrade if you don’t want to. Convenience wise the bigger cars (SUV, minivan, etc) are a lot better, but that’s more of a “want” than it is a “need.”

Amen Brother. My parents raised 7 of us and we never had anything bigger than a station wagon. With the rear facing back seat up we could still only cram 8 people into it and we only had it for a few years. I doubt that we were ever able to legally go somewhere as a whole family but they made it work.

oh wow, haha… hardcore!

One the flip side my parent drove a 1985 ford escort for a large portion of my life. It was almost inhumane stuffing a 6’7 adult in that thing with 2 6’5 children… It was like that Simpsons episode with the tall guy in the beetle. “This is the largest automobile I can afford…” can’t tell you how many times I’ve been the butt of that joke.

Awww, haha..

This is why your readers keep coming back.The honesty is refreshing. If I wanted to see all the fake, good life events, I can go on Facebook. :) I’d rather the real-life discussion any day.

Haha, thanks man…

I def. do my best to keep it real despite everything in me sometimes wanting to run and hide :) It can be a bit much having so much attention on you whether for good things or bad things.

Thanks for the tips on buying a car. Mine is getting up there in age and miles! Hopefully I don’t need to rush in to anything!

Best thing you can do is just start looking around to get an idea for what model/type you think you’d want next, and then just keep an eye on the market until that fateful day comes :) That way you’ve already done all your research and the only thing you’re looking for at that point is the best deal you could find!

When we purchase a used car recently from a private party I failed to calculate the taxes and fees to register the car into the overall budget too. So it ended up costing a bit more. Sounds like a hustling we will go.

“Sometimes we get REALLY GOOD at it and everyone wins!, and other times we suck just as hard as the next person and do our best to learn from it.”

This is the best f*n statement Ive heard in a long time….

Thanks man, it’s the truth :)

J. You sound like you’re suffering from a bout of buyers remorse. I know that you know it but thought it might help coming from someone else too, Don’t worry about it. We all make the best decisions that we can at the given time and with the most information that we have available to us. Unfortunately, we aren’t perfect and never have ALL of the pertinent information. Could you have found a better deal it you had waited a month? Maybe. A year? Probably. But this could have very well been the best deal that you would have found before Frankencaddy died and left you in a situation where you had to buy a car with even less time and thus had to settle for a terrible option.

Remember, “you have to put your behind in the past.” ~ Pumba

That is true actually!! I was waiting for the Caddy to die before getting a new one (or actually, was going to try and go car-less and see how that went if we were staying put, but that’ll have to wait! haha…) so at that point I would have had to do the same scrambling…

So really the lesson is to get a good feel for what car you want a head and then just keep the eyes open for whenever you need to activate it or find a steal…

Appreciate the extra head on it, thx man :)

You can find decent deals on cars at car dealers if you’re willing to travel and you’re a pro at searching used cars online. In September of 2014 we found a 2012 Hyundai Accent hatchback with all the bells and whistles (Bluetooth, fog lights, alloy rims, etc) for $7,000. Granted it had 74,000 miles but it was all highway driving and a single owner car with no accidents. My mom worked in auto financing so she had access to Black Book,the more realistic auto value company (dealers don’t use Blue Book as it’s overinflated) and she could see that the price the dealer was selling this for was below average dealer price and not much above auction price. Why was it priced so good? Dealer was 1.75 hours away from a town greater than 10,000 people and it was a Ford dealer that specializes in trucks (not all rural folk like small cars). The dealer employees just wanted to smoke cigarettes (everyone smoked there!!!) and get rid of the car. I found the car searching all sorts of used car websites and it is awesome. Sometimes deals can be had even for fancy cars like yours too, although it may not be as easy.

NICE!!!

And hilarious about the smoking???? haha….

Nice to see your human! Definitely no need to be embarrassed though, you’re still posting some seriously impressive numbers here! And you’ll be back above $500k in no time. It’s crazy what has happened post Brexit isn’t it?! Don’t think anyone really knows what to make of it, but good thing you didn’t panic like some might’ve done.

