And just like that, we wrap up another 12 months of exciting net worth tracking… That was fast! (And shows that taking stuff bit by bit pays off in the end! Literally!). If you’re not tracking your worth yet, I really recommend it. So in a year you can feel just as sexy as the rest of us do right now ;) The *habit* of it all is more important than the actual numbers starting out – that part takes time…

As for our December numbers, it was nice and steady just as it was in November. Which I’ll take any month of the year. When you’ve got a solid system down (ie control of your expenses and tons of money invested in the market) you quite enjoy when nothing *major* happens ;) Shows you’re def. on the right track, at the very least. And, oddly enough, we literally almost increased by the same % mark too! Last month we were up by 1.42%, and this one 1.40%. Another reason I’m glad y’all convinced me to track %’s now – it’s another fun thing to compare!

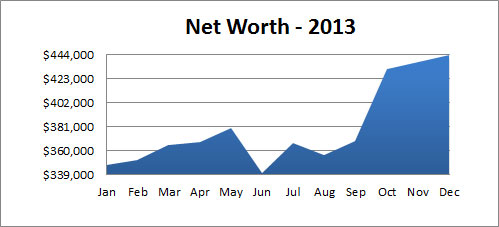

I’ve also updated our chart for the entire year of 2013 too – it’s at the bottom of this post. I highly encourage you to pump one out too so you can see (visually) how your year went – it’s kinda neat.

Here’s How December Broke Down:

CASH SAVINGS (+$5.90): We squeaked by on this one! A few lottery tickets, or a cup of Starbucks, and we would have gone into negative territory, haha… Probably the ONLY time I’ll say I’m glad I didn’t splurge on either ;)

529 College Savings (+$85.50): It’s been a while since we’ve pumped this little guy up, and now w/ a 2nd bambino on its way, it’ll be another long while to come too. At least until business picks up, or the wife lands a job, or I inherit millions from a long-lost cousin/etc. Basically, this isn’t a priority right now (staying sane is).

IRA: SEP (+$652.52): Nothing new added to this pot either, but we’re right around the corner of maxing this out again as soon as my accountant and I are done running the numbers for the year (yes, I use an accountant because she saves me sooooo much money! I would marry her if I could!!!). I’m guesstimating I’ll be moving around $15,000 into it.

IRA: ROTH(s) (+$1,750.01): These have been put on pause as well, but as soon as we max out that SEP and I do a quick review, we’ll decide if it’s smart to then max out these bad boys too. One for me, and one for the Mrs. – both under the 2013 tax year. I’m currently leading towards it right now cuz I don’t want to break my 5-year record of doing so!! But I gotta be smart and make sure our cash reserves are good first ;) Now that I’m old and a dad like that, ya know.

IRA: TRADITIONAL(s) (+$3,381.37): No changes here either, at least with amounts dropped in ($0.00), BUT, while I’ve been saying it for months now, I’m finally ready to pull the trigger and merge all this junk into one account and be done w/ this 2-year old IRA Test once and for all. It’s time to get back to streamlined and *simpleness* again. I’m quite excited for this – and how I’ll be doing it – and will post about it as soon as it’s all in the works… All giddy just thinking about it!

Here’s how they currently break down, though:

- IRA #1 (NOT Managed): $78,937.51 **Leader for two years now

- IRA #2 (Managed, USAA funds only): $72,968.11

- IRA #3 (Managed, ALL different funds): $73,765.10

AUTOS WORTH (kbb) (-$55.00): Now this one has a BIG change in terms of valuation. Namely, my car is TOO OLD to be tracked by KBB.com now! UGH!!!! I guess there’s a 20 year limit, and we’ve now crossed it :( So, going forward I won’t be able to track it on a monthly basis as we have been – harumph. That being said, I did venture out to a new site to see how others do it (Edmunds.com), and according to them my pimp mobile’s worth exactly $1,244. $600 less from what KBB has been pegging it recently (WTF?). So, in an attempt to stay conservative and just lock in a value from this point forward, I’m taking the difference of the two and just calling it $1,500 flat. Which I think I can reasonably get if I were to try to sell it at any point in the future… So I’m cool with that.

