A new month, a new net worth! One of the 12 best times of the year ;) And this will mark month #88 of tracking it so far too, whew. One of the biggest game changers of my finances, I’ll tell you what.

You can think all you want about your money and where you believe it to be (or not), and how good (or not) you are with it, but until the numbers are down on paper somewhere staring you back in the face, it’s a whole other story. We’re so good at convincing ourselves that we have stuff on track (or not), but letting the numbers speak for themselves is where it’s at! The numbers never lie!

But of course every month I try convincing y’all to start doing it if you haven’t already, so this time I’ll end my spiel there… And instead, let you hear from my new friend John Feldmann who just found out how powerful it can be! Haha…

Check out how motivated he is ;)

J. Money!!!

I have been following your blogs/articles for a little while now and started tracking my net worth at the beginning of the year. I just logged my Q1 results and wanted to share with you.

- Net worth @ 1/1/15 = $51,464.61

- Net worth @ 4/1/15 = $60,707.87

That’s a whopping 18%! In just 3 months!! Ya dig?!?!??!

I’ve done this mostly by upping my 401k contributions, set up monthly payments to max out my Roth IRA and starting a brokerage account. Every dollar I used to spend (throw away) on random crap I now analyze how much it would be worth in 40 years.

I still have a ways to go. I spend WAY too much money eating/drinking out. I am getting married this October and will be merging accounts with the Mrs. pretty soon so that will present some road bumps…

[that was part of his first comment he left on my site, and then this was part of the 2nd one he dropped just the other day… giving me an update]

- Net Worth @ 5/1/2015 = $63,234.44

That’s up 22.87% since the beginning of the year!!! I am still pumped, but I know I could have saved more. I went to Vegas this month and definitely spent more than I should have.

This month is going to get tough as I am currently locking a mortgage and will need to come up with closing costs/ appraisal fees/ etc. On a more solid note, most of my stocks in the brokerage account killed it on earnings this quarter and that portfolio is up ~12% year to date.

As you can see, this guy’s excited. And as he should be! Of course not every month will go in his favor like this (the more you have in investments the more its reliant on the markets), but the more you control what you can – like your savings rate and investments/debt pay offs/etc – the faster it’ll grow.

And then one day you don’t have to even worry/think about your money any more cuz it’ll all be working magically behind the scene! Woop woop!

Anywho, here’s how the month of April went down:

CASH SAVINGS (-$3,021.02): Down some G’s but up $5,500 in our maxed out Roth IRA – woot! With a little encouragement from you guys (thanks!). I’d been going back and forth on whether it’s worth taking out even more cash, but now that we’re not spending $2,000/mo on childcare and biz is starting to pick up, I decided it was a safe risk :) Plus as I mentioned $4,000 of it is already banked in our Challenge Everything Account! So it’s like free money!

BROKERAGE (+$58.04): Nothing too major going on here, just the markets doing its thing with our Motif experiment, as well as a handful of more dollars being automatically invested by rounding up all our transactions w/ Acorns. It feels good knowing a few pennies are going towards this every time we swipe our card or pay a bill!

IRA: ROTH(s) (+$5,263.22): Boom! $5,500 thrown in and up almost that same amount this month but not – wha wha. Good thing we’re in it for the long haul ;)

IRA: SEP (-$1,283.70): Nothing too exciting going on here… didn’t add anything this month, as I probably won’t for the next 11 months either until it’s time to drop in another load at the end of the tax year. I’m still feeling that $10,000 deposit last month!

Here’s a screenshot of the growth since switching to Vanguard last year (IRA + SEP):

AUTOS WORTH (kbb) (-$430.00): Another drop in my wife’s Toyota, and wondering if it’s due to a new change I saw on KBB.com when I went to run its calculations. There’s now an “exterior color” option to click, which actually makes sense because cars that are bright yellow or pink or something I’d imagine would sell less than a boring average color, yeah? I know when I sold my hot yellow mustang years ago I didn’t have as many enthused customers, haha…

Here’s a screen shot of the new addition I saw over there (w/ my Caddy’s color picked):

And here are the values of both our cars:

And here are the values of both our cars:

- Frankencaddy: $1,000.00 (KBB shows $1,717, but I’m chopping off more due to its “character” :))

- Plain Jane Toyota: $4,968.00

HOME VALUE (Realtor) ($0.00): This remains the $300,000 its been for a while now, but I did reach out to my realtor again (who is what I base this # on) to get an update. I typically don’t like using Zillow or the other home sites just ‘cuz it fluctuates so much, but I know others love ’em so do check them out when you’re running your own reports and see if they’re more accurate for ya.

