Remember when I listed a bunch of things last week that were scarier than Halloween?

Well, here’s another for the list: Losing $60,000 in one month! 😱😱😱

Haha… Okay, well, it would be scary if we actually cashed it all out and called it a day, but since we all know that it’s just one blip on a multi-blip timeline, we just shake it off and keep on looking forward ;) No need to fret if you’ve got DECADES left of compounding to go!

So scary for one month if you’re just looking at that, but not as bad when you zoom out and take a look at the overall picture. Which looks more like this if you’ve been tracking it for over 10 years as I have:

(Look how tiny that dip is there at the end!!)

You also quickly get used to losses since they’re never permanent ;) Particularly those that are by and large outside of your control.

Here’s a look at the biggest “losses” we’ve incurred over the decade – notice the trend?

- Oct, 2018: -$60,000 (market crash)

- Jan, 2016: -$51,000 (market crash + sold house)

- Jun, 2013: -$40,000 (market crash + income crash + cash crash)

- Feb, 2018: -$29,000 (market crash)

- Aug, 2015: -$23,000 (market crash)

- Jun, 2012: -$16,000 (house value ↓ + loss of 2nd income)

- Sep, 2011: -$15,000 (market crash)

- May, 2012: -$14,000 (market crash)

Almost every single dip was due to the markets and not anything I specifically screwed up myself.

Now take a look at the major INCREASES over those same years:

- Dec, 2017: +$93,000 (sold a website)

- Dec, 2016: +$75,000 (new partnership)

- Oct, 2013: +$62,000 (sold some sites)

- Oct, 2011: +$60,000 ($20k inheritance + mad hustlin’)

- Mar, 2016: +$48,000 (market rebound + tax refund + $10k gift)

- Oct, 2015: +$34,000 (market rebound)

- Sep, 2012: +$30,000 (sold a website + mad hustlin’)

- Jun, 2008: +$27,000 (got back all 401(k) money owed to me!)

Unlike the first batch, the majority of these changes were 100% my own doing! And apparently I like to make moves at the end of all the years! Haha…

(You’ll also notice that the ups far outweigh the dips too, coming out $181,047.42 ahead in the end)

So yes, it stings when you have major drops, but do your best to keep it all in perspective! And remember it’s much better to have wealth to begin with to lose than none at all!

As a friend of mine likes to say, you can’t have the ups without the downs. So mourn your “losses” for a hot minute, and then get right back to focusing on what you have control over!

******

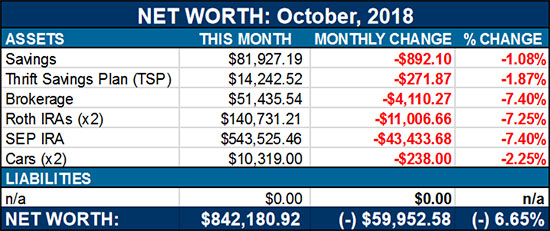

Here’s Net Worth Report #129: $842,180.92

[As always, these reports are shared to better start discussions around money, and to showcase *real life* snapshots which we rarely see in our world… Some months we’re up, and others we’re down (like today! The “Red Wedding” of net worth reports!!), but it all gets shared in hopes it helps you along your own journey. Here’s the breakdown of October’s money…]

******

CASH SAVINGS (-$892.10): This is one of the only times I don’t mind it being red so the entire report stays nice and universal ;) The truth of the matter though is that about $6,000 of owed payments hit me late and thus are being carried over into November instead of October. So technically we’re down, but really it’s just stupid timing.

THRIFT SAVINGS PLAN (TSP) (-$271.87): This one here though is a true loss! And the first actually since my wife began her foray back into full-time employment. Her $500’ish monthly contributions were no match for this market crash!

BROKERAGE (-$4,110.27): A nice hit here as well, almost wiping away *all gains* since we first opened up this account back in May. But we’re still ahead compared to what this $50,000 would have been had it stayed in our savings account accruing miniscule interest!

ROTH IRAs (-$11,006.66): It’s starting to sting a little more, haha…. Almost TWO YEARS of maxing out lost in this round! Pretty wild to think about!

SEP IRA (-$43,433.68): And of course – this is the whopper of them all… An entire salary’s worth right out the door just like that – wow. Hard to look at, but gotta keep those blinders on and keep pushing forward!! Can’t have record breaking highs every month up in here!

