Morning, net worth lovers!!

Did you open up your accounts this morning and see a nice surprise too? ;)

I literally log in only once a month for these reports, so I never know what I’m going to get until I’m in there, haha… Maybe that makes me a bad personal finance blogger, I don’t know, but for sanity reasons I just can’t take the daily look-ins like I used to!

Though it was great when I was still wrapping my head around things… And something smart to do with ALL your accounts, really, until you get a good grasp of where your money’s coming and going. Once you get into a rhythm you can relax more knowing the ship’s steering in the right direction!

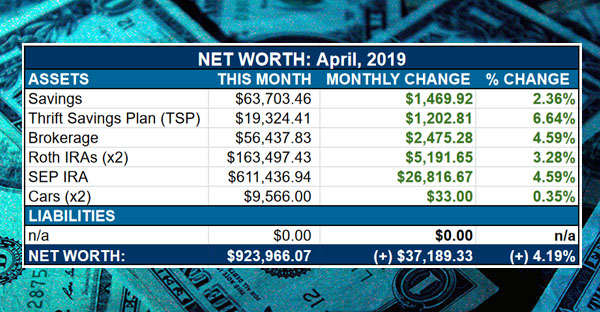

At any rate, it’s a good month to be invested in the markets! We hit a new high this month eclipsing the previous $902,133.51 mark from back in September, and now we’re that much closer to that ever elusive double comma club… 11 years in the making already with I’m sure more to go ;)

Whoever says this stuff is fast is a cold blooded liar! But you do get there eventually so keep on truckin’! And enjoy the journey along the way!

Here’s what April looked like for us…

[This is part #135 of our Net Worth Series, where we share our real life #’s every month no matter how good or bad or downright ugly they are, haha… This was by far the most powerful thing I saw when I stumbled across the PF world myself years ago, and have since made a commitment to do the same when starting my own bog over 11 years ago now too… I hope it motivates you just the same!]

CASH SAVINGS: $63,703.46 (+$1,469.92): Just an average month going on here without any major surprises one way or the other… which I’ll take any month when it comes to cash flow! :)

THRIFT SAVINGS PLAN (TSP): $19,324.41 (+$1,202.81): A nice normal bump here as well, as the wife continues to regularly contribute to her retirement account at work and snagging all those (FREE!) matches… One of the easiest ways to double your money right on the spot!

BROKERAGE: $56,437.83 (+$2,475.28): Great little bump here too, as the markets continue to do their thing even when you’re not contributing a penny to it :) (The beauty of passive income!)

ROTH IRAs: $163,497.43 ($5,191.65): Same dealio here – only the #’s start to rise even more the bigger amounts you’ve got stashed away! Which again is crazy since you’re literally not doing a thing to grow it. (Though the reverse is very much true also, haha, and it can just as easily sting as much as reward when the markets throw their hissy fits ;))

SEP IRA: $611,436.94 (+$26,816.67): The biggest bulk of profit this month! Though it’s not true “profit” until you actually cash out of it, which we have no plans on doing anytime soon, so… Still a nice thing to see though than the opposite ;)