Here’s the value of both our cars now (for some reason the Toyota went UP $300?):

- Pimp Daddy Caddy: $1,500.00

- Gas Ticklin’ Toyota: $6,351.00

HOME VALUE (Realtor) ($0.00): As for our house, we’re still keeping it at the $300,000 we evaluated it at over the summer with our realtor. He thinks we might even be able to get $315,000 from it (at least back in July), but we’d prefer tracking the lower amount and being pleasantly surprised once/if the day comes where it does goes for more. After all, that’s the only time when you can – for certain – put an exact price on the thing. And unfortunately for us this is still some ways away since we’re very much under water, ugh…

MORTGAGES (-$652.46): House value aside, we sure chip away at the debt towards it every single month! I swear it feels like we magically pay an extra dollar more every month off the principal too, haha… To which I attribute to rounding up every time we pay our bills :) One is for $1,860-something, and the other $62. So we round up to $2,000 and then $200 – automatically paying off a good $280 extra on top of what’s already paying paid off via the amortization schedule. It’ll all add up to one sexy little pay off in the end! I can’t wait!!

Here’s what’s left on ’em:

- 1st Mortgage: $275,369.39 – 30 year conventional @ 5.5%

- 2nd Mortgage: $28,630.74 – Maxed out HELOC @ a variable 2.8%

And there you have it! 2013 all wrapped up with a pretty little bow on it… That graph above tells the whole story: $105,000 increase in just one year – I freakin’ love it. I’m tired as $hit, but hey – it’s not called hard work for nothing, right? And a few years from now all that money will be making its OWN little baby monies helping the pot grow faster and faster, all the while I’m on that beach sipping mojitos… I can take some pain in the mean time :)

Your turn. How did you do?? Are you better off than you were last January? What worked and what didn’t?

Again, I put these updates out there not to boast, but to help motivate those who need a little kicking in the pants. And hopefully you get some good ideas too and at least understand the importance of *tracking* everything. I couldn’t tell you what was in my checking account 6 years ago, nonetheless what my net worth was (or what net worth even meant), but now I can go back and revisit all the numbers over the months and use it to my advantage!! Even those dumb crap months – they all paint a picture, and it eventually leads to a Mona Lisa… Or, better yet, a painting like this.

To a prosperous 2014 :)

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Dude! You are an IRA King! Nice work on rocking them for every angle.

I love being frugal and all, but isn’t it time to upgrade to a new used car if the one you’re driving now fell off the KBB map? It’s been my experience that once a car gets past a certain age / mileage, it costs more to keep it running than it does than to buy a slightly younger used model.

That may be, but since I barely drive it anyways (once a week?) it doesn’t really cost me too much… But the odds I fast track to a newer (used) car gets increasingly closer as baby #2 is about to arrive – so we’ll see ;)

I’m not so sure. I’ve had good luck with ancient vehicles. Just do all of the scheduled maintenance and you’ll be doing your car a big favor. It makes me cringe when someone tells me that they’re 5,000 miles late for their oil change. Arrrrrrrrrrrrrrgh!!!

Nice! And a 30% increase in one year. Great job J$. Now get some sleep.

Gotta do my best now before the next baby comes!! I’m squat out of luck then.

My net worth had a similar meteoric rise this year related to the market run up, but how real is it? Of the market had had a 15% correction in December, the markets would still have beat their 30 year average performance. Does this mean that we have bubble value in our net worth? My doubt puts a pallor over my net worth, even with it not increasing by the same percentage as your’s.

Who knows if a bubble is here, or coming, or what really… But at this exact point in time, it’s real as real can get :) And all we can do (in my opinion) is keep saving and hustling and let the power of time do its work regardless of what’s happening around us. I don’t mind down months/years as I know long term all shall be well…

Definitely motivating me! I’m going to start tracking. Though meager – everything has a beginning! Thanks

Damn straight! We all (exceptions aside) start from the same spot: the bottom. The trick is figuring it all out sooner than later, and hopefully when you’ve got plenty of time to let the magic work ;)

Nice 2013 J$! I’m sitting down tonight to see how the year end up for us.

WORK IT!!

You are so close to breaking even on that mortgage … 304K owed, 300K value. Two more months!

Great progress this year.

I was just about to say the same thing. Not the underwater anymore!! Should be out in just a few months. THAT will be a good feeling.

I’m glad y’all are saying something because that’s totally slipped my mind!! I’ve *NEVER* been not underwater that I don’t even know what that feels like??? Haha… except for, maybe, the day I signed my life away ;)

Nice work J, especially on the IRAs! We’re working with our account as well to see where exactly we should be in terms of our SEP & Roth. It looks like it’ll be a nice sum, just wish we wouldn’t have kept so much of it in cash with how crazy the market went last year.

True, but everyone knows timing stuff like that is a joker’s bet. Had it gone the other way you’d have lost your money for the SEP!

I am very excited by the idea of one day getting to contribute to an SEP IRA (sure, my 401k has a match, but it means that I am tied to my employer!)

