Happppppppy New Year, everyone! Can you believe it’s already JANUARY??? Of 2016??? Wow. I remember when we were going into 2000 and everyone was freaking out about technology exploding all over the place – hah. Good thing the internet is still here :)

Well, we didn’t reach our glorious goal of becoming a half-millionaire this year, but we did end up roughly $20k higher than we were at this time last year, so it’s hard to complain all too much. Still, to make myself feel better I went back further through the 8 years of tracking this stuff to see how even farther we’ve come. A big perk to being a numbers nerd :)

Check it out:

- January, 2015: $469,631.26

- January, 2014: $443,561.57

- January, 2013: $332,608.93

- January, 2012: $285,368.44

- January, 2011: $208,485.96

- January, 2010: $143,817.65

- January, 2009: $64,189.42

- January, 2008: $58,769.65

In the 8 years since paying attention to this stuff, we’ve grown our net worth from $50,000 to almost $500,000 – an increase of around $450,000. Not too shabby at all. And a MUCH more exciting story than a $20,000 bump!

So while we missed the mark of crossing into the $500k’s, as well as hitting our $50,000 yearly growth average for the second time in a row, at least we’re on the up and up and can try harder in the new year. I won’t make excuses for why we didn’t hit it, but needless to say we have some work to do.

(Okay, hell, yes I will :) In the past few years our household went down to 1 income, we converted our house to a rental property which sucked up a bunch of cash, I re-focused my business on stuff I’m passionate about vs stuff just for money, and we *ahem* had kids. All stuff we consciously decided to do, but still financially-wise stung.)

So for 2016 it’s all about hitting $500k, and hopefully by the end of it around $550k. But I’ve long since given up money as the #1 priority in my life, so if we get there we get there and if we don’t we don’t. True happiness, I’m finding, is in enjoying your daily lifestyle more so than the # of zeros in your account. Though of course I’m still gonna chase that ultimate freedom ;)

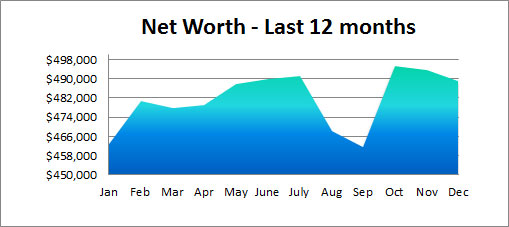

Here’s how the entire year panned out from start to finish:

Hopefully you’re tracking yours too so you can easily review as well! This is seriously one of the best perks to tracking your net worth consistently – getting the snapshots of your money frozen in time. It’s a powerful thing to be able to look back and see how far you’ve come. I really hope you try it out if you aren’t already (tools to help you do this are down at the end of this post if you need some).

Here’s how the month of December broke down:

(PS: To all new readers here, I share our entire finances at the end of every month in hopes it makes talking about money easier for people. It’s not about showing off or patting myself on the back – there was a time I had barely $50 to my name! – but more so showing what happens when you actually care enough to make some changes in your life. And hopefully this inspires you to do the same!)

CASH SAVINGS (+$3,146.02): This is a temporary bump due to a better than expected month of business, but a great sight to see no less and helps recoup some of the $$ we’ve poured into our house to get it ready to sell. And more on that here in a bit (though, spoiler alert, it’s never fun paying for an empty house!).

DIGIT SAVINGS (+$392.59): In other savings news, Digit continues to not disappoint either. I haven’t lifted a finger since signing up last January, and our account is now well over the $2,500 mark!

CHALLENGE EVERYTHING (+$302.64): Another solid month here too, bringing our total (easy) savings to $1,200 after just four months. I haven’t listed a thing on Craigslist lately, but we continue to catch extra money coming in like this year’s USAA dividend check they send out to members, and a little Christmas cash too. We just keep stashing it away in hopes of maxing out another ROTH Ira this year like we did last year when finishing up the first round of this challenge.

ACORNS (BROKERAGE) (+$9.25): A nice little increase here too. All money being invested from rounding up our daily transactions via Acorns. If you’re looking for an easy – and non scary – way to start investing, this could be a possible route.

MOTIF (BROKERAGE) (-$10.03): This will be the last time you see these guys here as I just cashed out our holdings and will be forwarding over the money into our Vanguard account shortly. This comes after a 12 month test of seeing if it helps me get excited about dividend investing (it didn’t), as well as playing in a friendly blogger competition of picking the best stocks for a year :) Hint: I lost. You can see the full review of Motif I wrote as they are a clever way to invest, but it just reinforces my strategy of keeping things simple and being “all in” with index funds. Plus, the game of investing is all for the long haul anyways, not short, so the whole competition was pretty silly from the start.

