Happy best day of the month: Net Worth Day!

How many of y’all have already updated yours? How many saw an increase from last month?

We eeked out a little gain compared to previous months, mainly due to the markets being flat (where most our money is), but we did start seeing a few welcomed changes now that my wife is working again:

#1. We have a 2nd income again!

The paycheck amounts have been changing as we tweak retirement contributions and get healthcare going, but so far getting one for $1,389.93 and another of $1,193.04 have felt the opposite of bad ;)

#2. We have another retirement account to track

The Thrift Savings Plan (TSP), which is like a 401(k) except for government workers. And looks like they match contributions dollar for dollar up to 3% (WOO!), and then another $0.50 on the dollar for the next 2 percentages thereafter. So if you put in 5%, they’ll match 4% of your entire paycheck which is FREE MONEY!!!

They also automatically give you 1% whether you contribute to your account or not (good for people who don’t pay attention!), meaning you’ll actually get an extra 5% total for free so long as you put in 5% yourself. Which of course we’re doing, and will probably increase as time goes on.

Something else the gov’t does is set the automatic contributions to your TSP at 3% for all new employees, forcing them to log in and change it if they’re unhappy about it. Which not many do, because you know – effort ;) A study I just read showed how the participation at one company among new hires rose from less than 20% to over 90% due to automating contributions for their employees like this! Pretty incredible! Here’s a great article by My Money Blog if you’re interested in reading more: The Power of Default Settings: 401(k) Auto-Enrollment

#3. We now have a pension in the mix!

Every paycheck a little over 4% goes towards my wife’s future pension which, from what I gather, is an annuity that pays out every month for the rest of her life once retired (as long as enough time has been banked). There’s always a question of whether pensions belong in your net worth or not, and while I don’t personally believe they do (to me it’s more of a *cash flow* thing – similar to having a second job or passive income stream coming in), it WILL of course affect your $$$ and your future.

Instead, I prefer including it in my retirement calculations/spreadsheet where all other income streams come into play as well (you don’t include your salary in your net worth, right?). Then, if that money is saved or invested once we get it, it’ll be accurately reflected in our net worth at that point. Though hopefully we’re spending it and enjoying our lives :)

So lots of good changes going on over here, for sure… All helping us to regain sanity from the past few months of moving and starting daycare again, yada yada yada.

Now time for the numbers….

(And btw, for all new people – the reason I share this every month is to give people a real life snapshot of someone’s money to help them with their own. It was something I LOVED seeing myself when I first stumbled across personal finance blogs 8 years ago, and ever since I’ve been including them in my own. Feel free to ask whatever questions you’d like!)

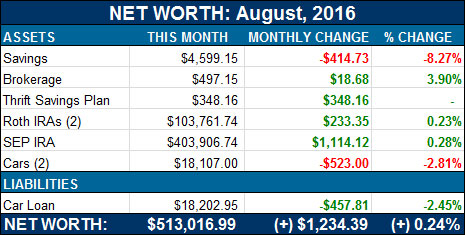

Here’s how August broke down:

CASH SAVINGS (-$414.73): No more $2,000 losses – woo! We’re not out of the woods yet, but now with the move and other unexpected costs out of the way (turns out we like to drive over razor blades and get flat tires – yay!), the ship should start turning around. And perhaps I should halt my aggressive car paying down plan too until we’re gaining again…

BROKERAGE (+$18.68): Every month Acorns invests a few dollars for us by automatically rounding up all our daily transactions. Nothing too crazy, but it’s fun to stash a little extra on top of everything else we’re doing and looks like we’re about to cross $500!

*NEW* THRIFT SAVINGS PLAN (TSP) (+$348.16): Hubba hubba! A new account to grow, and another chance at hitting financial freedom sooner than later :) I wasn’t able to log in and get the exact #’s of this account as the gov’t is slow to send info out (we still don’t have our health insurance account # even though we’ve been enrolled for weeks!), but going forward we’ll be tracking it to the penny as we do all other areas here… The $348 is a combo of what my wife contributed herself + the matches she gets. Hopefully this will rise even faster as it’s invested into the market.