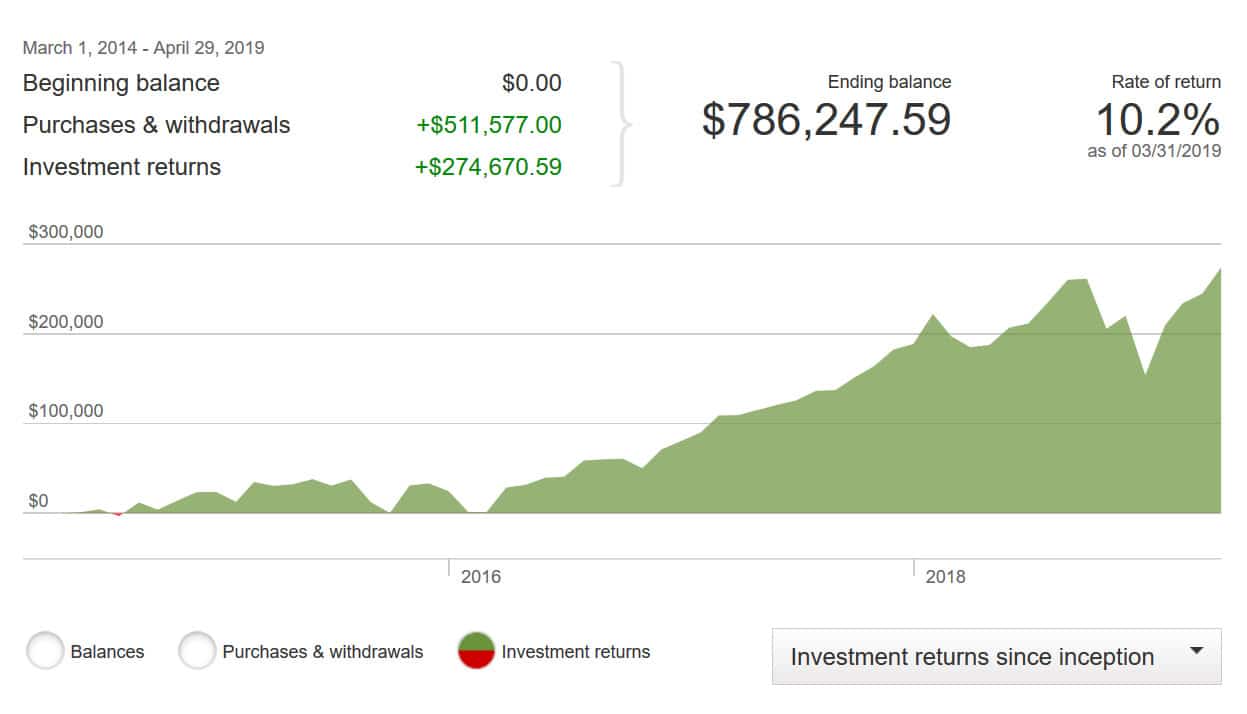

Here’s a snapshot of how our investments have fared in recent years:

(Everything is in Vanguard’s VTSAX index fund)

CAR VALUES: $9,566.00 (+$33.00) — Finally, the cars! Who didn’t want to be the only ding in this month’s report apparently, haha… But it’s what KBB is reporting, so we do too as we always do!

Here’s what they say our current two rides are worth, both completely paid off:

- 2008 Lexus RX350: $7,005.00 (up $31.00)

- 2005 Toyota Corolla: $2,561.00 (up $2.00, haha…)

(Our minivan search has been put on pause since house hunting, but my wife assures me it’s only temporary and we’ll be getting right back to it as soon as we sign on the dotted line, haha… But I’ll be enjoying every last day of delay in the meantime! ;))

And that’s April!

Total change in net worth this month: (+) $37,189.33

Can’t complain about that one bit…

But again, what a wild ride it’s been these past handful of months!

That’s a $110,000 rally since The Red Wedding of last year! Insane!

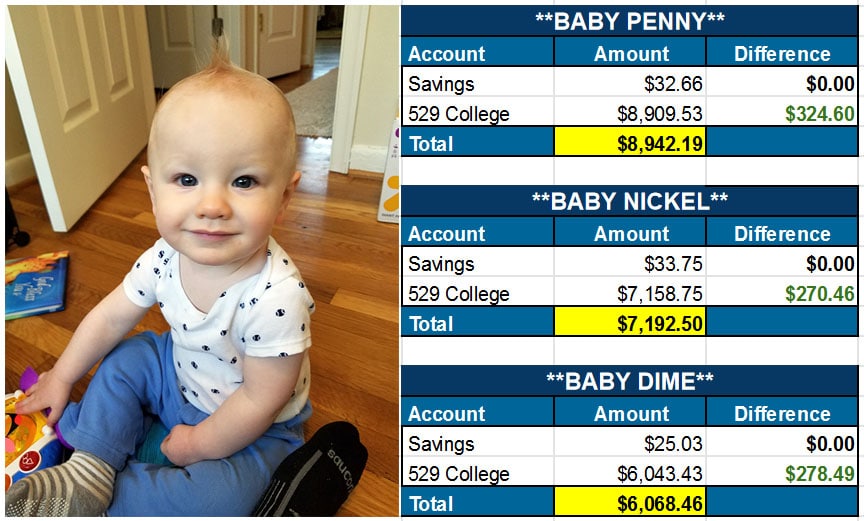

Lastly, here’s the KIDS’ net worths as we like to post up here monthly too:

A nice little bump for all, to match my wee one’s nice little ‘hawk daddy recently gave him ;) Who is the only boy in my household who will let me do that to them!! Don’t they know it’s all the rage?!

