I got the following note from a reader the other day…

“Joel, I noticed you keep a big emergency fund for your rental property. 2 questions for you…

1) It seems like you have too much cash because shouldn’t you only need 3-6 months of mortgage payments as a cash reserve?

2) Also why do you keep this emergency fund separate from your personal emergency fund?”

Great questions! It’s been a while since I calculated how much to keep in rental reserves, and admittedly I do probably have too much right now! So in this post I’m gonna run some math and figure out just how much I should really be stockpiling for emergencies.

Right now I’m sitting on $14,360 in my duplex emergency savings account. If it turns out I’m holding too much cash, then we have the fun problem of figuring out where to put the excess!

How Much Emergency Fund Do I need for a Rental Property?

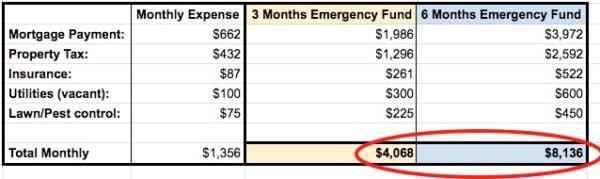

A general rule of thumb is about 3-6 months of expenses. While some investors only account for “PITI,” which stands for Principal + Interest, Tax and Insurance, I like to add a few other expenses in there to be on the conservative side.

Here are the PITI expenses for my rental property in Texas:

- Mortgage payment: $662 per month. This covers principal and interest only.

- Property tax: $432 per month. This is based on my 2020 tax year bill of $5,185. It increases slightly each year.

- Property insurance: $87 per month, based on my 2021 policy of $1,042 for the year.

Total “PITI” expenses = $1,181 per month.

There are 2 other expenses I like to add, and I’ll explain why:

- Utilities when vacant: ~$100 per month. When a rental property is vacant, the utility companies charge the property owner instead of a tenant. Even though there’s nobody living in the unit, workers need power for tools to fix stuff, and in Texas we need to keep the air conditioner on to make sure no moisture builds up in the house during hot and muggy days.

- Lawn maintenance & pest control: ~$75 per month. These expenses are necessary for all housing, whether I’m receiving rental income or not.

Total monthly expenses: $1,356!

All in all, based on the 3-6 months of expenses rule, I should keep somewhere between $4,000 and $8,000 in emergency savings.

Will this be enough to get me through an emergency? Let’s go through some potential disasters and look at the potential costs in an emergency scenario.

Disasters That an Emergency Fund Should Cover

The point of having an emergency fund is to cover unexpected expenses when shizzle hits the fan. Here’s what my emergency fund is mostly protecting me against…

Once-off disasters with large, upfront costs:

- Wind, Hail & Fire Disasters are covered under my insurance policy. My deductible is $2,310.

- Large appliance disasters like an A/C blow-up ($5k), water heater replacement ($1-2k), fridge/stove/kitchen appliance breaking ($1k).

- A new roof would cost me about $6k.

- Trashed units happen sometimes when a tenant moves out. If there’s property damage, it could be covered by my insurance policy, or if I need a small renovation I wouldn’t expect more than $5k of fixes needed.

This tree came down during a big storm a few years ago. Luckily, it fell the way it did. If it fell the opposite way, it would have hit my building, caused major damage, and displaced 2 tenants!

Longer term disasters are scarier, because they bleed you dry over months/years:

- Vacancies: With no rental income, I’d be missing out on $1,950 per month (my hard expenses are less — $1,356 per month like we calculated above). The beauty of having a duplex, though, is that it’s kinda rare to have both units vacant simultaneously. With only one renter in place, my loss is only half.

- Squatters or rent not being paid: Again, this would cost me loss of rent ($1,950 for both units per month). Thankfully, Texas has pretty decent laws that side mostly with landlords when it comes to eviction. The most I’ve ever had a squatter stay for without rent payment was ~90 days (under the first eviction moratorium in 2020).