Brexit was a windfall for me. Through sheer luck and coincidence, I cashed out of my crappy 401K like the day before the market mini crash. I let it sit in cash in my new IRA until the market got its head out of the toilet, put it all in an S&P fund and made $2500 in a day. I take it as a sign from God that taking control of my retirement savings was the right move!

Wow – you don’t see that every day! Well done!

I like your point that most of us aren’t professionals and still make decisions based on wants occasionally – we have made our fare share of mistakes as well, just part of the process.

To quote Cait Flanders: “Your net worth is not your self-worth.” OK, she said “salary”, not “net worth”, but same idea.

Such a small bump in the road, and the purpose of the bump? More upside for the Money family!

I had a similar “hit” for this year, with Mr. F2P telling me two days ago that he finally is pulling the trigger and planning the dream vacation I’ve been bugging him to take with one of his buddies for later this year. It’ll be a hit to our savings rate this year but it’s a once-in-a-lifetime type of trip. There’s no contest there!

We need to fuel our lives both now and in the future and you’re managing to do both.

That’s awesome he’s taking that!!! I suck at vacays! Except for our yearly family one which coincidentally starts this weekend – woo!

Enjoy!

Mr. F2P sucks at it too…thankfully, he has a significant other who’s good at pestering. It only took 2+ years of convincing, but I managed. ;)

We bought a used car last year and you are definitely right that the price ends up being a lot higher than you first realize. I think the part about having the time to find the “right” deal is huge and that is another benefit of being FIRE’d. The great thing is that your enjoying the car! If you didn’t like it – you’d have a lot more regrets!

Oh man, being FIRE’d and tasked with finding the best deal – on anything really – would be awesome!! Though from what I hear everyone in that position wonders how they ever fit in a day job – hah.

Posts like this one is why I come here. good work.

Really?? That’s so good to hear man, you have no idea… posts like these are the hardest for me to ever put out and gives me a killer stomach ache each time :(

I actually changed how i figured out my house’s value. Instead of trolling zillow, trulia, etc and instead of using purchase price i’m going to use the tax man’s assessment. It is somewhere in-between the others plus it will be more consistent since i’d only update it once a year.

Oh wow, that’s much lower for the house too – so you’ll actually get a nice surprise when/if you ever sell :) Though I don’t like using Zillow and the rest either – I used to just hit up my realtor once a year and run comps for me since it was semi-accurate based on the market at that point… And in fact when we eventually sold it we got the exact same price we had valued it at – $300,000!

maybe it is just that we bought our house from foreclosure and our area has been increasing pretty nicely post bubble but our tax assessment is higher than purchase price.

I was surprised to see my Vanguard account moving in a positive direction after Brexit, too! I was really tempted to buy some “cheap” assets during that period, but I didn’t really see the kinds of discounts I was hoping for. It definitely goes to show stock market hype works both ways! :)

It happens….but in the big picture your still on your way! You may have spent a little to much but you will make the vehicle work for you for many years. I have to say that I enjoy seeing that you guys are just like the rest of us….up and down and working for a better financial future.

Keep enjoying that riding…..it makes the payments easier ~

I’m glad you’re liking these Lisa :) It won’t be the last time I share something stupid I did haha…

Cool thing about life is we can learn from mistakes and hopefully do better the next time around. I got some good lessons from today’s post J. The big one is to not be in a rush when buying a car. Thanks man!

Lexus is a big commitment although $14K isn’t too bad. You are still very close to $500K level so I am sure you will jump up that hurdle relatively soon.

Our family just achieved $200K mark. Hopefully it grew from there!

Cheers!

BeSmartRich

Seems like you are confusing best car with best price. Yes, private sale might have been cheaper but that is just based on a printed price not the actual car including history of accidents, condition of the interior, engine, etc. With Carmax you got some knowledge of the car – plus you got a warranty plan. I’m not sure you really overpaid…two sweet boys in a safe vehicle are worth the extra paid in vehicle knowledge.

