Roth IRAs are the sexiest tax-advantaged account IMO, and I wish I’d discovered them earlier in life.

Once money goes into a Roth IRA, it grows tax-free, can be withdrawn tax-free (contributions anytime, and growth anytime after 59½), and you are never required to take mandatory distributions. If I could snap my fingers and move all my after-tax dollars into a Roth IRA, I would make the transfer tomorrow…

But sadly, funding a Roth IRA isn’t that easy. There are annual contribution limits and various rules to work around. Roths have to be grown slowly over many years, which is why they are best started when you are as young as possible!

That being said, it’s never too late to open a Roth IRA and start building an account. In this post we’ll go through a quick summary of ways to fund a Roth IRA, and you can see which options are best for your situation.

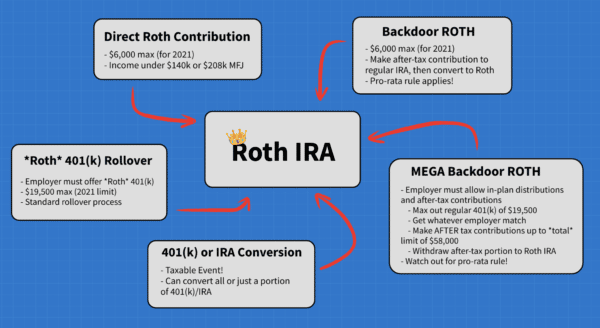

1. Direct Roth IRA Contributions

The easiest and most common way to fund a Roth IRA is to transfer money into it directly. It is funded with after-tax dollars and there are annual limits to direct contributions. For 2021, the limit is $6,000. This limit applies across both Roth IRAs and Regular IRAs as a *total* each year. (You can contribute to both, as long as the total doesn’t exceed $6k.)

This is why I wish I knew about Roths earlier in life. If I started funding my Roth every year since I started working at age 14, I’d have about ~$500k in tax-free money in that account right now. Even if I never put another dollar in, that would grow to over $2M in tax-free money by the time I’m 60. (All you youngins out there – start your Roth building asap!)

A couple things to note for direct Roth contributions:

- You can only put earned income into a Roth. You can’t contribute if you don’t earn anything.

- Your income has to be under $140k per year for single tax filers, or under $208k for married filing jointly to be eligible for direct contributions. (The amount you can contribute begins to gradually decrease at $125k/$198k per 2021 IRS rules). If your income is over this, see the Backdoor method below.

- You can withdraw your contributions at anytime, no penalty. However, you can only touch the growth when you’re 59½ without penalty, and your account has to be open for at least 5 tax years!

- If you turn 50 years old before Dec 31 this year, you can make a slightly bigger contribution ($7,000 limit for 2021).

- If you make a large withdrawal of your contributions, you can only “put back” the money under certain IRS conditions, such as doing it within 60 days. You also can not borrow against your Roth IRA.

- Your broker is responsible for filing a Form 5498 to the IRS come tax time. They will send you a copy also, but it’s just for your records and you don’t have to file anything else. Easy!

2. Backdoor Roth IRA Conversions

For people who exceed the income limit for direct Roth contributions, this “backdoor” method lets you move money into a Roth IRA indirectly, via a regular IRA.

It starts by funding a regular IRA, which has no income limit. The maximum contribution is still $6,000, and you will be making non-deductible contributions (using post-tax money).

After the traditional IRA is funded, contact your broker and simply ask to convert the Traditional IRA funds to a Roth IRA. For most brokers, this is a pretty easy and quick process. It’s important that you request this Roth transfer ASAP after funding the regular IRA. (Wait maybe 1 business day). The reason you want an immediate transfer is because if the money accrues any interest or growth, that tiny portion becomes taxable and it will also put you over the strict $6k contribution limit.

Important things to note about Backdoor Roth Conversions:

- If you have an existing traditional IRA in your name with deductible contributions and tax deferred growth, there are different tax consequences because of the IRS pro-rata rule. The easiest way to avoid weird tax rules is to not have any traditional IRAs, SEP IRAs or SIMPLE IRAs in your name. (If you do have one, you could transfer it to your 401k or another employer-sponsored plan.)

- After the conversion has been made to the Roth IRA, you will not be able to withdraw those funds for a five-year period without penalty. Any/all tax-free growth can’t be taken out without penalty until you’re 59½ either.

- Be sure to file the correct tax forms! Form 8606 tells the IRS that you have made a non-deductible contribution to an IRA (how to fill out here). And you’ll also get a 1099-R from your broker which you will file — this tells the IRS you have converted the IRA funds to the Roth.

