[Heyo! Got a fun (and smart) guest post for y’all today by Nick Vail of RemoveTheGuesswork.com. It’s a pretty hardcore idea, but if you’re hardcore about growing your wealth, this is the method for you! Starve and stack, baby!]

********

Want to get ahead quickly and set yourself up for financial success?

Of course you do!

Today you’ll get a new idea that can change the game for millennials. I came across this from speaking with a guy I sat next to on a plane ride. Sharp dude. He and his friends would “starve and stack” their per diems when they traveled for work.

We’re going to take that concept and use it to jump start your wealth. Here’s how it works…

The Starve And Stack Method

So… what is the starve and stack method? First off, it’s not literal. You won’t starve. Please, eat and be healthy. The idea is that when a young person gets married, the newlyweds then spend the first 18-24 months living completely off of one income and saving 100% of the rest. This way, you will save a substantial nest egg early on in your life and let compound interest be your biggest wedding present.

There are two caveats I should mention. The first, if this will put you in a bind to cover your essential bills, just get as close as you can to living off of one income. Live off of 60 or 70% if you can. The second, this is not for saving a down payment on a home. It’s for investing. If you want to buy a home, I would either put off the down payment savings until after the 18-24 months or save extra on the side for it.

How You’ll Benefit

Far too often I hear from people that they will invest “when they can” but right now is not the time. The best thing that young people can do is invest as much as they can early on in their career. I know it isn’t easy. You have student loans, you’re looking for the right job, and you may be saving for your first home.

However, building a nest egg when you are young is the best financial move a young family can make.

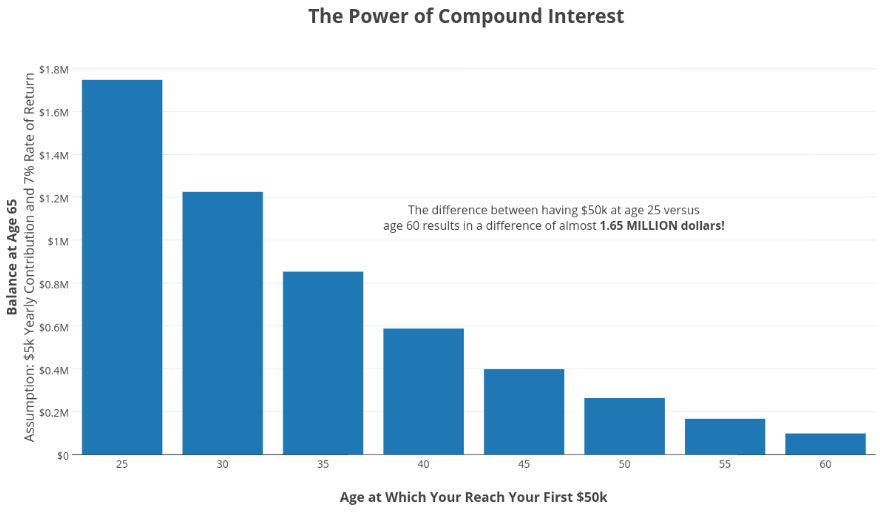

Here is an example, John and Jane “starve and stack” after they are married at 23. By 25 they have saved $50,000. To illustrate how this can change the trajectory of their financial future, I put together the following graph. The assumptions are that they will continue saving $5,000 a year until age 65 and have an average annual return of 7%.

As you can see, the difference is huge. Having $50k at age 25 versus age 60 results in a difference of almost $1.65 MILLION dollars! Starting to save later in life is extremely detrimental to your wealth-building efforts.

Starve. Stack.

Sacrifice some luxuries while you’re young so that you can have financial flexibility later. Make it your goal to pinch pennies until you reach $50,000 or more. It’s not easy, but it’s possible. (Note: if you already have $50k saved on your wedding day, set a higher goal. $50k is just a nice round number that I used here. Set a high goal and crush it.)