IRA: ROTH(s) (-$1,766.27): Nothing too snazzy going on in this department. Just the markets doing what they do, while it waits for us to invest again… We’ll probably max this out in one fell swoop come March or early April after taxes get sorted through.

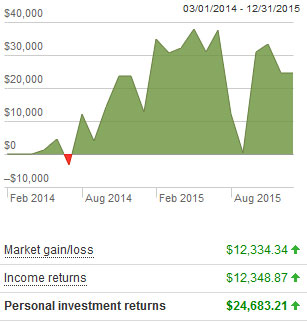

IRA: SEP (-$7,239.64): Same with this guy. As soon as we wrap up the tax year and see how much we can invest (it’s tied to company profits for the year) we’ll go in and fill ‘er back up again. Here’s a snapshot in the meantime of how our funds have performed since moving to Vanguard over a year ago:

AUTOS WORTH (kbb) (-$8.00): Nothing too exciting going on here. Just the cars doing what they’re supposed to be doing and losing value as the months progress… I did get a little scared when my Caddy didn’t start up again the other week, but it seems it just needs some extra TLC during the colder days and then purrs just fine. Every month we still have her is another month without car payments! :)

Here’s how their values break down:

- Plain Jane Toyota: $4,368.00

- Frankencaddy: $1,000.00

HOME VALUE (Realtor) ($0.00): Okay, well I don’t want to jinx anything here, but fingers crossed talks on selling our house continue to go well and we have some good news to report soon!! Until then, I continue to keep my mouth shut and will take all the positive vibes you can pass over, paleeease. This is the biggest move we’ve made in a while and we’re incredibly hopeful! We’ll leave the value of our house @$300,000 until anything’s official, but as we all know the only true value of property is the amount someone will pay you for it ;) All the calculators and home sites can only give you an estimate.

MORTGAGES (-$716.45): In the meantime, we just keep paying off our mortgages as if nothing’s going on to avoid any ugly surprises down the road… Always better to be safe than sorry with these things as nothing’s locked in until it’s locked in. Here’s what’s left on our two mortgages:

- 1st Mortgage: $262,180.76 (30 year conventional @ 5.5%)

- 2nd Mortgage: $25,283.98 (HELOC @ variable 2.8%)

And here’s what our entire journey looks like so far! 96 months of tracking!

Pretty cool to watch…

Pretty cool to watch…

Here’s the journey of our two little boys too :) (We actually deposited $100 more into each of their 529 accounts this month, but sadly the markets were quick to eat them up)

And that’s 2015! How’d you guys do?? What are your financial goals for the new year?

Again, none of this matters except to ourselves (most people don’t spill their numbers to the world), but I find the more people talk about this stuff the more we can learn ourselves. So I sincerely hope this helps start some discussions :) And you don’t have to track your worth every single month either if it’s too scary/annoying for you – try quarterly or bi-yearly or even just once a year. As long as you have a good understanding of where you sit at any point in time you’ll be on the right track.

You can also check out our list of 180+ other bloggers who share their net worth. Maybe they’ll inspire you/give you some good ideas to work off?

To a prosperous 2016!!!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

I noticed you said you will max out savings in one fell swoop. Is that one fell swoop of cash in followed by dollar cost averaging in or do you dump thank investment into your investment vehicle of choices in a one fell swoop? When making a “big investment” typical advice is to “dollar cost average” in. Have you considered slightly altering your investment strategy in that front to work your savings in gradually and avoid any sudden market fluctuations (see Aug 2015)?

Yup, def. a better idea/strategy for sure. I used to dollar cost average when I was working a 9-5 with more predictable income, but since going self-employed I like to wait until the end of each year to make sure I know what I’m dealing with. Some months can literally swing from $20,000 to $2,000 in income, so I take the 2nd best option of investing it all at once every year even if it’s not the most efficient way. I’d love to get back to it at some point though :)

The truth is, J is dollar-cost averaging. He’s just doing it less frequently (yearly as opposed to monthly) than most people do. ;-)

Hah! I like the way you think :)

I must have missed it… You are higher than 20k compared to this time last year…. More like 44k right?

Duh. Never mind

A lot of positives to finish out the year, now we just need the market to settle in for the winter. :) That’s a pretty good seven year swing, dumping the mortgage will give you a big boost as well.

