Well hello October!

What did you do with September, and can I have her back?

(I feel like September is a girl, yeah? And October a guy? Ever wonder such things? Or why a blog about money would even bring up such a thing when it clearly has nothing to do with finances? (Ever wonder why you continue to read this blog??))

So yeah – a new month, yay! Never will there be another October of 2016, nor will you be any younger :) On the plus side, all that hard work you’ve been doing should be paying off like gangbusters! Compounding is a mother, and in a perfect world each month should be trending up…

Unless you’re name is J. Money, who’s managed to still lose cash even though his wife got a new full-time job. I can assure you I have plenty of good excuses for this, but knowing 78% of you will just call me out on it, I’ll save us the trouble and admit I suck. Though trust me, if you thought my jokes about giving each month a sex were bad, you’d really have a field day with some of these ad deals I turned down! So really, I do it all for you… (you’re welcome).

On the positive side, we did activate a pretty cool new feature that the gov’t offers! It’s called Dependent Care FSA, part of the Federal Flexible Spending Account Program (FSAFEDS), and it allows you to siphon out money for daycare PRE-TAX, saving you a solid 30% or so depending on your tax situation. The max you can put in is only $5,000 per calendar year, but that alone saves you a couple of G’s so we jacked it up as high as we could and will then max it out at the beginning of 2017 as well… It’s a little disconcerting seeing your paycheck at only $650 when you make $53,000/year, but hey – it’s the mental price tag you pay to save thousands of dollars :)

If you’re a federal employee – and have daycare bills the size of your mortgage – look into it! (UPDATE: As many commenters have mentioned below, this dependent care FSA is actually open to others outside of the gov’t too! I’m not sure if all employers offer it or only some, but check with your HR and see if you’re interested :) Here’s a great article on it by Investopedia: The Benefits Of A Dependent Care Flexible Spending Account)

And now to the breakdown of how the entire month of September went down…

It’s pretty exciting. #NoItsNot

September’s Net Worth Changes:

CASH SAVINGS (-$1,393.76): Turned down business, didn’t find new business, took 2 year old to emergency room (he’s fine! just a lot of blood from an epic fall/lip biting!), and pretty much miscalculated quarterly taxes… See – no excuses :)

BROKERAGE (+$18.58): SWEET!! Time to retire y’all! (Or just keep doing a whole lot of nothing and letting Acorns round up all my purchases to invest in a separate investment portfolio for me… Up to $515 now in a year and a half.)

THRIFT SAVINGS PLAN (TSP) (+$414.30): This one actually IS exciting! More than double the amount in there from last month, and the wife keeps funneling it in! Sure it was only opened up last month, but hey – doubling your investments is doubling your investments :)

(She’s 100% in Lifecycle 2040 which aims to “achieve a high level of growth with a low emphasis on preservation of assets.” Not as aggressive as I personally like (the C and S stock indexes are my faves), but hey – it’s her money. And all the funds TSP offers are pretty damn good w/ low fees.)

ROTH IRAs (+$114.79): Over $100,000 invested and pretty much broke even! That’s hard to do!

SEP IRA (+$621.36): But do you know what’s even harder? Having $400,000 invested and breaking even :) Although not if all the $$ is pretty much in the exact same fund (VTSAX), haha… (the wife’s IRA money – $25k – is invested a bit differently, but still spread out enough that the flat markets kept it relatively flat as well).

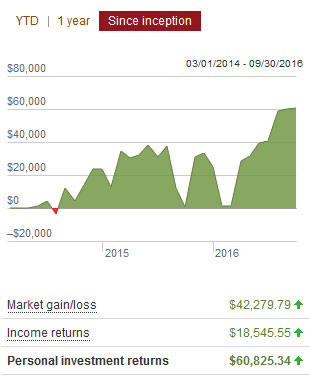

Here’s how these investments have fared over the past couple of years since moving to Vanguard:

(These are *returns* btw, not total amounts invested)

CAR VALUES (-$179.00): Nothing too amazing here! Cars doing what they’re supposed to do over the years… Even luxury cars :) Here are the KBB values on both of ours:

- Lexus: $13,985.00

- Toyota: $4,122.00

(Been four months now without FrankenCaddy, can you believe it??)

