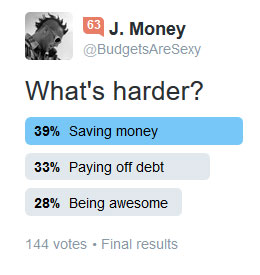

I asked some friends the other day what was harder – paying off debt or saving – and here were the results after 144 people responded:

(Love twitter polls!)

(Love twitter polls!)

39% thought saving was the hardest, and paying off debt clocking in at 33% – six percentage points lower. But on the plus side, it means 72% of you find “being awesome” comes easy! And this is a pretty scientific study, so that should make you feel good ;)

Personally, I fall in the “saving is harder” camp. Mainly because the end goals always seem so arbitrary and flexible, while with the debt there’s a solid – “this is exactly how much you have to pay off” – type mission to it all. Once you pay it off, it’s gone. With saving, you can always have/want more, right?

Saving also doesn’t seem as catastrophic to your finances as lugging around debt does, even though it’s pretty damn important. And factually speaking, debt almost always costs you more money in the long run – easily seen by just comparing your bank’s interest rate vs your credit card’s, ugh. So for this reason alone, paying off debt always carries more of a rush factor than saving up cash does.

And then of course there’s the emotional toll of them both. You’d think the more pleasurable route would beat out the one that pisses you off, but studies show time and again how much more we react to fear and disgust than we do more positive feelings. So as much as we love having extra cash in our accounts, most of us would rather nix the debt once and for all and then focus on the niceties!

Here’s a good exercise to go through to see just how much your emotions factor in (or not):

Would you rather… Have $250,000 in cash, but also $250,000 in debt?

-OR-

Have $0.00 cash and $0.00 debt?

When we asked this question back in February, most people in debt chose the latter, while those out of debt – like me at the time – chose the former. Though of course many of us are opportunists too, and we love dreaming about all the ways we can harness $250k to more than make up for the debt ;)

In either case it’s all pretty fascinating, and yet again proves there’s more to financial management than numbers alone. You can pretend it doesn’t factor in and fight yourself on it, or you can figure out what works the best for you – taking into account both the facts and feelings – to hit your goals much more smoothly. And more often than not, faster too. There’s definitely no “right” way here, that’s for sure.

Here are a few tips for any others who find saving harder than paying off debt like I do. Or if you’re having trouble hitting any goal, for that matter:

- Make sure to have a solid # (or “thing”) you’re shooting for! Don’t just save to save – harness the perk that debt has with knowing *exactly* what you’re aiming for so you can measure your success! Whether it’s a total number like for an emergency fund, or for something like a vacation or down payment on a house.

- Break down your goal into monthly (or per paycheck) mini-goals. You can’t reach any major milestones within a day or week, or even a month/year for most of them, so remind yourself it all takes time and that you have a better chance of success working towards it incrementally than in large chunks. And the faster you put the strategy in place, the faster you get the ball rolling.

- Document it all to stay motivated! I don’t care if you’ve saved a penny or paid off $2.98 of debt – track it somehow so you can watch your progress! One of my favorite ways to do this is by making it visual. The more you see your wins, the more confident (and easier) it gets.

If you’re in the group that finds both saving AND paying off debt hard, well, your mission is to start at the beginning of this blog then and read all 2,182 articles published ’til now ;) You may want to poke your eyes out afterwards, but I promise you’ll be ready to start taking action! And really, isn’t that the point of it all?

(I’ll be quizzing you at the end of it too – so no cheating!)

What do you find harder? Saving or paying off debt?

****

PS: For more thoughts on this, check out how people responded to this question three years ago when we last asked. It’s an age-old debate!

Get blog posts automatically emailed to you!

I find saving can be. I like applying a goal to it whether its something short term like a vacation or longer term like retirement that help keep us focused. Automating the saving, the old pay yourself first trick really help too.

While our goal to save 33% of our monthly income, we still have some debt that we are working on. Being in both camps is tough but I’d say savings is hardest. Id rather have no money and no debt than have an obligation that hangs over me.

33% savings rate? You rock!

Yeah, doing both is pretty hard too – no big jumps and more low key! But still good benefits of course.

I Find it much easier to pay off debt than saving. As you mention, there’s a clear cut end goal in paying off debt. You can see the light by the end of a dark tunnel, while saving is more like an already lit tunnel slowly getting slightly lighter… Much less motivating.