It’ll actually drop our net worth in the beginning, once all the realtor fees and what not get accounted for, but yes – over the long run that extra cash flow will help immensely :)

I love that you’ve brought a voice of focusing on more than money to the personal finance world. And that your net worth has still increased, despite not being solely honed in on money. I wonder what your net worth might have been at this point had you continued on your original trajectory and not started challenging everything? Also, I’m looking forward to your house news.

It would be at LEAST $10,000 or so less. Just by taking out all those savings and factoring in my new mindset :)

Sometimes I think about the opposite – what our net worth would be if all I did was focus on $$$! Haha…. I guarantee I’d be a millionaire by now as I turn down a lot of opportunities and ways to make $$ since it doesn’t fit with my goals/lifestyle. And I would never have had kids either which just breaks my heart to think about!!

So I’m glad I chose the “life” path over money :) Even if I dream about having more – hah.

I think you need to change your name to J. Life now! haha j/k. Nah but keep it up man, life is definitely about balance too. Yin/Yang.

Fun fact: when I first started this blog I used to go under “J. Savings.”

Great news …hopefully….on the house sale. I’m with you on not “jinxing….”mums the word”….until the check clears. MAN…if that goes thru what a load off!…Might want to fund your IRA’s early as the market appears to be getting ready to take a “hit”….and your investment would/could buy more shares.

As soon as I get all our taxes stuff done the IRA maxing will hopefully soon follow :) I’ve been tracking stuff a lot better this year than in past, so so far I’m loving the idea of sitting down and getting all our records ready for our accountant! And even more so that we have an accountant to do it all in the first place! haha… I don’t dare pretend I could do it better ;)

For 2015 our net worth was up by $25,662.30 for a family of 4 living on one salary of $59k. I love tracking my net worth but think that I might be a bit obsessed with it since for the last 18 months I’ve tracked it first thing every morning when I get to work. And I’ve tracked it on a spreadsheet where I keep all of our financial information every two weeks since 2011. I love having the historical snapshots to look back at and see laid out on a graph.

Holy crap! That is awesome! On BOTH counts, haha… At least since you do it at work it’s not really on your “own” time – hah. So impressive you’ve basically saved HALF your income with such a large family and on $60k. You’re def. beating me in that department as we’d have banked $60k’ish if we were following suit, d’oh.

Thanks for the encouragement J. Feeling better about myself after reading your response!

Awesome! Going up is always good. :) Net worth, we were over 50k this year.

Over at my eBay blog (FlippingADollar.com), I was also short of my goal of 10k in profits. I had 6.7k which is still pretty awesome. I’m going to aim for 10k in profits and 20k in sales for 2016. Speaking of, I have to go downstairs to ship some stuff out now!

Work it! Killin’ it in both departs, congrats sir.

Great job on the net worth growth. I noticed most of your net worth is in 401k instruments. If you retire early, you will need a good portion in non-tax deferred accounts (non-401k mutual funds) because you can’t withdraw any of your 401k until 59.5. Are you structuring this way on purpose?

Good eyes over there :)

The truth of the matter is that I’ve never sat down to really strategize on it all yet. I’ve been maxing out my IRA every year which is something, but you’re right – there will be no retiring early anytime soon without a re-structuring/new funneling of money. Half of me likes not being able to touch any of it, and the other half (ie the early retirement half) does not.

So pretty much all that to say I have some work to do if I’m serious about really cutting the cord and can’t just “go with the flow” anymore. In other words, I suck at planning for the future :)

No worries on that end. if you use a 72(t) you can take equal distributions out of our IRA without penalty before 59 1/2. This is is a strategy I will be using myself in 5 years when I hit my number. The best thing you can do is work backwards. Have your yearly spending number and multiply that by 25. That’s your BINGO number. The number you have to hit to NEVER run out of money. Happy Saving!!!!

Love it! I keep hearing about the 72(t) strategy, just haven’t researched it myself. So awesome you’re gonna hit your number in 5 years – that’s great! Congrats!! I hope you’ll come back here and let us know once you do :)

You got it bro! The 72(t) strategy is a great one. It’s simple. Just take equal distributions from your accounts monthly and you’re all set. 5 years is the goal!!!!!

You can also do the Roth IRA conversion dance. Roll 401k to IRA, then convert to Roth annually in increments that minimize taxable income. Details over at gocurrycracker or mad fientist. It’s possible to retire early, live off tax-deffered money and never pay taxes or fees.

I like it! I’ve read some of those posts by Mad Fientist and the gang… so clever those guys!

Solid year! We didn’t creep up too much net worth-wise in 2015, but I did get my wife pregnant. So…maybe that counts for something.

