[Hey guys! Have a feisty one for you today from fellow blogger ERN at EarlyRetirementNow.com. Some of these you may disagree with, as do I (no emergency fund? Blasphemy! ;)) BUT I always love hearing other peoples’ perspectives, and Ern here can surely put up a convincing fight. Regardless of where you stand though, I hope you’ll find some takeaways here to help you in your own journey.]

******

As members of the FIRE (Financial Independence, Retire Early) community, we are all nonconformist. We scoff at conspicuous consumption of our neighbors in their full-size SUVs and McMansions, and instead budget with a very sharp pencil (spreadsheets are fine, too) and grow our stealth wealth, one dollar at a time.

But the FIRE community is far from monolithic. For example, I consider myself nonconformist even inside our nonconformist movement! I hold some pretty strong non-consensus views on many financial topics. I’m a rebel among the rebels, imagine that!

Here’s a list of my seven favorite disagreements with the personal finance consensus:

#1: The 4% Safe Withdrawal Rate is safe! (No it is not)

The Trinity Study and the resulting 4% recommended safe withdrawal rate have become the gold standard when designing a savings target (25x annual spending) and the eventual withdrawal strategy. Even J$ here uses it. There are (at least) two problems when extrapolating the Trinity calculations to the early retirement community.

First, instead of a 30-year horizon in the Trinity Study, the average early retiree faces a 50-60 year horizon. That wouldn’t be a problem if the success criterion in the Trinity had been capital preservation, i.e., preserving the purchasing power of the initial portfolio value for 30 years. If your capital lasts for 30 years, then why shouldn’t it last another 20-30 years? But for the Trinity Study, even a portfolio value $0.01 after 30 years is considered a success. That one cent will not last another 20-30 years!

To gauge how much of a “haircut” we should apply to the 30-year safe withdrawal rates when extending the retirement horizon, let’s do the following thought-experiment.

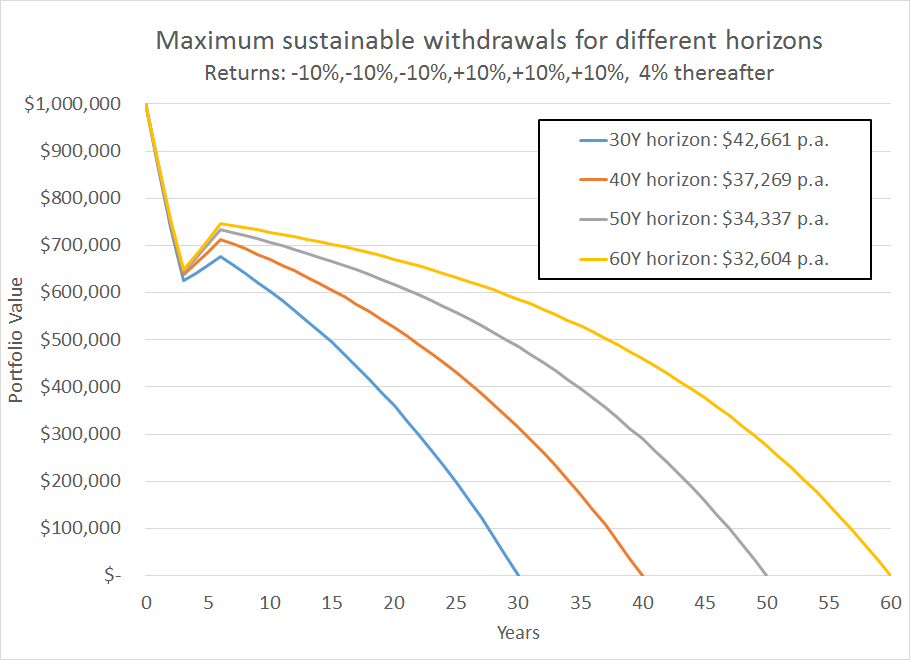

Imagine we have a $1m portfolio that generates 4% p.a. (per annum) of real return in the long-term, but we got unlucky and suffer 10% losses for the first three years, followed by three years of 10% gains and then 4% returns after that (assume all returns are real and all withdrawals adjusted for inflation). That’s not even a worst-case scenario, more of a garden-variety bear market.

Our portfolio can then sustain a withdrawal rate of about 4.27% p.a. for a 30-year horizon. But over longer horizons that number will be significantly lower: Only 3.26% over 60 years, a whole percentage point less and that’s all because of the longer horizon!

[Figure 1: Path of portfolio values over 30, 40, 50, and 60-year horizon with different withdrawal rates, targeting capital depletion.]

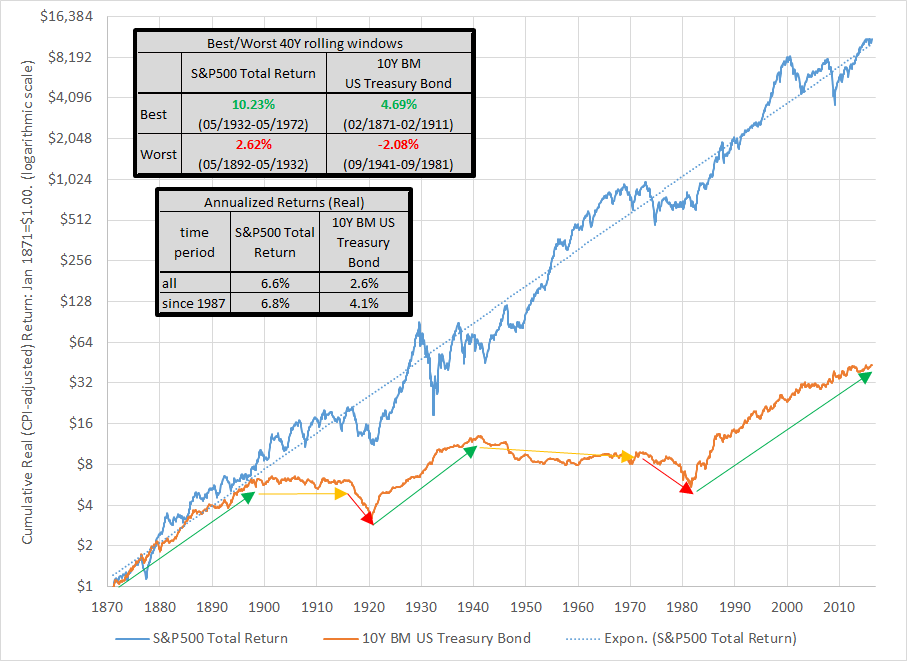

The second objection is that today’s expected asset returns are significantly lower than the average returns observed since 1926. The Trinity Study averages over many decades with different financial market regimes. Sometimes the stock market was overvalued, sometimes undervalued. Sometimes bond yields were very high, sometimes they were very low.

Does anybody else see a problem with that procedure? Relying on safe withdrawal rates that are averaged over the past 90 years is a little bit like calculating the probability of getting into a traffic jam by averaging over the entire 24 hours of the day. That may not be the most informative figure if you already know that you will be driving during rush hour!

For today’s retirees, only today’s market conditions matter, not the averages over the last 90 years. And more than seven years in the current economic expansion, equities look more expensive than over the last 90 years (measured by the CAPE ratio) as I show in this blog post. Bonds don’t look too hot either. Since 1926, the real, inflation-adjusted bond returns were solidly above 2% for government bonds, and even above 3% for corporate bonds, but today’s yields are far lower. Lower bond yields and expensive equity valuations support only significantly lower safe withdrawal rates than 4%.

If 4% doesn’t work, then what’s the alternative? Personally, I plan to start with a lower withdrawal rate of 3-3.25% out of our equity portfolio to account for today’s expensive valuations and the long retirement horizon. Having income-producing assets with a less than perfect equity correlation is also a good idea, so, I started moving some of my investments into rental real estate. Owning rental properties with a 4%+ rental yield (after all maintenance and repair costs!) I can probably push the overall withdrawal rate to 3.5%.