Look up Roth IRAs! That’s usually a perfect way to invest outside of employers, as well as grow earnings that are tax-free!

Paid off almost $15k in debt, opened a Roth IRA, got a 401k at my job (switched it to a Roth 401K), and we have more in our saving account. Here’s to hoping I can top that in 2014!

Hot damn! Rock it, girl!

That’s awesome.

We’re up a huge chunk too and couldn’t have done it without sites like yours motivating us.

Goal for 2014 is to fully fund my own Roth from only eBay sales. I’ll have a running tally on my blog!

Love. That. HARD.

(And totally going to stalk your blog now)

J. Money, your net worth graph is insane!

I maxed out my Roth IRA in March last year, and forgot to get ready for the automatic withdrawals at the start of this year… I accidentally overdrew my account, but I’m hoping my bank will refund the charge. Also, combining my IRA’s and reducing the number of websites I had to log into to check them made managing my $ significantly easier.

Call them right up, and speak to a manager if the 1st person says no! If it’s your first time, and you’re a good customer (which, of course you are ;)) they’ll totally wipe it for you.

And I’m all about combining accounts and simplifying financial lives too. I’ve done like 80% of it so far and I can’t tell you how easy it’s made my life…. Next up – all my dang IRAs!

Awesome increase! 30% is not something to laugh at.

(I hope no one’s laughing! ;))

NICE! Our 2013 gain was only about $20k. I didn’t track it. I’ll be tracking mine this year, and I can only hope that 2014 is half as successful as your $105k gain in 2013. Great work!

You too! $20k is a heap of cash, no doubt about it.

I started tracking my and the Mrs. net worth about a month ago when I found this blog. Over the last month we are up about 25K to 1,029,895. That includes investment and bank accounts, house and rental house but not other assets that are hard to value such as jewelry, furniture… I am not including the cars right now as they are newer so not much equity… and I am part owner in a small business that I would not consider sellable so its really more of a job than an asset. I also made a personal loan to someone of a not insignificant amount that I am not including… no issue with it at all but not something I would put on the smartest thing I have ever done list.

The net worth breaks down to 51% is in the 2 houses, 49% in cash and investments. We are putting away about 20% of our income each month and the investments are doing well so I would expect the cash percent to overtake the houses very soon.

Rock on, man! I can now say I rub elbows with another millionaire out there ;) I’m workin’ on it, but man does it take some time, haha…

I love seeing the huge jumps your net worth made towards the end of 2013. Way to finish strong.

I am kicking around the idea of getting a 529 even though we don’t have kids, putting some cash in it, and letting compounding work its magic…then transferring it to the kid later. What do you think? Good planning or just crazy?

I think it’s pretty brilliant, if you ask me. And, if the odds that you have kids are pretty high. I’m all about taking advantage of all those tools out there to have money grow tax-free! And what’s the worst case? You cash it out and pay taxes/penalties on the earnings? (I honestly don’t know cuz i’ve never researched, so that is both a serious, and rhetorical, question, haha…). However, all that said, I’m sure there are other places to invest that money without any kid-attachment to it that would probably be better – if you’re not doing them already.

Hi J.Money!

Got a question for you. You currently have about $370,000 saved in IRAs. I believe you are around the same age as me, in your early 30’s. If you were to stop making contributions now you end up with 1.2 million (at 4% rate of return) or 3.7 million (8%) 30 years from now.It’s hard to say what the market will do in that time but 4% seems nicely conservative and I think you would be more likely to end up somewhere between these two amounts. I’m not sure what your retirement number is, but it seems like this might be getting close. I’m curious what you are aiming for? How much do you plan to contribute? At what point will you consider directing your money to other uses? While I’m not sure you can oversave for retirement, I think there is a balance between saving for the future (long-term) but also the shorter term future (before retirement). For me I am planning to retire early so much of my savings does not go into retirement accounts. Though I do still have an employer sponsored plan and contribute to a roth IRA. I have spent alot of time lately thinking about what percentage to I want to tie up in funds that I can’t reach until I’m 65 versus those I want to have access to sooner. I am curious to hear your take on the this!

Great question! And even BETTER calculations you put up there – I’ve never checked that out specifically – that’s dope!

To be honest, and this is going to sound weird coming from a finance blogger, but I don’t think about the future much. I save and invest and do all the “right things” you’re supposed to do, but my brain just can’t comprehend that far out so I do whatever seems smart at any given point in time until my situation changes. Which these days seems to happen every 3 months!