CAR LOAN: (-$207.47): I stopped rounding up the payments to $500 each month until I get my cash flow back under control… I tend to get stubborn with changing gears once I set my mind to things, but I’m trying to get smarter in my old age and understand that you have to change your strategy as life itself changes. Even if it feels weird!

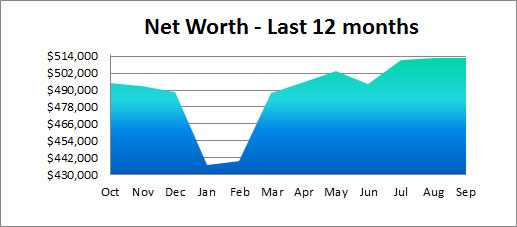

Here’s a look at how the entire last year has gone:

A pretty precipitous dip earlier in the year (we offloaded our house), but outside of that just gradually humming along… And same goes with our kids’ net worths too (you know we have to track that :)):

And that’s Miss September! (She’s totally single)

How did your month go? Are you ready for the pumpkins and leaves and cool crisp air? Are you ready to disclose your sexy numbers for all the world to see too?

Shaun from Road To A Tesla put out a call for everyone to do it on Facebook last month, and although I love the idea of complete transparency among communities, something tells me it’s much easier to do so around a group of like-minded people than your ex-lovers and classmates.

Though happy to watch you experiment? :)

As always, you can gawk at over 200 other bloggers’ net worths we feature on the Rockstar Finance Net Worth Tracker, or even take a trip back through time and scan 100 of my own previous reports listed here over the years…

No shortage of numbers around these parts!

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Glad to hear your 2 year old is ok! I bet that was scary.

Is the pre tax dependent care a government only program because I know we are allowed to take pretax money for daycare up to $5k too.

Thanks for the update J$, keep working hard. And glad you are looking out for us and turning down those sketchy ads! :)

I think you’re right!

Saw a bunch of other people commenting about it not being a gov’t only thing too, so googled and sure enough seems like it’s not restricted to just federal workers :)

Here’s a good post on it:

http://www.investopedia.com/articles/pf/09/dependent-care-fsa.asp

I’m not sure if it’s something ALL employers offer, or just some, but either way pretty cool it’s open to many people! (And just updated the article above – so big thanks everyone!)

We’ve had our share of trips to the ER, never fun. Glad your son is okay.

September always feels like a big transition month, back to school, weather begins to change, holidays loom. I’m looking forward to October.

Do you miss FrankenCaddy?

I do :(

I love the Lexus too – more every day, actually – but if I hadn’t needed to get rid of it I totally would still be rolling around in it… Just wish it was more safer/dependable for the kids! Gotta put them first, always.

Sorry to hear about the emergency, glad everything is okay though.

I see mostly all green numbers, except for the savings – which is fine in my book.

Nice job J, I bet your next month’s update is going to be a big one!

Tristan

Dependent care Fra is not government only. We have 1 as well. Applicable to day care if both parents work up to age 12. Also usable for other care expenses for a dependent to allow you to work, look for work, or go to school if you have a dependent. Tax free if used correctly but use it or lose it. We have use it the last 4 yrs but my wife is going stay at home so it’s something we are giving up.

I have been using a dependent care FSA for the last 4 years. Its awesome! The only part that stinks is, it isn’t enough to cover all my day care expenses and counts against your dependent care deduction on your taxes. But the tax savings is still much better than the pathetic dependent care deduction anyways.

Love to hear this guys! And that it’s open to more than just federal employees!