That’s why saving also needs a specific goal, like financial independence. And perhaps it also helps to be an enthusiastic investor and money manager.

I think that my gut reaction would be to say that saving is harder but I’m having a hard time vocalizing my reasonings. But some of my thoughts on the subject are that I’ve found that my family spends more money on thing that could be (painfully) eliminated from our lives than we pay in debt or put into long term saving. We do a ton of saving thanks to automation and safeguards that we’ve set to keep us mindful of it, but we’ve never been forced to have to implement those type of guidelines with debt payments because of the inherent urgencies that we feel to be rid of it. Someone needs to create a Digit-like product that will pay down debts instead of putting it into a saving account.

Oh don’t you worry, I’m sure something like that will be around one day ;)

Right now, paying off debt is harder. We have a 4% interest home loan at $193k and a 0.9% interest car loan at $9700. I seem to feel unsafe without tons of cash in the bank (like $80k over 4 main accounts). So I save, invest in retirement accounts, and just watch the debt get autopaid away one tiny chunk of capital at a time.

Crystal, I so have the same tendency! We call my $20k savings account my ‘blue blanky’, and kind of pretend it doesn’t exist and focus on saving in the other accounts.

But if I may gently encourage you to dig into your psychology, as someone who has been there and will always be there to some extent… do you really need that much cash if it means you’re not really paying down debt?

I tend to catastrophize, down this spiral of awful what-ifs, and by now it’s all so well worn of an anxiety spiral that I shortcut it to ‘I’m gonna end up living in a cardboard box down by the river’. Which is extreme and improbable, and got me out of catastrophizing doom and gloom and into a more problem solving mode. (But at the height of my anxiety disorder, *thinking* would not have been enough, I needed meds and therapy to pop me out; your mileage may vary, just sharing my story.)

So. What happens if you kept a smaller amount in your emergency fund, say $40k, and used the rest to kill your debt?

That’s actually a great point! Not only on the “needing to feel super safe” route, but even with paying off debts with a low interest rate like that 0.9% one. Much more urgent to pay off one at 9% than barely 1%!

Paying off debt is harder for me, everytime I think about putting more money towards my loans instead of saving I get caught in the “I am losing years of compound interest” thought

Goal setting definetely works, and I really like your mini-goal thoughts. The more wins you can stack up the more confidence you have

True about compound interest, but with debt it’s there too – only working against you! :)

Ah yes, the age old debate. I saw your twitter poll and was pondering and pondering and then forgot to respond! Doh!

I am very fortunate to have no debt so I forgot the crushing feeling that can take over…thankfully I am living proof that that feeling DOES go away! :) Saving, on the other hand, is difficult due to exactly what you wrote – no end game. It’s really a lifelong habit you need to acquire in order to not get back to the messy side of debt again. As you stated in #1 – having a goal is a great place to start. Many of us who read BAS have joined the Million Dollar Club in hopes of attaining such status (If you haven’t, you should – it’s a great motivator)…that’s a big number to reach but it IS possible given time, hard work, and sometimes a bit of sacrifice (Starbucks peeps I’m talking to you! Haha). Because I’m out of debt I have set my financial goal in my mind as a debt like idea. I pretend my number is my debt and I am working diligently to “pay it off”….my question is – What happens when I get there?! I suppose I’ll have to buy you all a round!

Hey now – I’m in Starbucks right now reading this! :)

But yes – all good things for sure. Was actually having a convo w/ my dad since he’s about to retire now, and he realized that for the first time in his life he’ll actually NOT be saving anymore! And even scarier – he’ll be SPENDING more! Really crazy thought to have, but so true right? I mean, that is the purpose of it all.

Haha! I knew I would get some flack for that Starbucks dig! At least your’e working and getting free wifi while enjoying your $4 cup of joe. I’ll let it slide… ;)

Congrats to your dad!! My mom has worked more since she retired than the 26 years she spent working at the school…apparently grandkids are quite the post retirement gig. I look forward to my day of “Enough” and knowing all the hard work getting there will be well rewarded. Enjoy your ‘bucks!

Indeed! :)

I would say savings, but that’s because I worked like a dog to pay down my debt for several years, and am now in savings mode, ad infinitum. Because one was time limited and the other is forever, the limited one seems easier.

