This article is about The Great Wealth Transfer. But before we get to that, a quick hypothetical question to help me explain why this is so important …

What would happen if you took all the money in the world and split it up evenly across all the people in the world?

Let’s say there’s $360 trillion in ‘wealth’ floating around the world right now, and we divided it up equally between the world’s 7.8 billion people…

Each person would get about $46,000.

Forget for a second whether this is fair or if the numbers are correct… This is just a fake scenario to get you thinking about what would happen afterward.

How long would the equal transfer of money last? If this happened tomorrow, how would people spend their money? Would it be invested? Or would people blow their $46k on consumer crap and lifestyle upgrades? Maybe a bit of both?

Experts believe that within 5 years, all of the world’s money would end up right back in roughly the same hands that it is in today. It’s crazy to think that a massive global event like this would be so short-lived!

It’s because the way people manage wealth strongly depends on their financial education and money habits. People with high financial IQ tend to build and maintain wealth easily. Whereas people with bad money habits or little money knowledge find it hard to hold onto wealth. This is also why most lottery winners go broke quickly.

Of course all of this is a hypothetical scenario, because a global money division will never happen in real life.

But, do you know which large-scale money transfer event will happen in real life…?

In fact, it’s happening right now…

The Great Wealth Transfer

Over the next 20 years, the most prosperous generation that has ever lived (Baby Boomers) will be passing down $68 trillion in wealth to their heirs. The recipients are Gen Xers and Millennials.

The reason this is more significant than previous wealth transfers in history is because:

- Baby Boomers represent a huge percent of the population

- Their ownership percentage of current wealth is ridiculous

- The money habits of the younger generation are grossly different

Here are some stats around the great wealth transfer that will blow yo’ mind 🤯:

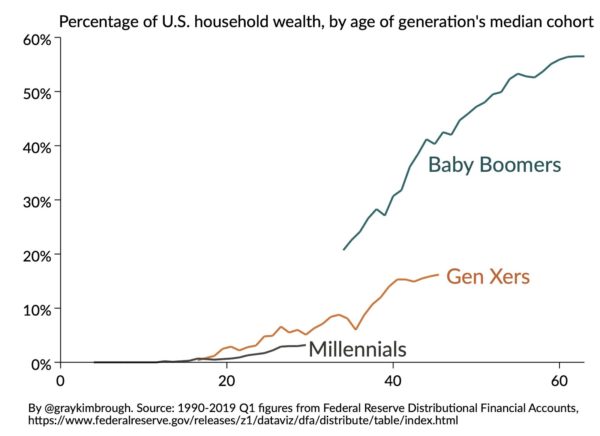

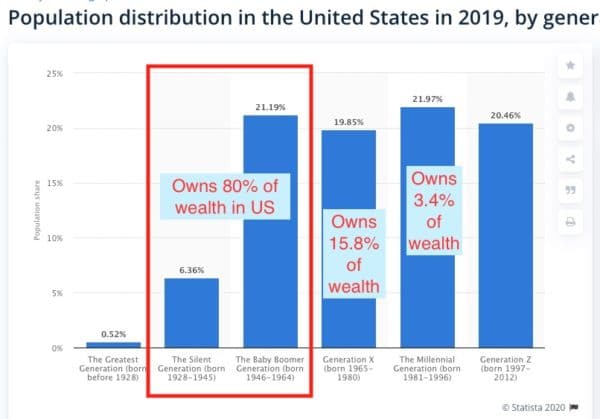

The Baby Boomer generation currently owns more than 56% of the wealth in the U.S. And their parents own 24% of the U.S. wealth. This totals a whopping 80%!

Gen Xers own 15.8% and the Millennial group only holds 3.4% of total U.S. wealth.

The chart below shows our current population split by generation. And it’s projected that in 2029 (when the last baby boomer turns 65), boomers will still represent 17% of the population.

