Last September I got the following note from a reader of the blog:

Hi J$,

Not sure if you caught some interesting news, but Vanguard’s rival Fidelity has introduced two ZERO expense ratio funds – one domestic and one international. Interesting maneuver to try and compete with Vanguard and ride the indexing wave:

Thoughts? I’m a die-hard Vanguard guy, but at 28 years old, the opportunity to shave costs over decades is appealing…

I told him it was SUPER intriguing, but like most things that try getting in the way of my already-locked-in-plans, I tend to ignore them until I actually can’t anymore ;) Similar to how I got into Vanguard to begin with – I finally couldn’t resist the logic from everyone!!

I told him to keep me updated over the months though – especially if he ends up making the switch – and then just yesterday I heard back from him again, offering to share his current insight in the form of a guest post.

So that’s what you’ll see now below – a little analysis from our friend here to help us all be better about keeping an open mind ;) And to avoid having rotten tomatoes thrown his way, he’s opted to remain anonymous, haha…

Take it away, Mr. Anonymous!

******

Let’s talk expense ratios and question conventional index investing for a moment. It’s important to do this sort of thing, especially when it becomes easy to get lulled into the belief that one product has always been and will always be the way to go, a la Vanguard for index fanatics. The “challenge everything” mindset is a must.

As a faithful follower of the indexing movement, I agree with and submit to all its fundamental assumptions and acknowledgements – passively mirror the market, avoid paying someone to mange your money (only to screw it up), understand that being “average” year after year actually puts you well above average over time, etc.

So, Vanguard it was.

My dad invests with them, and at the early age he got me started, of course I followed his suggestion. He gave me the autonomy to pick the investments I wanted, but they were going to be under Vanguard’s roof, no question.

With time and learning, I became fully committed to the indexing ways. I’ve now moved all my invested money to indexes and am 100% stocks. Why all stocks? Among other reasons, I read the Jim Collins article on Investing for Seven Generations and understood the point.

This money I invest is here to support all my wants and needs throughout my lifetime, yes, but it can and should be about so SO much more than that. It’s for generations of family I will never meet. So I increasingly look long-term – like, really long-term – and can easily subscribe to the idea of being 100% stocks, perhaps for the entirety of my life.

With a general philosophy now adopted, it’s tempting to become complacent. I’ve picked my investment approach, established my risk tolerance, and selected funds that match it (VTSAX, VTIAX and that’s it). Now it’s time to simply cruise, let the automation occur, keep the faith, and not worry about it, right?

Nope, can’t do it. I like to remain engaged and always stay current. That usually doesn’t mean too much in the passive indexing world, but there’s something new on the horizon and I’m intrigued…

That shiny, new thing? Fidelity’s zero expense ratio funds. They caught my attention in September of last year, shortly after Fidelity rolled out four funds that all tout a “0.00%” under that all-important expense ratio listing.

As an indexer, I pay close attention to this, and I know Vanguard has dominated the field for quite some time. The greater investing audience has also paid attention, as report after report tell a story of more investors adopting the passive investing approach, leaving their active fund managers behind.

But Fidelity has pushed the envelope. They didn’t go the Vanguard route and drop ERs by 0.01, as Vanguard’s been known to do periodically. No, Fidelity created four new funds and told investors “invest your money here and pay nothing”.

I was understandably skeptical at first. This went against what I’d known for quite some time and felt the need to keep my distance. So I did. I monitored the two funds I cared about most – FZROX and FZILX – and waited for something to change. Certainly, the funds wouldn’t remain at 0.00, I thought. There must be a point in the not-too-distant future when they’d quietly raise the ERs in the middle of the night. If not that, perhaps Fidelity’s funds couldn’t track their indexes as well as Vanguard, and the returns would be sub-par when compared to the market.