Very very true – I tend to overlook all the reasons that convinced me to go through Carmax in the beginning, haha.. This is what $$$ does to you – messes with your emotions! :)

Thanks for the reassurance.

Awesome, thats why I continue to read your blog – because you are so FREAKIN HONEST. We all make some good financial decisions and some bad, but the most important thing is to look forward and not in reverse. If it makes it any easier, look at all the DUMB things I’ve done and yet we’re still doin ok!

– Moved from a no income tax state to an income tax state

– Tried to time the market and missed out on some big market moves!

– Leased an expensive rental house when we had a cheap house in the no income tax state!

– Moved within a year and incurred expenses in the new state

– Lost money on the sale of previous house due to having to rush to sell it.

Still, its all good. If you aren’t making mistakes you aren’t trying to do anything difficult!

That was fun to read!!!

More please!! :)

Thanks for the *honest* update. Shows how much a car can set someone back, but I’m sure you’ll make up for it once you and the Mrs. get settled down.

Brexit was funny I know you shouldn’t time the market but it was almost certain there was going to be a big sell off the day after, and there it was. What was surprising is that the market did awesome the next few days and the S&P actually came out ahead after a few days! Like Brexit never happened! I’m sure there will be some long term ramifications but the short term results were interesting.

Yeah, that’s the only thing you actually CAN count on – people freaking out when major events occur!

Enjoyed your transparency and showing that even those who understand personal finance have bad months either, nothing is ever a straight line so I am sure you will be back over that 500k very soon. Keep up the great work man you inspire a lot.

The fact that you are telling us the truth behind the numbers and the emotion behind it teaches everyone more than a perfectly clean net worth update each month. No one is perfect (even though sometimes bloggers tend to only share the good things as well). We all have those times when things can’t go perfectly even if we “know better”. Can’t get better if you don’t take risks or make mistakes!

Now you can knock out the car loan quickly and move on to bigger and better things!

Thanks man :)

Someone joked last week that I only financed the car so I can show how fast someone can pay it off and that it was all a rouse, haha… I’m def. going to shoot for that latter part though!

I think June was rough for just about everyone, though it got better at the end.

If it makes you feel better, we have a $5k repair bill thanks to a renter who trashed our house and moved out without notice. Money problems are the ties that bind us. :)

Ugh, sorry to hear man… The things outside of our control are always the worst. And they’re always *surprises* too!

Hey, don’t worry about the car too much. Sometime you just have to forget it and move on. At least you got the car you wanted, right? We are all human and none of us is perfect. I make plenty of mistakes too. :)

That warranty is where you could’ve saved some money. Even if it says bumper to bumper, the fine print will exclude lot of things. There is very little chance that you will use it. It’s like an insurance. If you really wanted it for peace of mind, there are multiple plans that might be cheaper with a little more deductible.

I used to buy them (Dealers made me believe that every car will have costly engine or transmission problems) before. After two cars that reached 200k miles without any costly repair (only oil change, tires and brakes), I stopped buying them. Today’s cars are much more reliable than the older ones, especially the Japanese ones.

I would disagree. I have drank the warranty kool aid with every car purchased since 2001, and have made my money back every time except when the car was totaled two years after purchase. I got a refund on around 50% of the warranty cost so it wasn’t a total waste of $1800. With dealerships charging in excess of $100 an hour and 300% mark up on parts, a small repair or two can offset the initial expense. The warranty on the used truck I bought paid for itself in six months when the O2 sensors and catalytic converter went out. 7 ears and 80,000 miles later its still a good truck!

Well, I hope I never have to use it so that BK is correct up there, but the peace of mind I’m getting knowing that it’s there just in case is totally worth the cost for us… I probably wouldn’t have gotten it for a normal vehicle (at least the specific plan we got), but since we picked up a luxury one for the first time I didn’t want to chance it. I’m sure those rates/costs are even higher!