Anyways, our rental property is up for renewal again (so fast!!), so I pinged our realtor just to see if it’s worth considering selling again, but unfortunately we’re at the same stagnant value of about $300,000-$310,000 so we’ll try and get our tenants to renew for one more year and then hopefully offload it on the next round. If they dip out though, we may just bite the bullet once and for all and be free once again! I can’t wait!!! (Can you tell I’m not a huge fan of real estate? :))

MORTGAGES (-$696.48): Another $700 chipped away! All from paying a little extra every month and rounding up to the nearest $100th or two… We’ve been doing it for so long that I don’t even notice the difference anymore – which is the position you want to be in!

Here are the balances left on our stupid mortgages ;)

- 1st Mortgage: $266,744.33 (30 year conventional @ 5.5%)

- 2nd Mortgage: $26,398.70 (HELOC @ variable 2.8%)

And no, we can’t refinance… Unless we want to pony up $80,000+ (vomit).

That wraps up another net worth!

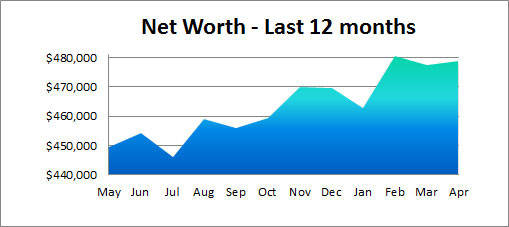

Here’s how the last year has gone… ups and downs and all arounds:

And here’s how our boys did :) Baby Nickel got a little 529 action from baptism money last month…

How’d you guys do? Anyone hit any major milestones? Anyone just started out tracking and want to say how awesome it is so we can all congratulate you? :)

As always, you can see my full list of net worth updates over the years (all 87 of them) here, and if that doesn’t quench your voyeuristic thirst, you can check out how much 150+ other bloggers are worth here: The Ultimate Blogger Net Worth Tracker. We track that over on my other site, Rockstar Finance, which pimps out my favorite articles on $$$ I see every day. And shockingly they’re not all mine ;)

Here’s to a new month, everyone.

![]()

——–

PS: As always, my favorite ways to track this stuff:

- The “Money Snapshot” spreadsheet – a simple Excel template I created for my coaching clients

- The J$ “Budget/Net Worth” spreadsheet – the Excel sheet I use myself – in all its colorful glory!

- Mint.com (free) – If you’d rather have it all automated for you

- PersonalCapital.com (free) – If you want Mint, but on steroids… Here’s our in-depth review which shows how kick-ass they are. Lots of pretty graphs and tools for your $$!

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

I’ve just started tracking our net worth, and boy, is it an eye opener! It’s so motivating to see the numbers creep up every month :) our numbers are nowhere near as impressive as yours though ;) but, we’re just at the beginning so I’m excited to see where it goes! Thank you for sharing yours, it’s posts like this that are such a big inspiration and motivator in terms of making my own finances better :)

Good job! It’s always unfair to yourself to compare your situation with others just cuz we’re all in so drastically different phases/ages/lives/etc, but I am glad this helps motivate you to keep going :) You’ll have down months that will inevitably occur too, but keep on rockin’ it. Can’t track your success when you don’t know the #’s, right?

I have to thank you for posting these. I’ve been reading them for years but it’s only this year I finally got my act together and started tracking ours – at your insistence :-)

We started in January 2015 with a net worth of $360,338NZD and have been slowly edging up to $365,855NZD. It’s been slow because we are travelling and not really actively earning or investing (just a couple hundred each month so we can get the government match). But I still love that I have to log on to all four investment accounts each month and check how they are going. I never really cared about the retirement accounts before because it seemed so far away (we can’t access them until we are at least 60) but seeing them as part of the bigger portfolio and combined with our rental properties is really motivating me to take more interest.