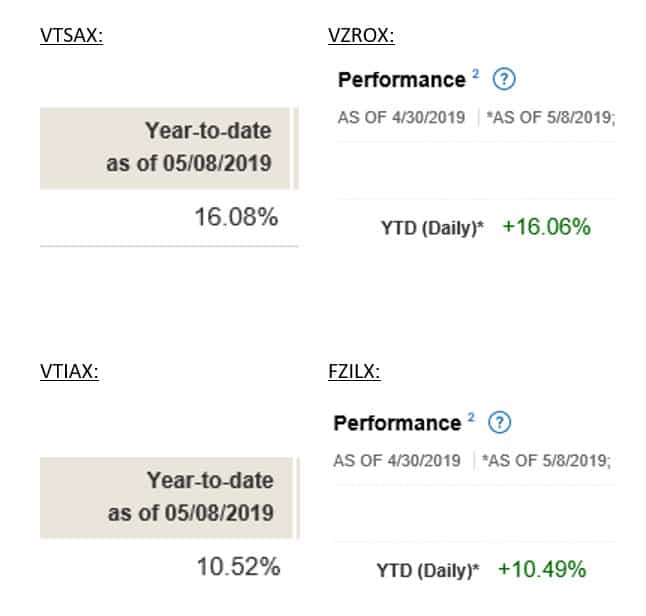

Those were my main concerns, and neither of them happened. The fund is still at an ER of 0.00 and the funds still track their index (and Vanguard’s matching funds) extremely well. See below:

By my assessments – and they may not be entirely comprehensive – the Fidelity funds check out. Now comes the “does it really matter” part. Am I really saving money by seeking a miniscule reduction in ERs? Based on what’s current on Vanguard’s page, investors pay an ER of 0.04% for VTSAX and 0.11% for VTIAX. Great, low rates by all accords, except now there’s something lower.

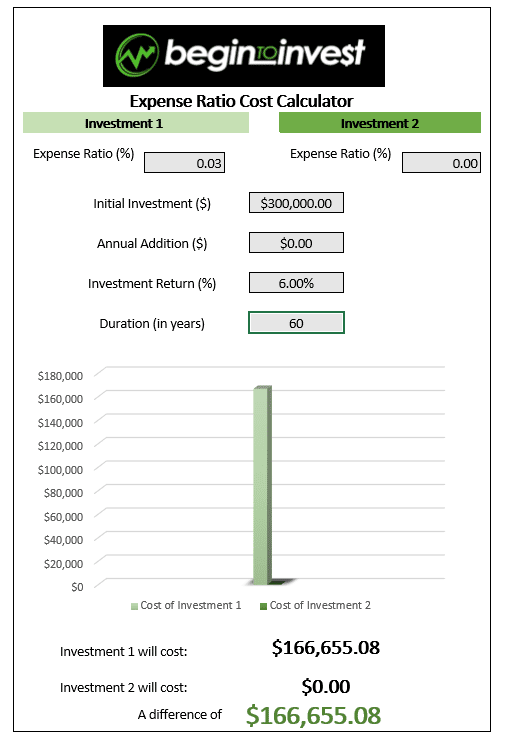

Time to bring in the expense ratio calculator.

A simple calculator I found is listed below. First, it’s important to tackle a couple of assumptions here:

- The money that I’m evaluating is what I have invested in a taxable account, meaning I can move it anywhere, anytime with no limitations. My choices are not limited by the options offered through an employer’s 401k selections.

- Everything I entered would likely be considered conservative. I did this in order to prevent an exaggerated effect from the difference in ERs. I assumed returns of only 6%, I reported that I would not be contributing ANY money beyond the principal amount of $300k, and I took projections out 60 years (remember, I’m thinking seven generations here, not just my lifetime).

- I actually used 0.03 for the VTSAX ER, not its current listing of 0.04. This is because the matching ETF, VTI, is currently at 0.03 and I’m making a guess VTSAX will drop to match it before too long.

- I also have money invested in VTIAX, as mentioned above. VTIAX is at 0.11% currently, but I’m not even factoring that in. I’m only evaluating the VTI ER of 0.03 and being extra kind.

That big number in green at the bottom? That’s the $166k I’d be paying to Vanguard over the next 60 years, just to have them manage my $300k plus it’s 60-year growth. STAGGERING!

One might argue that $166k over 60 years isn’t a huge deal and that with inflation, it will be less impactful in the future than it seems now. All good points, but remember my assumptions and purpose.

In reality, I expect to make a greater return than 6%. Also, I will obviously be adding to this investment over the years, not just letting the principal compound. And finally, I want this money to be passed on well beyond my lifetime! With all those “new” assumptions applied, the costs to manage the funds go up “bigly”! The larger the value of the investment becomes, the more that ER drags on my returns.