“Compound interest is the 8th wonder of the world.” – Albert Einstein

How to Make it Happen

Is saving $50,000 in 18-24 months feasible? You bet it is. Here are a few ways you can make it happen:

Max out work retirement plans. If you have a 401(k) or 403(b) available to you at your employer, you can invest up to $18,000 a year (since you’re under 50, those over 50 could invest up to $24,000). For a married couple that both have workplace plans, that is $36,000 per year! This is not even considering any employer match. This is huge.

Max out IRAs. In an IRA, whether Roth or Traditional, you can invest up to $5,500 a year if you’re under 50. If you both contribute, that’s $11,000 per year. You could max out your work plans and max out Roth IRAs for one year and you’re almost at the magic $50,000 mark. (note: Traditional IRA contributions may not be tax deductible if you’re contributing to a work retirement plan, hence my use of Roth IRAs)

Brokerage Accounts. You could invest outside of retirement plans as well. You won’t be receiving any pre-tax or tax-deferral benefits, but you will have more flexibility to use this money before retirement age. Be aware that these are taxable accounts so it’s important to understand how the assets you hold in these accounts will affect you annually at tax time. There are no limits to how much you can invest in these accounts.

There you have it. I know it won’t be easy but I promise that it will be worth it. It will take discipline and sacrifice. You may have difficulty if you struggle from FOMO and have to turn down luxuries that all your friends are partaking in. However, setting your family up for long-term financial success is better than any short-term luxuries.

Starve and stack!

********

Nick Vail blogs over at Remove the Guesswork, where he helps you to “remove the guesswork” from your financial life. He is also a financial advisor, helping families all over the country pursue financial independence. If you’d like to stop guessing when it comes to your finances and start planning, sign up for his newsletter.

Get blog posts automatically emailed to you!

I love this approach to investing and the magic of compounding interest! It clearly lays out how investing “early and often” (or “early and intensely” in this case) can set you up for financial success down the road and jump start your nest egg. An added benefit is that a strategy like this encourages good savings habits and combats lifestyle inflation.

I like that, “early and intensely”. So true that you will learn good habits and you’ll definitely learn early on how to live (well) below your means.

Ahh, if Mr. ThreeYear had only had the discipline to do this right after we got married! We had the money, we just thought we didn’t! We’re teaching our boys the importance of investing early and being financially disciplined, so hopefully they’ll start off their careers/married lives strong!

It definitely takes discipline, that’s for sure. Maybe your boys can implement this idea!

If you cannot max the 401K, MAX THE MATCH! No throwing away free money.

This is me giving you a digital high-five!

When people talk about saving a huge amount of money, the first question is usually how and when we can do it. One of the most simple answers is always start investing in your retirement accounts as soon as possible.

Mr. FAF and I have also talked about this at length. Once he starts his new job, we will also live on one income and start investing aggressively in our retirement. Thank you for highlighting this great point!

Smart!! And MUCH easier if you plan for it BEFORE it comes, and then of course not get used to the extra $$$ where it changes your lifestyle really fast ;)

Great! Sounds like you are making smart money moves. Good luck with starving and stacking!

That’s what we did too!! When my husband got his new job that doubled his old income, we saved all of his income and lived on mine. We later burned it by buying a used van and a townhouse to welcome baby #2.

Yes! Great advice for us fellow millennials. Invest as early as possible. Luckily we started to dabble with investing in college. Time is our largest asset for our investments.

The earlier the better. You did the right thing!

Excellent advice. I’d suggest the same concept be used for the new college graduate. No rush to buy you own home or even rent alone. “Live like a student” for the first few years, or as long as the fun lasts, and you’ll have the adult salary but student level expenses.

Haha yeah – and not to be confused with “spend all your money until the fun stops” like what I did when I moved to New York City to pretend to be a rock star :) (Although I must admit, I’m glad I did it then cuz now I’m an old man!)