(Right now her $$ is going into the default Lifecycle Fund (like a “target date”) but hoping to convince her to get more aggressive since we have plenty of years ahead of us… My wife’s more conservative than I am though, so we’ll see how that goes :) The good thing about the TSP options is that they’re all really good! Especially in terms of expense fees, so gotta love that…)

ROTH IRAs (+$233.35): Nothing major here due to the flat markets and not contributing anything extra, but once we get going again we’ll be switching from yearly lump deposits to monthly ones. For now it’s just at the mercy of the markets.

SEP IRA (+$1,114.12): Same with this guy too. Nothing new added and just going with the flow of our economy. Here’s a snapshot of our account since switching over to index investing two years ago (we’re 100% into VTSAX – Vanguard’s Total Stock Market Index Fund):

(This shows *returns* fyi, not total amounts invested)

CAR VALUES (-$523.00): Both our cars declined in value this month – as to be expected – and here’s the value of both of them now via KBB.com:

- Lexus: $13,985.00

- Toyota: $4,122.00

I still miss the Caddy, but fortunately the Lexus helps make up for it :)

CAR LOAN: (-$457.81): We might have to stop this until we’re above water, but I’m just so addicted to rounding up debt payments to the nearest $100th – or in this case, nearest $500th :) I just love seeing the amounts drop so fast!!! Highly recommend for anyone also trying to kill off debt faster. You barely notice it when you’re rounding up normally…

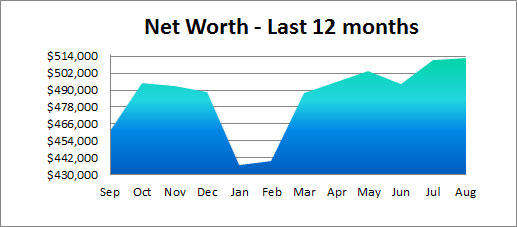

And lastly, here’s a snapshot of how it’s gone over the past 12 months:

Oh, and our kids money too (yup, gotta start them young!):

And that’s August! How did you do??? Anything new or exciting to report?? Anyone just starting out on this wonderfully nerdy path? :)

If you are, check out the resources below if you’re looking for a good way to track it all, and if you like seeing peoples’ net worths like this, hit up my other project where we track over 200 other bloggers’ money too: The Rockstar Finance Net Worth Tracker. It ranges from those in hundreds of thousands of debt, to those in the MULTIPLE millions of dollars! Pretty fascinating stuff.

Here’s a list of the past 100+ of our reports too if you’d like to peruse: Net Worth Archives

Good luck y’all! Another month = another chance to gain freedom!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Looking good. I’m updating our net worth this weekend. What’s the vesting period for the pension? I recently took a state job and I’m in a pension too. I have a 10 year period. Still nice to know I’ll have some additional income.

Nice – congrats!

It seems that 10 was the minimum for FERS people too, at least for partial pension, but then I saw something about 5 years as well so not sure which is the absolutely minimum there? I’ve never been with a company for that long so I give anyone mad respect for putting in time like that :)

Congrats on another increase J. Every month where your net worth is above $500k and it goes up is a good day!

It’s also great you’ve got 2 incomes going again. Nice job.

Tristan

Thanks man! Hope yours is going well, too!

Thanks for sharing J. Money, it must be a great feeling to have the 2nd income again. I like the sound of that Thrift plan as well, their matching is awesome and who doesn’t like free money?

Good job on the 529 plans as well, off to a strong start. When my kids were each born, I started them with $500 in a 529 plan and then made monthly contributions after that. They are in high-school now and we have quite a tidy sum socked away.

I pretty much have a continuous view of our new worth as I keep all of our accounts in Quicken, and so far, up 18% for the year – WaHoo!!

Rock on!! On all accounts! I keep trying to get my kids to stop growing, but I know eventually they’re going to have to leave the nest! :(

Our second income just started again too on the last day of August now that my wife went back to work part time. It is a nice feeling seeing that extra income come in.

I have heard great things about the TSP! Many say it is one of the better retirement plans out there so it nice you get to take advantage of it!

Big congrats to you all too, then! Love hearing that!

Yeah – I had posted something on Twitter about TSPs and it blew up with how incredible it was. What’s nice is that they literally only have like 7 or 8 options for your money which is divided down even more into either “Lifecycle” funds or straight up indexes! So you can easily put together a nice portfolio without being overwhelmed by all the choices… And again, the expenses are so dang low thanks to how big the gov’t is!