Plus I totally look forward to the 1st of the month now so I can update the spreadsheet!

Thanks J.

LOVE IT!!!

Keep on going!!!

Like you, I’m still waiting on the day when my house value and mortgage don’t practically cancel each other out! Finally this year its starting to approach positive territory.

Haven’t crunched the April numbers yet, but don’t expect any major changes. In the same boat in house and mortgage.

Sorry to hear you’re not a fan of real estate. Couple of things….been my experience you “make your money” in real estate when you buy and collect it when you sell. If you want out, might want to reconsider selling if the Fed raises rates …. big bearing on real estate prices as people “buy a payment” not a price. So if borrowing rates go up prices take a hit. It will be interesting to see the dynamics of your next home purchase when you do sell…

I think it also makes a difference whether you’re buying a home to live in vs to make $$ off. Our now rental used to be our home so all we cared about was living in it comfortably, but had we gone in looking for an “investment property” it would have been a lot different. And there’s no way we would have bought it :) (provided I was smart enough then, of course… which I doubt I would have been – hah)

Congrats on maxing out the Roth IRA. How do you decide what to put into the kids’ college funds? We have auto-draft payments for one kid’s but are generally haphazard about it. We do try to put any gift money they receive in them.

When $$ was flowing we were working on maxing out the amount the state would allow for tax breaks (I think it was around $3,000/year per account), but now that money’s more tight we just put whatever $$ they receive as gifts in there. So pretty much we don’t have a real “plan” right now ;) But investing *something* is better than nothing, right?

I took a big hit to my net worth in April. Damn taxes- but I knew that was coming ;) I also moved which is killer costly.

I remember those days! I used to include all my tax $$ in my net worth, but then just like your it would go down every quarter and piss me off, haha… So now I just keep it all separate and pretend it’s not there. If we were working 9-5’s it would have been gone already, so I don’t even bother including it in the worth as it’s not ours – it’s the gov’ts.

We had a relatively mundane month for April, which I can’t complain about too much I guess. :) We do meet with our CPA this week to talk about moving from an LLC to an S-corp which will likely mean LESS in taxes and MORE for retirement savings – I’m pretty excited about that if it comes to fruition!

That’s pretty cool! I haven’t gone down that road before, but I hear good things about S-Corps. Let me know if it’s all true once you’re converted and rollin :)

April looked really good for us because of the tax refund (I’m still not good enough to figure out our withholdings). It’s even tougher because my wife will be getting a big bump at the end of the year once she starts her post-doc. Still piled most of the leftover $$ at the mortgage. Almost out of PMI and one step closer to our goal of paying off our mortgage early!

Congrats! Both of those steps are killer ones :)

Exciting to read John’s story…you can feel his excitement in his email! What you said it key though – it’s all about the savings rate. Too many people focus on getting a 20% return in the market and not on how much they are saving. If they would just save more and not worry about their return, everything would work out in the end. For most, savings rate is much more important than return.

Also, I got curious when you mentioned this is #88. I looked back at when I first calculating my monthly net worth and April 2015 marks #146 for me. I can’t believe it’s been that long!

Woahhhhhh – you are a financial nerd, my friend – I love it!

We too are reluctant landlords but the longer we have the rental house and the closer it gets to being a paid off mortgage, the more I like the idea of forced diversification in my “retirement” accounts. Something to keep in mind…

for sure… long term I know it’s a good $$ play, but emotionally I want to punch it in the face ;)

This really has been a game changer for us as well.

We ended 2014 at $181,364 and as of 4-30-15 we are at $204,209. So far this year we have been averaging an increase of $5,700/month. Starting with May I expect net worth to increase by about $8,000/month.

Like you, my detailed financial reports that I publish every month are my favorite posts to work on.

So close to the $500K…Keep up the good work!

Cheers!

oh wowww – what’s making the jump to $8,000 like that? that sounds incredible!

Congrats on the amazing continued achievements J$!