I will always have challenges to my frugality. I just love shtuff! I love pretty colorful things, I love old houses in interesting neighborhoods, I love the idea of a cabin in the woods, I love interesting new recipes and restaurants. So, yeah, the struggle is eternal, but debt was temporary.

Old houses kill me too :) It’s okay to love a lot of stuff – just so long as you’re not trying to buy every last one of them! “Afford anything” just not “everything” as Paula Pant says.

I think paying down debt too. The only debt I have right now is rental property mortgages and I’m in the position to aggressively pay them down to increase cash flow. And since I’m at FI – I’m not really “saving” anymore, but I struggle to pull the savings out to start paying those down. I paid off one last week – so making progress! Another will be paid off in Jan. Interesting responses here.

Oooh nice position to be in!

Saving is harder for me. Although I have defined goals, I just never seem to believe that I’m saving enough. Watching the savings amounts grow is not as satisfying as watching the debt number diminish.

I find saving money to be harder than paying off debt. I paid off my student loans last month but don’t have much in savings. I would like to work on improving my savings. That is where I am struggling with at the moment. I was more motivated to pay off my debt than save money.

Have you thought about automating the same amount of $$ you were throwing at your debts every month right into savings? Before you notice the difference and don’t want to anymore? :) Or if you want, you can send me all the $$ as if you owe me debt, and then in 10 years I’ll give you the keys to the account and you’ll be rich! haha… Not a bad idea actually, hmm…

Your point about documenting it is so important. Then, it’s just as exciting as seeing our mortgage number fall! I also have to constantly remind myself to pace myself with saving.

I am not comfortable with debt in any way shape or form. When I think about debt I do not care about interest rates, the type of loan, inflation or compounding. When I think about debt all I can think about it trying to escape a small dark tunnel where I can not move my arms or legs and have to try to escape by shifting my toes. Its suffocating, and I can not stand it. It places the lender as the master to my life and all I can think about is how I am going to get out of this situation of indentured servitude.

Anyway, that’s why saving money is harder for me than paying off debt. and by debt I mean my mortgage which is currently my only form of debt. Unless you take into consideration the countless beers I owe J.Money for giving me a place to talk about personal finance where people don’t immediately just shut down mentally.

You’re welcome :)

“Break down your goal into monthly (or per paycheck) mini-goals” is so important. It’s something we’re studying with Tip Yourself. Members that have more “realistic” savings goals are more highly engaged (Save more. More frequently) than members that set very large long term goals.

I’m also in the savings is harder camp. Too bad you didn’t include the option that I always choose and that I find people have the hardest time with: investing.

My money doesn’t sit in the bank long before it is either used to pay off loans or contributed to my IRA.

Great take on setting up mini goals – it helps make it more fun and enjoyable!

Damn, yes – good idea w/ the investing! Would have been much more telling than sneaking in “being awesome” haha… for some reason I find that the easiest above them all so maybe that’s why I psychologically omitted? I think the really hard part to figure out is *what to invest in* once you are ready to invest… So glad I came across index funds the other year, but for 30+ I was aiming in the dark!

We’re kind of late getting started, but I find saving right now is easier than paying down debt. I’m still attached to my credit cards even though I save about 38% of our net take home pay each month. I tend to use them out of convenience. Our savings is growing by leaps and bounds but I still have some credit card debt. We are retiring soon and my hope is to pay off all debt in one big swoop and consolidate and simplify our accounting. Right now sometimes I feel like I’m juggling too many balls in the air, between several savings accounts and my credit cards. No car loans or personal loans, just a very low interest mortgage payment. But I can see the reasoning to be completely debt free, just wish I’d started sooner.

You’re not alone in that one,believe me. Another idea is using cash to wipe them all away at once, and then auto xfering $ back into savings to fill it back up before you hit the button to retire? might give you a big motivational push right before entering the next phase? :)

We are debt free and mortgage free. I wouldn’t say it’s hard necessarily but it’s hard to make good choices sometimes to save money and not think, “Oh, I can blow some money because I’m not in debt” and spend money unnecessarily, say like going out to eat.

Definitely saving is harder. Debt weighs on you, wakes you up a night. It’s an emergency… you’d do anything to be rid of it. Once it is gone, saving becomes easier, but it’s hard to keep that sense of urgency that you get with paying off debt. That race to do as much as you can as quickly as you can. Which sucks because if you’re like me, you do wake up one day and think crap – if I had been saving like this all along I’d be a money god right now!