A great month I see. Nice!!

I just learned that I can access my pension whenever I retire. Which was friggin awesome news as I thought it was 55 based on what turned out to be an outdated set of plan information. I can get it in two years when we pull the trigger.!!

Tempted to celebrate at Starbucks on way to work but Mrs. PIE won’t be having any of that splurging….

Agree, those TSPs rock it. And good luck to get the conservative other half thinking your way. Sending equity vibes your way…..

Nice!!! Oddly enough I’m at Starbucks right now typing to you ;) Maybe that’s why I’m not retiring as early as you are? Haha…

Interesting point on #3 with the pension. I’ve always had a really hard time finding out (or any agreement) on how to include this. Using it in cash flow makes a lot of sense. We will have pensions that pay out over $60K each year and without including them in somewhere in net worth, it certainly makes us look like we are not FI :) If my pension pays out $40K per year – with the 4% rule, what would you have to have invested to get that? Interesting – huh? If anyone has more posts on this, I’d love to read them. I guess I should probably write some on this too.

NICE!!! You guys are gonna be set with that humming alongside your investments :) Hell, even just with the $60k/year you could be fine pending any serious health/life issues. Baller!

This is awesome, first time to your site and love it. Amazing to see your progress, me and my wife are about to hit 1/2 million in investments our goal is 1 million, what’s your goal?

Welcome aboard! You hit the more juicier articles of the month ;) Our main goal is to just work towards financial freedom – which last I checked (few months ago) was around $1.7 Mil. It seems our expenses keep drastically changing over the past 4 years though (having kids, moving, changing jobs/etc) so not sure what this # will look like by the time we get closer :) So we just pour in as much as we can into the markets to help speed up the process as best we can… And currently we’re in low cash-flow levels so that’s priority #1 at the moment.

I think that’s the hardest part of our early retirement plans. My wife and I have been married almost 2 years so thinking about kids in the next few years may push our freedom fund higher. It’s hard to predict upcoming expenses. Gonna work full time till I’m 40, but would rather do what MMM did and retire before our first kid. Best of luck J.Money, will definitely be following your journey.

Not a bad position to put yourself in at all :) Though just keep in mind sometimes kids can take a while to produce, so don’t wait too long if starting a family is important to ya!

Very motivating and encouraging- thank you for educating us all about money. My hubby and I just retired this year at 62 and each have a comfortable pension and savings. I continue to read your blog to become more money wise and we plan to hold off on our SS for larger earnings. We are planning on downsizing our 2,600 sq ft home and read you just did this! Would love to see pictures and savings analysis to motivate us to take the leap of downsizing to a more minimalist lifestyle.

Nice! Congrats on thinking about all this and making moves :) Def. a fan of downsizing as it comes with much more than just savings as rewards. We don’t have many pics of the old places, but I’ll add “financial analysis” to the ideas list for future posts. Glad you’re enjoying the blog!

Nice update! It definitely sounds like a positive month all around. Great having the extra income, the TSP is great, and a pension on top of it all! Awesome stuff, thanks for the update!

Congrats on the new paychecks and retirement fund! Gotta feel good getting that 5% match for free

Nice!! Gotta love the extra income. :) Congrats on staying in the green this month.

I just updated my numbers and it wasn’t until now that I realized I am officially a Quarter Millionaire!!! What?? Here’s the numbers in black and white…and a bit of green… :) https://missmazuma.com/2016/08/31/augusts-losses-and-wins/

Thanks for being the motivator behind the MIllion Dollar Club!!

CONGRATS!!! POUR OUT SOME BUBBLY!

Great update! Welcome to the world of federal employment. Another great thing about being fed – it’s very easy to set up and change an automatic paycheck allotment to savings. We have ours set up to go straight into Vanguard and then you can tell Vanguard how you want it distributed among different funds.

Beautiful!

Nice! The extra paycheck has to feel good and the TSP is great! Even without moving to a more aggressive allocation, the TSP is still a big win.

I use Mint, so it gives me my net worth every day in the app. It also handles trending and graphs. This month wasn’t so good. Normally, I go up about $4000 a month (surprisingly consistent), but I only went up $2000 in August. The good news is that my spending in August was the second lowest month it’s ever been since I bought a house last year. And the lowest month was only about $50 lower. We’ll see how September goes. I’m thinking I can set a new spending record, but the net worth thing is up to the markets.