So what sort of action should and will I take? That’s the big question here. I’ve been sitting idly by for more than six months and not taken any action yet (always a cardinal sin), so should I be compelled to act? Maybe. I’m monitoring for a few things.

The first is the cost of closing out the Vanguard accounts and realizing all the gains. Having been invested over the last 9 or so years, there’s been some powerful growth in the stock market, and the gains would be taxable. That would hurt and make for an ugly time next April 15th.

If the capital gains tax deters me, what I might do instead is monitor for any downturns in the market. They inevitably happen and would actually give me a perfect exist strategy from Vanguard with lesser or no gains to be taxed on. Admittedly, it would have to be a pretty significant downturn, but that’s a good problem to have.

My international funds, however, have grown a lot less than the US funds, so, I could withdraw just the international portion and move it to Fidelity, purchasing the 0.00% ER fund that targets the exact same index. It would cost a lot less in realized capital gains. Would that constitute a wash sale? Would I have to sit on the sidelines for 30 days before entering Fidelity’s international fund? Those are not rhetorical questions – maybe someone can help me answer that.

The second option to consider is remaining idle, although this relies on a big assumption/hope: believing that Vanguard will also drop its ER to zero. I hate relying on things out of my control, which is exactly what I’d be doing.

Nevertheless, there’s plenty of literature out there claiming that zero ERs is inevitably where it all goes. The articles argue that investment firms will ultimately bend to the will of investors who increasingly demand ultra-low cost funds and will leave if their demands are not met. I tend to believe it will eventually happen, but how long must I wait and how much in fees will I lose while waiting? Impossible to answer. This is the conundrum I’m left with.

For new investors, I’d say the answer is easy: if you believe in the indexing philosophy, invest with the firm that offers you the cheapest way in. Right now, that appears to be Fidelity. I hear there are other, smaller investment firms that also offer 0.00% funds, but I also feel the need to be part of a larger, more substantial institution.

Where to go from here largely depends on getting oneself off the sidelines…

******

So there you have it! What do you think?? Have you been tempted to move over too, or perhaps you’ve always been a fan of Fidelity but just kept quiet amongst our sea of Vanguard lovers?? :)

The part that stuck out to me was the fact that if the Vanguard funds are outperforming fidelity’s as it looks like in that comparison up top, even if by just a fraction, wouldn’t it come *closer* to breaking even in the end? Making the fee differences not as important?

I coincidentally came across another Vanguard vs Fidelity article while reading about this (albeit in a more “review” type format), and one of the comments someone left at the bottom brought up an interesting point:

“One of the reasons Fidelity is able to offer Zero fee funds is that its not actually tracking the total market index. Instead they created their own total market index and avoided the index free – which is charged to all index trackers. Now this could be very similar or it could not. Time will tell. But in the meantime, would you like to actually track the total market index or not? That’s the question that the Zero fund investors should answer.”

So it’s not exactly *apples to apples*, even though of course it’s certainly close. But that does explain why the performance is off by a fraction… (and a fraction, mind you, that goes on to become quite the difference in the long term which is the precise point of this post!)

I relayed this over to our friend, who was kind enough to continue the discussion…

******

Sure, solid points. It is true that “time will tell” whether the Fidelity zero-fee funds will actually mirror their intended indexes and deliver returns on par with Vanguards indexes. Nice points by Money Wizard too.

With the screenshots I provided (current as of May 8th), I think it showed Vanguard to be ahead of Fidelity by 0.02% to 0.03% thus far in 2019. If Vanguard’s VTSAX should take a “lead” of 0.04% over Fidelity’s FZROX or more by the end of 2019, then it is true that switching to the Fidelity funds would have created no benefit. However, the lead that Vanguard would have to create for the VTIAX fund would have to be greater though, as VTIAX is currently costing 0.11% annually, while Fidelity’s matching fund is also 0.00%.

Vanguard themselves actually offer a cool “fund cost” calculator at https://personal.vanguard.com/us/funds/tools/costcompare. Using this, they introduce two different “costs” that an investor absorbs when paying a higher fee than needed.

- First is the incurred fee, which Vanguard describes as “the cumulative fees, expenses, and other charges associated with buying and maintaining shares”. That is super straight-forward and easy to process.