It’s estimated that women will inherit 70% of the Great Wealth Transfer, according to Boston College’s Center on Wealth and Philanthropy. And by the year 2030, women will control 2/3rds of the nation’s wealth.

Studies suggest that 80% or more of heirs will look for a new financial advisor or wealth manager after inheriting their parents’ wealth.

70% of wealthy families lose their wealth by the second generation, and a stunning 90% by the third, according to the Williams Group wealth consultancy.

*All the sources I used for these stats are linked at the bottom of this article, along with other interesting articles about generational wealth.

So What Does This Wealth Transfer Mean?

First, it’s important to note that this “great transfer” is more like a “slow trickle.” The shift of wealth will be rapid, but not sudden. We all have time to prepare and adapt as things change around us over the next 20 to 30 years.

Also, recognize that assumptions and predictions around this event are very generalized. We can’t predict exactly what will happen because the world hasn’t experienced something like this before. And each individual country, business, and person is affected differently when money changes hands.

One thing’s for sure though… Just like in the hypothetical example at the beginning of this article, financial education will be one of the biggest deciding factor of whether wealth grows or shrinks within your household.

It Not Just For Extremely Wealthy Families

Many of you might be thinking, “Hang on a sec… My parents don’t have much money, so I’m not expecting an inheritance. Why should I care about all this anyway?”

Well, think beyond the direct transfer for a moment. When money rains down on people, in general, it only sticks around as long as the recipients know how to keep it. Sadly, there are millions of Gen Xers and Millennials who have poor financial education. Over time, wealth will flee from their accounts if they are not prepared or taught responsibility.

When money evaporates due to bad financial habits, do you know where the money goes? It goes to business owners, shareholders, investors, savers, hoarders, side hustlers, net worth trackers, FIRE walkers, and the sexy readers of this blog. Money is attracted to people with good financial education and habits. You will indirectly benefit from more money changing hands and as the economy is redesigned to support aging boomers.

Financial Planning for the Next Few Decades

These tips are useful if you’ll be giving or receiving wealth directly, but they are also just good general advice all around!

Talk about money more often! Financial conversations with family members can be awkward, ugly, and sometimes lead to fights. But, the more that money is discussed and problems are addressed early, the higher the likelihood of a family succession plan working out well. Remember, when talking to people from different generations about money, go in with a complete open mind. We all hold different values and motives around money.

Keep increasing your financial education! There’s always something new to learn. If you are confused or need help with wealth management, there are professionals and advisers in every single industry that can help you with hard financial planning decisions. If you’re already very financially literate, help educate others out there!

Consider charitable giving and directing money to services that are needed in the world. Many people inherit more money than they need, and some accumulate more than their heirs need to inherit. Take some notes from this guy, who built a fortune and donated it all anonymously.  Even if you can’t afford significant sums, any giving is good giving!

Even if you can’t afford significant sums, any giving is good giving!

Estate planning and tax planning. Uncle Sam is rubbing his hands together just waiting for the wealthiest generation to make mistakes in the wealth transfer process. Inheritors usually find out too late that they pay major estate taxes on family wealth … and that much of it could have been avoided if proper planning had been done earlier!

Consider the “burden” of some assets. Some wealthy people are asset rich but cash-flow poor. If they hand down complex assets (for example, a large real estate portfolio or a unique business that requires constant upkeep), there’s a chance the offspring or loved ones can’t handle the maintenance or annual expenses. Think about simplifying wealth before transferring family assets. This goes hand in hand with planning ahead of time and educating younger investors!

I’m curious to hear your thoughts. Got any predictions on how this will impact our lives over the next few decades?

Reference articles for this post:

All of the world’s wealth in 1 visualization (2020)

Wealth percent by generation, (Interesting data since 1989!)