One thing I just realized is that your net worth includes two people. Since I’m more than half of yours by myself, I guess I’m doing good.

You’re doing good regardless of what others (and esp me!) are doing :) Sounds like you’re KILLING IT in the expenses department which is a pretty important piece to the puzzle – so I salute you!

Something I learned during this year off, is that kind of miss paychecks. It’s weird. Our account definitely has enough cash in it, so that’s not it. I just miss extra cash showing up a few times a month. I hope she is enjoying seeing her income flow into the house.

It’s probably because we’re so used to it our entire lives! Imagine when you’re retired for real and all you do is SPEND your money??? :)

I’ve forgotten how nice it was to get recurring – and scheduled – payments. There’s so much comfort in it and it’s been yearrrrs since we’ve had it (I get paid running all these online projects of course, but it’s all over the place! And def. no free matching :)).

I just updated my spreadsheet to generate a table like yours every month, beyond the other charts I made. Super sweet.

Glad to see you having to dive into some pension nuance. Right or wrong, I’m counting the “refundable” portion of my pension contributions to date because I’m not vested yet–and dammit, it’s my money!! Of course, it’s also a long time before I would start drawing it down, but the contribution rate is 6%. It’s in a separate column so if I every change my mind on this practice I can just wipe it all out and everything will adjust back retroactively.

I can get down with that :) If it’s a certainty I’d be more inclined to include as well. Plus, it’s good to know where ALL your money – and future possibilities – are anyways. So not like you can’t put anything and everything into a spreadsheet even if it’s not in the *net worth* part itself.

Sounds like a pretty good month! I bet the good feeling from the extra paychecks (and retirement savings) won’t get old :) My net worth increased a whopping $76 this month. Even though that is minuscule, it has gone up every month this year so I will not complain.

Wow that sure was a big drop in the January / February time frame. The TSP is incredible. They match the 10 year bond yield but for a money market account I believe. Plus the expense ratios are 1/10th that of Vanguard. Would love to see the TSP adopted as an alternative to traditional pension funds to save American states and cities’ balance sheets, but time will tell.

Yeah – market crash AND ponying up $20,000+ to finally offload our house earlier this year.

Not the best combo for net worth :)

Last month was pretty rough for our bank account. We paid cash for a new car and kitchen countertops. Both purchases were pretty necessary and we got good deals, but it still stings.

And you paid cash! Like a baller! :)

Nice job with the net worth! Any month that’s not negative is a win. :)

I like the TSP. It’s a very safe way to invest. My wife has a TSP and it’s been a great account for her. I wouldn’t bank on pension, though. I thought my wife would work until she qualifies for a pension, but she’s about ready to retire. It will take over 12 more years of work for her to get the pension. Not exactly sure how many years, but I’m sure she won’t make it.

Totally. Good to only count on the things that you already have in possession and all others will just be bonuses if they ever come true. Not unlike social security :)

You may want to check the Federal rules.. Unless she is military (which is an all or nothing affair under the current plan), FERS employees can get benefits for as little as 5 years of service

If you leave Federal service before you meet the age and service requirements for an immediate retirement benefit, you may be eligible for deferred retirement benefits. To be eligible, you must have completed at least 5 years of creditable civilian service. You may receive benefits when you reach one of the following ages:

https://www.opm.gov/retirement-services/fers-information/eligibility/

I think that fits in her case! Not military and I saw “5 years” mentioned somewhere while skimming too… thanks for this! (And not bad!)

This is my first reading of one of your net worth updates post since I started subscribing to your blog, and I’ve been adopting your spreadsheets these last couple of weeks to calculate my own. I’m a baby finance enthusiast (read: 25), and just starting out with contributing to a 401(k) and Roth IRA and all that jazz, so my net worth is definitely going to be in the negative, but I think it’s prudent to keep an eye on it.

I have a question about the car values. When you look them up in KBB, what value do you use: the trade-in or sell to private party value?

I also have a question about your early retirement spreadsheet. For “yearly add’l investment”, could you expand upon what all is included in that? Or at least, what you yourself include?

Thanks!