I was just looking into the FSA dependent care last week, child care costs are shocking but that will take a little off the top mentally. Between child care and health insurance one of our pay checks is going to drop significantly.

I am with ya on September being a girl

I know – kids are crazy expensive :(

Glad to hear your kid is ok! My 3 year old (just turned 3) has been to the ER more than my other 3 kids combined! Nice on the TSP! I split mine C, S, I – 40/40/20.

So scary, right???

We were about to head out to a party when it happened, and after we got him all glued up (apparently they use super glue instead of stitches with face cuts??) our boy still wanted to go to the event, haha… So we went! And he got mad attention :)

I should track my net worth. Before I stop your heart, let me clarify. We know what is in all of our accounts, and we do add them up at least quarterly. But right now, it is like someone is turning our savings account upside down with grad school tuition. My husband just finished his. I’m a few months into mine. And my husband is starting more classes. Maybe when the hemorrhaging stops. Right now, I think it would be too easy to get discouraged. And I get a little obsessive over numbers. Like that one time I checked my Vanguard account six times a day. Yeah…only one time ;)

Haha…

It’s all good :) You gotta do what you gotta do, and at least you know yourself well! As long as you have a pulse on it all you’ll be fine.. It’s not like you’re not a personal finance blogger or anything and won’t be holding yourself accountable :)

That’s great about the FSA Dependent Care Act. Child care can be outrageously expensive and it’s unfortunate how that can really hinder parents’ careers. I hope this helps a lot of people!

You could have been doing the dependent care thing all along. Its not just for federal workers… I am assuming you are set up as an S-corp, which you should be or you are paying more than your fair share in taxes. Part of the deal with that is you can give yourself dependent care reimbursement as a fringe benefit and not have to put it in a use or lose FSA. I pay for my sons pre-K like this, just write a check straight from my business account. I think I technically have to claim it as income but then its written off. Whatever it is the accountant pre approved it so I’m good. I get why you are doing it through your wife’s job though, with her job you don’t have the option of just leaving that money in a business account.

I had no idea until today that this even existed! I don’t have an S-Corp (though it’s been on my list forever to look into) but very cool to see how you’re using it. Amazing what you can learn (or not even know about??) until you put it out there. So thanks, man.

Your accountant should have suggested it. I would seriously think about hiring a different one if they did not. Some are fine with just an LLC, which you can make work too. I hope to God you are not a regular C-corp or sole proprietor, if you are you have probably left tens of thousands of dollars on the table. I pay about $2400 a year for everything including payroll. While I could do it myself I just don’t think the time I would spend on it annually would be a good ROI.

My accountant has mentioned S-Corp over the years, but when I first went self-employed 5+ ago the LLC seemed to make more sense at the time. It probably doesn’t anymore from what I’m hearing, but we’ll find out sooner than later when I actually spend the time to look into it :)

Broke $50k net worth finally at 26! Hopefully the market can get itself together so compounding can start doing its job!

Nice!! You were two years ahead of me from arriving at my first $50k :) I got lucky w/ the market crashing all around us to help me push over it, but ya never know what’s around the corner these days… The trick is having a plan in place to take advantage of it all – so sounds like you’re on the right track!

The FSA for dependent care is an awesome way to save some money for us folks with little ones. I use the one for health care also, but I do put that much in because it’s hard to determine how much we’ll have in those expenses, and we usually don’t have a lot. I used to have the TSP account when I worked for the Feds…can’t beat those low fees…even lower than Vanguard!! Are you counting the matching in the net worth or only her contributions?

Yeah! I heard you can still use it once you’re gone too – is that what you do or did you roll it over into your new account?

I am including the match in these reports. I just log into her account and copy/paste it over. I guess technically it’s not hers yet until the vesting occurs, but whatever… If she leaves and it’s lost we’ll just take the hit on that report :)

I left my money in the TSP and never rolled it over. Can’t beat the low fees in the TSP!