I could care less about anything else you wrote because this right here was screaming at me …. and this right here is why I follow you loyally. Keep kicking ass JMoney and keep it real.

>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>>

And lastly, this is further proof that I’m no “expert” at everything money… The media/other bloggers are quick to label us so, but the reality is most of us (or at least me) are just regular people trying to talk openly about our finances in hopes it helps people as well as ourselves. Sometimes we get REALLY GOOD at it and everyone wins!, and other times we suck just as hard as the next person and do our best to learn from it. The key is to take a little here and there and then use it to make the best decisions in your own life as possible and hopefully come out better for it :)

Appreciate that man :) It’s the truth! And sometimes we (bloggers) forget and let the publicity get to our heads!

I wouldn’t worry about the car. Moving seriously disrupts life and with everything you have going on, there simply isn’t enough time. Been there, done that. There is something to be said for maintaining your sanity when life is chaotic.

I was surprised we didn’t take more of a hit with Brexit, too, but rebound was fast! We are currently working on a mortgage refi, which is going to take some funds up front, but payoff very quickly in interest savings.

This article is exactly why I keep coming back to read your stuff – it’s real. You’ve spoken before about how you want to hear the good, bad and ugly and now you’re doing it too!

I’ll be honest, I LOVE my car and that’s a good thing with the amount of time I spend in it – but I really do NOT love my car payment. Knowing what I know now, I wouldn’t have bought as much car as I did. But I did, and now that the loan balance is in my cross-hairs I’ll be keeping it until it dies. Many, many, many years in the future.

Enjoy the ride, sometimes it’s just the cost of time+need+want+circumstances.

Thanks Liz, appreciate the kind words :) Let’s hustle out of our debt together!

I was thinking about getting an SUV but the gas mileage is tough since I have a long commute. I think I’m going to put off buying a car for a little longer. I asked you in regards to the SUV in your other post, but how was 2 car seats in a regular sedan? I have a Hyundai Sonata…probably the same size as your wife’s Toyota. Was there space for a small adult even with 2 car seats? (I ask since we have a newborn on the way and will be adding another car seat) While it’s usually my wife and kids, sometimes we need to transport another adult.

I answered ya on it! :)

But up – you can totally fit an adult next to the two car seats.The bigger the SUV the better of course, but you’d still be fine w/out that 3rd row. Unless we’re talking a more massive person then it would get tight quick. There’s def. more room than a sedan though, especially in the legroom since you can move the whole row back and forward in some SUVs.

Congrats on the new one to come – that’s awesome!

Sorry for the confusion. I was thinking about buying an SUV and originally asked you about space in an SUV for another adult with 2 car seats. Changed my mind and I’m gonna keep my sedan for now and not get an SUV so I was wondering if I can still fit an adult with 2 car seats in a sedan. Like you said…it’s probably not as much room but I guess on short trips we can still manage. Might upgrade to an SUV next year. Thanks!

ahhh, gotcha…

yeah, that’s do-able as well :) kinda tight if you’re tall/larger but def. do-able! my wife and my mother used to sit back there all the time in our Toyota Corolla. Not the end of the world at all (unless some car seats are a lot bigger than others?).

Still 70%+ in Intl stocks, 30% in US stocks. AND I have the five year underperformance ‘my portfolio returns suck’ numbers to prove it

Oh geez, haha…

Aww man sorry to hear on the net worth drop! There are always going to be bad months though. Just the way it works and im also sorry to hear if anyone is “labeling” you for any life decisions you make.

We always appreciate seeing how others manage thier personal finance and its called “personal” for a reason, its going to be different for everyone and everybody is in their own unique situation.

I do feel your pain on buying from the dealer though, I have never bought from a dealer and have always bought via private party (mainly craigslist to be honest). It just always seems you can save money going private. No biggie though, you’ll bounce back!