This number, though, is not set in stone. If the CAPE ratio were to drop to a more normal level, say, under 20 (currently around 27) I could move the withdrawal rate closer to 4% again.

#2: Robo-Advisers are great! (If by “great” you mean “expensive”)

You can’t read through the personal finance blog world without finding glowing endorsements of Robo-Advisers, like Betterment and Wealthfront. I beg to differ though, and recommend Robo-Advisers only to my most financially disinterested friends.

But folks in the FIRE community? We are the masters of budgeting and frugality, financial hackers (not hacks) and always on our toes to find new ways to eke out a basis point (0.01%) of return. Why would we want to throw away anywhere between 0.15% and 0.35% in fees p.a.?

Robo-Advisers do nothing magical and are nothing but expensive gimmicks. You can go to their website, find out their recommended asset allocation and simply implement it with inexpensive index funds at Vanguard or Fidelity. But do you even want to use their recommended asset allocation? You could do significantly better by further hacking their recommended allocation, for example moving ETFs with a high dividend yield and taxable bonds from taxable to tax-deferred accounts.

But what about tax loss harvesting? Tax loss harvesting is a neat tool that can lower your taxable income by up to $3,000 p.a., so folks in high tax brackets can save $1,000 or more on their annual tax bill. In taxable accounts, simply sell your underwater investments, i.e., equities, ETFs and mutual fund shares that have a cost basis greater than their current value, and the loss can be used to offset up to $3,000 of ordinary income per year. Check Bogleheads for more details.

Robo-Advisers can do this process really well and in a systematic and automated fashion. But apart from the fact that we find Tax Loss Harvesting overrated (see #7 below), it’s also something that most investors should be able to do themselves. Here’s my guide to becoming your own homebrew Robo-Adviser. Do it yourself and save thousands of dollars over the years!

Finally, under no circumstances should anybody ever shift an existing brokerage account with sizable capital gains to the Robo-Advisers, because they might first liquidate your holdings to purchase their recommended ETFs.

And that’s true whether you are an experienced financial hacker or complete finance novice. I’ve saved $42,000 by not switching to Betterment! The tax bill could be so excessive you’ll never recover the loss even under the most optimistic assumptions for harvesting future tax losses.

#3: Everyone Needs an Emergency Fund! (Not everyone)

The almost universally accepted wisdom is that not only do we all need an emergency fund, but building that emergency fund is the number one priority of personal finance, taking higher priority than saving for retirement. Some even want you to start an emergency fund before paying off high-interest credit card debt. That’s nuts!

I laid out our plan for having no emergency fund (featured on RockstarFinance on 5/25/2016!) and two follow-up posts as well to debunk some of the common arguments in favor of the emergency fund. With our savings rate of 60%+ we are usually able to finance all expected and unexpected expenses out of our current cash flow.

Just to be sure, I’m not saying that anyone should forego savings altogether. An emergency fund is better than having no savings at all. I merely take offense in keeping large amounts of money in unproductive, low-interest money market accounts. I consider our entire portfolio our emergency fund and like to put our hard-earned dollars where they can work harder for us: in equity and real estate investments.

Am I not afraid of having to dig into an equity portfolio right when the market is down? Yes, to a degree, but as a passive investor, I try to stay away from timing the market. Keeping cash on the sidelines for fear of a market decline exactly coinciding with a cash flow need is market timing on steroids!

#4: Use bonds to diversify equity risk. (Don’t get your hopes up too high!)

What was the correlation between an all-equity portfolio and a portfolio with 80% equities and 20% bonds over the last ten years? 0.998. For all practical purposes, that’s a correlation of one.

To be sure, the 80/20 portfolio has a lower volatility; pretty much exactly 20% lower. But that volatility reduction came from the lower equity weight and had little to do with bonds reducing risk. In fact, simply keeping the 20% in a money market account would have achieved that exact same volatility reduction. That said, bonds delivered very nice average returns over the last few years, so the appeal of an 80/20 stock/bond portfolio came mostly from better returns than investing 20% in a money market account.

But that could change in the future; yields have been heading higher since November 8th, and bonds could have a rocky road ahead of them. In addition to having little diversification, they could also lose their potential to boost returns.

#5: Bonds are safer than stocks. (Depends on the horizon!)

Of course, stocks tend to have higher daily, weekly, monthly, even annual volatility than most bonds. No discussion about that. So, for folks with a very short investment horizon stocks may seem unattractive. But over a 50-year investment horizon, we should weigh the short-term volatility with the long-term sustainability of funding our expenses in retirement.

There have been extended periods of very poor bond returns. For example, there was one 80-year window (!) of zero real (inflation adjusted) bond returns from about 1900 to 1982. True, equities can be volatile in the short-term. You see overreactions both on the upside (late 1990s) and downside (2009). But equities normally return to a long-term trend growth path within a few years, see chart below.

Bonds, on the other hand, can move sideways for many decades. That’s poison for the retiree who relies on a nest egg to last for half a century! And what’s worse, the spectacular run of good bond returns that started in 1982, might be overdue for a reversal as has happened with the other two bond bull markets in the late 1800s and 1920-1940. I’m not saying that this will start now, but bonds did get crushed after the spike in interest rates since November 8th!

[Figure 2: Which one is the risky asset now? Cumulative real total returns (CPI-Adjusted) of the S&P 500 and 10-year U.S. government bonds. January 1871- December 2015.]

So, to stay with our “financial rebel” theme, just like our American Founding Fathers preferred “dangerous liberty over peaceful servitude,” this writer likes dangerous equity volatility more than running out of money for sure with low volatility bonds!

#6: Cash serves as great bear market insurance in retirement. (Think again)

The idea sounds almost too good to be true: simply keep a few years’ worth of expenses in a money market account, enough to fund expenses during the occasional bear market, and we never have to worry about market volatility. Unfortunately, it is too good to be true.

The first issue is opportunity cost. The cash cushion is a little bit like leaving the house every morning wearing a Robin Hood costume, just in case I might come across a fancy-dress party that day. That strategy works beautifully every year in late October, but it would be a bit of a burden for the rest of the year. Likewise, the opportunity cost of carrying too much unneeded cash when there isn’t a bear market can compromise the average portfolio return. Remember, timing Halloween parties in late October is easier than timing the next bear market!

But even if you do get lucky and have the cash cushion ready to go at the onset of a bear market, it’s not going to make much of a difference. If you were unlucky and started your retirement too close to the market peak in 2000, then with or without the cash cushion your retirement portfolio would have been seriously compromised; we are talking about “going back to work” compromised! True, the portfolio with the cash cushion would have been slightly less compromised than an all-equity portfolio, but still seriously underwater. The cash cushion is no panacea because you will have to replenish the cash cushion right around the time when the stock market rallies again.

One way or another, opportunity costs will catch up with you! It’s very simple: there is no true bear market insurance. A good start would be using a lower withdrawal rate (see #1 above) and being prepared for plan B, plan C, and all the way to plan J (Money).

#7: Tax loss harvesting saves you a ton! (It’s nice, but you won’t get rich)

As mentioned above, I do the tax loss harvesting by hand without any help from the Robo-Advisers and my guide on how to be your own Robo-Adviser has a lot of the details on how to do this right.

Did I become rich from tax loss harvesting? Absolutely not! The claims of 0.7% or even north of 1% of additional annual returns from tax-loss harvesting claimed by the Robo-Advisers are vastly exaggerated. If you are like me your taxable portfolio is the result of many years of regular investments. So, even a bear market with a 20%+ drop right now would result in much less than 20% harvestable losses. I have some tax lots that would require a 50%, even all the way up to 70% drop in the stock market before generating even a single tax loss dollar.