The boys’ progress is particularly impressive. Were they baptized by FIRE?? ;)

Good one! Almost spit out my water reading this :)

I always think it’s a good month when my net worth can grow even if the markets shrink, which is what happened this month (although my husband’s Roth investment in some random Mutual Fund focused on Heavy Industry in India did quite well).

Good job on the net worth its good but could be better. I want to see 500K by August my friend, no more slacking on the savings rate. Just your fellow motivating PF blogger cheering you on. 5ooK by labor day, this could be a new challenge. HAHA

Hah! I think I need to work on my income rate more so than my savings. If only I could go back to my hustler days before my babies were born! :)

The amount you’ve saved in your retirement accounts is incredibly impressive. Based on how aggressive you are with saving for retirement, I imagine you want the option to retire early. Is there a target you want to hit before you dial back and instead re-build your cash savings?

I haven’t run any numbers (so I’m winging it here), but if you plan on selling your condo next year, it’s likely you’ll have a lot of fees associated with selling and perhaps a tax bill depending on the profit, not to mention any maintenance or upgrades you want/need to do prior to selling. Don’t mean to stress you out :) just throwing out some suggestions for your financial consideration!

As always, I appreciate the honesty and openness you show here!

Even more reasons I hate owning! ;)

And yup – early retirement is def. the name of the game now… Last time I calculated it I’ll need to continue to max out my SEP and my Roth for a solid 13 more years before I can even start seriously considering it. Unless the investments go way up by then and/or my expenses way down. This calculation has already changed by a handful of years when I took out $2k/mo in daycare which is only temporary until my wife gets a job, haha… But at least then we’ll also have more income :)

So to answer your question, my target really is to just keep maxing out both those IRAs until it’s time to “retire” or something magical happens. And even then I’ll still work, but only on the stuff I love… like this blog.

I love how excited John is about tracking his net worth! Woo hoo! It really is an awesome thing. I sort of vacillate between focusing on it and then just letting money do its thing and not worrying about it. I think I actually like tracking my expenses more because I feel like I can control them to a greater extent (since I still haven’t figured out how to control the markets… ;) ).

The last day of the month used to be my favourite day because it’s pay-day – but no longer! Well, ok, it’s still pay-day…but now it’s my favourite day because I know it’s time to update our net worth tracker!

It’s not something I can talk to my friends and family about (other than the Mrs of course) so it’s great to be able to read about everyone else’s story here – when we first got married back in March 2012 our net worth was just £262,000 ($396,000 US) but as of yesterday it was up at £570,000 or USD $866,000! I’m so excited about keeping going on this journey and getting to the point where we reach $1m and then eventually £1m. J, you’re definitely one of the most motivational finance bloggers out there and it’s great watching your journey – as well as everyone else’s thanks to the blogger net worth tracker! Keep it up :-)

Thanks PP! And great work on increasing that $$$ by so much – that’s $500k in 3 years – wow! Sign me up! :)

It sounds so much better in US dollars! About $85k of that growth was underying growth in the value of our two (mortgaged) properties as the market around here has grown – but the rest has all been pre and post tax saving and investing hard (mostly index funds).

Just got to keep going as we’re not yet in a position where we can consider ourselves financially independent and won’t be for a while – but it sure beats having nothing in the bank and living payday to payday! Fortunately there’s a great community online to keep us motivated and focused on the goal!

damn straight.

J$,

Awesome month once again. And the two kiddos over there are keeping pretty good pace as well. :)

I don’t track my net worth only because I plan to eventually live off of the dividend income the portfolio generates, but tracking your finances (however that is done) is absolutely imperative to financial success. Couldn’t agree more with you. If you’re not tracking things, how can you possibly know if you’re on pace for your goals or not?

Keep up the great work.

Best regards.

Nice Work J. Money. Is it weird that I felt like my net worth started increasing just because I started tracking it. I felt like Mint was making monthly contributions to keep me excited and coming back.

Not weird at all – it’s TRUE!

You’re totally more motivated when you’re tracking stuff and keeping an eye out – even if you’re not aware of it consciously. I’m sure there are plenty of times you’ve decided not to buy something knowing full well it’ll affect your worth in the future. It’s why it’s one of my favorite things to do EVER w/ money – and barely takes much time!