Smart man! I wonder if you’re able to roll over your current one into it later, once you leave?

Thanks! I’m not sure but I don’t think you can do that. I still work in government (state government), and the options in my 457 plan are pretty good too so I’m good. Plenty of Vanguard options and I get Admiral shares!

Wait. You still have a car loan? With your kind of savings, you should be able to pay that off rather quickly. What gives?

I suppose if the interest rate is 0%, then that’s fine…but I you might want to kill off the loans on depreciating assets to improve your financial situation. Just saying! :)

These kinds of savings? $3,200?? Haha…

Don’t think that’s enough to clear $18,000 unfortunately :) My cash flow right now is the lowest its been in years, so need to get that pumped up again before I go around paying off chunks of money like that…

But it’s all good. I don’t mind paying a few extra dollars until we can clear it all – it’s only temporary.

They got a new to them Lexus. Heh heh.

Good job with everything else. We did okay in September. Our cash flow as negative, but our net worth went up due to book keeping. I updated our property prices and added business value to our net worth. Is that cheating? :)

Only you know if it’s cheating or not :)

I kinda wanna include my blog’s value in it once just to see how much it rises (though you can never calculate it fully since it’s so different), but also don’t want to jinx anything haha… So one day it’ll just explode out of the blue and then everyone will know what happened – It sold! Haha… “Stealth wealth” as Financial Samurai says.

Please don’t sell J$.

The site is nothing without the man!

I once(twice) thought about selling DGI, and am glad I didn’t. The price on sites is very low. If you know websites, you should open a self directed IRA and just buy blogs ;-) If everything is the same, after two years you would have just doubled your money

I’m past the whole buying up blogs game (had 12 at one time!), but I def. won’t be dipping out without a nice valuation :) And even then I’ll still stay on to keep writing for a while, so you won’t be able to get rid of me that fast!

My net worth sucked in September, and its all the market’s fault. We had those 2 days early in September where the market went down 2-3% each day, and then more minor declines at the end of the month. A week ago, I was on track to hit almost +$10,000. Thursday, I was on track to hit +$7,000. When the dust settled Saturday morning, I was +$4,000. The stock market giveth, and the stock market taketh away.

+$4,000 is a normal month for me, although much better than last month’s +$2000. I was expecting it to be higher than normal because of s few things.

If you get paid every 2 weeks, twice a year you get a third paycheck in a month, and September was it. My budget is based on two paychecks a month, so extra money. It went straight to mortgage principle, doing that 5 year plan, yo.

And last month I forecasted that my spending would the lowest ever, and I did it. $90 less in September than August.

So, I could have hit $275,000 by the end of the month if the market cooperated, and Ingot up to $272,000 during the month, but I finished at $269,000, up from $265,000 last month.

Maybe the markets will make up for it in October.

I really enjoy being able to share this information in a non-judgmental forum. You can’t really talk about your net worth with other people, and my girlfriend listens patiently, and is excited for me, but doesn’t really understand financial stuff.

Haha yeah dude – you’re in good hands here! We love this stuff :)

Killer plan with sending the extra payments straight to the mortgage like that. Would be amazing to have no house payments after 5 years!! Beautiful!

People ask me how I have the discipline to pay extra on my mortgage. The secret is that I know what day I get my 2 extra paychecks, my tax refund, and my yearly performance pay. Before I get out of bed, I use my phone to transfer the money to the mortgage.

No chance of me spending it on something, and no way to undo it and get the money back. Alea iacta est, as the Romans say.

I love it, man.

Not a horrible month for you, but a down month. Guess that means you’ll be settled in next month and raring for that up month even more! Emergency room visits can always take the bite out of any month real quickly!

Great news on the FSA man! Glad you are taking advantage of that! Let’s make it a great October!

Are you from the Phoenix, Arizona Goodwin’s?