My personal estimate is that I have generated less than 0.10% in additional annual return from tax-loss harvesting so far. Going forward, especially once I retire, the benefit will likely go away altogether.

I put together some calculations on how much extra return you’ll likely generate depending on different marginal tax rate scenarios and portfolio sizes. Under most realistic assumptions, the benefit is even lower than the 0.15% to 0.35% Robo-Advisers fees. It’s a benefit large enough to not leave on the table, but don’t get your hopes up too high. And don’t pay anyone 0.35% p.a. to do it for you, either!

I’ll now be taking all questions and concerns below :)

*****

About the author: Mr. ERN runs the EarlyRetirementNow blog where he writes about his path to early retirement, planned for early 2018. He currently works for a large asset management firm and holds a Ph.D. in economics.

[Top photo cred: hobvias sudoneighm]

Get blog posts automatically emailed to you!

ERN, thanks for sharing your well-supported thoughts! I must be a non-conformist as well, as I agree with most everything you said. Emergency fund? I have a HELOC instead. Robo-Advisors – I’m a DIY type of guy. 4% withdrawal rate is risky over 30 years for sure which is why rental properties or other passive income sources are so important and so valuable.

And as for bonds, I’ve still got 8% in my portfolio but to your point, I’m not sure they are helping me much. That’s the piece I want to figure out over the next few weeks befor my semi-annual rebalancing.

Thanks for sharing your thoughts!

Thanks, Jon!

Yes, I remember your HELOC post, great one. Glad we’re on the same page! Not so controversial after all. Who knows, maybe we are all the silent majority here?! Not so silent anymore!

Cheers!

That was a really intense read before dragging my butt out of bed this morning! Wow! I must say that I do tend to agree with a good portion of those points.

I do think emergency funds are overrated. Of course we have one, but I often question whether or not we should just invest the majority of the money and take our chances with monthly cash flow and, dare I say, credit cards as a parachute. Any emergencies not covered with cash could be covered from investments or on low interest credit cards for a month or so. It’s definitely something I struggle with.

I also agree with his outline of the Trinity study. We’re planning to produce the majority of our early retirement and retirement through real estate investing. That way, in a bear market, we just keep collecting rent and don’t touch our investments.

Great financial food for thought!

Mrs. Mad Money Monster

Haha yeah – it took me a while to sit down and review/edit all this because it was so heavy with knowledge :) But I enjoyed reading it a few times in doing so!

I will also say again that I believe that money is meant for more than just “growth” all the time. Or else we wouldn’t be spending it on insurance or traveling or other things that don’t return a tidy profit. To me dollars serve different purposes, and the important part is making sure you’re putting them wherever you think they belong!

Here’s a writeup I did on it recently because it started bothering me that everyone just wanted every single dollar to GROW which just isn’t possible ;) https://budgetsaresexy.com/2016/09/each-dollar-serves-a-purpose/

I totally agree that every dollar shouldn’t grow. I’m just curious, have you heard of the concept of a “steady state” economy? You can learn more here: steadystate.org. Very controversial, but interesting, nonetheless.

I haven’t heard of Steady State before – going now to check out!

Thanks, Mrs. MM! I usually need a strong coffee in the morning. But a dose of BudgetsAreSexy works too!

Also, agree on the SWR issue: Having some other investments like Real Estate that pay stable yields prevents having to dig into the principal of the nest egg, right around the worst time. That’s a real smart idea!

Cheers!

Agreed, excellent article!

It’s important to distinguish between people with their financial house in order, vs those who are in panic mode. This article is for people who have their house at least somewhat in order.

So the emergency fund – someone who is barely living paycheck to paycheck needs a cushion, because being poor is ironically one of the most expensive conditions (in the US at least). It’s that simple.

But someone who has comfortable savings can then fine tune how that cushion can look – cash or cash equivalents, easily liquidated investments, etc. This article is for fine tuning.

Personally, I love to talk about personal finance. If someone asks what they should do, I ask questions to figure out if they’re in panic mode or comfortable. In panic mode, I usually recommend Dave Ramsey (even though I disagree with parts of his technical approach and the religious enmeshing) – because he is amazing at harnessing emotions to do something really hard. In my own life, I was comfortable financially then got knocked back and had to struggle back up – I knew enough not to follow his method, but relied heavily on his website and radio for motivation.

Excellent way to distinguish between the two type of people – I like that! Panic mode or Hustle mode. Might have to borrow that for an upcoming post :)

Really appreciate these perspectives ERN. I think I agree with most of them (but not all), especially #3. When I first heard about robo-advisors I was really intrigued. I then realized that they’re doing little that the average index investor can’t do on their own and taking a piece of the pie to do it. For some people, it’s a good solution – certainly better than many traditional options, but for those of us who know a little about this stuff – I can’t see where it makes sense.

Yes, thanks! Again, the emphasis is on “it’s not for everyone”… For a young person just starting it might be great. For the more experienced FIRE crowd with the DIY gene, not so much.

It was a great starting place for a newbie. But I am too frugal to pay 0.35% and I much rather DIY at this point with more knowledge:-)

Loved this quote I heard today: Money is relative to the time you have to enjoy it.

I like using the 4% rule as a simple long term estimate. Obviously there are going to be a myriad of other unforeseeable variables that are going to arise when we actually start into our early retirement but this at least serves as a starting mark to aim for. Once we get to that minimum value we will have better information due to lessons learned through time and experience. I’m actually hoping to use the strategy one of my professors taught me that you get to the 4% mark then you only withdraw what your investments earn (less 3% for inflation) each year. For example, if in our first year of retirement our portfolio earns 10% then we could technically withdraw 7% if we wanted to. But if it only gains 4% then we would only be allowed to withdraw 1% and have to find ways to make that work or subsidize our income in other ways. And if it drops then we aren’t allowed to touch it. This will make sure that the purchasing power of the investments will sustain themselves indefinitely.

Great point: You gotta be flexible when withdrawing money in retirement. Slow down withdrawals if the market performs poorly and you can probably avoid a lot of headaches.

One caveat of being too dynamic: Adjusting the withdrawals when the market goes up might create some lifestyle inflation that’s hard to get rid of when the market goes down again.

Thanks for your feedback!

ERN

I kinda like that one, Band of Savers!

I have to agree with a lot of it. I am not a fan of bonds especially in a rising interest rate environment. Plus as you shared with a 80/20 stock to bond strategy have a correlation close to 1 why not just hold stocks and get the benefit of the upside.

I also agree that robo advisors are the easy/expensive way of managing money. With a little bit of research it’s pretty easy to figure out what the right balance for an investor is.

Anyway great article!!!

Thanks, MSM!

Another way to lower volatility: Just hold lower vol stocks (duh!). So a 100% portfolio with stocks that have a 0.8-beta might be the best of both worlds: Lower vol and higher return that 80/20 (though probably slightly lower expected returns than a 100% S&P500 portfolio).

Thanks for your feedback! Always appreciated!

Love the post, ERN. You probably know already, but I’m very much in agreement with you on these points. I don’t have any need for an emergency fund, there are too many other good options to serve as an emergency fund without having the drag of cash sitting idle in an account.

4% SWR…I’m not going to hang my 50+ year retirement on that. Better safe than sorry given the lower rate/return environment and the long horizon.

My portfolio is diversified…among all stocks. That’s the best performing asset class over the long run so I’ll stick with that.

Great post, ERN. Consider me a rebel among rebels as well!

All right, that’s the spirit! More rebels around here in the blogging world! Thanks for your support and feedback!

I think the robo advisers like Betterment are great for accounts starting out ($100 – roughly $18,000 due to $3,000 min. to get into each mutual fund and having 6 different funds) but after that you can replicate what they are doing yourself and choose your asset allocation a bit more strategically, without the added fee.