(I do get a kick out of what some of their classmates call me though – “Dinosaur Dad,” haha… There could be worse things! ;))

How’d you guys end up faring this month?! You enjoying the current ride of investments too? Anyone a freshly minted Millionaire now?! :)

As always, feel free to share or ask anything down in the comment section and we’ll discuss! It’s a 100% free zone here to talk turkey without anyone glaring at you! Unlike the “real” (boring) world! ;)

Your friend in finance,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Hi J,

Insiprational bud! Was looking forward to your update today to see how you got on.

I left a comment last month about my goal to hit £30k net worth by age 30 (13 months time).

I was at around £13.2k last month. You asked to get in touch when I acheive this…… I just have!!! £47.5k. around $62k I believe.

A bit of a strange reason why this has come about, but involved working out current pension pots within a system that does not give visable access to current value. Strange system but same as all those in the Civil Service in the UK.

Anyway I will be raising a drink to us both!

Got my next goal set up – to pay off car loan of £4.5k by the end of the year.

Peace out,

Doug

Rock on man!! No car debt is a damn good feeling – keep going!! Totally doable goal!

That’s another 3.5 miles of that thin green line and getting closer to the elusive second comma.

Congrats on the new high.

Did you just reference that net worth mileage post from earlier this year??

Haha… already forgot about that one but so fun! :)

(here it is for anyone else interested: https://budgetsaresexy.com/money-trails-a-useless-but-fun-perspective-on-money/ )

I was interested! At first I was all disappointed to find yet another fun net worth trick I can’t do until I’m out of the negatives (sometime next year) but then I realized: just use the absolute value of my net worth, measure a distance starting from home, and see where I’m “coming home from”.

If net worth zero is home, last month I was at my favorite pizza place. I guess that’s sort of like bringing home the bacon… bringing home the pizza…!

Hahaha that is a cool way of hacking it!! I like that! :)

At long last, after months of flirting, barely cleared half a million last month, and then this month got over $525,000. I guess the market is making up for a lower few months. A return to the mean.

You’re a solid half-a-millionaire now, baby! Congrats on the continued climb!

When you say everything is in VTSAX… do you mean EVERYTHING? haha silly question probably but do you mean the brokerage account, Roth IRA’s, SEP, TSP, everything everything? I always wondered what exactly you were investing into in each account. My husband and I are just getting started investing and are young enough to go aggressively for quite some time but I still have concerns about putting “everything” into one index fund I guess. Maybe because it would feel “too easy”?! I also think its because we are just getting started and although I’ve learned a lot from financial blogs it all still feels very new and obviously I have concerns about making wrong choices haha. Can you tell me your insight as to what makes you feel comfortable enough to do this. Did always put everything in VTSAX from the beginning. Would love to hear as I’m trying to educate myself as much as possible on finances and investing :)) Thanks in advance!

Here you go!

The two articles that covers this stuff since we first switched over to Vanguard and VTSAX :) It def. feels “too easy” but that’s also exactly why I like it, haha.. I don’t need to make the best returns every year – I just need to make “good enough!”.

https://budgetsaresexy.com/say-hello-to-vanguards-newest-member/

https://budgetsaresexy.com/lazy-one-fund-investing-strategy/

(And yup – VTSAX is all I have in my SEP IRA and ROTH IRA which accounts for a bulk of our household invesments… My wife’s TSP and IRA is a bit more diversified but still in mutual and other index funds)

Please do continue learning about the different strategies out there – no right answer to any of this, only the one that makes the mos sense to you guys!

Hi J!

Awesome thanks so much for the direction! (it was too good and now I’m back ha) Those 2 articles were SUPER informative and just what I needed (along with the linked articles within the articles:) 2 more questions for you.

1. Have you ever written any articles about how much you are able to put into the investments over the months, quarters, years? I was looking for a breakdown, thought it would be interesting to see the comparison of how much you and your wife were able to put away along with the market adjusting. Life happens right, so its not consistently the same amount year over year and the market changes as well as your investment decisions but I thought it might be cool to see I from the other side of the table. (you referenced those other 2 articles quicker than I could search for them:) )

2. What do you do in a 401K when vanguard is not an option? Curious to hear your thoughts on this. S&P500 100% contribution or do you try and mimic the VTSAX if that’s an option…or something else entirely I’m not thinking of? I have low fees for both options but S&P alone would be a lower fee total vs having 3-4 options I contribute to. I’ve been contemplating this currently and blogs go back and forth over this topic. Is this a personality (aggressive vs less aggressive) call?…

How much I invest — It’s actually somewhat similar every year as I only have one main goal to hit no matter what: Max out my retirement accounts!! :) Which includes my SEP Ira and Roth IRA, and then my wife’s Roth IRA too if we have more money left over…

Here’s some posts I wrote on it if it helps – it’s the backbone of our net worth!

https://budgetsaresexy.com/my-1-financial-goal-each-year-max-out/

https://budgetsaresexy.com/power-doing-one-financial-thing/

When Vanguard isn’t an option — Yup, pretty much what you mentioned! Just looking for the closest funds which would be other market indexes depending on what you’re going for :) Some people just stick with the one overall index (like me), while others prefer diversifying more and throwing in some bond indexes or foreign indexes as well. Really just depends on your comfortability and plan.