- Second are the opportunity costs, which represent “the compounded return you lose because you’d be diverting investment assets to pay fund costs instead of buying additional shares”. This gets at the lost “re-purchasing” power from losing 0.xx% to fees, which could otherwise be going towards buying up more of the fund through dividends. It does operate on the assumption that an investor chooses to have dividends reinvested, not paid out to them.

Finally, if it’s possible that Fidelity’s funds will slightly underperform Vanguard’s because they aren’t following the exact index (and are thus avoiding that small fee to do so), then I see that it’s also possible that Fidelity could slightly outperform Vanguard’s indexes.

There’s no secret “formula” to mirroring the index, so Fidelity can and hopefully did do their homework is studying exactly what a Vanguard fund like VTSAX invests in and tweaking it just enough so that they avoid paying the index-tracking fee, but are comprised of an equally large and equally diverse number of companies.

It comes down to a bit of what can I vs. can’t I control. I can control the fees I pay, but I can’t control the returns experienced over time.

Just my two cents.

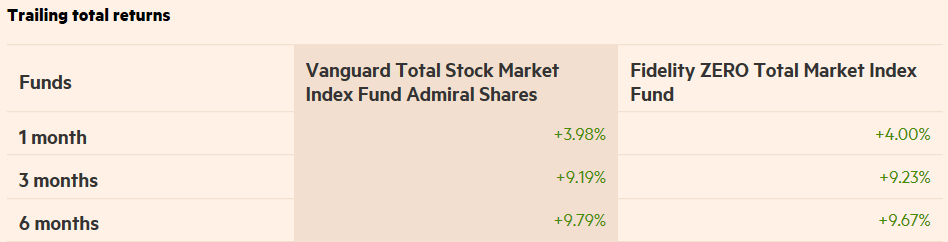

One last illustration. This graphic below compares VTSAX and FZROX over the last six months (FZROX has only been around since August 2018) and it shows that at 1, 3, and 6 month periods, the funds have shuffled in terms of who’s generated better returns. VTSAX wins the six month battle, but if you wanted to withdraw your money at 1 or 3 months, Fidelity would’ve been the better option.

******

And that’s the end of this post for real ;)

Thoughts??

——-

UPDATE: Here’s another great article around this stuff from White Coat Investor: Don’t Obsess About Expense Ratios (thanks for the tip, Andy!)

UPDATE II: Got a note from our author here with a follow up:

Hey J,

Thought I’d follow up several weeks later.

I made a move to swap one of my Vanguard funds for a Fidelity ZERO fund. Specifically, I sold VTIAX (total international index) and bought FZILX (Fidelity’s same fund).

Couple reasons for this:

- The savings in ERs is greatest here (going from 0.11 to 0.00)

- I was essentially at zero profits or losses, so next to no incurred capital losses or gains (unclear if I could claim losses on this due to wash sale rules anyway)

- Good way to get my toes wet without a full commitment

Thought I’d share in case anyone was interested.

UPDATE III: Another update from our experimenter :)

Hey Buddy, I thought I’d do an end-of-summer check on the performance of Fidelity’s no-fee funds vs the Vanguard funds, just to see how the ongoing experiment is playing out. Below is what’s current as of yesterday’s market close. The domestic funds remain in a fairly close tie, but the Fidelity international fund seems to have pushed towards a bigger lead. Interesting stuff I’d say.

Get blog posts automatically emailed to you!

I moved everything to Vanguard and have invested it all in VTSAX based on your recommendation. It has worked out well for me. I’m not moving to Fidelity just yet. I’d like to see how they perform over a few years compared to Vanguard first.

Rock on man – glad it’s been working out for you so far!

TINSTAAFL

(There is no such thing as a free lunch)

It cost Fidelity something to maintain these index funds. Even if the entire thing is automated there are still costs here, administrative, maybe regulatory, etc. Maybe it’s a tiny fraction but much like how you show the possible savings over Vanguard in the long term, those costs are going to add up in the long term too.

So how are they covering those costs? The obvious play here is that this is like any other freemium offer on the web, and they hope to upsell you on other Fidelity products and services. However, given these funds obvious appeal to the kind of people that hang out here, that seems like a bad business model :)

I think they eventually have to add a fee, or they shut them down.