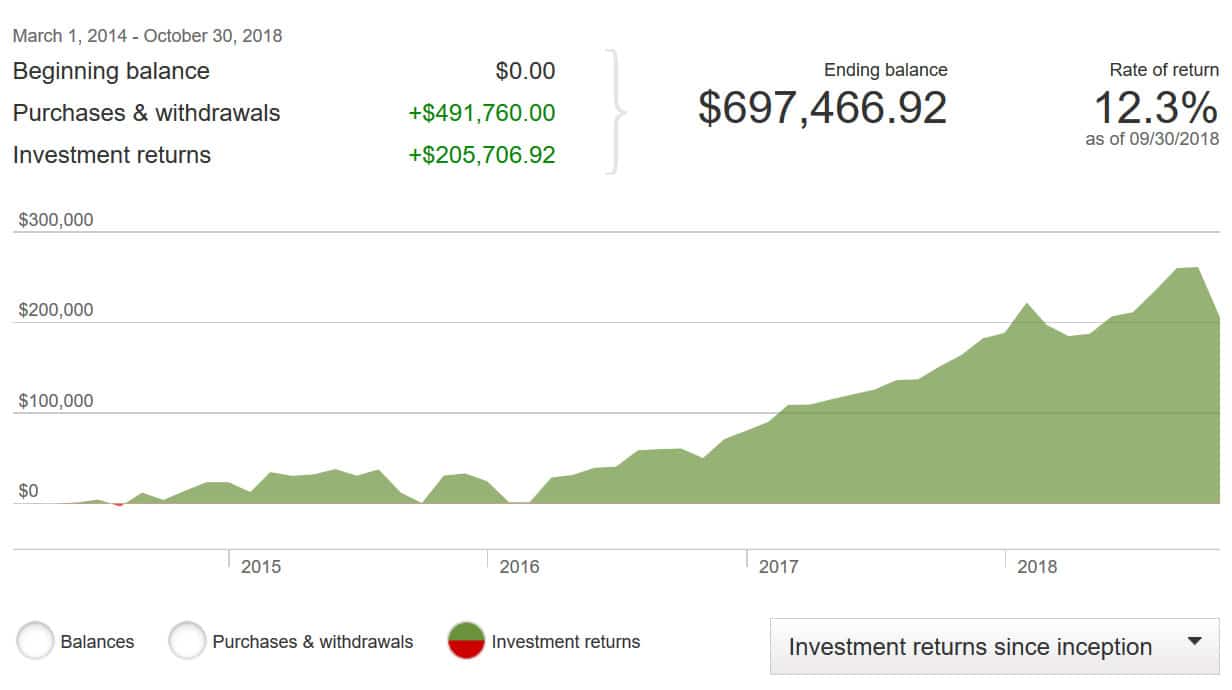

Here’s a snapshot of how our funds at Vanguard have fared over the years. Not sure why the rate of return hasn’t been updated yet, but needless to say we’re still very much ahead of the game:

CAR VALUES (-$238.00): Lastly – the cars. Which of course you expect to devalue :) Here’s a look at the two of them, although the months are getting shorter for when that minivan comes… My wife is starting to get itchy fingers!!

As per Kelly Blue Book:

- Lexus RX350: $8,005.00 (paid off)

- Toyota Corolla: $2,314.00 (paid off)

Total change in net worth this month: (-) $59,952.58

Going in the opposite direction of that Milly, but hey – what are you going to do?

Here’s a look at the past 12 months that helps soften the blow. Still up $150,000 from last year!

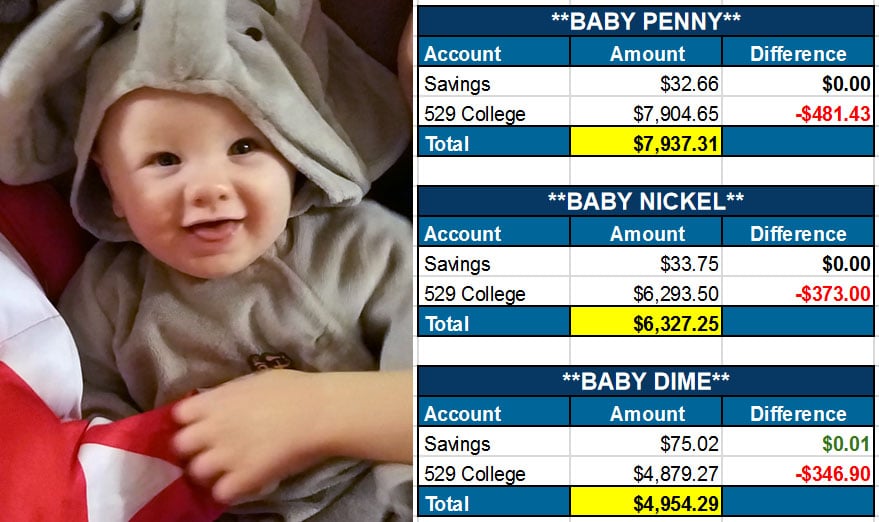

And then here’s how our kids’ net worths are faring too… The markets don’t discriminate! Those meanies!