As far as safe withdrawal rates go, I agree wholeheartedly that past performance is no indication of future results, and I think that there simply isn’t a safe withdrawal rate at all. People shouldn’t blindly take out a fixed percentage of assets every single year, it isn’t an efficient withdrawal strategy.

With that being said, I think on average withdrawing over 4% per year may not be out of the cards. In the trinity study the median account ending balance for a 4% withdrawal rate and adjusting for inflation was 10X the starting balance.

Thanks, great comment. I completely agree with the Robo advisers approach. That’s the advice we should all give to the folks who are new to investing: Start with Betterment, then do the account transfer to your own broker (make sure that no capital gans are relaized and the transfer is in-kind not in cash!!!).

Also agree with the SWR: The caution about the SWR<4% is about tail events. The median investor over time did much better. That's because the median/mean stock return was 6%+.

But the poor guy who runs out of money after 30y and has another 20-30y ahead of him, can't just knock on the door of the "median guy" and ask for help. :)

Also, when I'm older and have only 20-30y life expectancy and the market returns to normal valuations, I will definitely hike up the withdrawals. You're right: 4% on average is absolutely in the cards.

Cheers!

Hiiiii folks, I’m a big reader of y’all and a 25 year old just starting out. I have a 401k with my current employer, and a betterment account from my year interning around low paying gigs. Right now, with betterment, I have a few thousand in an IRA and a thousand in another long term growth portfolio. I’m realizing the fees are not worth it, and have been planning to switch to vanguard with the assistance of a savvy pal, or at least switch to wealthfront, which is free under 10k. Any advice pulling the trigger on this? I’m paying .35 annual interest at betterment. Additionally, after reading this post I’m nervous because I have been vocally supporting my parents as they pull their retirement accounts out from under a (slimy) investment manager to a betterment account. How can I support them to avoid cap gains tax on this transfer? They are super hands off. THANKS for everyone on this thread– I read your blogs every day! So grateful for the knowledge and discussion!

Big ERN! I’m thrilled to see your ideas featured here. I can’t argue with any of them; Of course, I’ve read most all of your posts and rationale already.

Here’s a #8: Vanguard is THE place for your money. I’m a big fan, and pretty much all of my money is with Vangaurd. But there are other excellent options.

I recently helped someone close to me unwind a mess of 28 mutual funds (mostly in a 401(k) fortunately). The funds were held at Fidelity, and we transitioned to something close to a three fund portfolio with Fidelity. The costs were slightly lower than Vanguard (lower ER) for each of the three funds. Keeping the money within Fidelity simplified the transactions. If the account owner has questions, he can visit a Fidelity branch.

And don’t get me started on ETFs being better than mutual funds. Different, yes. But not necessarily better.

Cheers!

-PoF

p.s. Thank you J$ for featuring my $ post on Rockstar Finance today. A Happy Friday!

Hi PoF,

Thanks, and congrats on your Rockstar Feature today!

Yes, I like Fidelity, too especially for the plain-vanilla large index funds. But that might be a real hornets’ nest that even I don’t want to mess with. Those bogleheads will all come after us…

Cheers!

Also heard good things about Fidelity here too.

In fact, my parents whom half retired last year and the other half will retire this year, all have their $$$ in Fidelity and rave about them.

I’ll keep mine at Vanguard, but if someone put a gun to my head and told me to move it out of there, I’d take a trip down to Fidelity :)

BIG ERN! Love your stuff, your withdrawal rate series was the best I’ve ever seen. I love a nonconformist nonconformist (is there such an adjective?), and the way you challenge us to think. Strong points, all. I agree most strongly with the 4%, and am using 3.5% or less for our FIRE plan in June 2018. After seeing your analysis, I’m looking at bumping it down a bit more. Great work, and you’re making an impact on the FIRE community!

Thanks, Fritz! And I didn’t even write about the options trading… Geez, we would have agreed on that one, too. Are we twins separated at birth???

I agree with most of your points here. The longer expected retirement of an early retiree is a good point on the 4% withdrawal rule. A better idea is to generate passive income to cover most or all your expenses.

At this point, I will disagree with you on Robo Advisors. I’m still testing them out, so I’m not making any final judgments, but I like them so far. First, I haven’t reached the threshold yet for when I will start paying 0.25%. When I do, we’ll see if the benefits come close to outweighing the cost. The ease of using a Robo Advisor frees up time to spend on other income generating activities.

I’m also curious about tax loss harvesting. I don’t have any illusions that it will make me rich, but I do think there is benefit (saving money on taxes while you’re in a higher tax bracket now). Again, we’ll see if the benefits out weight the cost. If what I’m giving up is substantially more than what I’m receiving, then I’ll make the switch to a DIY method.

Overall, I enjoyed your list. Thanks for sharing!

Thanks for your comment! Probably on the Robo Advisers we agree too: Simply transfer the account once the account balance becomes big enough to no longer justify the fees. I would totally endorse that!

Cheers!

I politely disagree with a few of your points! :) But the reason I’m commenting is to point out how you can have professionals disagree on fundamental principles, which is why I continue to believe that most people owe it to themselves to learn about money and make their own financial decisions. I don’t think a professional can do it as good as you can yourself because sometimes there isn’t one right answer and it’s personal preference! As is the case with these points!

Thanks! Agree! Personal Finance is way too complicated and diverse to be solved by some general advice from finance experts. It’s best to educate ourselves!

Cheers!

I agree with everything you wrote, ERN, but I’m sure that’s not a shocker. :D

Awesome, TJ! Not a big surprise- we are all finance rebels!

Have a great weekend!

ERN

I do think that the 4% withdrawal rate isn’t necessarily the gold standard. There are a lot of factors that play into how much money you should take out. For us, ideally we’d take out as little as humanly possible and never touch the principal amount–dividens only.

Most people do need an emergency fund because most people aren’t saving a huge chunk of their income or paying off debt. ;) But having thousands of dollars in savings while you’re in debt doesn’t make a lot of sense–the money works harder for you when it eliminates liabilities and interest payments.

Thanks, Mrs. PP!

Yes, having an EF while still in debt is probably a good idea. Foregoing the EF when having assets takes some time getting used to, I admit that.

Cheers!

Excellent post and great proof there are few / no ironclad rules of thumb.

One sidebar – I believe the professional designation referenced in your short bio at article end frowns upon its use by anyone cloaked in anonymity. I suspect you know that as I haven’t seen it on your site, but you may need to ask J$ to strike it.

Thanks Paul,

You are right, I should double-check with the Institute about the proper use of that designation, out of an abundance of caution. It is absolutely improper to 1) attach the designation to the blog name (only people can have the designation), 2) attach the designation to my blogging alias, e.g. “Mr ERN, XYZ”. I would never ever do that!

But it is completely proper to refer to people having the designation, as in

“Three analysts in our department hold the CFA designation” without naming them by name. So I would think that it’s OK to mention that the person running the blog has the designation.

But you’re right, better check it before someone complains…

Cheers!

ERN

We have nixed it just to make sure ERN doesn’t get tracked down ;)

I’m with you on the emergency fund – doesn’t apply to everyone though. From 2013:

http://www.howtosavemoney.ca/why-you-may-not-need-an-emergency-fund

Got some flak for publishing that one :)

Yes, thanks! Good article! If we don’t get at least some flak we must be doing something wrong! :)

Cheers!

Hi all!

Thanks, J$, for featuring my post, actually my first true guest post ever (because the “Christopher Guest Post” over at PoF was really an interview, haha)

I hope this wasn’t a dumb idea to open seven fronts all at once. But I like J$’s attitude: You don’t have to agree with everything and still enjoy it. It’s just food for thought, friends! Looking forward to your comments!!!