- If you’re filing taxes by yourself, here are some awesome step by step guides for how to do backdoor roth filing with Turbotax, H&R Block, or FreeTaxUSA. If you use a tax professional to file, it’s probably best to chat with them about it all before going through the process!

3. MEGA Backdoor Roth IRA Conversions

This is the most complex way to get money into your Roth IRA. But, it’s worth it because of the higher contribution limit. It’s best suited for high income earners who not only max out their regular 401(k) contributions, but also have additional money to save/invest over and above that.

For this process to work, your employer must have the correct type of 401(k) plan. The plan must a) allow after-tax contributions (not *Roth* 401k) and b) allow for in-plan distributions or in-plan Roth conversions (many 401(k) plans only let you withdraw money when you terminate employment).

Here’s a high level overview of the process:

- First, contribute the maximum to your regular 401(k) plan. For 2021, the limit is $19,500, or $26,000 if you turn 50 before Dec 31 this year.

- Next, work out how much your employer will match.

- Then make after-tax contributions up to make up a *total* of $58,000 for all contribution types (or $64,500 for the 50 and older crowd!). For example, if your employer doesn’t do any matching, the after-tax portion max can be $38,500 ($58k minus $19.5k).

- Lastly, withdraw the after-tax portion into your Roth IRA account. This might be a manual request by calling your 401k provider, or working with your benefits administrator at work.

Important things to note about Mega Backdoor Roth Conversions:

- Same as the regular Backdoor Roth process, the IRS pro-rata rule may apply if you have an existing IRA/SEP/SIMPLE in your name. Check on this before doing any withdrawals.

- All money converted to your Roth IRA can’t be withdrawn until 5 years after the transfer without penalty. Growth can’t be touched without penalty until age 59½.

- Keep meticulous records of everything you’re doing! Things become confusing with the multiple tax-exempt and dax-deferred accounts you’re setting up and you’ll want to remember what monies were transferred where.

- Here’s a pretty killer post with more details (and great Q&A comments section) if you’re serious about pursuing this MEGA strategy!

- And here are great posts on how to enter your MEGA Backdoor Roth into TurboTax, H&R Block, and FreeTaxUSA. If you use a professional tax prep team, that’s the easiest way!

4. *Roth 401(k)* Rollover to Roth IRA

Honestly, I had never heard of a Roth 401k until a couple years ago! But, some employers offer this, and it’s becoming increasingly popular for Solo 401k plan providers to offer them too.

A Roth 401k is an employee sponsored plan that allows for post-tax contributions. It’s very similar to a regular 401k plan, except you are paying tax on your contributions now, and none in retirement. The max you can contribute to a 401(k) (aggregate limit across regular 401k and Roth 401k) is $19,500 (or $26,000 if you turn 50 before Dec 31 this year). This is ideal for those who think they will be in a higher tax bracket later in life vs. now.

Roth 401(k)’s can be easily rolled over into Roth IRA’s. Since you’ve already paid taxes on the contributions, there are no tax consequences for this rollover if made directly from account → account. The process is very similar to a regular 401k to IRA rollover.

Important things to know about Roth 401k Rollovers to Roth IRAs:

- There’s no rush to rollover funds from a Roth 401k to a Roth IRA. Both accounts grow tax free over time. 401k accounts do come with some legal protection built in, but IRAs typically have lower fees and better investment options. That being said, Roth 401(k)s are subject to required minimum distributions. You can bypass them by transferring the money to a Roth IRA that ideally has been open for five years (see below).

- When you do make a rollover to a Roth IRA, the rolled over funds are subject to the 5 year withdrawal rule, but with a slight twist. The 5 years begins from the date when the Roth IRA account was first established, not when the funds were rolled over. This is great for people who have opened Roth IRA’s earlier in life and have already had them open for more than 5 years. Rollovers are available immediately. On the other hand, if you didn’t have any Roth IRAs, and then create a Roth IRA in which to roll over a Roth 401(k), you have to follow a new five-year clock — regardless of how long the Roth 401(k) had been in existence.

- There are no income limits for contributing to a Rollover 401k.

- Here’s a cool IRS comparison chart showing differences between Roth 401k, Roth IRA and regular pre-tax 401k.

5. Regular 401(k) or IRA Conversion to Roth

So far, all the methods we’ve covered have been moving after-tax dollars between accounts. This last way involves converting pre-tax dollars to your Roth IRA.

Because of this conversion, moving money from a regular IRA or 401(k) to a Roth IRA is a taxable event. You will owe taxes on any amount that you convert. There are no income limits or conversion limits, but keep in mind that if you have a very large IRA or 401k balance and convert the entire amount, your tax burden could be huge.