[That’s a power ranger and the arm of Phineas Flynn hugging the babe, if you were wondering…]

And that’s October! You guys do any better?? Anyone do worse?? (And want to trade? Since it probably means you have more than me? ;))

Some quick tools and spreadsheets can be found below if you’re new to tracking this stuff, but as always – keep paying attention and do your best to stay the course! It gets messy up in here, but it’s a lot worse when you ain’t got much to lose! Keep going strong! 💪💪

Your NWBFF,

![]()

(Net Worth Best Friend Forever)

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Oh, man, the rains of Castamere was echoing in my ears while reading this. Kudos to you, I hope that if I once will be tested the same way I could keep my focus on the long-term… For now, it is not a problem as my net worth is lower than your swing :)

Haha yup, the more you have invested the larger the swing in either direction! Good thing to remember (and account for!) as most people only concentrate on the UPs :)

same situation here. The way I look at it if I had escaped the loss it would mean that my money was invested in a money market account and I would not have had the gains I made the last last year, which more than outweighs the October loss. But I have to admit, it still hurts.

And the gall of Mr Market to pick on little kids. Is nothing sacred?

Right?? ;)

While I always enjoy seeing your monthly net worth report, I really appreciate seeing it this month! I LOVE your “Red Wedding” comparison, and it’s always nice to be reminded these market downturns affect all of us so we’re not alone in our pain. I also had a similar savings situation to you this month with delayed financial obligations coming due, so it felt a bit like salt on the wound combined with the stock market downturn. But when I look at my net worth over time, these are tiny blips in the big picture which is always great perspective to have. Although I’m pretty sure I won’t hit the goal I set for myself at the beginning of the year for total net worth now.

Glad you liked seeing this :) It’s all a part of reality! No one can escape it!

I agree. This was a jaw-dropping post. A loss of $60k! A red wedding indeed. I remember seeing that GoT episode. Like that episode, I had to stop watching my 401(k) balances so closely cause it was just loss after loss. But as you say, that is reality and it can’t be escaped from.

Great post!

Miriam

$60k that’s about how much we dropped too as well. It’s better than at one point $100k which was entertaining Creates some serious buying opportunities at least :))

It sure does!

The downside of having more wealth, it looks a lot scarier on paper when you “lose” money in the stockmarket. Holy cow, that’s a full year salary that disappeared. Ouch.

Ah well, it will bounce back at some point (and then some!)

This is true, the risk % is definitely larger if you have less wealth

Small negative blips every now and then are to be expected. Markets correct on a pretty routine basis. The longer term trend line going up is the important thing to focus on.

It was a red month for me too. The saddest part was seeing my donor-advised fund drop and wondering why I had not donated more when it was up… That will teach me to be more giving in the good times!

I did do some tax loss harvesting this month to the tune of 10k…so there is that. But yes, sit back and enjoy the ride for now I suppose. It helps to have a job (though I am taking 2 months off starting tomorrow!).

Take care J Money.

Hey, you’re donated $$$ will go much farther if you invest it now! :)

Whatcha gonna do on those two months away? Sounds magical!

How did you create that green chart that showed your total return on investments? Is that in Personal Capital or Vanguard? Would love to have another tool to voyeur-out on my money ;)

That was a screenshot right off Vanguard :) It’s in one of the tabs that shows your performance once you’re logged in.

Pretty much everyone’s situation. I’m wondering now if all the PF bloggers will switch from passive indexing to having a robo-adviser manage. After all indexing is only the best “for most” solution when the market is rising. when its in turmoil a more actively managed account could help cap losses. Just a thought. I am 90% vanguard indexed but have been thinking about wealthfront and betterment as alternatives to help curb my losses with the likely massive dip that is coming.

Either way you slice it, its a sad day when one of the best performing areas of your NW is car depreciation.

Haha yeah…

A lot of people will prob start moving around money for sure, for the better or the worse.. I can see doing it with a portion of your $$$, but I don’t mess with the bulk of it anymore because I’ve never been good at timing anything :( As long as it trends up over the years I’m fine with it.

I don’t think your gain vs loss is a fair comparison. In the list of losses 5 out of 8 months are 100% market movements. In the list of increases only one month is 100% market movement, the rest include income events.