For me it was always harder to save but all that’s changed recently. We sold our home last month even though it was NOT on the market (offer too good to refuse) & are now temporarily renting (6 month lease). I’m amazed at how much we’re now saving! Just had a plumbing issue. Landlord paid $972 to fix it. The advantages of renting! It was nice having an old house but it was a money pit. Seemed almost every month there was some sort of emergency. Really enjoying the freedom of no mortgage, no upkeep & saving like crazy. Will probably buy a brand new home in a few months. No more old house money pits for us!

Credit card debt/loans were house related. Poof! All gone now that the house is sold.

NICE!!!

Did someone just walk up and make an offer to you off the street or something? Haha… I’ve seen that done in the movies but never in real life :)

My post today is actually all about owning vs renting:

https://budgetsaresexy.com/2016/08/questions-ask-before-buy-house/

I’m having trouble working on paying off the mortgage. Though it is debt and I don’t like debt, the rate is so low…Savings is easier for me when I track the net worth each month and see the progress. Progress is motivating. And you’re right, having a set goals is so important!

I can see that. Especially when the amounts are pretty big too. I’m always needing those small wins under my belt to keep things exciting :)

Quite the conundrum for a Friday, J. While reading, my prevailing thought was “Different strokes for different folks.” Not too profound, but we’re all different, and our inclinations and feelings can change over time.

Six months ago, I was enraged by my student loan debt and found it very easy to pay off almost $18,000 in 54 days. Today, I’m sitting on a super small car loan and finding it really hard to find the motivation to just kill the stupid thing and be done with it.

The psychological components of how we handle money are fascinating like that.

Rage will do that to you! haha…

Honestly, I think both are hard. Of course, having debt is a pain in the ass; however, saving money for something in the future isn’t exactly a walk in the park either. It’s stressful knowing you don’t have enough in savings in the event of a major emergency and it’s stressful knowing you have an $80,000 student loan gorilla hanging around your neck too. However, training for marathons are not easy and slow and steady wins the race. Right now it’s a delicate balancing act of the two until I’m where I need to be financially.

Saving money…I am terrible at paying myself first and sticking to it. It has gotten easier now that the kids are out of the house and my income is mine for the most part. I can cut back on myself easier than it was cutting back on the kids “wants”.

I found paying off debt was much harder. It took over a decade to do so. I would make progress and then charge again. I would tell myself, “Well, I still have $XXXX left of this card, what are these $XX shoes really gonna hurt?” This made the process so much longer than it needed to be. However, once I was debt free I realized I had all this money that was going towards debt available to save. And it was a large sum. I got addicted to seeing that number in my savings account grow and grow. It has been about 6 years since I have been debt free (cars, and all…) and I still try to save as much as I can. I’m hooked on savings…

Good!!! Sounds like you’ve really turned things around!

I’m guilty of always changing my mind on what I’m saving for. I’m glad to say I did manage to save for three years for my “quit my job” fund, and now I’m self employed! Yay!

Bad ass!!

For me its easy, do what the wife wants. In reality, she is one of those people that looks at debt as voluntarily putting on a strait jacket and the banks get to decide when you can take it off. So we prioritize debt reduction. We really got serious in 2014 and now can see an end on the horizon. 66 more house payments. Less time than many car loans these days!

One of the things that made it simpler for me is focusing on a small detail, I call it my magic number. $310. That is the number (rounded up to next $1) at which the extra principle payment reduces my monthly interest by one dollar. It is great to know that by paying that extra amount all my future payments will include $1 more principle, and $1 less interest. It’s a benefit I can see on paper. I can also see the compounded effects of making those extra payments over the years. It soothes the number crunching addiction I have.

For the visual reminder, we use a picture of Walter’s Wiggles on the Angel’s Landing Trail in Zion National Park. Every few payments results in another marker placed on the trail. When the markers reach the top, the mortgage will be gone!!

Once the mortgage is gone will add to the retirement and savings accounts. They are not totally ignored right now, but they are not the main focus.

Cheers

Thank you, Richard, for sharing your method for paying down your mortgage. Very interesting formula! I’ll have to remember that later when we buy another home.

YES! SO COOL!! I remember mine going down by $1.00 every now and then too, but never tried figuring out how much it took *every month* to get it that way. Love that thinking!

I absolutely need concrete goals! Beings I’m not sure how much more we really “need” to save for retirement (which provide NO motivation), I am starting a new savings goal. With a visible, tangible goal I think after our year off, I will be fired up to start saving again!

