What’s up money lovers!

I’m a bit late to the game this month, but as always our latest net worth numbers are posted below. And also like always, 95% of it rides on the whims of the market ;) Which thankfully I believe in, or else it would really feel out of control!

Speaking of which, I really like this quote I saw the other day by fellow blogger, and author, Tom Corley:

“Choice, not chance, determines your fate.”

BOOM!

Do you remember that time when you finally “got it” and realized you needed to start making changes with your $$$? When something just clicked and it was time to put it into overdrive?

That’s where I was almost 10 years ago exactly, and by making that one commitment to finally start saving some *real* money completely changed the game for me. I’ve literally done one main thing every year since (max out my retirement accounts) and the power of compounding has taken it from there.

It’s a surefire way to reach independence – so long as you have the patience for it :)

But in either case, it all comes down to choice, not chance. Much to the dismay of my kids… (“But dad, we didn’t doooo anything? It just fell and broke!” Uh-huh….)

There’s a lot of things we can’t control in this world, but personal action – and by extension, our finances – is not one of them. We all have the power to make a change, and it starts with one big decision followed by hundreds more little ones.

If your money isn’t trending in the direction you want it to be, it’s time to take that first step!

Now to July’s $$$ numbers…

[We post these updates here on the blog once a month to show a real-life snapshot of what someone’s money looks like and to get good discussions going around it. Tracking this stuff has been one of the best things I’ve ever done with my money, and I hope you are doing the same – even if you never share it with a soul! :) You can find all 115 of our net worth updates over time here.]

CASH SAVINGS (+$58.07): Nothing too exciting going down in this department. Shaved some expenses here (less daycare) and spent others there (beach vacation) and by the end of it we pretty much broke even. Though I must admit – it’s been nice working less over the summer, especially if it’s not affecting the income!

THRIFT SAVINGS PLAN (TSP) (+$503.24): The wife keeps on working, and the automatic transfers keep on hitting! I know the gov’t is all kinds of bonkers right now, but man – their benefits sure are killer for its employees. I hope everyone working there is taking full advantage of it while they can! Never know what’s around the corner w/ those guys…

ROTH IRAs (+$2,418.48): A nice little boost here as well. It’s been a few months since we’ve put anything into it (we max it out once a year after tax time), but I swear one of these days I’m going to go back to the monthly deposits… still just chicken since life keeps fluctuating so much lately.

SEP IRA ($8,806.76): Same with this bad boy here too – nothing new added while the market keeps doing its market thing. Awfully fun to watch when you have money invested in it, but won’t be so much as soon as it starts crashing ;) And we all know it will – it’s just a matter of when!