The point was to show the extremes on both ends, and how one I had a lot more control over than the other :)

I can really appreciate that perspective. Thank you for all of the motivation over the years!

I got slammed this last quarter as well. Time to hold on for a while. It will come back. I sold some RE this year for a large profit so all is well.

Our net worth dropped $75,000 in October. It’s almost as much as we saved this year. Man, all that hard working saving and investing is gone. Oh well, that’s a day in an investor’s life. You have to deal with the drops too.

Same here. About a $50k drop. Our international allocation has been in bear territory most of the year also also. Staying the course and plowing money into the portfolio as usual. Stay the course everyone. Cheers!

I have a feeling we’ll be seeing a lot of red this week from the net worth reports out there, mine included!

I take it as a good sign, because now that means my accounts have grown large enough that the losses from a bad month outpace the good amount I’m putting in. Like you said I’d rather be in that position than the opposite!

Yup! And it’s great for readers of our blogs too because it shows it’s not always UP UP UP all the time! Which I know can get annoying for some…

I ended the month up 2.1%, only because I got a free car…. without it I would have been down about 2.5%. I just try to remember that my weekly 401k contributions are more valuable than they were last month; more shares for the same amount, what’s not to love? I just need to ignore the big declining number at the bottom for now :)

Yup, pretty much, haha…

How’d you land yourself a new car btw? That’s pretty sweet!

$60k in on month? Holy $hit!!

That is brutal (just like the Red Wedding was!)

But like you said J, its only temporary and is so how the markets fluctuate. Nothing permanent to worry about.

Still, its pretty scary when you loose the equivalent to a years salary in just one month!

I read on Twitter that you anticipated you would be down as much as $70k. Good to see that it was not as bad as that. I am more active in our investments and we were up 18% for the month, but not without quite a bit of research and more than a little stress.

This is one crazy year in the market and not a kind one to index investors. Money invested last January 2nd was worth the same amount in June and is worth about the same amount today after riding it up and back down. The good thing is for those that invest on a regular basis they were able to take advantage of the lows in March and July.

We plan to keep paying down debt to help increase our net worth in this volatile time. Best wishes for a very Green Holiday season!

Up 18% – wow! Good for you! Just goes to show there are lots of alternatives to index investing if it fits your personality/skills/patience :)

Our net worth decreased 3.5% in October. A lot of our net worth is in our house (we put large down payment when we bought it) and we have a lot sitting in cash right now for various reasons so the stock market correction did not impact a good chunk of our portfolio.

https://financialpeacock.com/october-2018-review/

A nice perk of owning a home for sure :) Can always park more money into it and against those loans if you want!

Thanks to you, I started tracking my net worth monthly back at the end of August, and surprisingly, our net worth didn’t go down this month because the estimate of our house’s worth went up quite a bit. As a new reader, I’m sure you’ve posted this answer before, but I noticed you used to put your house estimate on there and don’t anymore. Is that because you own outright? Or are renting? Or did you decide that a house shouldn’t count as an asset towards your net worth? Just curious :)

(And, let’s face it—if we weren’t counting our house’s estimated worth in ours, our net worth would have gone down about the same percentage as yours this month!)

P. S. I was able to complete my challenge to save $1000 in 100 days! (And actually saved $1001, if we’re getting technical!). I’m actually pretty proud of myself, because we were able to do that while paying off all the hospital bills for our son’s birth back in June!

Nicely done!! Whatcha gonna do with that hearty chunk of change? :)

We rent – that’s why no home in the updates anymore :) Sold our house a couple years back and it’s been blissful ever since!

https://budgetsaresexy.com/we-sold-our-house-no-more-mortgages/

During the deep dark days of the recession financial experts jokingly? and said “don’t open your statements as you’ll be sickened by it”. W0e literally piled them up unopened in our lock box & NEVER looked at them for 2 years. Now the market has lost all its’ gains for this year & guess what? Deja vu. NOT looking at it! Like you, we have years left so we’ll just stay put & let it ride till the next upswing. Don’t want to spoil the upcoming holiday season looking at those depressing figures! LOL

Hey – whatever works for you ;) So long as you’re saving more than you’re spending every month!

It’s fun to watch it rise and painful to see it fall. We rolled over our 401ks a month or so ago. I thought about waiting for a market correction, but didn’t. I’ve seen plenty of red over the years, but this blip was the biggest yet at over six figures.

Oh wow – 6 figures, that is a lot! Hopefully we’ll have a whopper of a reverse sometime in between the falls to help keep us sane throughout ;)

I made no predictions but I knew we’d get hit hard enough and in the end it looks like October closed with a similar drop to yours! As much as I was nervous the past twelve months about the onset of the next recession cycle, I am taking the opening round of what may be the start of the recession with a lot more calm than I expected. It’s very wait and see right now and I know better than to panic and sell or move money around right now. I can buy and be patient, so long as we both still have jobs!

