“Most millionaires measure their success by their net worth, not by their realized income. For the purposes of wealth building, income doesn’t matter that much. Once you’re in a high-income bracket, say $100,000 or $ 200,000 or more, it matters less how much more you make than what you do with what you already have.”

This snip is from one of my all time fav books, The Millionaire Next Door.

For those of you who are not tracking your net worth on a regular basis, I encourage you to START TODAY. Growing wealth isn’t about how much you make, it’s about how much money you keep.

Tracking ensures you’re moving in the right direction! Please let me know if I can help you in any way.

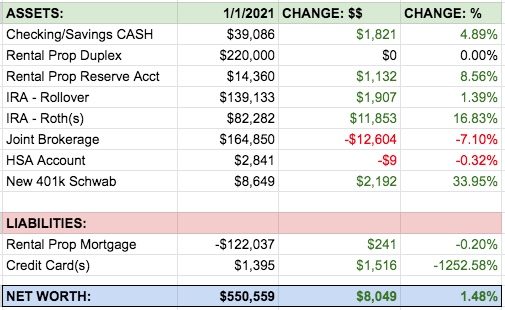

Feb 1, 2021, Net Worth: $550,559 (+$8,049)

Woot woot! Another month in the positive :)

Account summary below, as well as growth shown in dollars and percentages for each asset we’re tracking:

Here’s what went down in January…

Investment changes: We pulled $12k from our brokerage account and funded our Roth IRAs for 2021. Not really a *new* investment, more of a money shuffle for tax efficiency. Other than that, the only new money invested was ~$2k into my work 401(k) plan.

Travel refund: Over a year ago we pre-paid for an all-inclusive trip to Mexico for a friend’s wedding, but never got to travel due to covid… So the travel company finally just decided to give everyone their money back. Our credit card was refunded ~$2,500 which is why we didn’t have to pay it this month and we carry a positive balance!

Abnormal expenses: None. I guess this is a good thing? 🤷♂️ Boring months are sometimes the best months! It’s kind of nice taking a break from spending after the holiday season.

Small money wins and fun stories!

I love celebrating the small stuff. It all adds up. :)

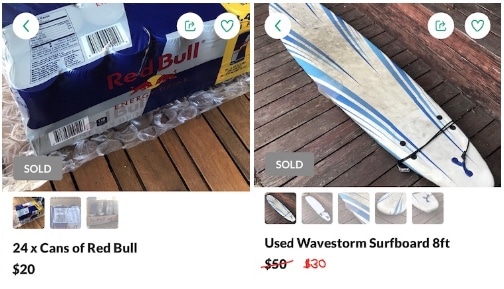

Last month, 6 boxes of Redbull accidentally got delivered to my neighbor’s house. It turns out a guy down the street from us is sponsored by Redbull, and they were sending him a care package but got his address wrong.

Anyway, after tracking the guy down and giving his Redbull to him, he gave us 3 x cases to say thanks. (We tried to refuse — we don’t drink energy drinks — but he insisted). My wife and I ended up with 1 of the cases, so I sold it for $20. 🤣

Also, I found a beaten up surfboard for free on Craigslist. I like having spare boards laying around for my beginner friends, but this was a little too broken, so I posted it online and sold it for $30!

One of my fun goals for 2021 was to make $1,000 from turning trash –> treasure. So I’m +$50 towards that goal so far! Maybe I’ll strike some luck and find some resellable stuff at Priscilla Presley’s estate sale next weekend!

Detailed Asset Breakdown:

CASH Accounts: $39,086 (+$1,821): Although we received our stimulus checks on Dec 31, ($1,200) I somehow didn’t include them in last month’s NW report. This as well as not having to pay a credit card bill this month means we have a higher cash balance heading into February!

Rental Property + Reserve Account: $234,360 (+$1,132): We had an absolute perfect month for rent collection and zero expenses outside property management. A great way to start the year! I 😍 this duplex.

IRA – Rollover: $139,133 (+$1,907): Back in December, I did some rebalancing and shuffled my index fund allocation a little bit. This IRA now has about $40k of FISVX (Small Cap Value Fund) and the rest is still total stock market index.

IRA – Roths: $82,282 (+11,853): We funded these Roths on January 4, moving money from our after-tax brokerage account. The reason I like funding Roth accounts as early as possible in the year is to take advantage of the tax free gains as soon as possible. All in all it looks like the funds actually lost money, because we moved $12k in and only have an ~$11k increase.

Joint Brokerage Account: $164,850 (-$12,604): Apart from the $12k we moved to the Roths, this brokerage account was also shuffled a tiny bit… In December, we reallocated $25k to VXUS (Total international index, minus US stocks) to give us some international exposure. Also we allocated $35k to BND (total bond market).