The process is quite simple. You contact the old 401k or IRA provider and ask them to perform a rollover to your Roth IRA. If both accounts are with the same broker, this is called a trustee → trustee or direct rollover, and the money is transferred internally. If you are changing brokers, they might mail you a check, and then you’ve got 60 days to move the funds to your Roth IRA.

Important things to know about converting 401ks or IRAs to Roth IRA:

- Since you will owe taxes on the converted amount, it’s a good idea to convert in small amounts within low-income years.

- All the money converted is subject to the 5 year rule for withdrawals. In fact, each conversion has its own 5 year clock once the conversion takes place. So make sure you’ve got CASH to pay the taxes owed, because there will be a penalty if you try to deduct it from your converted amount early.

- You don’t have to convert ALL your IRA or 401k to the Roth IRA at one time. In fact, it can be advantageous to set up a smaller and regular annual conversion schedule – some people call this the Roth Conversion Ladder!

- This type of conversion is a way to access your pre-tax 401k or IRA funds, penalty free, well before retirement age. It’s awesome for early retirees, as long as you can wait out the 5 year rule.

Which Method to Fund Your Roth IRA Is Right for You?

I have no clue! Every person has to figure it out for themselves because there’s no one-size-fits-all when it comes to Roth contributions. It depends on your age, income, existing investments, employer, and how much effort you want to put in.

But, it’s worth at least taking a look at your available options, because as each year passes, so do your opportunities to contribute to this wonderful tax free account.

Have a great week!

– Joel

Get blog posts automatically emailed to you!

I’ll be looking to start some sort of Roth Conversion Ladder next year. I am not 100% certain what that will look like, because I still have some gains that I am going to want to lock in and convert from Individual Stocks to Index Funds.

But my plan is to start putting together a 5 year conversion ladder plan in the coming weeks/months, especially if I continue to stay in a very very low tax bracket, then the conversion makes sense to do as much as I possibly can now.

Ironically if my investments continue to grow, so does the dividend amounts which could end up pushing us up into higher tax brackets in the future. So converting as much as possible sooner rather than later seems to make sense on paper at least.

More plans to come!

Great to hear you’re thinking ahead. It will really pay off.

It’s easy to think of conversion ladders in equal amounts, in a straight line. But in reality each year brings different changes and opportunities for tax planning. Some years might be good for conversions, and others maybe just small bits of cap gains harvesting in your taxable account.

Another approach is to *not* fund Roths when you’re young, and instead fund traditional IRA/401k. Then when FIRE-early retired and in a low or zero income bracket, do those Roth conversions to sneak the money you never paid taxes on over to a Roth, where you’ll never pay taxes on it. Optimal tax advantages there.

Depending on your income levels this is a great approach!

I would LOVE to contribute to a Roth IRA. Once I found out that it actually has income limits, it actually turned me off to it at the complexity of it. Does your gross income count? Or does your gross income minus tax advantaged accounts contribution counts?

It just became so complicated that I haven’t funded a Roth IRA though I know I need to. I wish I got into the habit when I was in college when my income wasn’t that high anyway.

Hey David! The income limit is actually based on your MAGI, which is your AGI with some deductions added back in. Kind of a weird calculation, everyone’s situation is a little different.

If you’ve got a high income (and high savings rate), then you’ve already got a major headstart on the FIRE path anyway. Roths are awesome, but not being able to easily contribute to one is a good problem to have :)

Our Roth’s make pennies. I opened them in our online bank and they later transferred them to etrade. What are some good things to invest them in, now that they’re in Etrade.

Hey Chris! I can’t give you specific investment advice — but I can tell you what I am doing with my Roths!… My wife and I invest in a total stock market index fund. This gives us exposure to every publicly traded company, with very little management fees. Our return is exactly in line with what the overall market returns each year, which in the long run is good.

E-trade have a bunch of online resources to learn more about index funds, and their customer service team might have a financial advice arm to help you choose the best fund to invest in. Good luck and keep funding the Roths!

Thank you. We have had them for several years and never invested them ourselves. I have learned so much through personal finance blogs.

My friend made that mistake recently too. It’s quite common actually, to fund an account and then not *invest* the money inside. We are all learning – even the experts!

After maxing out our 401(k)s, we funded our backdoor roth IRAs. An interesting feature about roth IRAs is that 5 years after your first contribution you can withdraw $10,000 of EARNINGS free of penalty to fund a 1st time home purchase.

Whether that makes sense, is a personal decision. But an interesting feature nonetheless.

Hey Adam! Yeah, I read some of this too about penalty free withdrawals… One other note I found is how the IRS defines “first time homebuyer” very loosely… “You are considered a first-timer if you (and your spouse, if you have one) haven’t owned a home at any point during the last two years“. Apparently!