ERN

It was a most brilliant post man, I’m the one who should be thanking you!

It’s not often you get to see drastically different thoughts here in the $$$ space, and certainly not 7 at the same time :) So I was thrilled to run it and see what my people think! And so far you haven’t scared many of them away! Haha…

Keep on being you, brotha.

Thanks for posting this J$. I’m in agreement with you that you need to read this a few times to let it all the grappling hooks of information flying out at you take hold in your mind! Alot of this information is what I’m currently searching for. I’m starting to feel confident in my stock investing approach, but totally uneducated on bonds. This bond information was a really great 101 place to start for me. Also, I loved the analogy of wearing a robin hood costume out every day just in case you run across a costume party. Haha. Although I do love jumping into a great random dance party, dressing up for one is too high of a risk for me. I like to time the market the best I can. But like I read once, “Money IN the market, is better than waiting to time the market.” Thanks for the mental chewing gum. I’ll save the article and give it another read later in the day.

Awesome! Glad you liked it. Once I actually saw someone with a Robin Hood costume in the street and it wasn’t Halloween, so if you wonder where that analogy came from, haha!

That quote about money in the market is great. I wrote that down because it’s a one sentence summary of my philosophy, too.

Cheers!

How about a heads-up before making my (typically casual) Friday-morning read the most intense thing I’ve done all week?!

Good stuff, Ern. And by good I mean scary. And good.

Haha, that’s a nice compliment! ThanksTDL! Have a great (and relaxed, calm) weekend!

Cheers!

We gotta keep y’all on your toes over here ;)

Excellent points. The key is to keep is to leave fear out of it no matter what but continue working on growing your finances to what works best for you and your current situation. My father passed at 55 and my grandfather (his dad) passed at 92. My father never even got to enjoy his retirement but my GF went way above the average.

Growth without fear no matter what.

Oh wow, that’s sad. I, too, saw a lot of relatives pass away right around their retirement age. A big incentive to accelerate the retirement, budget with a sharp pencil, and invest wisely!

Cheers!

About the 4% rule, no one know for sure what the future holds but we have to shoot for something…. I agree somewhat on robo advisers, but I still live acorns. Im going to keep doing that, I am actually going to just let that ride for a few years till I have enough to take my family to Hawaii. Then I repeat, every 5-10 years it will be like a free vacation since it wont tap my main accounts.

I do not think an traditional emergency fund is a good idea either and J, as someone who rents as a means of plumping up their retirement funds through extra % gains over real estate I am surprised you don’t see the merit. Its kind of the same principle. emergency fund = .001% interest vs market gains. I have somewhat of a hybrid approach as I don’t think my Roth IRA will ever be significant I rely on my Roth contributions as a safety net. I can withdraw those tax free as long as I leave the gains in the account there is no taxable situation. I haven’t had to use it yet but since Ill never have that Mitt Romney $100 Mil Roth IRA it’s whatever. I’m viewing my Roth as extra. Retirement will be 401k, which after careful planning with my accountant this year I am happy to say my 2017 contributions will be $54K. I put ever spare dollar after 401k and IRA into my house. I feel like this mortgage is a layer of ice preventing me from getting to the top side to take that much desired breath.

Thanks for the support! Glad we agree on the emergency fund!

Cheers!

I’m all for maximizing your money, just not *all* of it *all* the time :)

I agree with all your points. However, I don’t necessarily follow your advice or my own intuition. I think a big reason is fear and conformity…society likes us to conform and I often don’t have the courage to go a different route. It’s so much easier to just conform. But I definitely need to move a lot more money out of cash (earning practically nothing) and have it work for me. Same for a good portion that are in bonds. And I want to say that I admire your point relating to robo-advisors…apparently they have great affiliate programs so that perhaps may be a reason why we keep hearing about them in the PF space! =)

Thanks! Haha, yes as a blogger with some traffic to your site you’d be throwing away a lot of referral fees if you don’t endorse Betterment. But we all should only endorse products and services that we truly believe in. I was very intrigued with Betterment initially but the more I looked into it the less I liked it.

Cheers!

My emergency fund has been my buffer against credit card debt on multiple occasions, so I can’t dismiss its value. Though I agree that having large amounts of money sitting in a savings account earning next to nothing isn’t a great idea. When I read stats about average individual savings habits though, I still say an emergency fund is step one in their $ efforts. Yes, pay down debt, save for retirement and all that, but there has to be SOME buffer from high interest credit card debt. You’re clearly in a place where that buffer is already well established, (even if not in the form of a traditional savings account), but for most people, that’s not necessarily the case.

Very much enjoyed the read. Thanks for sharing!

Thanks, Stephanie! Yes, if you make a great point: If the EF is used as a stepping stone to get used to savings and then later save in equities and productive assets, I fully endorse having an EF. But if the EF is a hindrance to savings and folks don’t max out their 401k because they are too busy keeping and replenishing their EF, I’d be less open to an EF.

Cheers!

I have gone back and forth on the emergency fund. I have a pretty hefty one. But for me, it is not about ‘growing’ these dollars, but about having peace of mind. We have real estate and want to travel the world, so this money will provide a great buffer in case of a maintenance issue or vacancy while we are half way around the world. I always suggest that any real estate investor have a good emergency fund. In the stock market, if something goes wrong and you experience a loss, it is just money taken out of the account you already have, but with real estate, that same loss of ROI is usually in the form of writing a check. Similar losses, but different pots.

Thanks! Piece of mind is going to you (opportunity cost). Not much per month but a pretty hefty sum over time. It took some getting used to but I live pretty comfortably now. Part of that is due to a 50%+ savings rate to cover any potential spending shocks. It’s not for everybody, like the headline said. :)

Cheers!

Well, there might be more ‘rebels’ than you think, ERN. I am in full agreement with points #2 to #7, plain and simple. Been making similar points with various folks for a while, actually. And, as an early retiree, I put my money where my mouth is (figuratively speaking!).

On #1, the 2nd observation is not quite right, we had worse valuations (stocks and bonds) before, and the 4% rule takes them in account – even if I do agree that today’s situation is worrying. I suspect that what you really have in mind is that future returns might be more subdued than past returns, and I wouldn’t disagree, but this is a different point than what you talked about.

I don’t disagree with the math of the 1st observation, but the conclusion is clearly erroneous by missing the bigger picture. First, somebody retiring (very) early will still retain human capital for quite a while. If a 1929-like crisis hits, let’s get real, this early retiree will adapt, and find a way to make some money at some point in time to compensate for the deep crisis. Next, nobody in their right mind would use a constant-withdrawal technique for 50+ years (or even 30). And as soon as you start accepting the idea of variable withdrawals, then sequence of returns issues can be managed much more effectively, and the SWR sheer concept becomes pretty much moot. I really wish researchers would stop re-hashing SWR models, and focus on real-life solutions instead of false problems.

Still, this point #1 put aside, thank you for sharing excellent wisdom on points #2 to #7. You really have a knack for figuring out AND explaining things like that, congratulations.

I was going to reply to make the same points, so I won’t….but I will add this:

The 4% rule is still VERY good, even if it isn’t PERFECT. When you say “The Trinity Study averages over many decades with different financial market regimes. Sometimes the stock market was overvalued, sometimes undervalued. Sometimes bond yields were very high, sometimes they were very low” — that’s not exactly true. It looks at all 30 year periods within history, looking at what would have happened if you had retired on, say, October 28, 1929 (day before the big crash), and then tried to figure out what withdrawal rate would succeed 95%+ (or is it 99%+) of the time for 30 years. So if it survives even if you retired days before some of the worse market drops in history, it’s pretty sound.

I think people who say “4% isn’t safe enough, I have to go to 3% or 2.5%” are sacrificing a lot of freedom for an incremental (if not zero) increase in security.