HSA: $2,841 (-$9): A tiny decrease as this account is invested in the total stock market index.

New 401(k) at work: $8,649 (+$2,192): Slow and steady wins the race. Although I probably can’t max this sucker out in 2021, I’m trying to frontload as much as I can into this 401(k) at the beginning of the year.

Breakdown of Liabilities

Rental Property Mortgage: -$122,037 (+$241): I’ve always considered this mortgage “good debt,” but for the first time in my life I thought about pre-paying this down a little bit. With the *hopeful* sale of some of my other rentals this year, I need to figure out a good place to put the cash proceeds. Paying down this mortgage is one of those options.

Credit Card Balances: +$1395 (+$1,516): Most people owe money to the credit card companies. This month, the credit card company owes ME money! This positive balance is due to the refund we got from our pre-paid vacation. :)

Overall, not a bad start to 2021! Considering the total stock market was pretty flat, or maybe negative a tiny bit, somehow we walked away with an $8k net worth increase.

Questions? Comments? How were your updates the past month? Any of you nerds part of this r/wallstreetbets group and wanna brag about the mcmillions you made?

Have a great weekend, my friends!

– Joel

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Joel – I love your goal to hit that $1,000 trash to treasure number. And what a cool start by selling a box of red bull and a surfboard! It sounds like you just have to keep your eyes open for these money-making opportunities. Keep up the great work!

Cheers,

Fiona

It’s amazing how much free stuff is just laying around, everywhere you go. Just gotta look for it! Happy Friday Fiona :)

Agreed with Millennial Money Woman up there – $1,000 treasure number is a fantastic goal :) not too easy, but def. not too hard either – esp when you have a year to accomplish! kinda forces you to always pay attention and keep the habit going.

Hey J$! Yep, selling stuff is a great habit and a constant reminder that everything has a value to someone out there. Plus, it’s FUN!

Have a great weekend my friend!

Hi Joel,

Congrats on a good month! We love boring months with no extra spending :) Quick question, if we have determined that investing in retirement funds are always better than paying down mortgage, why don’t you completely fund your 401k first before paying down your rental mortgage?

Thanks!

HM – I love the way you think! Umm… this is embarrassing to admit, but, I am already contributing 100% of my salary into my 401k. I know, it’s very small, but I only work part time right now. So there is no additional paycheck money available to put in there. So unless I get a pay raise or do more contract work for my employer (very possible!) I can’t put more in my 401k.

That being said, I can always invest excess money in our after-tax brokerage account. In the long run, mathematically, it should work out better than paying down our mortgage.

One last note…. Remember how I told you in your other comment that it all depends on the mortgage rate?… You are locking in at 2.5%, which has a huge difference to someone with say, 7%, etc.. Anyway, my mortgage for this rental is 4.125% which is low considering, but also given the expected lower returns in the stock market the next 10 years, maybe it’s just a safer play for some of my money. It’s just a thought.

Have a great weekend!

Awesome work! I always debate whether to front load my Roth as opposed to dollar cost averaging through the first half of the year. I was regretting the front load in March last year. But because my past self has already set an automatic $6,000 payment for the first of the year, it’s more work for me to change so I’m a front loader for life now haha.

haha! Mathematically, if you have the money, it’s better to front load in a lump sum than it is to dollar cost average. Play around with this calculator….

https://www.personalfinanceclub.com/lump-sum-vs-dollar-cost-average-calculator/

I front load my Roth in Jan so I don’t have to think about it for the rest of the year. (In the background I’m saving up for next year but that’s automatic.) I figure my 401k gives me enough dollar cost averaging.

Great start to your 1k goal!

I had a good start to my walking goal in Jan, but the East Coast snow storm has meant a slow start for Feb. I am proud of myself for getting out, and having a ‘start’ for the month. 0.5 or 1 mile is better than 0 miles.

Have a great weekend! I think people are excited about a Superb Owl?

Great to hear you’re staying active despite the cold! You’re right, even .5 miles is better than 0! Just raising your heart rate each day is a great goal. :)

Wishing you a great weekend too!

I track my net worth on occasion, but as I get closer to retirement, the more important number is the amount of income my net worth generates. Building a retirement paycheck is the ultimate goal of investing so it makes sense to focus on that number the closer you are to retirement. At some point, you’ll need to convert a growth portfolio to an income portfolio to make your wealth last.

Just two cents from a man approaching 50 ;-)

Sounds like a fun problem to solve over time! I have a vague idea about my draw down strategy, but it’s not really well thought out because i’m still years away from retirement. Good to keep in mind though for sure. Perhaps I should also start tracking rental property payments and cashflow, as well as dividends from all the funds I hold.

Have a great week!

Joel