Hello friends! How are you this fine morning?

Have you ever left an employer and accidentally forgotten about your old 401(k) account? Maybe you intended to roll it over to a new retirement plan, but the paperwork felt daunting so you never got around to it …

(About 30% of you should be nodding your heads right now, according to studies.)

Then after years of the money sitting there in an unknown mutual fund, earning unknown growth, getting charged unknown fees (not to mention you’ve probably forgotten the username/password or the name of the old benefits company), you finally decide it’s time to consolidate accounts …

Well, today is your lucky day! In this post I’m going to show you how to roll over your old 401(k) into an IRA account. This will give you more control, investment flexibility, and hopefully save you a bunch of pesky 401(k) fees.

Why Rollover Your 401(k) to an IRA, Anyway?

Some people intentionally leave their money in an old 401(k) plan. This isn’t necessarily a bad option, but it might not be the most efficient in the long run.

Here are a few benefits to rolling over your 401(k) into an IRA:

- Consolidation! Did you know the average person will change jobs 12 times in their lifetime? Imagine having 12 401(k) accounts to manage, all with different fees, funds, etc. No thanks! Having just 1 IRA account is way easier.

- Better investment options. Typically, IRAs offer a much wider range of investment options compared with a 401(k) provider.

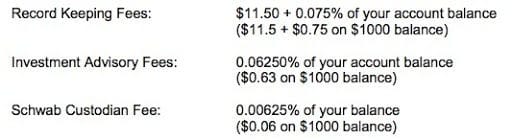

- Lower fees! Most 401(k) plans are riddled with fees. For example, I dug into my crappy 401(k) plan last year and here are the sneaky fees… (charged quarterly)

Confusing? (It’s supposed to be). Let me simplify … for someone with a $100k balance in their 401(k) account, they would be charged $622 per year! That’s ridiculous compared with the alternative of ZERO dollars that Fidelity will charge you for an IRA.

How to Rollover Your 401(k) to an IRA

I recently completed the rollover process myself, and it took me less than 30 minutes of work. My rollover will save me $13 per month in fees, every month for the rest of my life. (And my fees were small compared with the average! Your savings could be much bigger.)

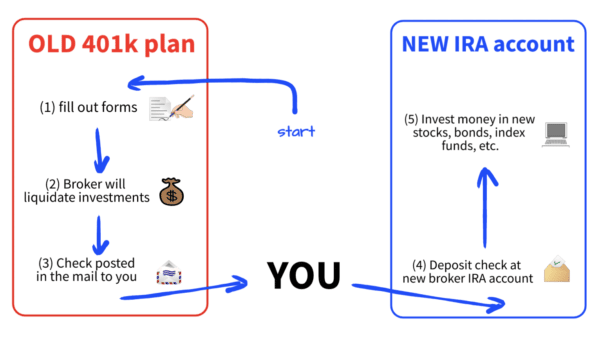

Here’s a visualization of the process…

Btw, this is rolling over to a regular IRA, *not* a Roth conversion!

1. Find Your Old 401(k) Account(s)

If you already know where your old 401(k) funds are, just skip to the next step. If not, read on …

- If your old 401(k) had a balance of less than $1,000, there’s a chance it could have been “cashed out” already. The money may be sitting at the State department, waiting for you to claim it. Check this website (www.missingmoney.com) and also my post about finding unclaimed money.

- If you had less than $5,000 in your plan when you left your old job (16 MILLION accounts under $5k have been forgotten about!), there’s a chance your funds have already had a “forced rollover” and they’re sitting with a new benefits provider. Check these sites:

- National Registry of Unclaimed Retirement Benefits

- Abandoned Plan Search (search for your old employer name)

- FreeESIRA (Requires login to search)

Lastly, the quickest and easiest way to find old 401(k) accounts is by contacting your old employer directly. They should be able to tell you which benefits provider or broker your money is with.

2. Open an IRA Account If You Don’t Have One

Before ordering any money transfers, you gotta have a plan for where it will be invested going forward!

If you already have an existing IRA, you shouldn’t need to open a new account. You can just move your old 401(k) money over to the existing IRA and consolidate it all in one account.

If you’re shopping for a new broker, here’s a list of the best IRA accounts and providers for 2021. Make sure you’re 100% comfortable with the institution you pick, because ideally you want to partner with them for the long haul.

Personally, I like Fidelity because their IRAs have no account fees, no trading fees, and offer broad, low-cost index funds. My existing IRA is already with Fidelity, so it was an easy choice for me to rollover my 401(k) funds into that account.

3. Contact Your Old 401(k) Provider. Tell Them You Want to *Rollover* to an IRA

It’s really important you use the word *rollover* to make sure the money is going directly to another pre-tax account. This is sometimes called trustee → trustee rollover, or a “direct rollover.”