I wonder where I stand against Budget’s are Sexy Net Worth? Little Arsenio Hall “Things that Make you Go Hmmmm? I’ve got money on you love that guy, that and me winning the FI Day race, goo.gl/FEmdR3 ???

hah! I do love that guy, but only cuz of The Apprentice when he was on it :) Didn’t know much about him (other than the arm shaking, of course) before that.

Great updates yet again! I haven’t done my net worth for this month yet, waiting on mortgage payment to go through otherwise it’s money in flux. But can’t wait to do it. My employer matches 3% for retirement and they contribute once a year! Well…that just happened!!!

Woo!

Good progress! One question – Have you considered using your HELOC to pay off part of your mortgage, considering its rate is significantly lower than the mortgage rate? Or do you think that is too risky?

I would totally do that but unfortunately our HELOC was maxed out from day #1, and then when the market crashed and we got underwater, the cap kept lowering with each payment we made.. Haven’t checked what it is in a few years, but I doubt we could add more to it just cuz we’re barely above water now w/ its value.

Sneaky thinking though! :)

Looking good J. Money. Congras on maxing out on the Roth IRA. Here in Canada the federal government recently announced an increase of TFSA contribution limit from $5,500 to $10k for this year so we need to work hard and maximize the limit ASAP.

Oh wow! That’s a huge jump! What a great thing though for all you hustlers out there :)

I want to thank you for encouraging me to do this. I always had a pretty good idea where my money was going and how it was growing, but now that I track it every month its pretty sweet to see the amount go up. It is especially reassuring in months like this last one when we spent an extra $2k but our net worth still went up! Pretty awesome!

Woo! Way to take that step and actually DO IT :) I can preach all day long about it but it doesn’t ever matter until people take action. So you make me so proud!

Net worth is such a powerful thing because it allows you to see how much you keep instead of how much you make. I know there are lots of high earners out there who probably have a really low net worth because of blowing money on stuff that really isn’t that amazing. I know because that used to be me! Thanks for sharing. I need to do an update soon.

Good month J$. It appears you are in the same boat as me, you deposited a bunch and were able to see a slight increase although the investments are down a bit. I too have a rental property that I am wanting to get out of, last October they said they will be there until October 2016, when they renew this year I will be raising the rent by $100 a month, first raise in four years. I will also be raising it again by $100 in 2016 if they decide to stay, I am sick of having my money sitting there not producing anything for me and want out.

On another note, it has got to make you feel all warm and fuzzy inside that you really did/do inspire many of the people on here (myself included) to take a serious look at their net worth. If I would have started this eight years ago, rather than eight months ago I could easily be in the million $$$ range, but better late than never. What I am trying to say is thank you for this page and all of the hard work you put into it, it continues to allow as well as force me to stay accountable for my earning, spending and saving and will help me reach FI much sooner than if I never stumbled across it in the first place.

Thanks

I’m so glad to hear!!! Man, y’all are so good to me today – I’m totally feeling the love :)

And, quite honestly, just sharing my own numbers with y’all every month is doing ME well too. It’s one thing to run the numbers at home, but a whole other to share with thousands of people, haha… So you guys keep me accountable too – it’s win win :)

(And good idea w/ the raising of the rates, btw. At first I thought you were going that route in *hopes* they’d say no and then you’d have a reason to sell it, haha… I’ve heard of people doing that – even asking for $200/mo more – and then if they happen to say yes then even better! Though that’s one helluva increase… and not all states allow it)

I got one even better then them saying yes, they asked me if I was interested in selling it to them in October, took everything I had to not say “F*ck yeah I’ll sell it!”

They were cool with the increase though.

Oh, nice!!!! I would die if mine said that, haha… In fact, I’m still waiting for them to tell me if they’re renting for another year after raising it by $25, so maybe they’re taking forever cuz they’re interested in buying too? That would be something!

That’s a huge net worth. I finally found this article. Thanks for sharing. I love it and I can relate some of it!

Thank you for sharing. Mine went up by about $500.

A little bit a the time. We will get there.

http://www.alainguillot.com/net-worth-may-5-2015/

That’s all we can do :)

This is amazing, thanks for sharing. I am working on my net worth as well and so far so good. Of course it depends on a month as some days are better than the other ones. But it takes lot of work, right attitude and calculations to achieve the goals. However, it feels great and gives a peace of mind.