US Generational Wealth Trends (Deloitte study from 2015)

Considerations for Women In Wealth Transfer

70% of rich families lose wealth by 2nd generation

What the Great Wealth Transfer means for the Economy

2018 US Trust Insights on Wealth and Worth

Staggering Millenial Wealth Deficit

What the Wealth Transfer Means for Advisors

Get blog posts automatically emailed to you!

The great wealth transfer will make a huge impact. You touch on business being handed down a little bit but I see more and more businesses that will unfortunately, fail. Owners think there children may be ready but like money habits they may not have taught them how to run the business either. Not only that, they may not have the exact same interest as their parents. There are many reasons the business could fail.

There will be unfortunate scenarios where the wealth transfer will be sudden to due an illness or like. Therefore, more businesses should focus on the premortem. So they better know what to do when uncertainty strikes.

The wealth transfer has began and will continue and the best thing to do is to start to plan for it now as who knows what will happen.

There’s a flip side to this, too. Some younger folks who get old business models handed down to them find more efficient and new age ways of running them. Millennials are crafty buggers – sometimes handing them stuff they know nothing about can lead to insights that past generations have never thought of. Definitely still comes down to entrepreneurial spirit and education, though. That’s needed regardless :)

“70% of wealthy families lose their wealth by the second generation, and a stunning 90% by the third, according to the Williams Group wealth consultancy.”

Hmm. I’m not sure I trust a wealth consultancy to give me unbiased facts about how people handle inherited wealth. Don’t they have a vested interest in making people feel incompetent to build up the market for their services?

Great point. Every stat should be taken with a grain of salt. Wealth consultants and advisors are going to have the toughest time with this transfer, as their management fees dwindle away and they might struggle to sell their value to younger generations. Their market is mostly likely shrinking. Whilst I don’t think they’re making up lies, they definitely could twist statistics to exaggerate the need for their services. Only time will tell truly where the money flows.

This statistic also feels to me like a quite questionable one. From what I could observe around me, the pattern was more as follow: rich kids go into excellent schools. When they graduate, they get a very good placement through connections or through the school. Thanks to their good placement, they can earn a very high wage and end up contributing to the family wealth. Now, as you mentioned, it may be that some of them earn a very high wage, but fail to contribute to the family wealth as they fail to manage their money wisely and are just spending all of it.

To come back to the wealth consultants and advisors subject, I think you’re entirely right when you mentioned that they will see their market shrinking. With robot-advisors and all the new online investment/saving services, they will be less and less needed. Moreover, the coming generations (Millennials and Zoomers especially) are more willing to try new products/services and are getting better along with technologies leaving even fewer chances to wealth consultants and advisors.

Overall, thank you for your article. It mentions interesting points to reflect on.

Thanks Emma! Yep, technology has a massive impact on how we manage things now. There are more DIY tools than ever.

It’s already happened in our family, my parents handed me a million when they passed. But it had no impact on my life, my wife and I were already self made millionaires. We just added it to our portfolio. Our kids will do the same some day. We taught them about money, just like our parents taught us. I can’t imagine anyone with wealth raising kids that won’t be responsible with money, but your data shows that’s common. Leaving ignorant and undisciplined kids a ton of money is a curse, not a blessing. Our kids will be fine.

The Millionaire Next Door was one of the most eye opening books for me. You’d be surprised about how many wealthy people try to give their kids a ‘better life’ by showering them with gifts/advantages and making sure they never have to think about money. This eventually backfires and it accidentally leaves the kids grossly unprepared later in life. I see a lot of this in Los Angeles.

So glad you’re teaching your kids the right way, Steve, just like your parents before you!

Excellent article! Now is the perfect time to contact a trusted estate planning attorney to make the transfer of wealth easy & find out options to preserve as much of the wealth as possible, i.e. keep Uncle Sam’s grubby paws off the money!

Yep, I’m always amazed at how many tricks and loopholes estate planners know about. There are also a bunch of free blogs, podcasts, and books out there that are great introductions for peeps who might not be ready to talk to professional just yet. Cheers, Kathy! Have a great week!