Sometimes you have to take a step backwards in order to move forward. That sounds awesome and totally cliché, and I’m not necessarily sure how the Lexus will help you move forward financially, but it will increase your overall happiness and enjoyment, from the sound of it. Moving to a new area and having your world turned upside down is stressful, so in that sense, if a new to you car helps stabilize emotions and is far from breaking the bank, I think it’s worth it.

I’m still flabbergasted about your Lexus. Don’t tell MMM about it, he could get violent ;)

I just have to feed him some beers and he’ll be okay ;)

Life doesn’t go in a straight line. It’s ok to take a step back once in a while. You won’t even be able to find this bump in a couple years!

Money is such an emotional journey. Can you imagine if 8-years-ago J$ would be so troubled to have dipped slightly below half a million in net worth?

My month was turbulent, but it ended well. I’m at the end of my first quarter of tracking my finances closely and I have seen a big percentage change. I hope I can keep up this momentum and get away from -$150K sooner rather than later.

Hah! good point. 8 year old J$ would have probably still bought the car, only with no money to his name haha… and then probably sold it once he realized what he had done :)

And I hope you can keep up that awesome momentum too!! It’s game hanging once you track it and see how all the actions affect you/your wealth!

No need to beat yourself up about the car! It really doesn’t seem that much based on your household income. With the monthly payments as a business expense, it ain’t no thing!

I like to buy private party b/c they usually are willing to put the sale price much lower than reality so the buyer can pay a lower purchase tax. It’s already double and triple taxation.

why did u take out a loan for the car when you clearly have the money to cover it… I get not wanting to dip into the savings but the hit your taking with the interest will take a way from what you could save monthly wouldn’t it? sorry if this sounds condescending it’s not meant to I’m really just curious behind the thought process

Not condescending at all – it’s a great question :)

While we do have the money in investments, we don’t actually have it in straight cash which is what I only allow myself to spend else it’ll become a slippery slope of pulling from it more down the line. So the hard rule keeps the assets growing and I act as if it’s not even there.

But even so, with all the fluctuations going on in our lives right now I probably still would have taken out the loan as I know it will get paid off sooner than later and don’t mind paying for the convenience of it in the meantime. I used to be scared of debt back in the day, but now it doesn’t concern me as much because I know it’s temporary. (If I didn’t trust myself though, there’s no way I’d ever take out some again!)

Sniff…Frankencaddy…sniff You were too young! Jk but seriously, I know it will be hard to give up my car when the time comes. Still, a Lexus would be nice ;)

It def. helps it sting a little less for sure :)

Though I do miss dear Frankencaddy already!

Well, that is the beauty of being financially responsible and having money in the bank. You have a great opportunity for your wife to pursue her career and sometimes you need to make quick decisions to pursue the right opportunity. I think they call that Opportunity Cost, right? Having money in the bank can make these transitions much more convenient and smooth, rather than having to pinch every penny. I’m sure you will make it back quickly with her going back to work.

I have moved around so much, I can’t tell you how much money I have left on the table. But it was always to pursue better opportunities.

Additionally, I looked at your net worth chart and it looks like you went from roughly $5ok to $5ook in 8 years. That’s pretty darn good!

Thanks, it’s been a wild ride so far and def. hoping the trend continues :) You’re def. right on the moving around for better opportunities too! The more open minded you can be on that (whether moving to different areas or just different projects/jobs) the better chance of growing all around… Learned that quick from growing up in a military household.

I had the same experience two years ago when I bought my Scion from the dealer… I wasn’t in a rush per se, but just wanted to get the whole thing over with. After it was all done with, I felt awful for a few days when I realized I should have been able to buy it for a lot less. But then I paid it off quickly, so I ended up saving a lot off the interest, which I suppose made up for it a bit. :)

I was also surprised that Brexit didn’t have a huge effect on my investment accounts! Mine went down a tiny bit, but nowhere near what I thought.

The paying it off quick def. makes everything a lot better, haha… well done.