So it looks like a 3 month cash reserve of $4,000 isn’t quite enough to cover some of the larger potential disasters. Personally, the minimum emergency fund I would like to keep is 6 months of expenses, so $8,136.

How to Build Up an Emergency Fund for a Rental Property

Before we go back to my personal scenario, you might be wondering if you have enough cash reserves for your rental property (or a new rental you’re planning to buy soon).

It never hurts to run through the exercises I just did above to evaluate your rental risks and potential disaster costs. Even if your bank tells you that “a few months of mortgage payments is enough to keep in reserves,” you should save more if you think you’ll need it.

I always recommend people build and store a separate emergency fund for rental property in addition to their personal emergency fund. This way, your family and your assets can both survive separate disasters simultaneously. One is not dependent on the other for survival.

2020 was a great example of multiple disasters happening at the same time. As a landlord, I had a separate emergency fund for each rental property I own, as well as a personal emergency fund for me and my wife. It’s certainly a lot of cash to be holding, but boy were we resting well at night knowing we had plenty of runway should we be unemployed *while* have failing real estate at the same time.

Looks Like My Rental Savings Account Is Too Big :)

Well, we’ve determined that a safe 6-month emergency fund for my rental property would be around $8,136. I currently have $14,360 in cash reserves, so definitely more than necessary!

I like round numbers, so maybe I should drop this cash reserve account to an even $10k, and invest the excess $4,360 elsewhere. I could drop it into the stock market, pay down the mortgage a little, or see if there are any strategic upgrades to make to the property that could attract higher rental income?

I’d love to hear how other real estate investors store their emergency fund for rental property and any good practices we can all share!

Make it a great day,

– Joel

Get blog posts automatically emailed to you!

Joel –

Thank you for sharing your thoughts on your emergency savings fund for rental properties. Although I don’t have a rental property myself (yet), I am planning ahead as it relates to those larger, possibly more devastating disasters such as vacancies, trashed rental units after tenants leave or (in my opinion the worst one), a new roof – where I live, roofs typically cost a boatload of money. I certainly agree that in the case of having rental units, it likely makes sense to sit on a portion of cash in case you need to utilize it for an emergency.

Thank you for sharing your insights!

Cheers,

Fiona

Things start to get really interesting when you have multiple properties and multiple emergency funds. It’s very tempting to go spend/reinvest that cash… But it’s really gotta be accessible when crap hits the fan. :)

I’m super conservative, so I like to h9ld 10 months worth of expenses (PITI, utilities, HOA fees) to cover unexpected problems. Also, I hold extra reserve for things I expect to replace soon (in other words, a sinking fund), such as an HVAC unit or roof replacement.

So, my approach to the reserve fund is told hold enough to weather both known and unknown expenses.

The goal is to avoid having the rental property investment affect my other investments. For example, I wouldn’t want to have to sell stocks in my personal account in order to pay for a big expense or extended vacancy in the rental property. The large reserve fund helps ensure that the rental property can stand on its own as an investment.

I hear ya Carroll! I also believe a rental should be self sufficient and not interfere with other assets. If assets are too interdependent they can come down like a house of cards in disaster time.

The downside of holding so much cash though is it lowers the overall return the investment provides. I know some people set up a tiered emergency fund approach, kind of like having a separate sinking fund but it’s invested in something that makes at least a little more interest than cash.

A tiered reserve fund is an interesting idea. I’m going to think about that.

Thanks for the feedback, and sorry about the typos in my comment above.

I love typos. Shows that you’re real! :). Have a great week!