I loved this Michael Kitces article (https://www.kitces.com/blog/the-ratcheting-safe-withdrawal-rate-a-more-dominant-version-of-the-4-rule/), particularly this part:

“In fact, not only do 90%+ of retirees finish with more than their starting principal after 30 years by following the 4% rule (so even if you outlive the time horizon, there’s still funds left over), the “typical” retiree actually finishes with many multiples of their starting wealth with this spending approach! Over 2/3rds of the time the retiree finishes with more-than-double their initial principal left over. And the median wealth at the end of 30 years is almost 2.8X principal! One-in-six scenarios finish with more than quintuple the retiree’s initial wealth! Since the 1920s – the “modern era” of stock investing (as illustrated by the classic Andex Charts based on Morningstar/Ibbotson data) – the odds of doubling wealth is 80% (on top of lifetime spending using the 4% rule), the median wealth at the end of the time period is 3.7X starting principal, and more than 1/3rd of retirees would have finished with over 5X their starting retirement portfolio!

Of course, in some of these situations, final wealth is augmented by decades of compounding inflation. Nonetheless, even on a real (inflation-adjusted) basis, retirees finish with more than 100% of their inflation-adjusted principal 60% of the time, and double their real wealth almost 1/4th of the time, even after supporting a lifetime of inflation-adjusted spending at a 4% initial withdrawal rate!”

In other words, 4% is VERY safe, generally speaking, and you’re FAR more likely to end up with MORE money than you started with than end up with nothing using it (which is why Kitces advances a cool “ratcheting” plan where anytime the remaining balance increases 50% over your initial balance, you increase your withdrawal rate by 10%, to allow you to enjoy a bit more of your wealth). But, just in case, be vigilant and flexible, in case some bad sequence of returns affect your portfolio.

Also, keep in mind — those pursuing Early Retirement (i.e. your 50-60 years of retirement) typically come up with their “number” based off a SWR without factoring in Social Security income (which they almost certainly will receive, to some degree, assuming they paid into it), any income in “retirement” (sometimes “hobbies” turn into things that make a little extra cash), the possibility they may NOT live 50-60 years (I’m 37, my dad died at 76 — I could live to 87, but maybe not), the possibility their spending may DECREASE later in life as they slow down/get older/don’t travel as much/as well, the possibility they may not NEED to increase their amount by the inflation rate every year (because their spending isn’t exactly similar to the prices affected by inflation), etc.

All a long way of saying — 4%? Still pretty good.

Agree: Flexibility is key when the portfolio value falls and you suddenly have a choice between cutting your withdrawals or withdrawing much more than 4%. Sure one could go back to work, but you might have to find a job at the bottom of the recession when millions more are trying the same.

Also, I am not quite sure when the stock and bond valuations were much worse before. What retirement start date do you refer to? I cannot find a time when the valuation was worse than today and the 4% rule worked.

1: in 1929 the CAPE crept up to over 30 for a few months, but only at the very extreme. For the most part of 1928/29 the CAPE was lower than today’s and 10y bond yields were 3%+ rather than 2.4%.

2: in 1999/2000 the CAPE reached over 40. Had you retired at the top of the market with an equity-heavy portfolio you would not have exhausted your portfolio by now but it’s so seriously compromised by now (<$500k real) that with the current 8% withdrawal you will exhaust the portfolio by 2030 even if equity returns go back to their 6% real average. Not a pretty picture.

What was different in 1999/2000 is that we had 6%+ Treasury bond yields. So with a portfolio that had enough bonds you would still have a chance to recover. But today's bond yields are so much worse!

3: the other unmitigated disaster for the 4% rule was a 1965/66 start date. CAPE in the low 20s (vs. 28 today) and bond yields 4%+. Much better valuations. 4% wipes you out after 30 years. I need 50-60 years.

The mistake a lot of people are making is to believe in the widely-circulated myth that 2001 and 2008/9 support the 4% rule. Not true: I have seen some whacky calculations where people don't do the CPI-adjustments to withdrawals (argh!) and/or not account for CPI in their final value (double-argh). If you do the calculations right, the late 1990s starting dates are not supportive of the 4% rule. We just didn't have enough time for the Trinity Study economists to update their 30-year windows. Once they do in 2030 we will see that the 4% didn't work over that time span.

I actually said “this early retiree will adapt, and find a way to make some money at some point in time to compensate for the deep crisis.”. Not necessarily DURING the crisis (I agree this might be hard). People totally freak out at the idea of selling stocks when they are at a very low point, but you only sell *some* stocks (for your annual spend), this is entirely recoverable if you tighten the belt a bit (variable withdrawals) and add some new capital at some point later on. Fact is early retirees are (or should be) an adaptable bunch, let’s not forget that.

Yes, you are correct, past cases like 1965 didn’t work with 4% SWR, even with 30 years (while 1929 did). My bad, I forgot about that. I just meant to point out that today’s situation is bad, but not the first instance of similar extremes. I would add though that the CAPE of today is not the same thing as the CAPE from 1929 (looong discussion!). Anyhoo, again, we need to elevate the discussion, SWR reasoning (and constant withdrawals) is just an entirely flawed premise, notably for early retirees.

First, I think the problem with the 3 CAPE scenarios you’re discussing is using an “equity-heavy portfolio,” when in fact the Trinity Study (and others) have consistently used a 60-40 stock-bond portfolio. Using that (or, at minimum, something incorporating a decent chunk of bonds, say at least 20%) certainly improves your results in years where equities tank.

Second, the problem with CAPE is that we’ve been above the CAPE long-term “average” for 25 years now (indeed, since 1992, we’ve only dipped below the long-term average once, during the financial crisis). There are many theories as to why this is, but at a certain point we need to consider the possibility that a long-term CAPE average that factors in eras before the internet/computers/Jim Crow/women’s liberation MAY not be as useful a predictive tool of forward returns as it once was.

Third, you write that “The mistake a lot of people are making is to believe in the widely-circulated myth that 2001 and 2008/9 support the 4% rule.”

I certainly do not believe it’s a myth. It’s pretty well proven, at least thus far.

Here’s an article (again by Michael Kitces, in July 2015) where he shows 1999/2000 retirees are no worse off at this point than retirees in other terrible market years (1929, 1937, 1966) where the 4% rule still worked: https://www.kitces.com/blog/how-has-the-4-rule-held-up-since-the-tech-bubble-and-the-2008-financial-crisis/

And yes, Kitces does his calculation in both nominal dollars AND real dollars. And per his calculations, a 2000 retiree is doing BETTER than a 1966 or 1937 retiree (and only slightly worse than a 1929 retiree) at this respective stage, and the 4% rule WORKED for all of those other scenarios. Per Kitces: “Relative to the 2000 or 2008 retiree, though, the results continue to look reasonably in line. Certainly the markets are not as favorably valued now for the 2000 retiree as they were in 1981 for the 1966 retiree, but then again the 2000 retiree is still only at a 6.2% withdrawal rate today (with just 15 years to go), while the 1966 retiree was over a 10% withdrawal rate at this point. And in the case of a 2008 retiree, the withdrawal rate is already right back at the 4% initial withdrawal rate the retiree began with (after already doing 6 years’ worth of retirement spending!).” And keep in mind this Kitces article was written in July 2015 — since that time (or, actually, since January 1, 2015), the stock market has returned 5% real, suggesting the 2000 retirees are still well on track (if not in even better position than they were in July 2015).

Now, the Trinity Study could be proven wrong — neither you nor I have a crystal ball for the next 13 years to figure it out. But I’d feel pretty confident betting that the 4% “rule” (which, really, was never a rule but more a guideline that people should have reasonable flexibility with) will work for 2000 retirees just like any others.