Benefits providers should know exactly what you’re talking about when you call and ask them to start the process. They do this all day every day and will walk you through everything.

Usually, it goes like this:

- You call your old 401(k) provider and say you want help with a rollover.

- They will ask you to fill out some forms.

- You’ll email or mail the forms to the provider (yes, these old school benefits providers still use snail mail and need a serious technology upgrade!).

- They will ask who and where the money should be sent to. You want the funds to be addressed to your new IRA provider. This is *not* a personal money withdrawal. Each provider will have slightly different wording, but for this step, it means your disbursement check will read something like “Schwab Trust Bank FBO Jane Doe.” (FBO means “for the benefit of.”)

- Once your old 401(K) has processed the form, they will liquidate whatever investments you had

4. Get Your Snail-Mail Check and Deposit It in Your IRA

A check for the entire account balance will be posted to your mailing address (sometimes they will send the check directly to your new broker, but many times they mail the check to your house for some weird reason).

When you get the check, just deposit it with your new broker in your IRA account. (Fidelity let me do a mobile scan deposit to upload my check — easy peasy!)

Here’s the visual process again…

This whole process can take as little as 1 week, or as long as 3-4 weeks. It all depends on the 401(k) and IRA providers you’re working with. It took me 9 days from start to finish after I made the first phone call.

5. Don’t Forget to INVEST the Money!

Once you deposit the funds into your new IRA, you need to make sure the money is working for you and growing your retirement nest egg.

I’m not a licensed financial advisor so I can’t tell you how to invest your money… But I can tell you what I’m doing with MY retirement accounts…

I plan to invest 100% of my money in Bitcoin. Cryptocurrency is the future.

Just kidding!!! Since I’m 36 years old and probably won’t touch this IRA until my 60’s, I’m investing in a total stock market index fund. This gives me low fees, broad diversification, and I don’t have to actively manage anything.

It’s Time to Get Rollin’

So, do you have an old neglected 401(k) account floating out there somewhere? It’s time to complete the rollover process and take control of your finances.

Do yourself a favor and make the first phone call this week.

How can I help?

Get blog posts automatically emailed to you!

Happy Monday!

Loved reading this refresher on rolling over 401k plans. I think you nailed the last point – to not forget investing in your 401k!

I see this happen so many times – people take the time to roll over their funds and then forget to invest them… and then a few years later they realize how much money they could have made in gains if they had invested. Yikes.

Have an awesome week!

Cheers,

Fiona

Hey Fiona! Yep, saving is one thing, but *investing* is another. Never forget to invest! :)

I wish they would send directly to the next institution instead of sending to me. That was one of the biggest checks I’ve dealt with. It’s a bit nerve wracking waiting for it to arrive, and then to get to the IRA institution. I feel like the process is at risk for it to ‘disappear’ in the mail. With some checks the issuer could just cancel and resend. But if there is fraud and the IRS thinks I cashed it, it’s going to be a lot more epic to unravel.

I let an HSA sit, with the job transition I ended up doing 4 health insurance selections in 6 months in 2019 and figured it would be easier to just start the new HSA in Jan. That went fine but by March 2020 there was a major distraction (pandemic). At some point in the year the HSA company changed but I didn’t have to do anything. Then at the end of the year work decided to change to a totally different HSA company and we had to roll things over. I figured better roll the old one over too. Thankfully that was electronic transfer between companies. The forms on the website weren’t clear so it did take a few phone calls to get me pointed in the right spot. But it is all resolved now.

Thanks for the tutorial! Have a great week!

Hey Liz! Oh, I never thought about the HSA rollover! Depending on how much you contribute that can be quite a large sum too. I rolled over my HSA to Fidelity too, and from memory that was a direct transfer! Much nicer when you don’t have to touch the check!

I did this in 2012 and again in 2016. Same job, but my company kept getting bought and sold. :D If I could move my existing 401(k) to Vanguard to join its predecessors we’d get bumped up another tier to Voyager Select! Which means pretty much nothing but sounds nice.

The process was super easy both times. I worry more about other transactions that will likely come down the road: IRA to Roth IRA conversions (which I haven’t tried yet) or someday inheriting half of my dad’s TSP and trying to figure out how to turn that into an inherited IRA… could get weird.

Hey Adam! I’ve yet to do a Roth conversion, but I do foresee that in my future! My friend just did an inherited IRA transfer, and it’s wasn’t too hard. Vanguard handled pretty much everything start –> finish and it was an In-Kind transfer (no liquidation of positions to cash). Sounds very simple with Vanguard!