My guess is that the marketing they’ve already gotten from it has already more than paid for itself, haha, but no way Vanguard is getting dethroned without a good fight :) So it probably will mean all us loyalists will see even cheaper – or ZERO – fees down the road too to better compete! So bring it on!

I’m interested to see how this unfolds.

We invest with Charles Schwab—blasphemy, I know—which has similar expense ratios. I Will Teach You to Be Rich was the first personal finance book I read, and Ramit recommended their checking account, so we opened one. The brokerage account came with it. I’m not concerned with optimizing every dollar, so we’ll probably stick it out there. My 401(k) is with Fidelity, but I haven’t seen these funds offered.

100% agree that you don’t need to maximize every last dollar unless it turns you on, haha… if something’s working for you – and you’re happy about it – great! Keep going until it no longer makes sense! Lots more to this stuff than pure numbers…

I can’t help but think that the expense ratio calculation is **very** misleading. Look at the assumptions: An initial investment of $300K that gets invested for 60 years. Is that a reality-based scenario? Assuming you live to be 80, that would require you have $300,000 to invest when you are 20 years old. Very few people have that sort of money. A more realistic scenario might be investing $150K for 30 years – which would be like having $150K saved up when you are 40 or 50. Using these numbers, you only save $7,285 with the no cost fund. That’s a huge difference compared to the $167K the author is touting.

True, but he’s also basing it on his *own* situation and strategy, much like I do here, so it is accurate to him :) But I see your general point here, and makes it a LOT less tempting when put that way too, haha… Which I also appreciate – so thanks for adding it!

When I dove deep into this (thanks for the shout out, by the way!) the thing that stuck out more than anything was the tax efficiency. Vanguard’s funds have been so much more tax efficient that they completely wipe out the expense ratio savings of Fidelity.

Quick math to show how much the added taxes skew the “true” expense ratio of Fidelity’s Zero funds. The Zero funds distributed $0.32 per share of capital gains last year. (Vanguard distributed $0 since 2000.) Say you have $10K to invest, and the average share price was $70 last year. You’d own 142.86 shares, meaning you’d receive $45.71 of capital gains distributions. All else being equal, you’d owe taxes on those distributions at your capital gains tax rate (15% for most people) That’s $6.86 of capital gains taxes owed. Relative to your $10K investment, that’s 0.068%…

In other words, Fidelity’s “true expense ratio” is about 0.07% compared to Vanguard’s 0.04%.

Granted, this advantage might go away in a few years when Vanguard’s tax efficiency patent runs out. But for now, it’s the biggest reason I’m staying with Vanguard.

Correction – Fidelity’s Total Market Index Fund (not the zero funds) distributed $0.32 per share. The Zero funds didn’t have a track record when I wrote the article, but I haven’t seen anything that indicates the capital gains distribution would be noticeably less. If anything, I’d guess they’d be a little higher because the funds are younger and therefor can’t carryover losses as well.

Well that’s something to consider! Haven’t heard much about that before, thanks man… You’re on a record showing up on my blog here this week :)

I don’t recall where but I saw a similar analysis at a financial site comparing these two with the same conclusion: including tax, vanguard has the lower cost.

I appreciate what Fidelity is trying to do. My company is migrating from Voya to Fidelity for 401k needs and honestly I’m kind of psyched about it. But I ain’t about to rush out with my own accounts and snap that up, for the same reason I bank with a credit union rather than some megabank: I appreciate Vanguard’s business model. They’re essentially a co-op brokerage. They answer to their clients rather than to their shareholders (or to what the board thinks the shareholders want, or what the C-suite thinks the board wants).

Even if it’s the lesser of two evils, that counts for something to me… and so it’s where I take my business.

Love the insight man, thank you.

We had a 401(k) that we set up through Vanguard. Circumstances changed, and we wanted to move it to a Self DIrected Solo 401(k). The process to withdraw funds from Vanguard was HORRIBLE!

The person who was assigned to assist me when I was DEPOSITING my mid 6-figure funds had left, with no one to replace her.

I spoke to SO MANY people, none of whom could give me a straight answer. I filled out MULTIPLE forms and Fedexed them in, only to hear that it was the wrong form, the wrong notary. One time they LOST my documents! With my personal information on them!

So while Vanguard has done a lot for a lot of people, their customer service is complete dogsh*t.