You got it. Don’t fall into a “lifestyle creep” where you always spend more because you start to make more.

Great advice!

Love this idea. Take on lifestyle creep right from the start. Make it a pattern. Awesome idea.

Tom @ HIP

Thanks, Tom!

Lifestyle creeping, or any other creeping, should be frowned upon…

Save early and often! Love it. It’s a concept I’m making sure my three teenagers understand. I ask them all the time, Do you want to be millionaires some day? Well here’s how. Thanks for sharing.

I just said that to someone the other day :) They were debating on whether or not to pick up a new purse and I just asked them if they’d rather have that or stop working forever? I rarely see anyone choosing the former :) (at least in person -who knows if they go out and then just buy it without telling anyone, haha…)

@j money What a coincidence, I was on Facebook the other day talking about buying a $2400 purse for $1100. I didn’t do it.

NICE! Now you know what would even be better? Putting that $1,100 you were about to spend into savings :) Double win!

This is an awesome mindset and approach! Get it done!

Love this idea. Another benefit of living off of one income is that more likely than not you might have to actually live off of one income at some point. Be it a medical issue, job loss or taking care of a baby or parent, things happen in life. It’s nice to know that you would be able to get by on one income if you were forced to.

YES YES YES!!! A built in emergency fund! Or even a “Freedom Fund” if later you decide to nix an entire income on *purpose*.

I like that, “freedom fund”. And great point, Syed. Everyone thinks that emergencies won’t happen to them… until they do.

Oh, I didn’t know there was a name for this! Mr. Picky Pincher and I have been doing this for the past year or so. We live on his income and use my (higher) income to pay off debt. It’s been awesome for paying down our student loans!

That’s awesome! Way to go!

We saved as much as we could when we were both working, but I didn’t keep close track of how much. Once I decided to retire early, we saved and invested all of my income. We did that for a couple of years and found I could stop working without impacting our lifestyle. It was a great test drive.

This truly is one of my favorite money tips! My parents instilled in me long ago 50% of your paycheck (allowance back then) goes into savings the other you can spend. I followed this approach once I started working and after my husband an I were married. Our investment/retirement portfolio is well over 1/2 million at the ripe old age of 37. I cannot begin to stress to my kids how important it is live by this strategy.

You’re a rockstar, Kristin! Your parents coming in clutch with the great advice.

That is a smart approach. Why only do it for a few years? Do it until you reach FIRE. Once you are used to living that way, you most likely won’t want to stop.

Well now you’re just talking crazy ;)

Great advice for younger people. If I had saved a lot more when I was younger the compounded amounts would be five fold by now. If I could just go back and NOT purchase that old Apple IIe I’d be set. Should have bought the stock instead. :)

Haha…. Reminds me of all those old AOL discs flying around back in the day.

Great post, it’s close to one of my posts called “Pay yourself first”.

I remember when I came to the States I couldn’t understand this saying “Pay yourself first”. People around me repeated this mantra almost every day. I nodded my head but had no idea what were they talking about.

Until one day it hit me – YOU HAVE TO PAY YOURSELF FIRST. And the whole concept became really clear – you have to invest and pay yourself even before you get your money.

Like IRS does, but you have to do it better and smarter. And for yourself of course. And since then we’ve started

– maxing out 401(k)s

– Roth IRAs

and investing in taxable accounts.

And the difference is huge. We were doing 6% only in our Roth 401(k)s but after starting maxing out and changing from Roth to Traditional, our take home almost didn’t change.

Hey, people!!!! Remember, YOU HAVE TO PAY YOURSELF FIRST

I’m actually surprised to hear that so many people you know were talking about paying yourself first! Most people I used to talk with in the corporate world only liked talking about where they were spending it all :)

I tend to find wealthy people and ask for their advice ;) And I am not kidding.