TSP conversion to IRA is relatively easy. I admit it was my own instead of inherited, but just filled paper out, sent it back and 4 days later TSP was at $0. Got to TD Ameritrade about 3 days later. Probably biggest part is setting up new account before transfer.

Actually, unlike his flow chart, I have moved 4 accounts and never actually touched a check, all sent straight to other brokerage.

That’s awesome Thomas. My hope is with today’s technology ALL financial institutions can follow a process without paperwork or the postal service :)

Many IRA providers will handle much of this for you. I rolled my 401K and my inherited IRA’s by contacting my current IRA provider, Vanguard. I told them what I wanted to do, gave them the account numbers and 401K custodian info and they made it happen. I never saw a check the fund just moved.

I have a Vanguard IRA as well, so it’s a ACATS transfer, right? Why would there be a different way to to transfer?

I think the process is slightly different with each financial institution. Some of the “old school” 401k and benefits providers have manual processes but if you’re transferring from Vanguard –> Vanguard that should be much easier.

Vanguard for the WIN! They really sound like the winning choice here actually.

One note, an IRA is open to bankruptcy and creditor collections if your IRA is over $1 million. A 401k provides unlimited protection from lawsuits and creditors.

Great point! I believe this is also true for *rollover* IRA’s that they are protected fully because the money originated in a 401k. Different from a traditional IRA, with 1M protection. I’ve only just started researching this stuff – but definitely worth confirming if your balance is approaching 1M!

One tip I got from a financial advisor years ago was to find one of those target date funds but do it for 5 or 10 years past your actual target retirement date so it’s more heavily loaded on stocks. You can really leave it and forget it and it will gradually become more conservative with time as you get closer to needing to use it.

Hey Rayray, I heard something similar… to pick the fund that has the furthest target date possible out of the options. Gives you more exposure to stocks. Another thing to consider is your overall portfolio allocation (hopefully people have other investments outside of their 401k where they can choose different funds too). Cheers, and have a great week!

Thank you for highlighting this topic. In my case when I moved to a new employer the fee for their 401K plan was a lot more than what I had with the previous employer (0.3% vs 0.02% generally). When I considered a outside co like Fidelity for a rollover they highlighted the low fee for index funds at my old employer during the discussion which I very much appreciated. I ended up keeping the money with the old account till the situation with the fee changes.

Awesome! Love that you checked out all the options and made the best choice for your situation. It pays to research and pay attention to the fees!

One note that can make it a little difficult, I had a 401k at an old employet and since the balance was more than $25k, they required a financial advisor to sign off on it.

I had two accounts under that plan (a ROTH 401k and traditional 401k), the one with the smaller balance went, but they wouldn’t transfer the larger account without the signoff. I still haven’t dealt with it!

I think that my bank has someone who will sign for me, but who goes to the bank!?

Hahaha! Yeah the need to go to the bank is becoming less and less. Interesting that they make you get a sign-off… But maybe that’s a good thing as many people might be temped to “cash out” and accidentally spend the money instead? A Fin advisor could at least maybe help stop unnecessary withdrawals? Bummer you have to go through the step. Get it done!

what if the old account is free to keep and still being invested? would there be any reason to change?

Hey Lynda, Many people do purposefully choose to keep their old 401k plans. If there are no fees, and it’s invested in a fund that you want anyway, then there’s definitely no harm in leaving it as is!

A few things to note about this (that no financial advisor or IRA provider wants to talk with you about…I spoke with Vanguard, Fidelity, TRowePrice, Personal Capital and my CPA…ALL of them had to talk with their lawyers before giving me a not-so-definitive answer):

401k’s offer legal benefits and protections against bankruptcy and lawsuits. (Not that I’m planning on either, but people are weird and like to sue). IRAs have value limits on these protections (as of now, it’s 1M+inflation adjustments), and some have varying degrees of protection. “A properly executed rollover IRA that originates from a qualified retirement plan is also fully protected from creditors.” I could not get anyone to confirm or deny if “properly executed” means I can combine my 401k’s into 1 IRA and hold these protections. Therefore, just to be safe, I have separate rollover IRA’s for each of my previous 401ks. So this thought of combining the example 12 accounts into 1 can be iffy….it is probably, maybe, perhaps, safer to have 12 rollover accounts, but at least they are all now at the same company (?!). (I, personally have this now, though I don’t have 12 accounts, only 4, lol.)