The kicker is that we were going to withdraw from one account, create a new one and put the money right back into that account. With Vanguard!

The whole experience left a bad taste in my mouth for Vanguard.

Damn!!! Can’t even give them money- that’s wild!! And really disturbing to see, I’m sorry friend :( Really glad you shared that here though as we’re totally guilty of just loving on them all day in this community…

I wouldn’t do it if I have to pay capital gain tax. It’s a huge drag. That’s not a wash sale and it wouldn’t matter anyway unless the found lost money.

The zero fee wouldn’t make up for that, IMO.

I have a Fidelity retirement that is ‘stuck’ (I started as an emergency hire for the state and as such you don’t contribute to CalPers yet, only permanent employees can) and has been sitting for about 19 years! lol However beginning this year I have also opened up a Roth IRA to roll the 2% points from my Fidelity Visa. I am a newbie at learning all this and trying to absorb as much info as possible.

I know most on this blog are Vanguard folks, do you know of any blogs that are Fidelity folks? lol I am not interested in switching over, especially since I love the Fidelity Visa, and would like to learn more on that side.

Thanks!

I don’t know of any personally, but I’m sure you’ll start seeing them pop up over time if this ZERO fund stuff keeps getting the press that they are :) But at least most of our love is focused on *indexing* first and foremost, so most of the articles/tips/etc are still aligned the same way… (now if you hate indexing, well then you’re in trouble haha… j/k… there’s lots of awesome stock-picking blogs too, especially around dividend investing :))

I think there is a greater point that’s being missed with these zero expense funds. A few basis points in fees over your portfolio’s lifetime does add up, but even if these new zero funds weren’t “zero” and charged a few bps, I’d still buy them for another reason.

These are designed as loss leaders, obviously to get you to invest w/Fidelity so that over time you’ll migrate to their fee based services and/or other proprietary products. These funds are only available to individual investors at Fidelity and not advisors, and you can’t acat them to another firm either.

As long as you’re ok with those caveats, the tax-inefficiency of a mutual fund vs. etf, and you don’t use Fidelity’s more expensive services or products (exactly what Fidelity doesn’t want you doing!) you are getting a proven strategy at a huge discount to current nav/market price.

Fidelity contracted w/Dow Jones to create the indexes for these funds and didn’t actually create the indexes itself. Their 500 index is nearly identical to the S&P 500 with some sampling differences and about a $10 billion difference in market cap. It’s like when Mazda used to take Ford Escapes and rebrand them as the Tribute (when Ford had a stake in Mazda) – same car, different name. Fidelity went to the S&P provider itself and pays for a cheaper generic version of virtually the same index, with some minor tweaks so Fidelity doesn’t run into any proprietary issues w/Dow Jones.

My point in this long rambling – buying the Fidelity 500 zero fund is like finally being allowed to buy a proven drug at a much cheaper generic price once it goes off-patent. The merits of index-investing now have decades of statistics as a proven, effective way to invest. But when VFINX started trading, it was new and unproven. So instead of having to pay over $200 per share/NAV for SPY, IVV, VOO, or VFINX, you can basically get the same strategy for about $10 NAV with this fund. We don’t know what the S&P will do in the future, how the market will perform, or how Fidelity’s generic 500 index will perform vs the actual S&P 500, but the merits of passive investing are now proven – why pay more for it however when you can get it cheaper?

Very good insight – thank you!! Never knew any of this stuff before today!

What is the major differnece btw VTIAX and VFIAX?

And, does VDADX worth of .08% fee?

VTIAX and VFIAX are both the same, just one with lower fees due to the higher minimum investment of $3,000 (VFIAX) vs the other one which is now actually closed to new investors (VFINX)

Don’t know much about VDADX…

Your retirement portfolio size is not determined by expense ratio, it is determined by investment return. The comparisons you do in the article are net of expense ratio – so if you’re worried about 4bp of ER vs the competition, you should definitely be giving strong consideration to 2BP of improved return versus the competition.

THAT SAID, once your ER is under the tracking error, it’s almost impossible to make a strong argument from fundamentals. The ER will tend to shift the graph ALL ELSE BEING EQUAL, but all else is seldom equal. Next year it could be -2BP, or 4BP, who knows? There are books out there such as “Active Index Investing” which go into great detail on the management of these indexes – basically, talented managers can eke out a few BP over the benchmark simply by being really really good at managing their securities. But I can’t think of any way to test for that short of letting them play out in real time and looking at the results.