This is what we do. Unfortunately we are 38 and 33 years old, so we’re doing it much later in life. On the plus side? These are our peak earning years, so saving a little more than one full salary really makes those savings add up quick. This year we are on track to save somewhere between $160k and $200k – we are doing our very best to make up for our misspent youth.

A tip for those who are above the income limit to contribute to a Roth directly – check if your 401k plan supports the the megabackdoor roth. If it does not, don’t despair. You can do a backdoor Roth.

How is that even possible?? $160,000-$200,000 in ONE YEAR???

My Lord, woman. You are incredible.

My boyfriend and I are talking about something similar if we get married; living off one income and using the other to pay off my $68,000 in student loans. It would perhaps be better to set some of that aside in savings, but the way I look at it is paying off the loans is a guaranteed 6.25% return. Plus he’s 35, I’m 30, so we’d be starting a family sooner rather than later and would like to get rid of as much debt as possible.

The good news is, once we get rid of the student loans, we could continue to live off one income and put more in savings.

It’s the habit that matters most :) Once you get used to living off half you’re free to make whatever moves you want! And each one of those increases your net worth so you’re gonna be setting pretty in no time.

This is so important for millenials to understand! The power of compound interest is so worth the initial sacrifice. I loved your graph!! What a great visual to see what a huge difference it makes.

I don’t travel very much like and my friend said if she had my money, vacations would be all she would do…which is the perfect mindset to utterly fail at wealth building.

Time is so unforgiving and compounding is something you want on your side. I’m not sure why I have to fight with my peers on this…I can travel *after* finding wealth vs the other way around that’s pretty much guaranteed to be more miserable.

If only blogging and personal finance was this popular in 2005 when I was 25…I didn’t get serious about this stuff until 2012 – 8 years later! Think of the compounding.

Great advice and I hope some people start saving based on it!

2005 was right around the time they started to pick up steam.. I think the first one was around 2003, then a good boost around 2005-2007, and then when I came on board in 2008 blogging was blowing up like crazy… You’d think there would be hundreds of thousands of blogs at this point out there, but sadly they die out every day and seems to be around 1,100-1,500 live at any given point in time… (At least from what I’m seeing so far tracking the industry over the past few months :))

I wish I had stumbled upon PF blogs and had the same interest in personal finance in my 20s as I do now. The things I could have done! But I guess better late than never, so the engine is started now and purring along nicely for now.

Ahh, but J! You can also invest $10k a year per person in inflation adjusted federal I-bonds!!! No state or local tax ever and you only pay interest on your earnings when you cash out. Between 401k, IRA, and I-bonds, that’s potentially $67k worth of tax deferred savings!

Me and the wife aren’t quite at $67k per year yet, as that would be 70% of our income, but we’re well on our way. I’m planning on maxing out all three of these options before starting a taxable account. Bonds bore me, but we’re letting my 457, her 403b, and our IRA’s ride 100% equities, so I won’t mind balancing it out with some bonds a few years from now.

Oh really?? I don’t know jaaaack about I-bonds, so very interesting to hear :) If only my kids didn’t suck up so much money from me so I had extra to keep on throwing in!

Hey J! My boyfriend and I just got engaged (which I guess makes him my fiance’) and we plan on doing this. Thanks for the post! It’s an excellent idea!

Beautiful! Your future selves are going to thank you immensely :)

Hey J! Let me share a short story. Five years ago while being on honeymoon there was a wealthy elder couple in our group and we had some conversation about the big questions of life. Some were financially related and they told us their secret to success: “Earn two income and live on a half.” Maybe it is not possible for everyone, but they were the proof that it can be done.

Yessir – gotta love it!

My husband and I started living on just his income when I started grad school at age 24. When I finished my master’s degree at 26 and got a full-time job we just kept living on his salary (and saving mine). We are now both 33 and still doing the same thing to this day!

And I bet by 43 you’ll both be nice and retired, well done :)

Great post. As Spock would say, “Your logic is sound”