I guess the ultimate plan is to “retire early” (which means me just doing pretty much what I’m doing now, except no needing to worry about money or do side stuff that I don’t enjoy), so I do my best to keep my head down as best as possible so that one day when I poke back up that day has come ;) Not the best way to do things – without a plan and all – but I don’t like major plans much anyways and I find by doing things this way I’m much more flexible.

I will say, however, that you’re the 2nd person to mention having money tied up in retirement accounts may not be the smartest move if planning to retire early, and that’s now actually on my mind. A lot! Haha… I never thought of it!!

So now I read MadFientist.com, and JL Collins, and Mr. Money Mustache more to get my mind right and see how to take advantage of all those tools more. With this new early retirement point of view… I’ve still got a ways to go, but people like you are helping so thank you so much for bringing this up!!

I totally understand how it can be mind boggling to think about the future! I’ve come up with a sort of framework for helping me think about retirement. One is money needed from beginning of retirement to age 65, so let’s say 40-65, and then the next is the amount from 65 to rest of your life. Now of course the money you have from 40-65 will probably (and ideally) not be spent so I see the money I am getting at 65 as a sort of bonus. And and I can contribute to this bonus tax-free which makes it very appealing. However, where the money is really needed in the 40-65 bucket, since this is the first nest egg. But there are no special accounts or tax incentives for this bucket, so I think it is less appealing to invest in. I would say you have the 65+ bucket covered and since you do mention wanting to retire early, I guess you have some thinking to do about your 40-65 bucket! Maybe we should pose this question to some other bloggers who retired early and see what they about investing in retirement accounts vs investing in general account?

Check out these two posts:

http://www.madfientist.com/retire-even-earlier/

http://www.madfientist.com/ultimate-retirement-account/

He’s all about figuring out how to use retirement accounts to still retire early :) Lots of tax hacking stuff really – similar to this one which is also a pretty interesting reads:

http://www.gocurrycracker.com/never-pay-taxes-again/

I’d love to get into the “early retirement” mindset more – even if I don’t technically retire yet… just knowing I *could* would be amazing! So you’re right – I need to pay attention to that first bucket :) Only I hope it’s the 35-40 one instead! Hehe…

I have a nice little graph set up for my net worth for the year. Started at -20k and ended up at 2k. It was really cool being able to see how the progress went over the course of the year. I plan on doing a yearly graph tracking it from now on because I enjoy seeing the numbers. I’ll probably start tracking percentages too once I get my net worth up a little higher. Right now increases for a single month will be over 30% and that’s just ridiculous.

Haha… ridiculously AWESOME!!

Wow! Great job for just this past year! Perhaps you will take a nice long break before Baby #2 comes along! My question was are you planning on trading in the caddy anytime soon considering the value and the growing family?

Thanks! The value of the caddy really has nothing to do with any decisions I would make (it could be worth $2.00 or $20,000) since I love it either way, but the baby is a whole other scenario ;) The wife’s been pretty good about it lately, but I have a feeling the whole minivan talk will be coming around the corner again soon… And when she’s finally serious about the whole thing, I’m betting I give up the Caddy at that point (and get an SUV! ;)). Either then, or when it finally breaks down… bless her little heart.

Seriously well done bro. I’m not quite where you are, but I’m on my way, especially with motivation like this. Off topic, but you’re right on- mojitos are the best. I’m not to ashamed to admit I would take one of those or a pina colada over Johnny Walker six days a week and twice on Sundays. Best of luck to you in 2014.

Haha… but only if they come with tiny little umbrellas right? ;)

Congrats! That is fantastic, one day I hope to be as successful as you are! Here’s to a prosperous 2014!

Over $100k increase net worth in only one year is freaking AH-MAZING! Awesome hard hustling J Money! Compared to last January I was over $57k in debt. One year later I’m at around $38k. :)

Hot diggity! I bet if you fast forward a few years it’ll be $38k too. In the green AND with an extra 0 or two!

J$ have you considered refinancing your primary home loan? I know you are just above water but you should look into the Harp program the government has established. I thought we were under water too but loan to value didn’t matter and I was able to refi to a much lower rate! Any local mortgage broker or quicken loans would be able to provide more details. I would bet you could refi to a 20 year loan and keep your payment the same ( due to lower interest rate) and that principle would start to really drop!! Just found your blog tonight and will continue to follow. I’ve been tracking my net worth quarterly for the past 5 years. It’s always motivating to see it moving up each time you track your progress.

Cool man, welcome to the site :) And yup – believe me, I’ve call my mortgage company (Chase) almost every 3 months to just check in and see. And I get denied one call after another, haha.. Mainly (from what I gather) because I had already taken advantage of some program out there a few years ago when we refi’d from our original interest-only loan, and since we did that these we’re omitted from the new programs out there. So at least I got one refi in when we did!