When you leave jobs though you can move it all into whatever you want! Just make sure to *transfer* it and not cash out and then re-invest so you don’t get hit with all the penalties!

What I like best about the Net Worth update is being able to compare percentages more so than total volume of money. Everyone’s total volume will be different (dependent upon saving rate), but it’s nice having a “friend” such as you to check my Rate of Return. We are always very close (such as your 4.59% and my 4.89% last month). It’s a nice test, to not see who is better, but to have a barometer to check against the long term financial climate and not the daily financial weather pattern. To that sir, you provide a very valuable service and as always…I thank you.

Happy to oblige!

“long term financial climate and not the daily financial weather pattern”

love that, haha…

Damn! You could theoretically be a millionaire next month! You need “only” about an 8.5% gain. While high, that’s definitely not outside the realm of possibility! :D

I’ll take it, even for just a day :)

Welcome to the world of $100K swings in net worth.

You’re so close to touching the $1.0M benchmark for the first time. Another 8.04% and you’ll see your dashboard light up and naked dancing girls will pirouette across your screen.

Ooooh really???

In that case I’ll double my Hustle game this month!!!

Since January 1 our total retirement balances are up just shy of $70k (on about $20k of additional investment in the last four months). Our HSA investments are similarly riding some nice highs. This is really mind-warping stuff. I imagine I’ll care more about percentages and sustainability in ten years when we’re right on top of FIRE… but right now, those big ol’ numbers sure do get the endorphins flowing.

Net worth is less important for us, I think. The house isn’t going anywhere and our ancient beat-up cars are probably net liabilities. That said, it feels pretty good to send in another mortgage payment. 102 down, 136 to go!

Something tells me you’ll have much less than 136 to go unless you’re playing that investment game over there with the difference of $$$ :) Pretty good on all accounts though! Literally!

Congratulations! You are killing it! You could be a unicorn next month!

I’m still gaining but it’s true what they say, the gains pick up as the gaining gets going (is that really what they say?!). Something ticked in side me a short time ago and I have been stuffing everything I come across away rather than keeping the ‘safety net’ and I’m noticing it’s amazing how much that actually helps. I’m not to the half mil point yet, but maybe this time next year?!

Dinosaur dad…..do you think that’s the hawk or the age??? Kidding kidding, but I couldn’t help myself. You know we are ancient to this youngins!

YOU STOP!!! Haha….

Although my kids do like to tease me about all the gray hair in my beard and go around calling me “old man” while pretending to walk with a cane, haha… I tell them each one is from a day they’ve been in my life ;)

I found an old excel file from 2008 where I was tracking my cash tips from the waitressing job I had in college (I’ve always loved excel). In that file I noted I had $3,221.13 in my bank account which was the extent of my net worth.

Today my net worth is over $215k!!! I’ve been tracking it for 2 years since finding your blog so I know how much it’s grown but it’s extra awesome to see how far I’ve come since college.

Huzzah!!! And I bet it only grows faster with each passing year too!

The first $100,000 is the hardest!

942.6K up a modest 2.5K to another new high. Up $54K from last Sept.

Sometimes Zillow addeth to the property valuation, but lately it has been taking away.

Nice jump this month, J!

only means I’m gaining on you faster!! haha…

but it’ll start taking away from me too as soon as we lock in on that house, womp womp…

That is true. It would give our asset allocations a little more in common. :)

But you’ve still got that second income that will ultimately coat me in your dust as you lap me. :))

Haha also true!! Which I am 1,000% thankful for as it was starting to get rough there for a while…

Yeah man, it’s been nice watching those returns do well! I’m still in the gotta check mode, but I’ve trained myself to give a quick woohoo during the good times and a “eh, stocks are on sale” during the downturns, and move on. I haven’t quite shaken that false hope that I will wake up one day and my accounts will somehow have magically reached the FIRE number. I’ll work on that!