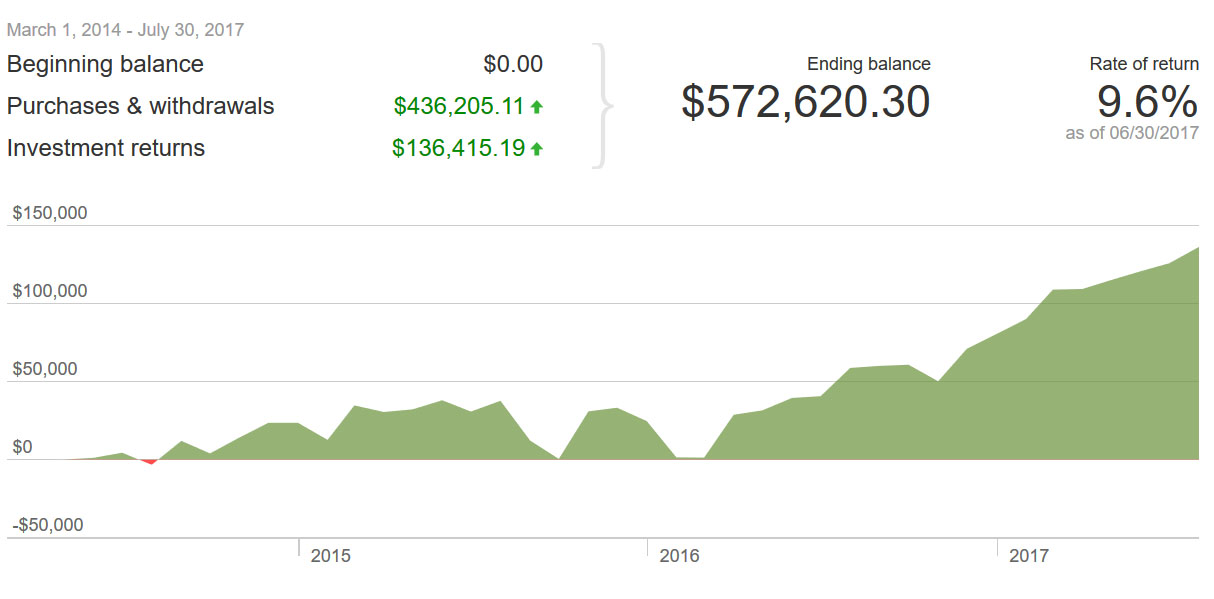

Here’s a screenshot from our Vanguard account since moving over the other year:

CAR VALUES (-$127.00): Nothing too exciting going down in this department – just the cars doing what they naturally do – depreciate. Here’s the values of them per Kelly Blue Book:

- Lexus RX350: $12,203.00

- Toyota Corolla: $3,955.00

CAR LOAN: (-$466.20): We continue to send a few hundred extra towards it every month! In fact, I’m pretty sure I accidentally paid like 3 months worth of interest ahead or something as it shows my next payment is due in December, haha… But can’t stop me from keeping going ;)

And that’s July’s net worth!

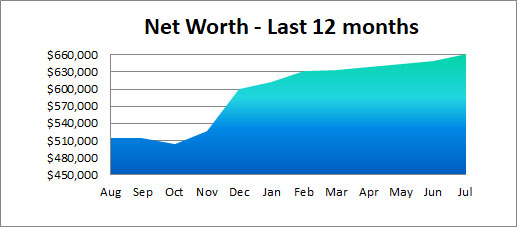

Here’s a quick snapshot of how it’s performed over the past year – with sexy gradient and all:

And of course, we can’t forget about my little nugget’s net worths… They may be only 3 and 5, but everyone has a financial footprint! Whether they know about it or not!

As always, you can see all 100+ previous net worth updates of ours here, and of course the net worths of 300+ other bloggers’ here as well, courtesy of my sister site, Rockstar Finance.

Keep on tracking that money, everyone!

Your money comes and goes by *choice,* not by chance!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Don’t read net worth updates while feeding babies, bottle gone without burping

Awesome to see the market cranking that Net Worth up so much in a month. Remember when everyone thought we were inflated with the Dow at 19k? Flew past that milestone!

Hah – yeah we did.

I came across some old newspaper clippings from from the late 1990’s and the Dow was around 9,000 something! it’s doubled in 20 years – crazy!

In the early months of 1996, Money magazine had a cover story asking if the Dow would cross 6,000 mark. Yup – it did in October of that year. And it was a big deal!

….and that means we have more than tripled in 21 years. :)

Pretty wild!!

I’d say that’s a pretty good month if you were able to take some time off and still do so well! My kids are always saying they didn’t mean to break things… I’m pretty sure it’s always the latter reason you mentioned :)

Our moment was about 6 years ago, when I finally accepted that paying 18% interest on a vehicle was really stupid. And then we kicked it into high gear to pay off all our debt and start working towards FI.

Everyone def has their moment that they realize what’s important. For us, having more time together is so much more important that spending tons of money.

Great month!

18%! That should be illegal!

Nice, well done mate! I cannot get enough of looking at graphs that keep going up, including yours. But before I’m getting ahead of myself here, I’m also very curious (and scared) to see what happens to the portfolio values of the various bloggers (including ours) when the market does tank…..

Oh, it’ll tank alright! No doubt about it! The question is whether you’re brave enough to ride it out (and scoop up the deals!) or you liquidate and run for the hills ;)

Niiiiice! That’s a good looking bump based on your investment increases… amazing how in a market like this, we can just sit back and watch it roll in (though I know that won’t last forever!).

Awesome! Love seeing investment accounts continue to go up even when you aren’t putting anything into them. Woohoo!

This year is pretty much the textbook example of why I don’t try to time the market. If I did, I would have pulled everything out last fall and missed the market going crazy!

Congrats on the growth!

Haha – yup! And the same goes in the opposite direction too – when you try timing *when to get back in* as well. That’s why i love this passive index investing route – I just put it in during good times or bad and then let the markets do their thing! No more timing for me anymore either.

Love seeing all those green numbers! So how are you feeling about the Lexus these days? That loan balance getting to you yet or are you still all good with it?