Also, if you’re interested in seeing how we were gonna try gaming the system, here’s an idea I had earlier in 2013 that I had to abandon:’

https://budgetsaresexy.com/2013/01/my-new-refinancing-plan-brilliant-or-stupid/

And then the follow up:

https://budgetsaresexy.com/2013/03/bye-bye-american-refinance-plan/

I’ll be tracking my networth each month for the first time in 2014! January 1st revealed…we are really, really, super far in the red! We don’t have any high interest debt though, just student loans and mortgage. I’m hoping that we’ll be able to keep a positive attitude as we slowly creep out of the red zone.

I haven’t been reading your site for very long…is there a reason that you have so much liquid cash? It just seems like a lot to me!

Good! Tracking it becomes second nature after a while :)

We have a ton saved up in cash for a number of reasons:

1) I’m self-employed and the only income maker of our house

2) My wife is super conservative (and I don’t blame her!)

3) Part of that money is allocated to maxing out our SEP IRA for the 2013 tax year, as soon as I know what number I can put in

and 4) Part is set aside for new business ventures if any come across.

But, mainly it just makes my wife happy to see it all in there :) And with kids now, it makes me pretty happy too.

J six digits baby! I hope it’s close to or surpassing your annual income. We passed a milestone this year when our net worth increased at a higher rate than our salaries. Thats my goals moving forward to increase my net worth at a higher rate than income.

Yes!! I think I’ve read you saying that before somewhere because I’ve literally just started paying attention to that this week :) And for 2013, that is indeed the case here (which is actually kinda bad since it was due to my biz income dropping this year, haha… but still – it counts!)

Being one that loves the emotional milestones myself, you’ll be rocking it in about 6 months when the first digit of the mortgage amount changes.

Oh man, I cannot WAIT.

If only everyone had as much love for their accountant as you.

I value my time and also know when I’m smart enough to do something myself and/or if I care about researching or not. And taxes is DEF not anything I want to get near anytime soon, haha… but I bet people would say the same about web coding or blogging too that we love :)

Hi J. Money,

I am newly 22 and I am trying to take control of my finances and plan for a beautiful retirement. Can you help me find out what my networth is? I think that’ll motivate me even more in 2014 and going into my 22nd year of life!

Thanks so much and just fell in LOVE with your blog.

Awesome! Welcome aboard :)

Sure, your net worth is pretty much just adding up your assets on one side of the equation (savings, investments, property, etc), and then your liabilities on the other side (debts, loans, credit cards, etc). Then all you do is deduct your liabilities from your assets and voila! Your net worth pops out :)

I’d say spend 30 mins or so tonight just logging into your accounts and writing them all down, and you’ll be off to a great start :) Then do it again each month so you can see how it’s moving!

There are lots of programs and spreadsheets you can use too to help you maintain it all and track, but I advise starting just w/ pen and paper first so you can get a good sense of how it all works together. Here’s the net worth/budget spreadsheet I still use to track it each month if you want to try that out later as well:

https://budgetsaresexy.com/budgets/j_budget_template.xls

Good luck!

Can you tell me what you use to track your net worth? Do you use a certain website like Mint or……? Thanks

I use a simple spreadsheet I made:

https://budgetsaresexy.com/budgets/j_budget_template.xls

It has a budget attached to it too, but you can ignore that if you wish. It’s basically just an area that deducts all my liabilities from my assets all in one nice spot.

I like to manually track my net worth every month so it holds me more accountable and I’m forced to do it – unlike with automated services.

I have a question about how you value your home.

If you were to hire a Realtor to sell your house, then once you got an offer you liked you’d have to pay your Realtor 3% and the buyer’s Realtor another 3%. That means if you get $300k for that house, you’re only going to pocket $282k.

Have you ever considered taking that 6% out of the value of your house, since you are gonna have to pay it? (unless of course you don’t use a Realtor and neither does your buyer)

Great question brotha.

Yeah, I’ve thought about it but then I’d have to include fees to sell any stocks or when selling my car/etc/etc. I consider all that expenses at the time of doing the deed (no pun intended), which would then get accounted for on the next update.

The point of net worth to me is to get a good snapshot of how everything is *today*. It’ll fluctuate as the weeks/months/years go on, and never be “accurate” until the day stuff happens (for ex the value of my house will be exactly what it sells for on that day, and also I’m mixing taxable vs non-taxable accounts up there in the worth), but I concentrate on the bigger picture than the details. I’d shoot myself if I had to do that ;)

But to your point, yes, it’s stuff that will definitely come into play one day for sure.