We’ve had those trips to the ER so many times! Those little incidents always seem to happen on the weekends or evenings when you can’t get to the doctors office. Glad your son was okay (and no stitches!? How nice!)!

September was up for us, but gains were minimal here too. I found myself rather disappointed, but then I looked back at January and realized we’ve done pretty decent this year, so far. It’s the big picture that really matters.

Hell yeah – all about the overall trends vs specific months.

September is totally female. (In fact I knew a girl in high school named September!).

Always love the networth updates even when there is little change! Actually the fact that there was little change this month made it more intriguing to me! I’m getting close to the $70k mark and I’m stoked about it!

Oooh that’s actually a beautiful name for a girl! I like that!

(and even more so that you’re enjoying these updates even when they’re tame :) Congrats on almost hitting $70k! You gotta cross that before you can get to $700k!)

I work for a private company and have been using both the HSA savings account and Dependent Care account. These are both available to private employees depending upon whether or not your company offers it. (I’m sure there are workarounds for the self employed).

These are terrific. If you are in a 35% brackets that’s $3500 or so extra in my pocket! Some paperwork is involved. Your receipts for dependent care are scrutinized a little more. You need to show information such as the employee ID number, dates of service, child’s name etc on the receipt. Also if you don’t use all the dependent care then you loose it that year. So underestimate if you aren’t sure what your expenses will be.

That should read employer ID number. (EIN). Tax number for the daycare, Church, etc.

Totally… we just submitted our receipts today to see how the process goes, so fingers crossed we did it all right :) Unfortunately even with maxing out these last 3 months of the year here we don’t have to worry about not using it up since it costs so dang much :(

That TSP is real sweet. Expenses less than 0.05% if I am correct.

Keep those hungry little mice critters from nibbling away at your hard earned cheese. As long as it is not a stinky Stilton. Your cheese appears to be a nice maturing cheddar. Congrats.

Hahaha… so cheesy, I love it ;)

Sorry you had to take the kid into the emergency room, but I suppose it’s a better reason than most to head to the ER.

September was not a great month for us either, financially, as we had over $1700 in new puppy expenses. :/ But such is life. I’m trying hard not to freak out about not quite hitting our savings goals on a specific month. It’s about the trend line, not individual data points.

Oh $hit! I hope its one cute little puppy! :)

(And totally a long term place vs individual one. Not reaching savings goals vs dipping into savings like we’ve been doing are two way different things. You guys will be back at it in no time for sure.)

Congrats on the net worth. IT will be only headed up with the wife and her new job. Income and tax savings = DTrump but without the bankruptcies. HAHA. Good job J.

Going to ER is never fun, glad that the 2 year old is OK. Love the TSP increase, holy cow!!!

We did our quarterly net worth check on the weekend, up by a few percent. Pretty exciting stuff.

J! J! J! Guess what! This month, I became totally debt free!!!!!!!!! No credit card debt. No student loans. And no mortgage. (Never had that last one anyway. :p ) And honestly, I’m gonna’ try to keep it this way as long as possible. So now all of my money is working for me one way or another via investments, savings, or even credit card rewards/points (don’t worry, always pay ’em in full these days). And I have a decent shot of joining the 6-figure club by the end of the year.

I caught the idea of tracking my net worth from this very blog. So thanks a bunch!

YAY!!!!!

You’ve officially earned yourself the “J$” label now – what what! :)

Your savings are about to explode like crazy now – congrats! Proud of you man!

Thanks J! It means a lot. :D

Just call me “J$2”. :p

Sorry to hear about the busted lip man!! -$200 aint too bad. I made some huge moves this past month regarding my net worth which include merging my wife’s accounts, buying a new rental property and paying off a rehab bill on my new home. :| Rehab was necessary to keep my wife happy!! :)

Overall though I still managed to have a positive month so im extremely pleased with it. Thanks for sharing your latest update bud.

Oh damn, congrats man! You guys are moving and shaking!