I love your point about making the best decision in the circumstances… And sharing openly and honestly. Aren’t we all just trying to do our best?

I am excited because as of the end of June I have paid off $4,827.50 of my debt (gasp!). I have just come out the other side of a divorce. We were never on the same page about money and my ex-husband spent and spent until all of the credit cards were maxed out. Legally I was stuck with half – a staggering amount of $69,769.20 – and no spousal support despite that his income was 2.5 times higher than mine (because of the laws in the state we lived in). I relocated to lower my housing and cost of living expenses. And changed jobs to somewhat increase my income (I choose to work in the nonprofit sector). I have a budget – it’s extremely tight – and a plan. If I follow my plan I can be totally out of debt in 5 years. But I have been in my new location and new job 3 months and feel sufficiently settled and emotionally prepared enough to get serious about pursuing a side hustle. So maybe things will get a little easier a little bit sooner. There are lots of fingers to point about how and why in my situation, and advice to dole out about how I should proceed. But the bottom line is that the situation is what it is, I am now fully in control of my financial future, and I am doing my best to get myself upside right … And I’m sure my journey won’t be perfect. And that’s ok.

YES!!! You sound like you know exactly who you are and what you want – I love it! Congrats on your $5k slaying so far – no easy feat for anyone! Keep going!! :)

Sorry for your car regrets :( We also bought our last through a (small) dealer and had to pay taxes. Probably won’t go that route again. I think we were too enamored with the lack of rust to think straight!

Small bumps in the road to reach your big destination, in my view. I am sure that you’ll be back on the half a mil mark. I just bought a car from the dealer, used, and I’m wondering if I was the one taken for a ride.. Hmm… But I shouldn’t think so much about the little things along the way, just the bigger picture of achieving my dream of FI!

I hope you can come to peace with it :) Putting this all out in the open for me has helped with reading everyone’s responses! Maybe doing the same on your blog will?

I haven’t read through all the comments, so I apologize if this was asked already, but did you not use USAA car buying feature? It was really, really easy and saved us a couple of hundred dollars.

Awesome! I’ve heard great things about it actually, but assumed that since there’s no negotiating with Carmax that it wouldn’t be as helpful? I’d love to try them out in the future when the timing is better so we don’t have to rush next time. Glad it worked out for you!

Certainly motivational. I like how you keep it true to what you’re really doing. Things come up and you must adapt while still trying to maintain your goal. I’m no where near where you are in terms of net worth, but I have my goals. Keep it up!

I can understand the security from buying from a place like CarMax. Especially after my last private party experience. I thought I found a great deal on a mini van. So I bought it from a private party. And regrettably, I was too cheap to do a vehicle history report. I few months later, I’m going to the mechanic every other week to fix issue after issue. I then decide to do a history report, only to find out the title was branded because a previous owner had rolled back the odometer! I odometer read 70k miles. But i did some digging, and find out it had as many as 299K! I ended up selling the van for half what I paid for it, fully disclosing that it was branded. Lesson learned, pay the $10 for a vehicle history report.

Ouch :( It seems more and more dealers/people are actively going out of their way to give out free car reports online to help woo customers and it certainly helps! Now whenever I see one that doesn’t show it red flags automatically go up, haha…

But I agree – def. worth paying for :) I always take the car to my mechanic too before purchasing when buying through private party and that gives me peace of mind too, even though they don’t always catch everything. And if the seller doesn’t feel comfortable with it then it also sends up red flags!

The brief Brexit crash was actually a good buying opportunity, though it is easy to say in hindsight. I think when adding money from a bank account via Vanguard, the transaction doesn’t post until the next business day, meaning the price you see now is not the price VTSAX will be at when your “buy” order actually posts.

I would agree given the much lower value your Lexus minivan shows for private sales that you paid too much. However, many others make far worse decisions—I have young friends who literally have 15%+ car loans due to not understanding how credit works (meaning, they didn’t have their first credit card or student loan until AFTER the car loan and got their loan at a used car dealership).