My wife and I are currently trying to figure this out on a smaller scale: each year we’re maxing out our 401(k) plans and invested HSA, our sole debt is a 2.6% 15-year mortgage with ten years left, and we’ve just topped off our liquid savings account to the tune of one year’s bare bones expenses.

So where does the excess go now? I’d love to feed our brokerage account four figures of VTI each paycheck, while she’s more interested in donating toward causes we support (and for the 29 days I am in 100% agreement). Her family background is parents with terminal degrees who commanded high salaries and bought whatever they wanted; mine was a federal employee dad and stay-at-home mom, and times were occasionally a little tight. She doesn’t like talking about money. It’ll be a series of interesting conversations.

Hey Adam. My wife and I also came from different money backgrounds. All I can say is it takes a long while to get the conversations going and get on the same page about stuff. My wife also doesn’t like talking about “money”… But she loves talking about “life goals”, “giving”, “designing our future”, “having freedom”, and stuff like that. It actually the same topic, just worded differently than talking about “money”.

As for the excess income… personally, I’d stuff as much into your after-tax brokerage account as possible!! Another thing you could do is set up a charitable giving brokerage account. You can invest the money and let it grow while deciding later how you want to give it away.

Hear, hear! When I stopped talking about buzzwordy “financial independence” and instead started trying to get her onboard with “hey, you know that 2018 vacation in Berlin? what if we could live like that ALL THE TIME” it worked a lot better. ;)

Yes – that’s awesome!

Fantastic article. I think as my generation get closer to inheritance we have to unfortunately think about these things more and more, but I agree that the more conversations you have the better we all will be.

The question now is HOW do we do it? How do we transfer the wealth from one generation to the next without loosing everything the previous generation has worked so hard for?! Next article?!

Thanks Mel! More to come on all this. I’m no estate planning expert but I love finding good ideas and will share when I’ve got them! Cheers, and have a great week!

I have to say that this article feels like it misses a level of analysis using wealth inequality as a lens. You write that the way people manage wealth is based on financial education, but I actually think the way people manage wealth is dependent on how much wealth they have to begin with. Low-income people are actually really knowledgeable about budgeting and where their money goes — because they have to be or they can’t survive. When I made below poverty line wages, I took in so much financial education, but it didn’t matter because I still had no money to begin with. I interpret the charts about who owns the most financial wealth in the country very different than you do; instead of thinking about wealth transfers from inheritances, I’m thinking why is our economy functioning so poorly that younger generations haven’t been able to accumulate wealth to begin with? Millennials are the largest generation in the work force right now, so it’s not that everyone is a irresponsible college kid.

The mantra “money is attracted to people with good financial habits” is pretty insulting to everyone making minimum wage and scraping by in unprecedented economic turmoil. This may get you more readers, but it’s just wrong.

Thanks Lindsay! Yes, many of the systems that gave Boomers a big financial advantage have been dismantled, so the younger gens have it much tougher. I’ll agree that education alone doesn’t build wealth – there are many factors to an individual’s financial situation. My oversimplification wasn’t intended to belittle anyone. Thanks for reading!

I’d like to respond to your statement “why is our economy functioning so poorly that younger generations haven’t been able to accumulate wealth to begin with?” with one huge factor: time! The elderly have more wealth because they’ve had the time for their investments to grow. If I didn’t invest another penny and got average returns until I’m 70, I’d be a multi-millionaire. However, my investments don’t look very impressive yet because I’m 39 and have only been serious about investing for the last 5 years or so. A better comparison would be to look at the average wealth of a boomer at a similar point in time as we’re at with millennials right now. I’m not sure how that comparison would look.

That said, there are certainly hurdles to accumulating wealth for younger people that didn’t exist 30-50 years ago. Education and housing are much more expensive for one. But we also have some advantages. I can invest for literally 0% in fees. 40 years ago I’d be shocked if they could invest for less than 1% and probably much more than that.