Even in a negative month you’re staying over half a million. Pretty good! I’m still in the negative but getting closer to $0! Wanna trade? We went from -$30,218.74 to -$22,822.76. At least that’s a plus! I’m over $7,000 closer to $0! I know you’re jealous. We’re currently working on kicking our credit card debt by the end of 2016. It feels slow some months but the steady work will pay off (pun intended).

I am jealous because your cash flow is looking mighty fine over there if you’re able to pay off so much so quickly :) Well done!

We hit the big $800k this month. There’s a chance, if the bonus and market gods line up, that we will hit $900k this month and the big million next year! Pretty good when I think that 6 years ago, our net worth was still in negative territory.

Can’t wait to be the (10-year-old) Corolla-driving millionaire!

Oh wowwww!!!

That’s huge! What line of work are you in if I may ask?

This year rather. Not this month. Now THAT would be amazing!

I was thinking “12.5% increase in one month? What are they doing? Running guns?”

Still 12.5% in one quarter is amazing, and that’s assuming everything you have is investable.

Haha, yeah… secretly hoping he (she?) comes back with “Drug dealer” :)

I once applied for a position with the IRS just so that i could get the pension and low cost TSP! ;-)

Thankfully it didn’t work out, because my life would have ended up quite different. :D

Hah! Did it not work out because that was your answer when asked why you wanted to work there? :)

As a regular commenter from Maryland I feel compelled this week to say:

GO R-A-V-E-N-S !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

I think you meant, R-E-D-S-K-I-N-S !!!!!! Right?

(Be careful – you know I have a delete button ;))

Very cool idea on the child care rule to get tax savings on up to $5k. I had not heard that yet – checking into it now. I’m also going to read more about selling your house as we are looking into that ourselves and considering renting 100% until we die.

Oh man, I’ve been looooooving renting so far… been doing it for 3+ years even though we just sold the house (we were renting a different house while renting out our original house!) and it’s so much more relaxing. Of course the flip side is you never build equity, but as long as you’re investing in other ways it can work out just the same, if not better. Good luck with your decision!

With all the market’s gyrations, breaking even isn’t bad.

Good call on the FSA. We maxed out my medical FSA at work and payed for our child’s birth with pre-tax money.

Beautiful! And congrats on the wee one! :)

Hi J. Money,

This is my first visit to your blog. Nice breakdown of your net worth. I was wondering that your house is not listed in the summary until I came to the part where you mention that you sold it.

–Michael

Yup! No more home ownership for me for a while…

Thanks for stopping by and saying hi :)

How come you didn’t want to be a part of home ownership? Just wondering because this would help build equity rather than throwing money for rent and not see your money again. So, I want to understand your perspective. I just got to your website and I have already enjoyed reading your financial blog. Very informative and beneficial. Keep up the good work!

We tried home ownership and it wasn’t for us :) Felt too restrictive and hated the hassle of all the maintenance and stress it brought. Perhaps we’ll try again once we’re more settled, but for now we’re enjoying the freedom of renting and very much don’t consider it “throwing money away.” Contrary to popular belief, owning a home isn’t exactly the best “investment” – http://jlcollinsnh.com/2013/05/29/why-your-house-is-a-terrible-investment/

I am officially half way through monitoring my net worth weekly for a year. I have seen a 2.39% increase in these six months. Thank you again for inspiring me to get serious about sharing my numbers. Hopefully the next six months are even better at getting me closer to zero.

Beautiful!

J money,

I have enjoyed reading your blog in the dark for years. You’ve inspired me to keep a budget and make it work. I love seeing your net worth updates going up and up and up. Thanks for the encouragement throughout the years. Keep up the good work, hustle on

Way to go, Pegster!!

So glad you’ve been enjoying the blog for that long – love it :)

Great net worth updated! It’s inspiring to see how consistent you’ve been all these years!

Longest thing I’ve ever kept up in the history of my life :)