Personally, I don’t think an extra $6k in your property’s emergency fund is that bad of an idea knowing the costs that can be incurred quickly in a home. I don’t know what part of Texas the property is in, but I do know that much of the state is still subject to hurricanes. Insurance companies will become real sticklers over the fine print of what they cover when there are big events like that and/or pull out of the state or not renew coverage en masse. I watched State Farm pull out of Florida for several years after the storms of 2005. So many homeowners and property owners had trouble finding any insurance after that year, and when they did it was common for the premiums to be over twice what they were before. You might need the fund to cover part of that increase when you can’t get it all from the tenant’s rental payments quick enough. Of course, then there are expenses like tree/landscaping additions or tree removals if a tree is at the end of it’s useful life. I recently had to remove 4 rotting Bradford Pear trees that had lived far beyond their average lifespan of 16-20yrs, and that cost about $3200 up front (worth.every.penny – those guys were amazing at what they did). Thankfully, planting new trees will not be nearly as expensive. I’m probably like you in that I would want to be able to weather something like that and still have money to cover it if I had a problem tenant that I had to evict or a vacancy. Perhaps one day when interest rates start going back up you could take some of what you would calculate as excess and lock in a CD ladder to keep some liquidity while also getting a tiny bit more of a return? Right now you have enough for 6 months of expense/tenant issues AND one new roof or HVAC system. I guess the other question is how old is the roof and HVAC? You could probably take a little more risk if they are new.

Awesome, I love the CD ladder idea to make at least some use of the cash. My A/Cs were replaced recently I believe (although in humid TX they seem to blow up way too often!). And the roof was replaced when I bought it in 2015 so we should be good for a while there. Still, I agree that having an extra 6k isn’t a bad thing at all.

Sorry to hear about your tree issues! Pear trees are beautiful, but rotting is a silent expensive killer!

That’s great! Those are two big expenses you don’t have to worry too much about yet. I don’t know if you have the A/C unit cleaned/inspected once or twice a year, but that does go a long way in extended the life of the units. I’ve lived in south Florida and North Carolina, and the humidity causes those units to be run hard and often. It costs me about $89-$129. As for the Bradford Pears, it stinks to not have trees there right now, but I’m looking on the bright side. The tree type has shown invasive qualities in NC and is now on the Do Not Plant List for the city, county, and I think the state. It’s a grafted tree that rots and splits really easily, and breeds with other species to produce even weaker trees in the wild. Now I will have the chance to plant trees that are either more native or have a stronger wildlife benefit.

I’m following this with great interest. My rental property is paid for and I am sitting on almost $25,000 in cash. My original thoughts were to purchase another property but I am approaching retirement and don’t want another property unless it is paid for and that’s obviously not enough to purchase anything. Housing prices have sky rocketed and I would make a tidy sum by selling but not quite ready to do that either. I have a property manager so that is an expense I could eliminate but I’m not particularly handy and I work a full time job so it seems to be a justified expense. There is a lot to think about. Including taxes. Investing the cash would seem to complicate the tax picture.

Hi Shay! No harm sitting on cash right now and letting it build. You gotta do what’s best for your situation and comfort level!

Most people actually don’t think about disasters that could happen in real estate. Not having enough emergency cash to float you in case of vacancies is a surefire way to get evicted.

You have to know what you’re doing in real estate otherwise you will get crushed!

My old job used to be in contingency planning for businesses. It’s amazing how many people float along with no back-up plans or safety nets.

Yeah, I see no reason to NOT be overly conservative with an emergency fund in this case. If/when an emergency hits you may not even need to add any funds to it.

When running our biz, we always had enough cash in hand to make it through any issue. I think the pandemic shows just how quickly things could turn south with things you’d never expect to occur.

Definitely the pandemic has taught us all a lot about planning for unexpected emergencies. (it’s also surprising how quickly people forget afterwards haha!)

What a great post! Unfortunately doing this math I quickly realized I only had ~2 months in my reserves because I keep the bulk of my cash in personal savings. A few quick transfers and I’m all set!

Also, this is a good idea to transfer the money now as I just found out some tenants are not renewing their least effective July. Might as well earmark the funds now to fix things/touch up/plan for a month or two of vacancies, etc.

Nice way to plan ahead. I guess if the cash is all in your personal emergency fund bucket it’s no big deal if you have enough. The trouble comes when you accidentally spend that money (or invest it) then have an emergency at the rental simultaneously. That’s why I like separate buckets. Easier for my puny brain to visualize :)

Cheers Mandy! Good luck with your tenant replacement in July!