I think April went well, even though my net worth is still a negative. I was able to pay off the remaining balance for my consumer loan, so now I just have one loan left. My plan is to keep throwing money at this loan until it is gone and than use the same amount to invest. Reading you net worth update is very motivating and I know one day I will get to my goal net worth.

YES! Perfect plan! Congrats on nixing that 2nd to last one – you’re almost there! What a feeling it will be to keep sending in those payments, only into your own saving/investment account :) You’re on your way!

Thanks for sharing & motivating :-)

Been lurking for the last 5 months – after I read this post on my last break at work, went right home and figured out my net worth, then made the decision to throw 50% of my take home (as opposed to 40%) at my debt.Targeting to be debt-free on July 4th (#yayfreedom!), then going galleze-ish at saving up my emergency fund.

You’re absolutely right – I needed to see those figures. And boy do I have catching up to do!

LOVE THAT!!!

Especially with the goal being July 4th, haha…

Way to take action and ramp it up!

I am also gonna max out the Roth IRA. I am very impressed with your net worth update, J Money. Congrats! High five!

Hey J,

Now that I’m doing this consistently, month after month, I can let you know what has happened so far this year:

Jan = $45,780

Feb = $49,174

March = $51,443

April = $55,305

I know the numbers aren’t as big as some – but I’m just trying to focus on the growth – which was $9,525 over the four months — I’m a little lost as to what to compare this to in order to see how well I’m doing, because I’ve never charted this before – but the more I work on it, the more I’ll (hopefully) start to see patterns.

(and your spreadsheet is awesome!)

S.

BOOM!

The comparing part is really hard to do, and you don’t want to risk getting pissed off ;), so I say just keep doing what you’re doing and gauging your *own* happiness (or not) with the progress. From a bystander here, Growing your worth by $2,000+ every month is INCREDIBLE! You doubled my own growth this month – how’s that for perspective? ;)

(You can also check out the blogger net worths over on my other site too, if you want to try and find the one that’s closer to your range:

http://rockstarfinance.com/blogger-net-worths/

Only thing to consider is that you don’t necessarily know if it’s a single net worth vs double (married family) or where they live or what they’re situation is/etc, so it still won’t be apples to apples. But what I DO like about it is that you can learn other ways to help grow it as we’re all into different things! :))

Good Job, J Money!!! Keep grinding my friend!

Hoping to update my April numbers later tonight.

I just started actively tracking our net worth. I’ve been using personal capital for a couple of months now, but did my first net worth post this week. We’re currently at $60538. I’m excited to have it as a way to hold me (and my husband) accountable to saving and investing. Maybe it’ll help us stick to our eating out budget a little better, too. :)

Well, fortunately there’s two ways to grow your net worth while still allowing you to eat out if that’s what excites you :) Spending less in other areas or just *earning more*! Nothing wrong w/ keeping your splurges as long as you’re making up for it in other areas, know what i’m sayin?

Absolutely! Our coffee budget will probably never go down, but I’m more than willing to stop eating as much fast food and only eat at good restaurants! And, gotta love those side hustles!

Great job. It’s so powerful to track those numbers. We’ve been tracking our net worth for the past 5 years and it’s amazing how fast it grows when you spend much less and invest the rest. Last year we finished paying off our remaining debt and grew the net worth by 45%! Now we’re less than 4 years away from affording early retirement. Keep these coming!

Holy crap – way to go man! Powerful as hell right there!

This is great! It’s always good to be reminded of just why it’s important to track our progress this way. I really do feel like net worth updates are where the rubber meets the road.

Managed $9,001 at the start of the month up 7%. Was hoping to have 10k by the end of the year but could have by the end of this month if the market moves in my favour.

The nice part is that you’ll reach it at some point real soon :) Then time for a new goal to keep pushing forward!

My Goal is to save 3k a month in my 401k between me and my spouse and it growing by 12% even though there was brexit.

Nice!!! Helluva plan right there, brotha.

(also – I like it how you found a net worth update over a year old, haha…)