With such high liquid net worth, why do you choose to pay 3.45% interest plus credit inquiries when you could just buy the car outright? Why do you have an $1859 warranty, which is clearly a money-maker for the warranty guarantor, when you could easily use your savings as your warranty? I suppose you are benefiting in the 10% “mix of credit types” portion of your credit score by having a car loan, but this seems no more worthwhile to me than keeping a credit card you don’t use that has an annual fee, just to avoid the hit to your average age of accounts from closing it (which doesn’t even occur until 10 years later, as far as I know).

Even most rewards checking accounts do not offer a 3.45% return. Most outlooks for the stock market are tepid compared to returns in recent years. A 3.45% return with no risk to the principal is pretty good.

I’ve been reading your blog for a while. You are definitely still a half-millionaire since your net worth estimates are very conservative. You aren’t including the value of most of your possessions, and you have barely any debts. Very smart.

Thanks man :) Yeah, actually just got an offer for the blog and my other project which raises the worth substantially more, but I never count on any of that until it’s actually a reality so that’s why I don’t include that stuff (I turned down the offer, btw).

As for liquidating some assets to pay for the car, it’s too slippery of a slope for me – I never like touching investments cuz it would tempt me too much to make it OK to do for other stuff down the road. And I honestly don’t mind taking on some debt and paying for the convenience of it since I know I can pay it off at any time and manage it responsibly. Plus, my investments will make much more than 3.45% anyways over the years :) And actually gonna spend some time and try and get it refinanced lower too as soon as the chaos winds down….

thx for stopping by btw – just checked out your site, your background is pretty impressive! especially in the speaking stuff – always admire that about people as I hate it. Keep hustling :)

Thanks for replying and checking out my site, J. Money! Toastmasters has been great… when I started 2 years ago I was super nervous but after being a club president and giving two dozen speeches I have improved greatly. It’s not really “public” speaking per se since you only have an audience of 10–20 people you already know, typically, so it’s a good segueway into more anxiety-provoking environments.

As for my education, financially I find it a very interesting topic. I still live with parents and have all my degrees (AA, BS, MA, starting PhD next month) from public community colleges / universities. This is so much cheaper than going to private institutions or moving away (though not as exciting). It must be awful to come out of undergrad with $100K+ debt which is quite common with pricey private institutions. Alarmingly, what is becoming more common is that people incur debt without ever finishing their degree! Might be a good blog post topic.

I can definitely understand the “slippery slope” dilemma, and I too think the VTSAX index fund will continue to yield more than 3.45% annually. Heck, it yielded much more than this over the past 10 years, even considering the 2008 crash.

I am glad you turned down the offer for your blog—I am sure it wouldn’t be as good. So many blogs turn bad when revenue generation becomes the #1 priority.

Best Regards,

Richard T.

Thanks man :)

Cars are not assetSSSSSS. Depreciating in value every day unless it’s a classic, collectible car.

I agree they’re not assets-assets, but I like seeing them in my overall financial picture especially since they’re items you can easily sell and convert to cash – which is an asset (unless you only choose to put in “income-producing” assets, in which case that wouldn’t fit either). I don’t put any of my other belongings in there – not even my coin collection or website values which would def. skew things – but thankfully we’re all allowed to track whatever we wish anyways :)

Nice article. I like your humility.

A few years ago a car I owned broke down right in front of an auto dealer. Wife and kids were with me, and I needed a reliable car. To make a long pathetic story short, they totally fleeced me. Don’t bring your kids along when buying a car!

Ouch!

Yeah – one of the reasons we went so quickly as we did was because we had someone to help watch the kids while we were out shopping around. No way you can concentrate and make rational decisions with them around!

Love your blog! So do you not include the value of your house in your NW calc? Thanks!

Glad you like it!

Nope – no mortgage, but only because we don’t have one ;) We prefer renting vs owning.

https://budgetsaresexy.com/2016/01/we-sold-our-house-no-more-mortgages/