Well one day it WILL reach that number, it’s just a matter of *when* haha…

Checking your investments on a monthly basis is probably about right. The trend long term is up, but the day to day is an upset stomach waiting to happen.

Congratulations on your new high, J! You’ll be a millionaire before you know it. We check ours in the middle of the month. We’re still working toward 0, but hopefully we’ll be a little closer!

Gotta pass $0.00 before you can $1,000,000!

Keep on going!! :)

Congrats, J! I haven’t checked mine in a while and TBH don’t closely follow the highs and lows of the market (lest I start checking my accounts every day), but you’ve inspired me to see what’s happening today.

I’m not anywhere near 900K+, but it’s in the plan! :)

Jules

I want an email once you cross it :)

I finally made it to the 6 figure club! Woohoo!

Now I’ve got to do that 9 more times…

PARTY TIME!!! WOO!!!!

J – I’ve been following along with you the last 25 months and just crossed the $600k level to set a new personal record. What amazes me is the size of increases even though I make the same monthly contributions to my 401k and brokerage accounts. The power of compound interest!

YUP!!! That’s the beauty of it all!!! Takes FOREVER to get going, but once you do it becomes a cakewalk with each passing month :)

You’ll hit $700k and then $1,000,000 in no time now… depending on how the market behaves at least, haha… Congrats on the growth!

We hit a new top net worth this month! 600k! That’s after dropping 60k cash into buying my husbands business this year

I had a few notes this month I’d love feedback from you and/or readers on!

1) did KBB change their algorithms? Occasionally one of our vehicles will increase in value by a couple hundred. This month was way different. Our oldest vehicle increased by 1500! And the three vehicles together raised by 2700 total. The only other explanation i can think of is that used cars in our area just had a massive increase in demand? (Just made the last payment on the truck…one loan left!)

2) I finally figured out a way to track my home value that I like! Zillow or Redfin swing too wildly for my tastes, and I could t figure out a good algorithm for adjusting my personal market value assessment. So! I took the value of the house at purchase and used the CPI calculator for each month. It shows a nice steady increase in value and seems to be a reasonable but conservative estimate of current value. Since homes in general seem to track with inflation it seems like a reasonable method? Especially since I would rather under value the house and not include any improvements to the value as far as net worth tracking goes.

Would love comments and opinions though!

Congrats on the new new high!

Do you include the business in the tracking, or no? (I don’t put my projects in it, but if/when they sell and I get an influx of cash it’ll then show up! :))

KBB – interesting to hear it’s happening to others too! Maybe used cars are coming back in popularity! Haha… (yeah right, probably just an algorithm thing :))

Home value — I always struggled with that myself when we owned. Eventually I just had my realtor run comps and tell me what the market value was about once a year and then kept it there until we ran it again. That was nice because it gave me a more accurate picture if I were to list it on the market at that time, and then my realtor liked it too because he knew I’d be going to him the day we ever DID put it on the market (which we eventually did with him!). In fact, it ended up selling within $1,000 of what he had told me the value was just months earlier :) (And it was nice not having to re-evaluate the house every month in the net worth updates too)

Great job man. Been watching you for years. I’m also a Fed Govt employee. How much does your wife contribute towards TSP? How much do you guys contribute to 529 plans

Oh cool! Thanks or reading – I’m glad you’re still enjoying it! :)

I think she’s a 5%? I can’t recall at the moment, but I know it’s enough to get as much of the matching at least as possible, and then we stopped it there as we were playing catch up with cash flow…. Something we should probably adjust again as that was a few years ago :)

Hello! Have you done any posts about the SEP IRA specifically? It seems like you’d have to be making a lot of money from a side hustle (like $250k!!!) in order to max that SEP IRA out. Or am I wrong on this?

SEP limits are a % of how much you make for a year, so you can always max it out – it’s just a matter of *how much* :) One year you can put in $4,000 if you don’t make much, and another $40,000 if you have a banner year!

Here’s more via Wikipedia: https://en.wikipedia.org/wiki/SEP-IRA

(Also there’s a cap on the highest dollar amount you can put in too)

Oh wow! So surely you must have a very large income in order to fill up your SEP IRA so much! I can’t imagine someone doing Uber as a side hustle, for instance, really being able to fill up their own personal SEP IRA that much

Been averaging around $15,000/year with SEP maxings lately… Used to be around $20,000-$25,000 but my hustling has slowed down over the years ;)