Life: +1

Money: -1

Congrats! :)

Awesome job, J$ – and that was one truly spectacular recovery you made this year after the “mini-crash” that happened back in September. Sadly, our capital gains growth was down by about a percent this year (thanks to September), but like you, we saw a nice net worth increase primarily due to our contributions.

And that just goes to show – contributions matter!

J. Money it is good to see you doing so well. You are an inspiration to all us who aspire to better our lives.

I am still thinking about opening a digit account. I have heard good things from you and some others.

I wish you much success this year and keep on inspiring us;

Let me know what you think if you give them a shot!

Nice seeing you here every day chiming in btw – appreciate it :)

ITs good to see the transition over the years and how close you came to reaching 500K. I predict the journey to reach 1 mill will be faster now that you have a mountain of cash working hard for you. Good luck in 2016 and with getting your cash flow back with the sale of the house.

You know what they say – the first $500,000 is the hardest :)

Solid work J$! I love tracking our net worth for this exact reason- it is so inspiring to look back at how far we’ve come! Good luck on your goals in 2016!

I’ll be hoping the markets continue to dump for the next few months so that you can do all your investing at local lows. Who needs January-April to grow their net worth anyhow?

Congrats on being up on cash… That always feels nice.

This month we temporarily achieved our highest net worth ever (now all the money is in the markets, and as we both know Mr. Market will do as Mr. Market does).

Yeah! In fact, can the markets just stay low for a solid 20-30 years please? But not affect older people at all so no one gets screwed?? :)

Disappointed that you haven’t kicked ass at Challenge Everything 2.0… You’re living off the fumes of last year’s efforts. Go out there and kick some bills ass!!

Sorry, not much of a motivational talk, ha!

This is true, sir, I have been slacking indeed… However, at least my slacking in this department is being made up for in the business building department which in theory should provide much more benefit in future years. So I think I should only be getting half of a motivational talk :)

HNY J!

I do hope you achieve your $550K goal, unfortunately, I think it’s going to be one hell of an ASS KICKING in the stock market in 2016. The good times are over!

Gotta do some side hustling on overdrive instead to make some monay.

GL to us all!

S

Haha… you sound like every pundit any month or time of the year :)

Fortunately I don’t ever count on anything happening – good or bad – in the markets. I just keep doing my own thing and worry about what I have control over.

Amazing growth. Congratulations. It is inspiring to see some one’s progress through the years. With some determination and discipline everything is possible.

I made $77 for the month and $2,500 for the year. My goal for 2016 is to grow by $10,000.

The best to all of us.

Here is my report. http://www.alainguillot.com/net-worth-january-1st-2015-77/

4x growth – I like that goal!

Going over to check out your report now too… I eat this stuff up!

Congrats on a great 2015. Hopefully selling the house is a done deal! 2015 was great for me and my plans for 2016 include increasing income, lowering expenses, and investing the difference :)

Wow thats incredible how far you have come in such a short time! Theres nothing stopping you from achieving your goals! Congrats

You are doing well! I hope 2016 is even better.

2015 was a great year for us. I hope it continues like this for years to come so that we can retire early :)

Somehow I don’t worry about you two over there :)

Any plans to share your own net worths over time, or just keeping forward with the income reports? (Which are also sexy, of course)

I’m liking that trend since 2008. Up up and away!

Congrats, and hopefully you’ll see some serious NW snowballing once the equities markets ever take off again.

Up up and up! Gotta love the ever increasing net worth. Will be interesting to see what 2016 brings. With high savings rate and continue investing in the market, I’m sure we’ll be just fine. :)

Great job on increasing the net worth!

My husband was a bit freaked by my wish to reveal our debt numbers, and he is firmly against revealing positive numbers – savings and investments – online. He thinks it would make us vulnerable to hackers. In your experience, has that been the case. (I want to go to my husband and argue, “Well, J. Money says . . .”)

Hah! This is one of the reasons being more anonymous online helps :) I haven’t been targeted directly because of my net worth postings (at least that I know of?), but I have had my fair share of stalkers and psychos. Anytime you do anything good or share positive news about yourself it pisses some people off. Hell, anytime you post *anything* online it manages to offend someone! But my view is to just do your thing and carry on with whatever you’re comfortable with, and then let the chips fall where they fall. I get both hate mail and love mail every single day of the year :)

I’m sorry to hear you get any hate mail at all! It just means that you’re making a difference that the dark side isn’t comfortable with. Keep on making that difference!

Excellent point. That’s the only reason I don’t buy lottery tickets. It’s not that the odds are so crazy it’s like throwing the money away. It’s that my state has a rule that you can’t collect and remain anonymous. What good is $200M (net) if that puts your family at risk?