I actually had a dream last night that I was shopping for used cars in the $2,000 market haha… That probably means that I miss my old Cadillac (which I do!), but not enough for me to sell and go back :)

Looks like a solid month!

When we had a car loan I fought the bank every time I paid extra because they liked to default it to the next month’s payment instead of onto the principle! I guess they make more money that way but it was really frustrating to deal with that all the time.

I’m pretty happy because I was able to convince another guy at work to start tracking his net worth!

Nice work!

I always see that “principal only” option when paying down ours, but I never click it which is why it probably keeps paying future months off haha… Probably should stop that :)

ALWAYS hit the principal button. You will still pay the loan off sooner but you’re paying them interest before they’ve “earned” it. So you aren’t saving any money even though you pay it off sooner.

Another solid month. Any thought on paying off the car loan? If you did you’d still be left with a sizable cash reserve.

I’ll probably pay it off at the end of the year when our 2nd installment hits from the portion of the blog I sold last year when teaming up with my tech friends. Still very much in no rush to liquidate our current savings – it keeps us at peace, especially with me in this recent stint of not wanting to work as much anymore :)

Congrats on another successful month of net worth increase. It’s really inspiring to see your net worth go up every month, especially over the past year.

P.S. The piggy bank’s color looks so pretty!

Yeah! That’s why I bought it years ago – thought it was fun looking :) Went to donate it last year and then realized my kids would probably want it, but little did we know of its fate! Haha…

Congrats on the growth! Have to love market booms – we’ll all just have to remember the good feelings when things shift.

Did you replace the kids’ piggy bank or make them pay for a new one? It looks like it was a cute one!

No no, I just found another jar for them to put it in for now until we get a new one. I’m a sucker and would feel bad having them use their own money :(

I went up $7,300 last month.

Just noticed FI looks suspiciously similar to Fl with a lowercase L.

I guess everyone is just trying to get to Florida. And who wouldn’t, really?

HAH! There are a lot of retired people there :)

Thank you for publicly posting your net worth. Your blog is the first place I’ve seen this and it is how I learned to track my own. I started tracking my family’s net worth 17 months ago and we were on the wrong side of zero. Like in the negative 50k. We’ve been working hard to hit zero and August first 2017 is when it finally happened! I was expecting to get there this fall so it was a huge surprise to see it this early. I am a teacher so I don’t get paid in the summer so we save to cover expenses and go into a holding pattern for 9 weeks. I was blown away to see a positive of over 5k. This is just what I needed to make the final push for the next few weeks of no paychecks for me and a dwindling summer savings account.

BOOM! Love it!

I’m sure you addressed this in a previous post but is there a reason you aren’t doing $18K/year into the TSP? I feel like daycare was the answer but I thought I would ask since I can remember specifically.

Excluding the $112k I have in 529 plans I keep flirting with the $300k line (depending on the day…). I just picked up an employee so I should be able to max my wife out this year too. it will be all before tax time though… still better than nothing at all. My goal was to hit $200,000 in just vanguard before the EOY, but I would need some serious help to hit that. Looks like Ill be about $10k shy, I will however finally have a 6 figure 401k, which is awesome for me having just got to the point I can dump significant money into retirement about 3 years ago. Self employed up to 54K a year contributions FTW!

Dammmmn yeah it is! Good for you!

We don’t max out my wife’s TSP simply because we need the money :) Moving up to this place blew our expenses out the door – especially with childcare – so most of it is just going directly to our budget every month. Things will get better once our oldest heads off to school this Fall, along with my wife getting a raise here shortly now that it’s been a year (woo!), but until we move out of here we’re stuck w/ a bulk of the high costs. Which I know you know of all too well too :)

Yeah, I try to rest easy knowing that this is considered a person’s most expensive time of their life. It helps sometimes, and other times well….I feel like putting my socks on OVER my shoes….

Your SEP IRA is pretty awesome. Nice job with that.

Yeah, why not max out your TSP. :) Just keep increasing it every year and I’m sure you’ll max it out very soon. The TSP is really an awesome way to invest. So easy and very low fees. Once the kids go to school it should be much easier, unless you send them to an expensive private school… Keep at it.

Yup, once the $$$ is freed up more it’ll all go straight back into investments

Keep on keeping on. Slow and steady growth is the way to win.