I’m not saying that Fidelity is doing anything wrong or dodgy, in fact I think it is awesome that Fidelity and Schwab and others are doing this, it puts pressure on Vanguard to up their game even more. But I am saying that Vanguard has a long record of doing great things in this area, longer than I have left until retirement, and at this point whenever someone comes out with a product to out-Vanguard Vanguard, my first question is “How are they managing this?” Vanguard’s structure of being owned by the funds it manages means they have a lot of incentive to keep things tight, and it makes it hard to see how a for-profit company can substantially beat them at their own game (Vanguard could just copy what they’re doing and _not_ profit from it). They aren’t perfect, they’re pretty conservative about what they’ll do, so you can certainly beat them by simply playing a different game, I’m just saying it’s hard to see how someone can beat VTSAX while duplicating it, without cutting corners or playing tricks with order flow or simply subsidizing things, none of which makes me happy for a position I plan to sit on for 30 or 40 years.

Thanks for adding to the convo, Scott!

Thanks for posting this response. This confirms what I was thinking. If the returns are almost equal, and they’re reported net expenses, then the ER doesn’t really matter when comparing the returns. Add to that the tax efficiency built into Vanguard funds (https://www.bloomberg.com/graphics/2019-vanguard-mutual-fund-tax-dodge/) and that Vanguard is owned by the mutual fund owners and not outside shareholders, I feel like gap closes and becomes more heavily weighted in Vanguard’s favor. Or at least I certainly hope so because I just moved all of our stuff to Vanguard. :-)

I moved my stuff to Fidelity several years ago when I was finally getting around to consolidating tiny retirement accounts from two previous employers and creating a SEP to go along with my then new, since shuttered, business. As such, I was thrilled when these el cheapo funds showed up. It is such a royal PITA to move from one place to another, I’ve never seriously considered moving to Vanguard, PF blogosphere fans notwithstanding. Glad this all floats someone’s boat, but I’m just not at that level yet!

I agree it’s nice having everything condensed and under one roof!! No shame in sticking to that since they’re obviously still great funds :)

Why are the only options of his to stay or go? What if he just opened a new Fidelity account and started funding that, then leave the Vanguard to grow and compound without any further investments? You would have 2 accounts that would both gain the same, but might cut a good bit of the fees you would pay. Seems like a good compromise. Unless I’m calculating that wrong – I’m not very familiar with investments yet.

I was thinking the same thing, Ashley. One could open a small $1000 account with Vanguard & $1000 with Fidelity (or whatever the minimum investment is required) & compare them after a year.

Yup! Another great option!! And would make for some even better side-by-side comparisons too since it’s all in real time :) Though would probably need to do it for more than just a year to really get a good sense (maybe 5 years? And if it all goes to $hit at any point xfer it out?! Haha…)

I’m surprised nobody has said this yet. Everyone is overlooking one big assumption – that is that the money will be invested for 60 years. Vanguard, Fidelity, and Charles Schwab are all in a race to the bottom with their index funds. In those coming 60 years, Vanguard will certainly do something to match Fidelity, or even outdo them, and definitely sooner than later.

These big 3 lower their index fund fees every couple or few years to try to beat the others. In that time, the “extra” that one would pay for holding onto Vanguard vs. Fidelity is well within statistical noise.

And speaking of noise, that’s all this is. It’s just the latest “shiny new thing”. If you’re with Fidelity, stick with Fidelity. If you’re with Vanguard, stick with Vanguard. If you’re with Charles Schwab, stick with Charles Schwab. You’ll do just fine in the long run. Now start squabbling over a few basis points, and go enjoy some time with your family. :p

Hahaha… But where’s the nerdy fun in that?? ;)

You’re missing two important points here:

1) vanguard’s fund performs better even after accounting for fees (right now it looks like 0.02% better), so you’d end up with more money in vanguard

2) vanguard has a parent on mutual fund tax efficiency which means their after-tax returns for your scenario are going to be about 0.2%+ higher per year.

I didn’t know about that patent! That’s pretty cool!