Hi Lindsay,

Thank you for saying this – I agree. It’s not just lack of financial education that keeps people from building wealth. Did you know that black families pay 13% more in property taxes than white families in the same situation? https://www.washingtonpost.com/business/2020/07/02/black-property-tax/

This is just one example of the institutional and structural issues that contribute to inequality in this country, and it’s nothing that more education will help.

I’m personally dealing with this right now. My Dad passed about a year and a half ago leaving me with a million + in assets. I sold his house but have yet to invest most of that money, plus the 700k or so he has with two brokerages/a financial planner, which I know must currently have a less than ideal expense ratio on those assets.

I’ve been going nuts reading whatever I can google, but I just finished Collins’ “Simple Path to Wealth” and I think I’m just going to go with his advice and transfer most of it to Vanguard, which most of our investments are with anyway, and invest it in VTSAX and forget about it. I’ve been trying to make it more complicated than it needs to be because of the fear I’ll invest 100s of thousands and the market will tank the next month or that I need to diversify into real estate or whatever the flavor of the day is in my mind. What I really need to understand is taxes, not how to invest (and yes, we are maxing the 401k, HSAs and IRAs, although I’ve been doing Roth and am now thinking traditional for next year because our marginal tax rate is 22%. I’m still learning).

But now I need to figure out how to actually, physically do it? I’m thinking since I’ll be transferring to Vanguard, I’ll call them and ask them how to do it and what the tax complications might be? Wish me luck and I appreciate any advice. I know just enough to know I don’t know it all.

Hey Sara,

I’m so sorry for your loss. That’s a massive responsibility handed down to you. There’s no harm in consolidating all the brokerage accounts to 1 single broker. You can do this all without even selling any stock positions. Most brokerages call it an “in-kind transfer”. Just call Vanguard and they’ll walk you through it. Many brokers are old-school, so don’t be surprised if they make you print, sign, and mail in forms (and scans of your ID) to get it all done. The transfer can take a while because they need to shift all the history and records from 1 broker to the next. Be patient, there’s no rush!

Once all the accounts are within 1 view, it will be easier to figure out allocation and all that stuff going forward. It mostly depends on your long term goals with the funds. Personally, I like your strategy of keeping things simple and following Godfather J. Collins. :) Keeping it simple lets you focus on LIFE, vs. worrying about whether your stuff is in the most efficient vehicle, etc. This is why I’m selling all my real estate over time and moving everything into VTSAX for the long run.

One last recommendation… Maybe you could find someone in the FI space who has gone through the same type of thing and pick their brain? Steveark (commented also on this thread) had a similar inheritance – he runs a blog too so maybe reach out to him or someone like that to just chat and talk it through? Just a suggestion :)

Good luck and thanks for sharing!

Joel

Thanks! This is so helpful, really! It’s not something I can really talk to friends about, and if I do they are as clueless as I am.

I wanted to start off my expressing my condolences for your loss. Nothing can replace the loss of a parent. Vanguard customer service reps are great, but their knowledge of tax laws around inherited assets at both the state and federal level will be quite limited. I would still highly suggest talking to a local tax accountant who deals with estates. There are some very specific rules over how different assets are valued at the time of inheritance (known as “basis”). In the example of stock, I believe your basis would be determined on the date of inheritance regardless of whether the values have gained or lost value since purchase. But it can also get more complicated than this with other types of assets (real estate, businesses, etc). Your inherited basis isn’t always determined at the date of inheritance. For example, when I quickly looked this topic up to refresh my memory I came across an exception where the executor of an estate can set the date of inheritance 6mos after the owner passed away. Depending on the timing, you could actually shield more of those inherited funds from taxation because you might have a higher inherited basis. Best of luck with this process.

Thank you. I will follow this advice. I really appreciate it.

Thanks for the information share. I remember telling people this was coming years ago and the called me crazy. And now it has begun. It was written.