With fancy gradient?? Be still my beating heart. It’s so fancy! Oh yeah, I guess I like the numbers it represents too. I just hit $100k in my 401k and I am PUMPED! I hope to hit $200k by the end of the year total, but we’ll see if that’s going to happen. (Ridiculous house is ridiculous.)

See you in DC end of Sept? I’ll be there for a whole week for work!

I hope so! That would be fun! :)

Thanks for sharing the Excel templates. I keep going back and forth between manual tracking and using Mint or Personal Capital. At heart, I’m sort of a financial nerd, so I like to create my own charts and tracking tools in Excel, but the automation and insights from Personal Capital are appealing.

Just curious – why the car payments? Maybe you explained this in a previous post, but couldn’t you just write a check and be debt free? I have a car payment, too, so I’m not throwing stones here!

Try out Tiller – they may be the perfect concoction for you as they merge automation WITH spreadsheets!

Car payment – I like hoarding cash cuz my online income fluctuates a lot. I’m also trying to work less over time which probably means earning less too (though I’m trying to find that magical sweet spot!) so for now the peace of savings trumps everything :)

Up 16.3K to 763K. Nice new high – broke 3/4 mil. Sort of waiting for the inevitable correction.

J, are you sure that the financing company isn’t just counting your additional amounts toward future payments? I.E. if they are saying you don’t have to pay until Dec, they may not be applying the extra dough towards principal (thus lowering the interest you will pay).

If they apply the extra payments towards principal they would still be expecting a payment every month. I’m thinking you aren’t actually saving interest if they choose to count the extra funds against future payments. Essentially, you would be giving them an interest free loan.

I think you’re right there – I’m *future paying* the loan amounts instead of wiping away the principal each time I send over the $$$…

I’ll click “principal only” next time and see what happens :)

I kind of miss doing our net worth updates. I personally got a lot out of the accountability aspect, but too many people in real life know about the blog now and I can’t bring myself to throw the figures out.

So I’ll do the next best thing and get motivation from you guys!

Ahhhh yeah, def. gets weird once people in real life see it haha…

If you’re still tracking at home though you should still be getting accountability for yourself? Just privately?

You’d think so, but I’m an extrovert. I think that’s half of the motivation for me to write: to get to interact with others in the comments.

I’m kind of crap when it comes to keeping myself accountable.

Still, once a year I’ll post my budget and (next week?) I do my annual, birthday check-in to see if we’re on track to hit FI by forty. That’ll be my annual dose of accountability.

Nice net worth growth J$. Keep on truckin! Pretty soon you’ll be in the seven figures!

Just trying to catch up to you!

That graph certainly has gradient that is sexy enough to be worthy of this blog. Nicely done!

We had a bumper July over at the BITA household, up $65.6k for the month. We also took our first camping trip (well my first anyway, and Toddler BITA’s), and it was SO. MUCH. FUN.

$65k – wow. That’s a year’s salary for people – and that’s before taxes and expenses!!

This was inspiring J$! The BF started tracking his network at the begin of the year, and he is already up $3K+ … I need to start doing the same. Thanks for the spreadsheet.

DO IT, BELLE!!! You’ll become even sexier, if that’s possible! ;)

Baby Penny and Baby Nickel are killing it- like those names by the way! And you are too! I agree that this month was a good month for the markets, it’s always nice when the net worth numbers are in the positive :)

Good for you. Another great month. For me, it feels surreal when I check my net worth and see $10k increases in one month. It shows that hard work, sacrifice, and the markets are all paying off.

I like that quote in the intro. It’s so absolutely true – “choice” really does shape our lives much more than chance.

Yeah! Clever wordplay too riffing off chance :)

Nice update! You’re slowly inching up to the double-comma club! I’m looking forward to that blog post. :D

I hit $100K net worth in Dec. of last year, and I just finally hit $100K just in the 403(b) alone this month! Hoping to make $150K total net worth by the end of the year, but as with you, a lot of that is at the mercy of Mr. Market.

Keep on truckin’, J! Love seeing these net worth updates. ;-)

Congrats to you too, my man! gotta hit $150,00 before you hit $1,150,000 :)

Congrats and great update! It certainly helps that the markets have been very kind to us all this year. But being smart like moving money into low-cost Vanguard accounts will ensure you make the most of the market! Great to see your progress I think I’ll start a net-worth post soon. Did I see that correctly, no home/mortgage… you’ve got to be a good post on that topic yeah?

Do it! It’s super helpful to track, even if you don’t publicize anywhere.