Vanguard has a patent for tax efficiency but when will that run out? Are the other companies holding out until that happens so Fidelity is just banking on getting new customers with their zero fee funds? I agree if people are worried about switching a ton of money from vanguard to fidelity zero fee funds because of tax implications, then just keep your vanguard account and start a new account with new money in fidelity zero and see how that goes?

I hope someone DOES do that last one and then blogs or shares it somewhere so we can all see… That would be a cool experiment over the years (and fairly simple to pull off!)

Please keep in mind that the index that’s followed REALLY matters. By using their own index, Fidelity is able to manipulate the fund in small ways to make money off the investors. See this article: https://seekingalpha.com/article/4251694-hidden-etf-transaction-costs-make-billions-market-makers

Also, I want to reiterate a previous comment that Vanguard’s patent to shield funds from putting off ongoing capital gains will save you much more than the difference in expense ratios.

Leave your money in Vanguard!

Regarding your question on wash sales… The wash sale rules only apply to losses, not gains. Therefore if you sell at a gain, the wash sale rules would not apply.

One thing not mentioned here is some of the no fee funds are loaning out shares to large hedge funds to cover short positions in their funds. I’d check this out before buying in. There’s no free lunch. I’m sticking with VTSAX.

In the meantime, you could at least do a non-taxable conversion to the equivalent Vanguard ETFs, shaving .01 and .02

> Vanguard has a patent for tax efficiency but when will that run out?

Somewhere around 2023 ish.

However it’s worth noting that the patent structure requires the mutual fund to have a ETF share class underneath, and Fidelity doesn’t offer its own ETFs right now. So even when the patent expires, fidelity will have to do some leg work if they want to implement it. No guarantee that they will.

The real difference between 0.03% and 0% over 60 years is zero.

Your real concerns are how effectively Vanguard and Fidelity manage the running of the index during that period, despite appearances, it’s not that simple.

The job of managing the small details is huge, tracking error is everything and will dwarf .03%.

I looked very carefully at a number of ETFs tracking Canadian stocks, available to European investors, the most expensive provider, iShares was significantly better over a five year period than other providers charging 10 to15 base points less. I’m sure Fidelity will be efficient but Vanguard really have some experience and run a lean machine…

I moved to the Fidelity Zero funds the day they opened. No regrets.

I’m missing something here, isn’t mutual fund performance reported net of the expense ratio?

https://www.investopedia.com/ask/answers/07/mutual_fund_cost.asp

If so, I think this clears it up for me without any unnecessary math.

oh wow, that is interesting?! I don’t know the answer myself (nor really ever thought about it), but from that article it seems like you’re right?

https://mutualfunds.com/education/mutual-funds-and-security-lending/

“Mutual fund sponsor Vanguard gives 100% of its fees generated from securities lending back to its shareholders. This is one of the main reasons why Vanguard is able to offer rock-bottom expense ratios. In some cases, fees from securities lending pays for virtually all of the mutual fund’s operating costs.”

Vanguard also has a patent on tax efficiency in it’s mutual funds. The Fidelity zero funds also distribute capital gains with their dividends which creates more taxes in the long run. Vanguard only distributes dividends which results in less taxes owed or even better with mostly qualified dividends.

In my opinion it’s a mirage from Fidelity. I’m sticking with Vanguard. JLCollins would agree with me. His comments at the end of the article.

https://jlcollinsnh.com/2018/09/25/what-we-own-and-why-we-own-it-2018/

It def. makes me feel better reading all this, haha… Thx ;)

I’ve been calling these zero-fee Fidelity funds “F-ZERO” funds. I think it sounds cooler, and hints at a bit of nostalgia for me, as well.

I currently have my Roth IRA with Vanguard (along with a solo 401k), but my HSA is with Fidelity. I have most of my HSA funds in the domestic F-ZERO fund, with a small amount in cash to pay for more expensive medical stuff (aka upcoming baby). My regular 401k is with Fidelity as well, but the options don’t include any F-ZERO funds.

Has anyone mentioned DIVIDENDS ? Vanguard is distributing them quarterly in vtsax vs only once annually at the end of the year for fzrox. https://www.personalfinanceclub.com/fzrox-vs-vtsax-the-hidden-cost-of-fidelitys-zero-fee-index-funds/