Yo yo mr. Money! I need help please! how do you calculate mortgage as part of your Net worth? you need to break it down for me please? I have 3 properties, one in which I stay and the other 2 I rent out. Do you add the amounts you paid off already and add that to net worth?

Thanks!

Hey man!

Everyone calculates this stuff different depending on your goals and what you’re trying to get out of your net worth, but technically it’s all your assets minus your liabilities. So the things that would go in the calculations are the values of all 3 of your homes (assets), and then the balances of all the mortgages still owed on them on the other side of the equation (liabilities). This gives you the overall financial snapshot, and any time you pay off more of your mortgage – or the home values go up – your total net worth will adjust accordingly.

The other variables like which house you live in or how much rent you make off them/etc don’t factor in here (at least with this method of tracking) and is more of a cash-flow thing than a net worth one.

Hope this helps!

2015 brought a lot of changes for us, but mostly I think it brought a value to time with my loved ones over earning the almighty buck. It’s great to see I’m not the only one.

Hi J!!!

Things are great! Digit has been a blessing and is what helped launch my financial goals in 2015. Remember those 2 nasty charged off credit cards?? Well I whipped them out and paid them off 2 months before planned. I got my Roth IRA set up to save automatically and I plan on paying the last of my debt off over the next 11 months. Since my goals are pretty much set up on auto at this point I plan to continue actively educating myself in all things finances and investing. And of course pushing forward with my fitness goals! =D. Hope you and your family are great! Thanks for everything!!

~Darlene

Yayyyyyyy!!

What a testament to prioritizing and CARING enough to make $hit happen!

So proud of you! Keep on going!!

Wow, lots of big accomplishments here. Very inspirational, and makes me realize how important tracking net worth is (note to self :)

I like what you said about realizing that your happiness isn’t based on the number of zeros, or something to that effect. Thanks for sharing the wisdom!

Great job J. Money on your accomplishment in such a short period of time. I have 5.5 years to go and then I shall be looking for another career/early retirement. At this point I am excited and look forward to a new phase in my life.

Take care my man.

That’s exciting! Will be nice to do things on your own terms, eh?

Yes sir it will be. Right now I am working no overtime and 4 days a week most weeks. Have my blog that’s growing slowly organically and my wife finishes RN school this year. Of course we have been living frugally, put in our time and hard work to get to this point but it was all worth it. We have been able to slow down a bit, enjoy life more and pursue what we love. We may not own the newest car or the best home on the block but we are content with our life style. We have less money stress and more options- financial independence is awesome! My only regret is I wish I had started my journey towards financial freedom much sooner.

Oh wow – you’re easing into the freedom nicely! That’s something I need to be better about here – cutting out the overtime/weekend work… I’ve been a lot better than previous years, but I have to constantly remind myself not to become a workaholic or what’s the point? I think the biggest problem I have is that I *enjoy* the “work” and anytime I think to myself – “what would you like to be doing right now?” in my spare time, I often dream up online projects to build haha… so I guess it’s both good and bad, but I def. want to have less computer face time :)

Anyways, congrats on the journey so far! Nice to take advantage and not make it an “all or nothing” type deal.

I was a bit confused on the value you used for the house, was it based on an appraisal or was it the cost you acquired it? Regardless, congratulations on increasing your net worth so much over such a little amount of time – very great feat.

Thanks man :)

The value listed in my net worth reports is the latest estimate that my realtor values it at. Every 6 months or so I ask him to look at comps and then update his best guess from there. I’ve tried using Zillow and the likes, but it fluctuates way too crazily and never seems to be accurate for my area. So the realtor route seems like the best option for us, and we’re cool with the less frequent updates. Hope this helps :)

I’m a newer reader. I found your blog on New Year’s Eve cause I know how to party. I’m interested in calculating my family’s net worth. Do you have a simple spreadsheet template for a newbie?

Hah! Welcome to the club :)

Sure, here’s a simple spreadsheet I put together when I used to do money coaching:

https://budgetsaresexy.com/files/Money-Snapshot.xlsx

also has a simple area to budget too if you want…

Thank you! I can’t wait to try it. If it ends up not fitting my needs, then at least I have something to work from. Thank you so much.

No problem!

There are other apps and services out there btw that track it automatically for you if that’s a route you’re interested in as well. Places like Mint.com or PersonalCapital.com are free. Here’s our review of Personal Capital: https://budgetsaresexy.com/go/personal-capital

Thanks! I actually recently read your review of PersonalCaptial.com and am considering it (or YNAB).