Correct – no mortgage, but only because we rent :) We owned for 9 years prior and finally sold the place last year to gain back more freedom/peace of mind. Loving it.

Everything seems to be on the up and up, speck-tack-alur (thanks T.Hanks). I don’t know about you, but I can’t wait for the markets to drop, dip, crash, or falter. Well, like you, I am contributing to things like TSP and IRAs, but I am also not dumping a ton of cash into the pool. Waiting for that inevitable correction… Just curious, how much of an emergency fund you keep on hand?

Yup – the same! The markets are starting to freak me out, haha… I want it to cool down for a while :)

Emergency Fund – most of that cash up there acts as an e-fund for us. It’s fluctuated from $5,000 to $90,000 over the years depending on what’s going on in our lives and what my online businesses are doing. (As well as what makes my wife happy – who’s much more conservative than I am :))

Congrats on the growth bud.

I really love the quote too “Choice, not chance, determines your fate.” I really don’t have much sympathy for people buying a $10 cocktails while whining about how they make minimum wages. Or not taking actions to change for the better.

Congrats J. Money on crushing it this month. I just started my own blog to track my net worth, and it’s always great to see the numbers go up (or down if it’s debt). Looking forward to the next bear market to snag some more investments hopefully not at these crazy valuations. But at least for now, happy to be seeing green everywhere!

Hell yeah, brotha.

Congrats on the new blog! Make sure you submit it over to our Directory to get you some free exposure: http://directory.rockstarfinance.com/submit-blog

“Your money comes and goes by *choice,* not by chance!”. I wouldn’t be able to find another simpler phrase to describe my philosophy when it come to managing my money. I wouldn’t leave my financial future to chances and I would never count on the security of government members money to sustain my livelihood when I am retired. Hence I choose to buildup own path and depend on my own wealth rather than the keys kindness of government programs.

Nice month for you! Especially with more downtime and vacation with your family! My July ended well, but I have some big dental expenses coming and I know that I will just have to keep on plugging away.

J –

Another positive month from the market, haha. Great job to reduce expense to allocate more towards experiences, though, has been the big takeaway from your post this go around. Talk soon JM, and keep the cash flow coming in to continue to build those assets up. Let the cycle do it’s thing.

-Lanny

Same to you, brother!

I just invested $20K in VIMSX (Vanguard Mutual Fund). Which Vanguard Mutual Fund are you invested in?

Sweet! I’m in VTSAX :)

I think I probably say this every time, but that rate of return is awesome! 9.6%!

What is your allocation J.Money? Are you 100% stocks? We’ve got 70% of our portfolio in mix of domestic and international stocks plus 30% in bonds/bank deposits. Early in my investing “career” I had a big loss that made me realize my risk tolerance isn’t as high as I thought. As a result my wife and I are somewhat conservative with our portfolio. Less return but less worry too.

Smart to change it up like that when you figure it out! I’m 100% in stocks right now like the old you :) 100% in VTSAX specifically, with Vanguard. I may branch out to international and bonds later to have the 3-fund portfolio going as it’s probably smarter, but for now just trying to reap it all in before I get conservative in my old age… Check in again though after this upcoming crash ;)

I’m confused. I see your networth listed as both $1.8M and $660k. I’m sure house is part, but where can I read where you post the difference in what is tracked here vs your total? I hope I’m not missing it above.

Second question…as I contemplate FIRE, do you or have you read of a strategy beyond an emergency fund of cash? Example: Stock market for us crashes, and your VTSAX is at 50% value for 60 months. Do you have tiers of investments that are more conservative to replenish your emergency fund when it is depleted during that 5 year drought?

You’re probably getting my numbers confused with Mr 1500’s numbers who writes for us on Wednesdays :) He’s got $1.8 million net worth and is retired early, while I’m at the $660k and still working on attaining that beautiful freedom.

Tiers of investments — I do not personally have anything like that set up as my plan is to just keep throwing more money into it when they’re all 50% off in that example, but again I’m not retired and needing to live off it yet. I’d check out some of the FIRE bloggers already there or working on it as they tend to focus much more on this stuff than the daily $$$ life that I do :)

Here’s a handful of them from our Directory, followed by our “best list” which also features some FIRE bloggers:

http://directory.rockstarfinance.com/personal-finance-blogs/category/early-retirement

http://directory.rockstarfinance.com/best-money-blogs