Kitces is actually THE reason to be concerned about the 4% rule.

a) the 2000 retiree would have almost preserved the principal. But only in nominal terms. As Kitces points out (for all who can and want to read through the whole post). In real terms you’d be severley underwater. You’d be lucky if the money lasts 30 years. You will FOR SURE run out of money after before a 50 or 60-year horizons is over because you’re already 40% down in real terms and now withdrawing 6%+ out of a portfolio that has expected return of around 4% real. Good luck making that last another 43 years.

b) In one post (the ratcheting post) he uses 1-year T-bills as the bond (to make the 4% rule work throughout the 1970s). In the post about the 2000s he uses 10Y bonds. A little bit too selective and back-fitted for my taste. The 4% rule only works if you know ahead of time which bond instrument to use. If you had used the recommendation of 1Y T-Bills from the ratcheting post, then your portfolio would have been down 65% in real terms by 2016.

See my contribution about the Y2000 retiree:

https://earlyretirementnow.com/2017/01/18/the-ultimate-guide-to-safe-withdrawal-rates-part-6-a-2000-2016-case-study/

Great post, ERN. I definitely do agree with all of your points.

For the withdrawal rate, I do think it will work as long as the individual withdraws 4% of their portfolio each year instead of 4% of the initial starting portfolio. However, it would definitely be more safe by having a lower withdrawal percentage or even if the individual/family was flexible on how much they withdraw.

For example, if it’s a good year and they find themselves not wanting to spend that much, they would simply just withdraw less and reinvest the gains.

Of course, this depends on the individual/family and their lifestyles. It can also pose a risk due to lifestyle inflation, if not controlled properly.

The 4% withdrawal rate reset every year (or quarter, or month?) will work in the very long-term if your portfolio yields 4% real (otherwise you never run out of money, but you walk down your purchasing power). 4% real is not even that hard to accomplish if you stay above 75% equities. The only disadvantage: your consumption now becomes just precisely as volatile as your portfolio. If people have flexible enough consumption and/or can make up for lost withdrawals with side income, that’s great. I personally would like stable income and not worry about going back to work, but that’s my personal preference.

Thanks for the great comment!

I mostly agree with these. Great post, ERN!

You rock! Thanks for stopping by!!!

Cheers,

ERN

Ok, I think you need to officially hand in the rebel badge. Almost everyone who commented agrees with you!

Just wanted to pop in and say that I enjoy your blog and appreciate all the work you put into coming up with original content.

Haha, yes who are the rebels now? Seems like most people agree with at least 5 out of the 7! Gasp!

And likewise, thanks for your work and your reminder. I found some “in my couch” thanks to you: http://www.bayalisistheanswer.com/how-find-unclaimed-property/

Cheers!

ERN

Nice article. I’ve heard an alternative to the 4% withdrawal rate for early retirees is to take your age and divided it by 15. This gives a more conservative rate of withdrawal.

I love that rule: It comes out to 3% at age 45 and 4% at age 60. But again: if folks retire in 10 years from now and we have very different equity and bond valuations at that time, even that rule can be scaled up again. I don’t want to be a perma-Grinch. :)

Cheers!

Great post ERN. I am not a fan of emergency funds either as dividends provide enough cash flow to serve that purpose. You are becoming the SWR guru in the PF blogosphere! I agree with everything you have written with only a minor adjustment to SWR – I think 3.5% is about the lowest you need to be even for 50 year retirement horizon. The ratcheting plan is also good as Kitces says or even better would be a SWR jump (to 4-4.5% from 3.5%) after the first decade of retirement if the portfolio balance is at least as much as you started out with. SORR impact is highest in the first decade of retirement so one you cross that, you have smooth sailing after.

Thanks! Well, I agree that if stocks cooperate during the first decade and the CAPE returns to more normal levels, we can indeed ratchet up the SWR towards or even above 4%. Just not initially.

Cheers!

Great stuff as always, ERN! And a big congratulations for the feature here – much deserved!

Thanks, FL! As a regular ERN-reader, you probably knew many of the points but I’m glad you enjoyed the feature here!

Cheers!

Great article! I love challenging the accepted thought process!

Have to admit to the Cash Emergency Fund norm here. It kills me to see that much cash just sitting there drawing a measly 0.9% interest from the Savings account! Time to research!

Thanks, Mistress Finance! That’s the spirit, get those green fellows out there and let them earn more than 0.9%. At the current rate of Fed Funds rate increases it will take years to get back to normal levels!

Cheers!

As a person with a variable income, I know that an emergency fund is important for me. If I had a different career situation and a better knowledge of anticipated earnings, it would be less relevant.

I like Financial Libre’s 3.5% SWR.

Thanks! Yes, definitely, I like FL’s analysis. Good to know that two guys using different method come to the same conclusion.

Cheers!

Hi

I am 61, retired with a guaranteed pension, and I really worry about the 4% retirement rate. Why??

I have enough income in today’s rates to live pretty well, but factor in inflation >3%, and suddenly our income doesn’t keep up with inflation. My workplace pension is restricted to 3%, so is 50% of my husbands, and while the UK state pension should keep up, it is only a proportion of our income.

The reason I am worried, is before all you millennials were born, we had raging inflation in the UK. Mortgage rates in double figures were common from early 1970’s to 1990’s. I paid 15% for several years.

So factor that into your lump sum, and suddenly 4% seems ambitious. Ok, your lump sum will grow, but at a high enough level?

It is why

A) I continue to save hard, even when I am in a position to take it easy

B) I continue to consider alternate income streams

Agree: Inflation is the one issue that people have forgotten (or maybe never experienced). And Inflation has the tendency to hit when we expect it the least. I like real assets that have some inflation protection built-in: real estate and stocks (in the long-term). And being cautious about the withdrawal rates and aggressive with savings rates would be important too.

The vast majority of financial “experts” know very little about managing money. They are experts, of course, but it’s just at writing, talking on the radio, or being on TV.

So I pay them very little attention…

Haha yup… Especially when it comes to telling you how much you need to retire! I’d like them to at least *once* ask you what your expenses and lifestyle is first before giving you a blanket $2 Million or whatever the latest “number” is.

Great point. We all have to become our own experts. There is no one size fits all!

Cheers!

Building an emergency fund is one greatest task of every person. For me, it’s a priority, and based on experience, there was an incident which required much money, and I fully depended on it and did not resort to taking any loan.

That’s what I thought, too, long time ago. But ever since we went without a designated EF and rather fund one big pot of investments we did just fine.

Thanks for your comment and Cheers!

Love the against the gain approach. Haven’t seen much of that around. You take on no emergency fund rings very true to me. For years I’ve wondering why some focus on this so much and without it do not feel safe. I’m not at your target of 60% but am at a comfortable 40%. It’s like you said and covers most unforeseen circumstances. I’m actually looking at putting some of that savings in bonds as you discussed. What I’ve been doing recently is looking at my local cities offerings. It’s a double whammy in the sense you get to diversify as well as understand more about what is going on in your community.

Thanks! So you are talking about Municipal Bonds? I have some and I like the tax-free interest. But even if tax-free the yield is still pretty measly. I’d still prefer stocks and collect a dividend yield almost as high as the bond yield.

Cheers!

losing 10% and the year after earning 10% is not neutral, assuming you wanted to make it looks like.

the reverse of losing 10% is earning 11.11111…%

doing this for 3 years is even worst: 100 -> 90 -> 81 -> 72.9 -> 80.19 -> 88.209 -> 97.03

Just saying…

Absolutely true. Good point! But it wasn’t my intention to come back to 100 after 6 years. This was just to show that over 30 vs. 60 years you get a different impact from capital depletion. Whether you take -10%/+10% or -10%/+11.111%.

Thanks for your comment!