Rock on – thx for stopping by! And paying attention so young too – you beat me out by a few years :)

RE: KBB – I use “private party” since that’s how we’d sell them if the day comes, but if you think the odds are you’d trade it in instead then I’d pick that one. Really you just want to be as realistic as you can since the only person that it would be fooling is ourselves :)

RE: “yearly add’ investment” – that’s anything I think I’ll be investing into the future. So, for example right now I max out my SEP IRA every year (it’s like a 401(k) for self-employed people), so I put down the estimate of what I think that will be for the upcoming year so it can forecast for me. Other years I’ve maxed out both my SEP and My Roth so in that case I’d add in both there.

It’s really a section to account for *future investing* vs what you already have invested and growing.

Hope this helps!

You can ignore my question below.. now I understand why the drop in value was so substantial. Thanks for explaining!

Oh good – glad it helped! Always cheaper to buy through private party than it is a dealership :) Just make sure you get it checked out by a mechanic before buying if you go that route! Good luck with your future purchase!

No problem! I’m thoroughly enjoying the site so far – as well as your love for the phrase “kitten caboodle” (in your early posts, at least). It makes me giggle every time.

As for my paying attention at a young age – honestly, if I didn’t have the opportunity to contribute to my 401(k), I never would have discovered my love (read: obsession) for finance!

RE: KBB – I like to think I’d go with a private party first, then trade in if I can’t find someone, so I’ll do the same. Which makes me happy, because that’s the higher value, usually!

RE: “yearly add’ investment” – If you worked for a company that matched contributions to your 401(k), would you add those contributions as well? Also, would you include contributions to an HSA, even if the money in that account is not invested (yet – it needs to get up to at least $5K first, which it is not…)

I just want to try and make sure I am accounting for everything correctly, so my calculations are not off. I wouldn’t want to get my hopes up thinking that I can “retire” at 40 when really I’m going to have to work until my feet fall off or something…

kitten caboodle! Hah! I remember my wife making fun of me so bad for using that all the time… you must have really gone back into the archives :)

RE: 401(k) – same with me! Finding out our company had a 100% match on 100% of what we contribute (literally up to the legal maximum – which no one believed me about!) def. helped start it all for me… Which then led me to blogs and eventually starting my own. So yay for 401(k)s! Even though they get a bad rap from some people??

RE: KBB – Haha yup. I’d try and be more conservative w/ it though if you can – like maybe picking one level down from the condition you really think your car is in just so it gives more wiggle room. And will still be worth much more than trading it in :)

RE: Yeah I personally include *all* ways I’m investing whether it’s from me or matching or whatever (unless you’re not going to get your match or it’s not vested cuz you’re dipping out early, etc). I’d probably put in the HSA too so long as it’s going into investments sooner than later. Or you can just update it on the day you do so – it’s all just estimating the best you can really w/ calculating this stuff.

At the end of the day you just have to do your best and what makes you the most comfortable :) No right or wrong way so long as you’re not purposely trying to trick yourself! (Because you’re the only one it’s going to affect! Haha…)

I started from the very beginning – and I plan to read them all!!

RE: 401(k) – Who gives them bad raps? I love ’em! I sock away money each month and my company matches 100% up to 8% (4% of which is fully vested immediately, the other 4% after 3 years – been here a little over a year), and I don’t even miss it. Plus, like you, it led me to blogs, and podcasts! And perhaps an MSFE, too!

RE: KBB – Conservative, check!

RE: Include all investments, check!

I agree; I just gotta do what’s best for me. Plus, I’m only using net worth as a guideline for my goals and to make sure I’m not making terrible life choices. Just a measure of my overall financial health, if you will.

Thanks for all of the advice!! I greatly appreciate it! :D

You know we love talking about this stuff :)

I’ve also got a pension and my job. It’s got a 3 year vesting period. The amount I am entitled to goes up at 3 years, 5 years, then every 5 years thereafter. I just hit my 5 year anniversary here, so I’m happy. I’m just thrilled to have a pension, as so few employers seem to offer those any more. I haven’t included the value of it in my net worth but I think I’ll look into that..