Can I have my 50 Grand back from the last post that I blew on coke and hookers in Vegas?

Yeah this past month hurt… losing a years worth of salary in 3 weeks… poof gone.

But that’s alright, keep pumping it in there. Make it work, see how much more we can push in while the knife is falling.

Good on ya for keeping perspective. It’s hard sometimes.

Ha ha! I often say to newbie investors who worry about dipping $600 or so overnight ….. just wait till you have a real sized portfolio! You’d be dead not to feel it.

But hey, great write up. Enjoyed it.

Haha thanks man. You definitely speak the truth!

We just get on with our automatic contributions. It did hurt, but I keep reminding myself we must continue to invest.

This is my first time seeing these net worth posts – which are cool. Just curious though – is there a reason no real estate is listed (but cars are)?

Hey Nate, glad you’re liking it :)

We don’t list real estate because we don’t own any – we prefer to rent.

I do have some other assets that we don’t include in here (such as a coin collection, and this blog), but I prefer to keep it nice and conservative and then add in the other stuff only once it converts to cash. Like how we did it when I sold another site of mine around this time last year – Rockstar Finance.

https://budgetsaresexy.com/end-of-year-net-worth-update-800k/

Ouch!

Took a little hit myself over the last 30 days. But thankfully very contained as I’m so widely diversified. Probably too widely diversified, although up over 8% YTD, so not bad IMO. But still I need to give it a better stress test between now and year end.

Rooting for you to hit that 1m$ mark soon!

Wow thats more than what some people make in a year. Prayerfully the market will eventually correct itself.

Yea last month was a rough one. I just finished my October calculations and I lost as I’m sure almost everyone did.

On the positive, since we are all in it for the long haul I actually enjoy seeing these dips every so often because not only will it go back up but it means the market is on sale!!

When you look at your chart on your millionaire journey, you can see a lot of little divots. They seem like big numbers if you look closely. When you step back and look at the big picture, they are only little divots.

Like the book says “Don’t sweat the small stuff, and it’s all small stuff.”

Dr. Cory S. Fawcett

Prescription for Financial Success

Haha… how true that is.

My wife and my retirement accounts went down slightly over $10 grand in October – more than our income for the same period. Add to the fact we bought a minivan, our net worth went down $17 grand (well, I’m only counting the loan for the minivan, I guess it’s value surpasses the amount of the loan since we put close to 50% down).

But I’ve been tracking debt + investments for almost two years now, and we’ve halved our debt and doubled out investments since then, so it’s all good.

I would say so! How long you have left until all the debt’s gone now?

I always enjoy your net worth updates and this one was no exception. I really appreciate your positive outlook and perspective. Here’s to hoping for a sea of green in your next report.

You too, sir!

So glad you’re enjoying them!

Ouch!

6.65% has to hurt.

I was down in Oct 5.7%, wiping out all the year-to-date gains. That tells me one thing. No, not that I’m smarter, a better investor, or even luckier. I’d bet that your investment mix is one with more stock than my mix. As a retiree, I’m in an 80/20 mix. If we go into another crash, I wanted to have about 5 years worth of spending without having to sell low. The downside is that with rates so low, I’m not going go see the high returns you will in up markets.

Always interesting to have a peek at someone else’s balance sheet.

And I’m reminded of the burden you don’t have. No house means no property tax ($18K for me) insurance (another $4K) or ongoing routine maintenance. The mortgage is the least of it all.

Be well!

Haha… Indeed on that house stuff ;) But we’ll see how long it lasts – my wife just yesterday told me how much she’s tired of moving around and wants to finally buy a house again! I’m angling for one more move of renting while we *look* for the perfect house, but not entirely sure I’m going to win that battle, haha…. It’s getting harder to move with a billion kids in tow.

(and yup – I’m 100% in stocks so your 20% mix is definitely stopping the bleeding on your end)

Lost about $30K…and I was in the middle of a rollover when one of the dips occurred so I lost less than I should have. Amusing timing.

Also amusing: my portfolio rebalanced itself. Not in the way I would have preferred…but I don’t have to bother anymore…

Lucky timing indeed! :)

This has got to be my favorite post of yours! Love it. So informative and so fun.

xoxo,

Greenbacks Magnet

haha really?? it is NOT a favorite of mine! lolol…. but it is the truth, so that always has to come out ;)

thanks for stopping by – always love your vibes around here.