This is a killer post. I used Betterment for 1 year right after they launched – I was sold by the User Experience, then I started doing the math after 6 months and realized how ridiculously expensive it was. I also did the hard work of trying to figure out the actual value of Tax Loss Harvesting (their value prop at the time – it will save you thousands of dollars), that wasn’t true. I calculated it would only save me about $410 total. I dug really deep into tax loss harvesting research and it just never added up as a cost benefit for me. The way they positioned it was that it would more than cover the fees. Which I ended up finding incredibly misleading after doing the real math (at at least hacking the math enough to figure out thats not true given the primary investment vehicle are index funds). Once I did the final math it would have been over $15,000+ over the next 20 years in fees for a better user experience? No thanks. I immediately withdrew and put it all into my own Vanguard funds. Regarding Emergency Funds I agree with you 100% and actually just did a podcast on the topic: http://podcast.millennialmoney.com/e/rethinking-emergency-funds/

Thanks for the very detailed great post! We need more healthy mythbusting and debate.

Awesome! I agree that for people Betterment wouldn’t be such a bad idea: See what they are doing for a few months and then move over to a low-fee brokerage account. No need to pay 0.15% p.a. for what they offer. Yes, they do have a pretty web interface. But it’s not worth my 0.15%. :)

I love the podcast on the EF. That’s exactly what I did. My first $10,000 was saved in equities and that was the foundation to future savings.

Cheers!

ERN

Quick question – what does p.a. stand for?

p.a. = per annum = annual return or annual fees.

Cheers!

This post is all-encompassing in terms of personal finance. Number five Bonds are safer than stocks. (Depends on the horizon!) is an excellent point. After years in this business I feel confident that your theory is absolutely true. Although I tend to disagree with the sixth point, everything else is true in my eyes.

Awesome, we agree on 6 out of 7! Do you have a post or some research on how to make the cash cushion work during the 2000-2009 era?

Thanks and Cheers!

Just out of curiosity, what would you recommend regarding #3 if you live in a country where you can still get interest on bank accounts?

Good point. If you have access to a cash-like account with an interest rate that’s higher than the expected inflation rate (after tax!) I’d say I can be convinced to hold some cash cushion in an EF. But I don’t see that anywhere in the U.S.

Cheers!

Interesting. I tend not to include inflation in my calculations, it seems to me that the basket of consumer goods probably doesn’t apply to people in the frugal/PF blog reading world ;). Plus given how rapidly what people value i.e. spend money on changes nowadays by the time they amend the basket it’s already out of date. But thats just me being a data nerd.

Reg Savers here pay 5% if you’re interested. Capped of course :(

Not everyone needs an emergency fund. True. For people in the FIRE community, I expect the value of an emergency fund may be more psychological than anything. In some ways, an emergency fund gives you the okay to invest aggressively with the rest of your money. However, the higher your savings rate is and the larger your portfolio grows, the less you really need an emergency fund.

Very well said. Most of us in the FIRE community with a high enough savings rate won’t really need an EF except for a psychological reason. Thanks!

Awesome article, I essentially agree with you on all the points. My WR is planned to be 3.33%, I don’t use roboadvisers and actually suspect that – same is true for bluehost recommendations – bloggers who recommend them do that just for the suspiciously high referral bonus.

And so on… the only point with which I disagree with you is Bonds and diversification. Having more asset classes is good not only for diversification, but as an automated mechanism to “buy low and sell high” when rebalancing.

A 60%/40% portfolio would have survived for 30 years starting in 1928 exactly because of that. In 30 years, S&P 500 didn’t fully recover its value but a balanced portfolio would since you could have sold bonds to buy stocks. that’s the true undervalued power of stocks/bonds split in my opinion.

Thanks!

I like the diversification benefit too. But there is a big opportunity cost when government bonds now have a 2.5% nominal yield (I guess around 0.5% real). Not sure how I would get to 3%+ in real terms when 40% is invested at close to zero real return.

I once wrote about having an equity portfolio and buying bonds in margin (10Y US Treasury Futures). But that might be too adventurous for most people. :)

Ugh, you are so right about Bluehost…

Ok *whew* I haven’t understood the draw of Robo-advisors either.

I will however continue to hold onto my emergency fund/security blanket. It’s emotion and experience. My industry fluctuates and I’ve collected unemployment. My salary means I max out unemployment, and the last round, it covered the rent. Power, food, internet to job search from home, gas to drive to interviews was all out of the emergency savings account. This wasn’t the first time, and it wasn’t the last. I also view my investments as untouchable. Sure I could’ve tapped my ROTH, but if I never let that be a possibility…I will have a lot more money at retirement.

I’m the same way with retirement accounts – once it’s in there it’s in there! Gotta find other ways to pay the bills :)

Wow did you get some comments. You made some excellent points some of which I agree others not so much.

I agree on your thoughts re robo advice. I am at a lost to understand why someone spent a portion of their limited time on earth devoted to mechanizing a process so easy to DIY. The robo algorithm merely suggests an investment portfolio as a result of establishing risk profiles. There are about 6 standard portfolios within the advice industry ranging from conservative through to high growth. This standardization of portfolio’s based on client risk has been ‘de rigueur’ for about 3,000 years (this figure may be slightly overstated), so what a robo is providing is absolutely nothing new what so ever. Robo advisers are not AI so you would be much better served to check the standard questions asked by all advisers to establish risk and check the corresponding portfolio and then do it yourself -, bingo..

And by the way, no doubt your friendly robo adviser also has their very own selection of in house products to push, which kinda makes a joke of the word ‘advice’ – it would be cheaper and far more sensible to get investment advice from a gum ball machine in a bowling alley

Haha….

While I agree with most of that comment there, the part that matters most with any of this stuff is the *taking action* part. And my guess is that robo advisors’ target audience are mainly people who have never invested before, and thus – better to pay extra in fees to have $$$ in the market than not. So I personally still think they’re adding value out there.

On your point that robo advisors are a waste of money, I don’t disagree that it’s a true statement for you…. and for every “FIRE” fanatic following your blog. But… for all my friends who still have their 401K at their former employer and haven’t looked at it for years … or for people who barely have any investments at all, it’s a huge value for them to hand their assets over and have them managed efficiently (and without turning over 1-2%.)

I have an issue with ERN taking such a affront to robi advisors. They are there so that we (or I) can save effiecitently, but not have my money the only thought on my mind. If i was do research all of the laws of the market and then research what to put my money into, I would better spend my time being a full time finacial person. I, however prefer to spend more of my time now following my goals sincesinceany of those are far more are dependant and retiri g early means squat when I haven’t spent the time learning other things that will gap me achieve the goals I want in retirement. It’s all well and good to say you want to retire early so you can travel, but when your reason for traveling is to rock climb in various countries, traveling when you can’t climb is pretty pointless. I think this is a good post for those who are bent set on retiring early, but doesn’t address personal choice of putting off retirement to follow an actual passion. I don’t think retiring early is a decent passion in the least. I think finances should be think about what you want to do, then think about how money can get you there instead of think about how to retire, then worry about what you want to do once you get there. I’m pretty young, but my dad just retired and he doesn’t really know what to do with his retirement after 30+ years of working his ads off to get there, so why not spend a few more years working of you can do what you love the entire time you are working?

Budgets Are Sexy is the first finance blog I started reading which started a chain reaction of finding new blogs to read. I was happy to see as I was reading through the Early Retirement Now blog that big ERN has a post on Budgets Are Sexy. Thanks for both of your work. I appreciate it.

FYI I agree with 100% of the article.

Rock on! Glad to have helped jump start the journey here for you :) Looks like you’re now in the blogging game too – welcome!

Be sure to submit it over to our Directory!

http://directory.rockstarfinance.com/submit-blog

I don’t agree with only one thing: not having a cash savings account, especially if you’re not retired or FI yet. Huge downturns in the market are especially correlated with layoffs, so a tumble on your money at the same time of a loss of income is tough.