For real! That’s awesome man. And you’ve already got through the first two vesting periods too – congrats :)

Nothing better than Net Worth Day! Looks like progress is being made as you iron out your money coming in and out with new jobs, new car, and a new lifestyle. As for us, up $17,500 from last month due to a nice bonus from work, a little gain from the investment accounts, and the housing market increasing. Not sure how long the housing market will be as strong – if rates start to creep up and wages stay stagnant we could see a nice drop in prices. Luckily, we live below our means and only spend 10% of our gross income on our mortgage/escrow payment every month. I really cant imagine having a high mortgage payment anymore. Less is more!

For real!! And the less you need to live off the less you need to make too :) Everything else is just extra and powers the growth!

Why don’t you include equity?

We don’t have any – we choose to rent :)

Awesome I’ve heard a lot of good things about the TSP. If your wife is eligible for an HSA that would be a nice little addition too!

She has the option but we didn’t end up going with a high-deductible plan (scares us with kids!) so we can’t benefit from it :( We did just find out that we have some sort of flex spending account we can use for daycare though??? So that’s cool!!

I take advantage of both the flexible spending account and HSA. All tax free in, tax free out options are awesome.

You have to be careful with flexible spending because it’s “use it or lose it” every calendar year. I almost forgot about some money Last year. Thankfully I sent the request in on the last day to submit claims.

Oh nice! Yeah that worries me a bit too. We plan on submitting requests at the end of every month for the day care $$$ just to make sure we’re getting it back okay, and to also help w/ cash flow. We spend close to $2,000/mo on daycare, ugh.

Pensions are becoming non-existent so if you have one good for you!

My employer’s 401k plan is a balance forward plan which basically means it is manually valued every quarter. I don’t have the ability to log in and look at it at all. I just have to patiently wait until quarter end to receive a statement (which I don’t get for 30 days after the quarter mind you). It bugs me because I can’t look at it. I don’t want to make changes (I’m an aggressive investor right now) – but I would like to look at it on a monthly basis at minimum. Ugh! It just bugs me.

I always look forward to your monthly net worth updates. Good job as usual. I am no where near your net worth but it’s fun to watch yours. Maybe I’ll be there one day – I just need someone to give me $400k LOL

I’ve never heard of that kind of a plan, but a quick Google search says that the consensus is those plans are evil. When the markets are up, you lose your gains to your co-workers. When the markets are down, you shoulder their losses. They get you coming and going.

How do you know what plan she has? :)

I agree it sucks to not be able to look at it, Beth, but on the positive side it helps you not to make any rash decisions if/when everything goes crazy! like w/ Brexit!! Soooooo many people pulled out and then missed the comeback just days later.

Why don’t you create your own spreadsheet that lists the fund names, how many shares you have of each, and then the current value of them? Then you can guestimate yourself anytime you want – though it takes a few seconds to look them up and copy the newer values over. You’d also have to figure out roughly how many shares you pick up every pay period but that should be semi-easy…

Just an idea, anyways :)

We’ve been actively tracking our net worth on a regular basis (thanks a lot to you!), and it’s been interesting so far. Not sure what our magic early retirement number is yet, but I know we’ll get there pretty soon. September won’t be a good month on the net worth (lots of problems and large expenses keep popping up), but I’m still very thankful, of course, for everything.

P.S. The pension sounds so interesting! I don’t know anyone who has one of those these days.

Yeah – you guys are killing it with your site income!! It’s a good thing it’s all about being smart with your money because if we were in any other industry we might end up spending it all like everyone else does ;)

Congratulations on doing such a good job building your net worth. Perhaps even more impressive is how accurately and consistently that you’ve been able to track it!

Keep up the great work!

Razor blades, that’s baby stuff, we apparently run over tent spikes!

Hardcore! :)

Well, I am nowhere near you and behind where I should be but I’m debt free now and just passed 100K for my net worth so that was pretty cool. Coming from a past where I was struggling to even make monthly payments, I never thought I would reach that so I’m happy. :)

As you should be! That’s one of the best 3 or 4 milestones if you ask me :)

The first being hitting $0.00 and getting out of debt

Then your first $10,000

Then $100,000

Then $500,000

Then $1,000,000

But most people will say the first few steps are the most rewarding because it’s where a bulk of the hard work and excitements starts… The rest is just a matter of time and patience :)

J,

Longtime reader never commented before. Really appreciate your awesome and inspirational blog man–helping me get a better financial place. I have a TSP and it is very good. Really helps to stay on track, and after reading your blog, I rolled over my old 401(k) into the TSP, which will eliminate tens of thousands of dollars in crazy fees I was paying. This means that my personal money machine just got a little greener. Thanks man. I will be looking forward to your future posts about your family’s experience with TSP.