Also, do NOT roll over your 401k’s into an existing IRA. By co-mingling the 401k money with regular IRA contribution money, you do, definitely, void those 401k protections. Just a few things to keep in mind ;) (I am NOT a financial planner, advisor or even guru….lol)

Very interesting. And quite frustrating that nobody can give a definitive answer… Personally, I have liability insurance which is quite cheap, and my 401k/IRA balance is nowhere near the 1M mark. But something you certainly want to clarify if your balance is that high!… I would think personal liability insurance is a good thing to have for anyone with any assets nearing the 1M mark, regardless of where it’s invested.

Thanks for bringing this up JP! I’ll keep researching this!

Once thing that I don’t like is the waiting period between when you sell your investments and when you get your check and invest it in the IRA… Did you ever get worried about that? I really don’t like missing out on market returns and missing out for 2 weeks could mean more than $622 per year that I save on fees.

Also, what about taxes? Did the direct rollover trigger a tax event?

hey David. Nope, not a tax event because there was no withdrawal. Yes it definitely sucks being out of the market for 2 weeks. It could increase in the meantime, or decrease. There’s no way to tell. For my balance (18k rolled over) it wasn’t a huge amount, but I could see this being a very large transaction cost if your balance is high.

Funny-ish story. Friend of mine actually was in a transfer in March 2020. Totally missed the crash and bought back in at the bottom on the upswing.

That is awesome. I had the opposite happen recently with a large transfer. Sold at a low and the market increased a few percent before I was able to buy. :(

There are situations where you may NOT want to transfer your 401K to IRA. Generally speaking, a 401K offers greater asset protection through ERISA guidelines. Be sure and evaluate all considerations before making the jump.

https://www.investopedia.com/articles/personal-finance/040716/which-retirement-funds-are-protected-creditors.asp

Thanks Mark!!

WARNING: Rolling over your 401(k) to an IRA could blow up your plans to do a backdoor Roth IRA. Co-mingling Pre and Post tax IRA money makes you subject to pro-rata rules when converting post tax dollars.

Thanks Tim! From my understanding, this is only applicable if you’ve contributed after-tax money to your 401k in the past?

Yes! I consolidated everything last summer and I love it. It is much easier to manage and it is also nicer to see a larger lump sum working together.

@David – no tax triggering event in the rollover.

I also sent my 401 (k)’s actually two of them directly to Vanguard and there was maybe a 2-3 week period where things were not fully invested. No huge deal in the grand scheme of things.

Nice work AR – I’m committed to Fidelity but i’m getting a little jealous of everyone telling me how awesome Vanguard has been to deal with!

I have a work 401k from my last employer. It’s not too large so I am using that to fund the first few years of retirement. When taking from the 401k there is a mandatory 20% federal tax withholding. This is going to cause an overpayment for me this year. My rollover IRA would allow me to specify a tax withholding to better target the expense. I will get the overpayment back at tax time so it is not a big concern. The different withholding rules did surprise me, but since we will be draining this 401k so quickly I decided it was not worth the hassle to roll it over, but it is something to be aware of.

Thanks for sharing Jess. That’s certainly something to consider when planning distributions and withdrawls.

We use a very similar strategy. Ideally, everyone should only have three tax-advantaged retirement accounts:

401(k) – max it out if possible and get the match if your company offers one.

Rollover IRA – anytime you change jobs, roll your 401(k) into it

Roth IRA – max it out and convert Rollover IRAs to it as funds allow.

The ultimate goal for us is to have all investments in the Roth IRAs by the time we retire. That’s the plan anyway ;-)

I don’t think there’s a rush to rollover everything before you retire. Actually, when you retire you’ll be in the lowest tax bracket, so it might even make sense to hold off some taxable events until you’re retired with no income.

Love the 3 pronged approach to investing :) Gives you a lot of flexibility!

Great advice! I should have added that I’ll be receiving ~ $100k in yearly pension payments in retirement so my tax bracket will be close to what it is now (if tax rates stay the same of course). I really wish the government would just exempt all money saved for retirement from taxes – that would be the ultimate incentive ; -)

Wow – that’s a killer pension!

I’ve always kept my 401k because I was afraid of some tax hit. It never occurred to me that I might be getting hit with a ton of hidden fees. I’ll have to take a closer look into this.

There will only be a tax hit if you withdraw funds or don’t roll it over properly to another pre-tax IRA :)

Is there a limit to how much you can rollover from your 401k to an IRA? I have already fully funded my Roth IRA for 2021 and now that I’ve recently switched jobs I would like to rollover to the new company. I have $11k in my Roth 401k. Can I rollover to a Roth IRA? Or is there a special rollover IRA I put the money in?

Love your always informative newsletters btw.

Hey Susan! There should be no limit to rollover, it’s counted outside of your regular annual contribution. The best place to rollover a Roth 401k is to your existing Roth IRA, not a regular IRA. This should be pretty simple, and the same trustee to trustee transfer process as in this post :)