Saving!

I’ve been debt free since the end of 2011 and have never been able to reach the 10k mark in my emergency fund. Still debt free but there’s always something and next thing I know I’m back down to 1-2 months expenses.

I make more money now than I did when paying off $48,000 in debt but there’s some kind of disconnect. Which is why I finally started my retirement savings even though it goes against the Dave Ramsey rules of following his steps exactly.

This past week I’ve started wondering if I need to stop looking for a magical number and just set mini goals.

Maybe as long as I’m showing progress each month that can be considered a win?

I would say so! You could do $1,000 mini-goals :) Hit $1,000 more in savings, then give yourself a month or two off, and then go again hard until you hit the next $1,000, etc. No way NOT to hit $10k w/ that route, and hopefully it would keep your motivation too! I want a report a year from now, please :)

It’s paying off debt because you’re in a tight situation and the emotional feeling is harder, and sometimes or always it’s hard to see how to get out of debt.

2182 articles, you’ve come such a long way ;) I never considered the two alternatives, having a lot of money with matching debt or having no money and no debt. I hate playing on leverage and am scared to play on leverage so I think I would choose the latter even if I have no debt. Having small wins throughout to conquer the big wins is so important!

“Don’t just save to save”– I think this is great advice (and probably why a lot of people don’t save like they should. Just as anything else in life, planning and having goals is the best way to accomplish something.

Interesting question about whether to have debt and cash, or neither. I’m certain I’d opt for the debt and cash. I’d have to say I find paying off debt harder than saving. Unless you’re paying it down with a snowball, it just seems to go on forever. Saving, on the other hand, if you are consistent, happily increases each month. Some health issues resulted in debt for me that I’m still paying down. Now that I’m in a position to attack it aggressively it isn’t hard, but I’d definitely find it easier to save.

Thanks for sharing, Sherrie :) Hope your health is now getting better along w/ your wallet!

Perspectives and situations can shift this mindset for sure. Right now, paying off debt seems harder. Even though there is a clear end result (being debt-free! woohoo!) as opposed to saving, paying off debt feels harder because it seems I’m always making payments, putting more toward it, and yet being debt-free still feels so far away.

Even when I was debt-free and unsure of strategically going about saving, I still thought paying off debt was harder. For some reason I really like making a game (and reaching each “level”!) out of saving money.

Gamifying it is always good! All about figuring out how you work the *best*, and then maximizing it.

Documenting either saving or paying down debt is definitely a great trick. Very rewarding to see the progress.

I say paying down debt is harder. It’s more fun to hoard cash!

This is a hard one! I am actually struggling with this right now and sort of wrote about it on my blog. I have some savings built up and that feels awesome but I also have a car loan and student loans that I would love to pay off. For some reason the idea of putting more towards debt over saving bothers me. I can’t put my finger on it. Logically I know paying off the debt sooner would save me money in interest and the sooner I pay it off the sooner I can save more. I think having money in the bank just makes me feel more secure.

No shame in that! Having extra cash def. gives you options and keeps you away from getting into MORE debt – so that’s good! Maybe once you hit a certain threshold you’ll be more comfortable putting future amounts into debt? Like, once you hit X months of living expenses?

I think that unless you have the savings earmarked for a particular purpose, that saving money is much harder. It’s too intangible to save “just because” or for some distant FI goal. Much easier to spend it on an awesome concert or something tangible, right?

Paying down debt has a clear, direct, and measurable benefit that you can see. You see your credit balance going down and you see the interest payments getting lower, a direct and satisfying correlation.

That being said, I haven’t had anything but mortgage debt in a while, so I’m working from memory!

This is a fascinating scientific study, J. I think paying off debt is harder than saving, but I think that is because my debts are so large. Maybe I’ll feel differently once I’ve settled the debt once and for all.

I love saving! Maybe that comes from being fortunate enough to never have had debt (until recently — new mortgage!). Now I’m struggling with having the option to emphasize one or the other. I feel like I equally want to invest more and pay down my mortgage quickly, so I think I’ll throw money at them equally for now. I need to stop stressing about it — both will make me better off. Once I come to terms with that I can have well-planned peace :)

Indeed :) My opinion is that as long as your net worth is going UP it doesn’t really matter which option you choose. Although the ones that *excite* you the most will always be more motivating.