YES!! Great idea! I was just reading about how you can rollover older accounts like that – it’s brilliant. Even just for having everything in one place and easier to manage, so well done :) Glad you’re getting a lot out of the site!

Congratulations on a positive month. We’re still in the hole over here but slowly digging out. Surprisingly, we’re up just over $14,000. Getting closer to $0! It seems strange to say my net worth goal is $0 but you gotta start somewhere. I’ve moved from -$59,860 in March of this year to -$30,595 on the first of this month.

Hell yeah! That’s one of the best feelings in the world – super motivational to hit! And will help you reach the next stages even better climbing out of the hole like that :) You’re getting closer! Congrats!

My net worth is heading in the right direction even if she has a long way to travel. I want to thank you again for doing these points. It definitely encourages me and helps me “remember” to make the good decisions.

I’m so glad to hear that :) And keep in mind we all make dumb mistakes too – myself very much included! The key is to just do more good ones than bad ones over time, hehe…

Another solid month for the books, J! And congrats on the new income and retirement plan! (“Hubba! Hubba!” :p ) That’s always exciting.

In re: to the LifeCycle investment in your wife’s TSP account, it may not be quite as aggressive as you’d like, but considering her current age (assuming she’s not wildly younger/older than you :p ), it will be pretty aggressive to begin with. I’m guessing it’s either ~70/30 or ~80/20 stocks/bonds. And some of that stock allocation is international stock, which adds even a bit more aggressiveness/risk. So in the end, at this stage in her life, it’s probably not too different from VTSAX in terms of risk.

And to echo what some other here have said, thanks for being an inspiration! Like a few of the comments above, I started tracking my own net worth on a monthly basis because I stumbled upon this blog. I’m hoping to finally hit 6 digits by the end of the year! And I’ll be 100% debt free this month!!!!! :D

Oh wow!!! So cool to hear man – thank you! That makes me so happy that it’s encouraging others to track this stuff too!

Good point about the lifecycle funds too – you’re right, at this age it’s def. more skewed stocks than bonds so it may not be as bad as it is in my head. Not that lifecycles are really bad anyways, at least in my opinion, I just typically like pushing the gas petal all the way down on this type of stuff :) But hey – it’s her money/comfort!

The real issue with lifecycle funds is that they typically have higher fees than if you were to invest in the same index funds separately. They should be plenty aggressive, but I’d watch the fees. Could be the difference between 0.5% and 0.05%.

damn, good point!

Hey, solid report.

As far as it goes up, it’s all good.

I’ve got a feeling September is going to be a bumpy month, let’s wear the seat belt.

I too am a big fan of the TSP. I’m planning on putting over $30,000 in it next year thanks to combat zone tax free income. I wrote about why I think it’s the greatest retirement plan in the world a few years ago: http://militarymoneymanual.com/tsp-the-best-retirement-plan-in-the-world/. I still believe that to be true today.

While the TSP site is a bit clunky, it gets the job done with a little patience. And, the price can’t be beat!

Oh nice! $30k is no joke!!

You should give the Army a call and tell them to start matching contributions. TSP is a joke for military folks because it has poor returns AND no matching contributions.

At least you are getting some good free bonus cash

Damn, really?? I wonder why they don’t match at all?? Are y’alls fund choices different than the gov’t’s TSP options?

Different retirement plan scheme. The current Armed Services plan is skewed toward a 20 year retirement (earned at 2.5% per year, but can only collected if you get past the 20 year mark (some minor exceptions of course)). They (I too as a Guardsman) have the same fund selection as the civilian TSP participants.

They are proposing a change that will offer matching, but at the cost of a reduced annual payment at the end. Bad deal for the long haulers (maybe) but a good one for the 80% who currently leave without any matching money from the government.

Ahhhh… I see how they’re working it then… Thx for dropping the note!