One of the reasons it might not be discussed much is because it’a s sore subject. Inheritance, giving money, aging and dying family members… I can understand why many people would rather ignore what’s going on. I’ll be covering more on this topic over the years – it’s going to be very relevant. :)

Joel,

Another fantastic blog post. I’ve read about the Great Wealth Transfer as well – and that quite honestly not that many heirs are ready to receive their future inheritances. That’s why I think financial planning – especially as it relates to preparing your heirs – is extremely important to maintain assets within the family.

Most of the time, heirs do not know how to handle a rather large inheritance and they end up squandering that inheritance – and quite possibly being financially worse than they were before the inheritance.

Thanks for the post!

Cheers MMM! It’s a sad story sometimes. Just like lottery winners, it’s so tempting to spend the money quickly instead of invest it wisely. Glad you’re helping people out there educate themselves and prepare for future wealth. Cheers!

My wife and I were just talking about this the other day. We are likely (and hopefully) a couple decades away from getting any inheritance from our parents. But with both of us having siblings we were wondering how our parents are planning to pass down their properties in particular. Investments are easier to split that land or a house.

I also have a great-aunt with no children and I know I’m in her will. Probably looking to receive low 6 figures from her. I’ve always assumed I would take $5k and take a nice vacation and plop the rest into VTSAX or something similar.

It’s really hard to plan on what you’re going to do with an inheritance because there are no guarantee’s you’ll get it. Maybe they live a long time in assisted living and spend it all. Maybe they give it all to charity, or don’t include you in the will at all. It’s fun to think about sometimes, but I don’t want to make any plans since it’s not my money at this point.

Hey Nate, thanks for reading. It’s definitely a weird thing to think about. You’re right – anything can change, so it’s best never to “expect” something will be handed down to you. I love that you’ll probably take a small amount and use it to celebrate and commemorate your relative’s long life. Investing the majority is smart too. I think that’s something they’d really appreciate.

All in all the best way to prepare is to keep striving for FI yourself. Focus on your own path and figure out windfalls if and when they come :)

Awesome article! I assume the inheritance will happen during the 40’s, 50’s, and 60’s of recipients’ lives.

I think it’s interesting that in this model people generally inherit money after the time we could use it most. For those of us that have kids in our 20’s or 30’s, or look to buy a house during those years, or pay off college debt, a wisely deployed inheritance at this time could help a lot! By the time you’ve reached your late 40’s, 50’s or 60’s, presumably your career is well underway (or winding down) and you’re more likely to downsize your house than upsize.

Personally I hope I can transfer my wealth to my kids much earlier than my old age, so that with the appropriate education they can live full lives when they are young, instead of struggling and then receiving a lump sum once they’ve already settled.

Thanks Mike! One cool thing I’ve been researching lately is there are also many tax breaks and opportunities to pass down wealth to Grandkids, not just immediate children. So instead of Boomers passing down to kids heirs their 50’s and 60’s who might already be financially secure, they could skip a generation and help the next ones down.

I like your plan to transferring wealth while you’re alive. There’s an old saying… Do your givin’ while you’re livin… So you’ll be knowin’ where it’s a goin’!

Wow, really interesting read. I knew the older generations had a disproportionate amount of wealth, that’s somewhat natural given accumulation, career building, etc. However, 80% was a shocking figure! Given the size of the millennial generation, that sub 5 percentage is pretty astonishing. I guess that changes pretty quickly when the inheritance starts tricking down though. My wife will likely inherit some from her family, but we’ve made sure our finances are already in order so aren’t counting on it!

Cheers Ed. I think it’s great that even if you might get an inheritance, making sure you already build your own wealth and foundation is important. And, hopefully your in-laws and relatives live as long as possible and you won’t need to worry about that stuff!

This is really a good article. Thank you so much, sir.

A year and a half after this article was published and I think that we the shrinking of the middle class..