I finally bit the bullet and gave Acorns a try, and I am SO glad I did! I am (healthily!) obsessed with watching that sucker grow with every purchase. Every month I was intrigued but I finally said ah, what the hell, and went for it. Thanks for keeping things transparent and sharing with the world, you are really inspiring me to get my act together and take control of my money. :)

Beautiful!!! I’m so happy to hear that!

I LOVE free money! It’s too bad my employer won’t give me free money until after 1 year of working.. Clever way of reeling employees in to stay extra time. I like my employer so I have no complaints though.

Those are very hefty accounts for your babies! They’re going to be so thankful that you started an account for them when they go to college. I’m sure they’ll get lots of scholarships though :)

That would be nice! :)

Glad you’re enjoying your job too – that’s such a nice perk, especially when you hear so many people bitching about theirs!

August hit Sarah and I with a surprise electric bill – the amount was surprising, not getting the bill. This summer (in many areas, including ours in the Toronto Area) has been incredibly hot and we hit up the AC a bit more than usual. We kept our usage to off-peak times but that still slapped us with a bill 50% larger than our June bill – and about 30% higher than the last few years. We have fought to get 1 bill ahead for our utilities so we had to dig a bit into our hydro budget’s reserves. We also had a leap up in our Net Worth since I “forced” Sarah to update her work stocks in our budget tracker – its a bit of a pain so she doesn’t do it weekly like we do with most of our investments.

Surprises are the worst :( Good thing you pay attention to it all though vs others who have their heads hidden! Much easier to come back from the nonsense :)

Thanks for sharing J. Money! So great that you guys are saving for your kids – as someone that is still paying off student loans (but will be done next year), I think I can say with confidence that one day they will really appreciate that : )

As an aside, I find myself on your blog today after reading another article about how budgets are, in fact, not actually sexy. And I had to disagree, as I still find budgets quite exciting.

Happy saving!

Haha yeah – just read that myself :) (Here’s the link if anyone else wants to see: http://www.physicianonfire.com/sexy/)

Totally cool to not budget or manage your money other ways *once* you know what you’re doing (and are awesome at it), but in the beginning stages?? No way… You need to know where all your money is before you can get all “mindful” about your spending… Get the foundation down first and then tweak from there.

Going now to check out your blog!

Awesome! Actually just saw you’d commented on the POF post too : ) Kara @ From Frugal to Free recently posted about how she doesn’t budget either and there’s an interesting comment thread there too. But I’m sticking with it. Whether I need it or not, I love budgets haha.

Glad you’re checking out my site! I’ve had a blast with it this year and have a lot of posts planned that I’m excited to share soon : )

Sweet! Such a great community, right? We’re pretty lucky that the $$$ space is so open and nice :)

Get job, keep up the good work!

Congrats to your wife! The great thing about the TSP is the G fund which never goes down in value. That way you can park all your money in a safe place if you aren’t comfortable with where the market is going. When not in G, the S and I funds are the way to go. The L Funds are for those who don’t check their accounts very often and have no interest in investing. I don’t think that applies to you ha!

Yeah, I’m loving the C, S and I funds the most for her :) Though at least with the Lifecycle ones it’s invested more so than G… I”m glad she’s not that conservative.

Hi J,

You’re doing great, keep up the good work. Mine’s tracking upwards ;)

Wondering – do you do book reviews? Have you read or would you like to read The Millionaire fastlane – MJ DeMarco?

It flies in the face at what i have been subscribing to for a few years now. Also critical of a couple of books that changed a lot for me back in 2013 when my plans really got started, According to this chap, im pretty much in the slow lane. Just wondered what your thoughts are? Where you at with this?

Best of luck, keep rocking ;)

Haven’t read it yet but heard of it :) I’m guessing it says to focus on income income INCOME as nothing else matters? And that you’ll never become rich working for anyone else?

I’ll put it on my list, but I prefer to focus on *lifestyle* and financial freedom than trying to become a millionaire just for the sake of being a millionaire. My old self would have loved it though! Haha…

Even though the markets were relatively flat, it still was a good month for you! Love seeing your reports! They always inspire me to put mine up too! Love being able to look back and see what happened and have that track record! Plus, it is always nice to motivate myself to try to do better each month!

I’m sure with that new match, you will see that account grow quite quickly too! Congrats!

So glad they’re helping, man :) It’s scary sometimes/lately to do them publicly cuz our cash reserves keep dipping, but we push on!